Wesfarmers Outlines Growth Agenda Spanning AI, Lithium and Retail at Strategy Day

Wesfarmers outlines accelerated growth and productivity agenda at 2026 Strategy Briefing

In its 2026 Strategy Briefing Day presented to investors on 10 June 2026, Wesfarmers (ASX: WES) articulated three core messages under Managing Director Rob Scott: accelerating growth and productivity execution, maintaining portfolio resilience through the cycle, and preserving balance sheet flexibility for strategic capital deployment. The Group reinforced its track record as a long-term wealth compounder, with total shareholder returns of +19.0% per annum since listing in November 1984 versus +10.4% per annum for the All Ordinaries Accumulation Index. Over the past decade, Wesfarmers has delivered +15.8% per annum compared to +9.2% per annum for the index, while return on equity has expanded to 32.7% from 9.6% in 2016. The company has distributed $42 billion+ to shareholders over the last 10 years, comprising $22.8 billion in fully-franked dividends, $14.6 billion in Coles demerger proceeds, and $5.3 billion in capital returns and special dividends.

The briefing covered strategic updates from Wesfarmers’ major retail divisions — Bunnings, Kmart Group, and Officeworks — alongside its industrial operations (WesCEF) and health businesses.

When big ASX news breaks, our subscribers know first

What is a strategy briefing day?

A strategy briefing day is an investor event where company management presents detailed updates on business performance, strategic priorities, and future plans. These events provide deeper insight than standard quarterly results, allowing management to articulate multi-year vision and respond to investor questions. Wesfarmers’ briefing covered detailed presentations from divisional managing directors across its major retail divisions, industrial operations, and health businesses, offering a comprehensive view of the Group’s strategic direction.

Strategy briefings signal management confidence and provide forward-looking information that shapes investment theses beyond backward-looking financials. For investors, these events offer material insight into capital allocation priorities, market positioning, and growth initiatives that drive long-term returns.

Bunnings maintains competitive moat while scaling emerging channels

Managing Director Michael Schneider outlined Bunnings’ strategic pillars underpinning its market leadership: lowest prices, widest range, and best experience. The division has expanded its addressable market from traditional hardware to Home, Living & Commercial (approximately $113.5 billion), supported by industry-leading operational metrics.

Bunnings delivered a 70.8% return on capital on a rolling 12-month basis to 1H26, with a Net Promoter Score exceeding 60. The business operates 353 stores across Australia and New Zealand with approximately 55,000 team members and maintains a pipeline of over 100 property projects to FY30. Bunnings has driven sales growth approximately 3.9 times faster than retail space growth over the last five years.

The division’s marketplace platform now features more than approximately 300,000 SKUs across 600+ sellers, with gross merchandise value growing at a +49% five-year CAGR. The platform has expanded into Trade Marketplace, launched in Q2 FY26 with approximately 4,600 commercially focused SKUs across Kitchen Appliances, Furniture and Cleaning Equipment.

The Blackwoods and Workwear Group transition into Bunnings, effective 1 July 2026, extends this commercial push further, consolidating industrial supply and workwear distribution into Bunnings’ trade infrastructure to target small and medium-sized business customers.

Bunnings introduced agentic commerce through “Buddy,” powered by Google Gemini, delivering materially higher average order values relative to non-AI enabled sales. The division has deployed over 3 million electronic shelf labels to support lowest prices and productivity.

| Metric | Value |

|---|---|

| Return on capital (R12) | 70.8% |

| Stores (AU & NZ) | 353 |

| Team members | c.55,000 |

| Marketplace SKUs | c.300,000 |

| Marketplace sellers | 600+ |

Kmart Group prioritises price leadership through operational digitisation

Managing Director Aleksandra Spaseska outlined Kmart’s execution of value-creating strategies, emphasising the division’s market positioning. 84% of Australians live within 10km of Kmart or Target, providing significant geographic coverage and customer access.

Digitisation progress includes over 700 million web sessions per annum and over 1.6 million monthly active app users who spend 2.4 times the average customer. RFID at source now covers over 60% of apparel purchase order volumes, enabling future end-to-end stock visibility.

The division has 16 stores trading in the new Kmart Plan C+ format, scaling to 40 by the end of FY27. A Next Gen omnichannel fulfilment centre is under construction to enhance fulfilment capabilities.

Kmart’s Anko international expansion has delivered 5 stores operating in the Philippines, with 5 additional stores planned by the end of FY27. The division launched a third-party marketplace and agentic commerce assistant “Joy” in May 2026 to drive digital engagement and conversion.

Kmart’s strategic priorities include:

- Growing addressable market through category expansion

- Store format innovation (Plan C+)

- Supply chain transformation

- Digital acceleration and app engagement

- Anko international expansion

Officeworks embarks on multi-year transformation with five strategic pillars

Managing Director John Gualtieri outlined Officeworks’ strategic framework for long-term profitable growth, centred on five priorities:

- Becoming a low-cost operator

- Resetting merchandise and value fundamentals

- Creating inspiring omnichannel experiences

- Winning as the first choice for complete tech solutions

- Being the market leader in B2B and Education

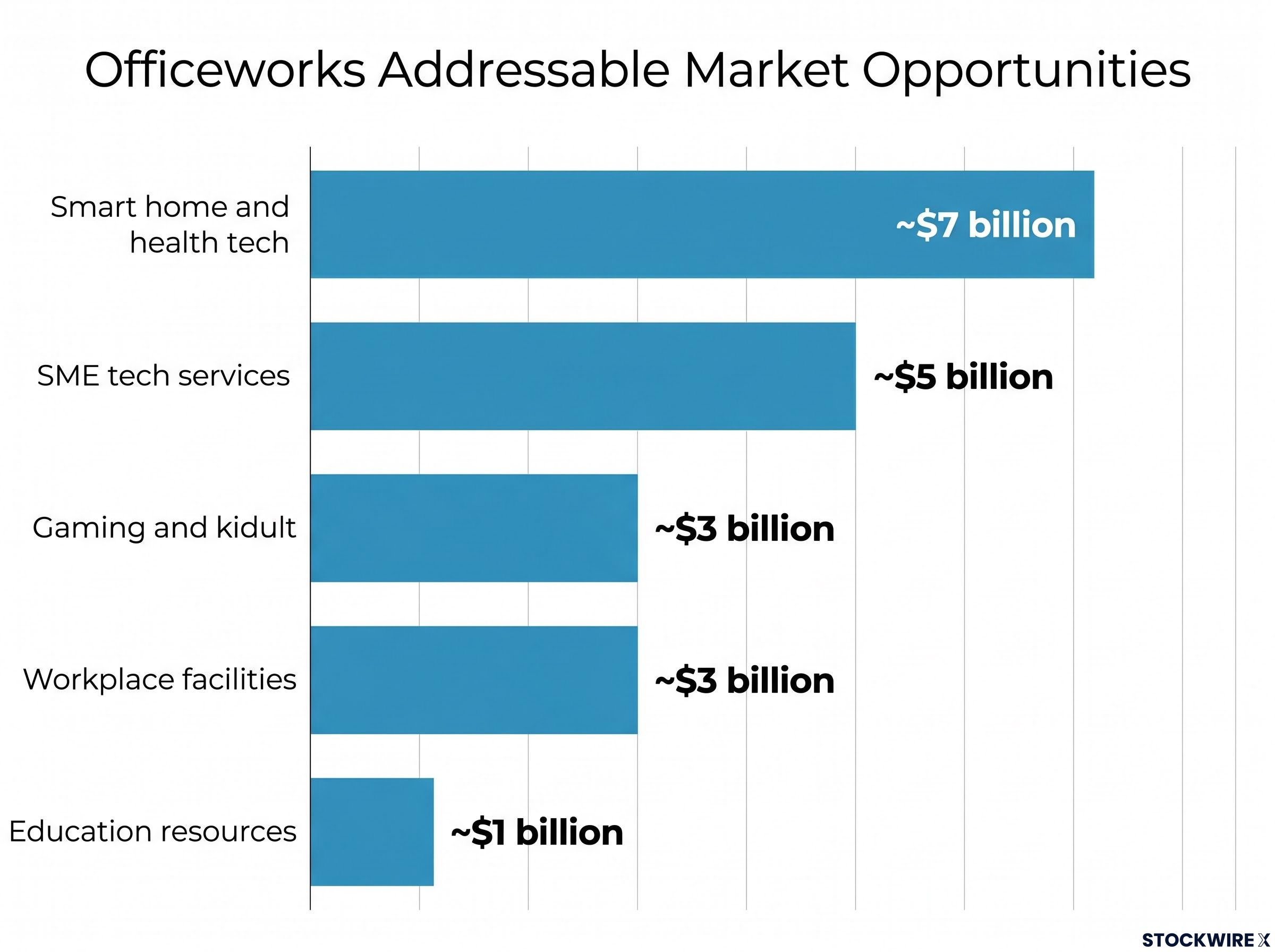

The division identified addressable market opportunities across multiple segments: smart home and health tech (approximately $7 billion), gaming and kidult (approximately $3 billion), workplace facilities (approximately $3 billion), education resources (approximately $1 billion), and SME tech services (approximately $5 billion).

Officeworks planned 3 net new stores for FY27 and has an automated Queensland omnichannel facility under construction to support improved fulfilment capabilities and customer immediacy.

WesCEF advances Mt Holland lithium project toward expansion decision

Managing Director Aaron Hood updated investors on progress at the Covalent Lithium project, with nameplate spodumene production achieved in FY26. First lithium hydroxide production was achieved in FY26, with refinery ramp-up the key focus for FY27.

WesCEF’s share of spodumene concentrate production in FY27 is expected to be approximately 190,000 tonnes, with production evenly allocated between refinery feedstock and sales. 60,000 tonnes have been contracted since January for FY27 sales. Realised pricing on 2H FY26 sales was largely set during mid-FY26 at approximately US$1,500 per tonne SC6.

The expansion project targeting Final Investment Decision in 1H FY27 includes concentrator expansion to double nameplate production to approximately 760,000 tonnes per annum (WesCEF’s 50% share approximately 380,000 tonnes per annum). Construction is targeted for completion in CY29 and includes an ore sorter to increase recoverable lithium volume.

WesCEF announced the appointment of Stuart Macnaughton as Covalent Lithium CEO and completed a gold tenement sale at Mt Holland, realising value in a high gold price environment.

Lithium represents a significant new earnings stream for WesCEF, with the concentrator expansion targeted to double nameplate spodumene concentrate production to approximately 760,000 tonnes per annum (WesCEF’s 50% share approximately 380,000 tonnes per annum) and supporting the division’s strategic growth objectives.

Other WesCEF growth projects delivering capacity expansion

WesCEF completed the Nitric Acid Ammonium Nitrate debottlenecking in 1H FY26, increasing capacity by approximately 40,000 tonnes per annum to approximately 865,000 tonnes per annum, with potential for an additional 80,000 tonnes per annum. The division highlighted sodium cyanide expansion, with the first phase delivered in 2H FY26. Total capacity increased by approximately 35,000 tonnes per annum to approximately 130,000 tonnes per annum, positioning Australian Gold Reagents as one of the largest global producers.

The sodium cyanide project was delivered on budget, on schedule, and without any recordable injuries. The expansion includes a new incinerator to reduce emissions intensity.

Higher ammonia prices translate to higher earnings for manufactured tonnes, with the timing lag of sales contracts pushing earnings from Q4 FY26 to Q1 FY27.

Industry-Leading Availability

WesCEF’s ammonium nitrate availability consistently exceeds 90%, with production regularly exceeding 100% of nameplate capacity. This operational excellence provides earnings resilience relative to competitors and supports the division’s capacity expansion strategy.

Wesfarmers Health targets multi-year transformation in growing market

Managing Director Emily Amos outlined the health division’s transformation priorities:

- Growing share and scale in Consumer

- Investing in unique loyalty, data and digital assets

- Improving Wholesale performance and operating efficiency

Priceline was highlighted as Australia’s largest health and beauty loyalty program. The division completed 24 new sites and 23 refurbishments in FY26. The atomica launch introduced a new destination for aspirational and affordable beauty, achieving a Net Promoter Score exceeding +90 in pilot stores.

Private label expansion now includes over 1,000 SKUs in Priceline Retail, over 400 SKUs in Wholesale, and over 100 SKUs in AestheticsRX. The division launched a new app in FY26 and completed DC automation investments in Brisbane and Cairns, with Adelaide and Perth facilities in development.

The next major ASX story will hit our subscribers first

Strong balance sheet provides flexibility for continued capital deployment

The Group’s financial position supports both investment and shareholder returns, with Debt/EBITDA of 1.9 times and a weighted average cost of debt of 3.56%. Wesfarmers maintains flexibility to deploy capital across its existing portfolio, adjacent opportunities, and value-accretive transactions.

AI and digital investments underpin productivity across all divisions, supported by strategic partnerships with leading AI organisations. The Group’s omnichannel scale includes over $35 billion in retail sales, over $3.3 billion in online retail sales, 1,900+ stores, and approximately 12 million customers in the shared data asset.

Balance sheet strength combined with demonstrated capital allocation discipline positions Wesfarmers to pursue growth while maintaining shareholder returns. The company’s track record of distributing $42 billion+ to shareholders over the past decade demonstrates its commitment to delivering satisfactory returns alongside strategic investment in growth platforms.

Don’t Miss the Next Consumer Breakout

Join 20,000+ investors getting FREE breaking ASX news delivered to your inbox within minutes, complete with in-depth analysis. Click the “Free Alerts” button at Big News Blast to start receiving alerts the moment market-moving news breaks across Consumer, Tech, Healthcare, Finance and Manufacturing sectors.