Elanor Investors completes $125 million Rockworth recapitalisation

In its June 2026 market update presentation, Elanor Investors Group (ASX: ENN) detailed the completion of a $125 million balance sheet recapitalisation with Rockworth Capital Partners on 17 April 2026. Management outlined that the transaction significantly reduces the Group’s cost of capital and stabilises the balance sheet after a period of financial restructuring.

The presentation revealed that recapitalisation proceeds were deployed to repay the existing Keyview senior facility in full, redeem FIIG Notes in full, repay certain commercial arrangements, and provide additional working capital. Management stated the transaction establishes a foundation for executing a capital-led domestic and Pan-Asian growth strategy. The Group voluntarily repaid an additional $4 million of Loan Notes on 1 May 2026, further reducing debt obligations.

The recapitalisation represents a balance sheet transformation that removes immediate financial pressure and repositions the Group for growth-focused operations rather than crisis management.

When big ASX news breaks, our subscribers know first

Understanding balance sheet recapitalisations

A balance sheet recapitalisation involves restructuring a company’s funding sources by replacing existing debt with new capital instruments, typically to reduce borrowing costs and improve financial flexibility. Rather than raising equity capital immediately—which would dilute existing shareholders—a recapitalisation substitutes expensive debt with lower-cost financing structures.

For Elanor specifically, the transaction replaced high-cost facilities with a combination of secured loan notes, subordinated perpetual notes, and warrants. This layered capital structure creates different classes of obligations, each with distinct interest rates, repayment terms, and security rankings. The secured loan notes sit at the top of the capital structure with preferential repayment rights, while perpetual notes are subordinated and have no fixed maturity.

The significance for investors is that replacing high-rate debt with lower-rate instruments improves cash flow available for operations and debt reduction. The warrant component represents potential future dilution if exercised, but does not require immediate equity issuance. This structure allows the company to stabilise financially while preserving the option to repay debt through asset sales rather than equity raises.

Key financing terms from the Rockworth transaction

The presentation outlined a three-instrument structure designed to balance immediate debt reduction with flexible long-term capital. Management noted that Rockworth retains the right to nominate one director under the existing Strategic Alliance Agreement, though currently no board representative has been appointed.

| Instrument | Amount | Interest Rate | Term | Key Feature |

|---|---|---|---|---|

| Senior Loan Notes | $70.0 million | 7% p.a. | 24 months + 12-month extension | Secured with relevant covenants |

| Perpetual Notes | $55.0 million | 9% p.a. (years 1-3), then 11% | No fixed maturity | Subordinated, distributions and redemption at issuer discretion |

| Warrants | 30.0 million | $0.01 exercise price | 30 June 2028 expiry | Not exercisable within first 6 months |

The 7% senior rate and 9% initial perpetual rate represent material improvement versus prior facility costs. The senior loan notes provide 24 months of committed funding with a 12-month extension option, while the perpetual notes have no fixed maturity and allow the issuer discretion on distributions and redemption. The warrant structure provides Rockworth with 30 million warrants exercisable at $0.01 per security from six months after issue until 30 June 2028.

This financing structure directly benefits cash flow by reducing the weighted average cost of capital across the Group’s debt portfolio.

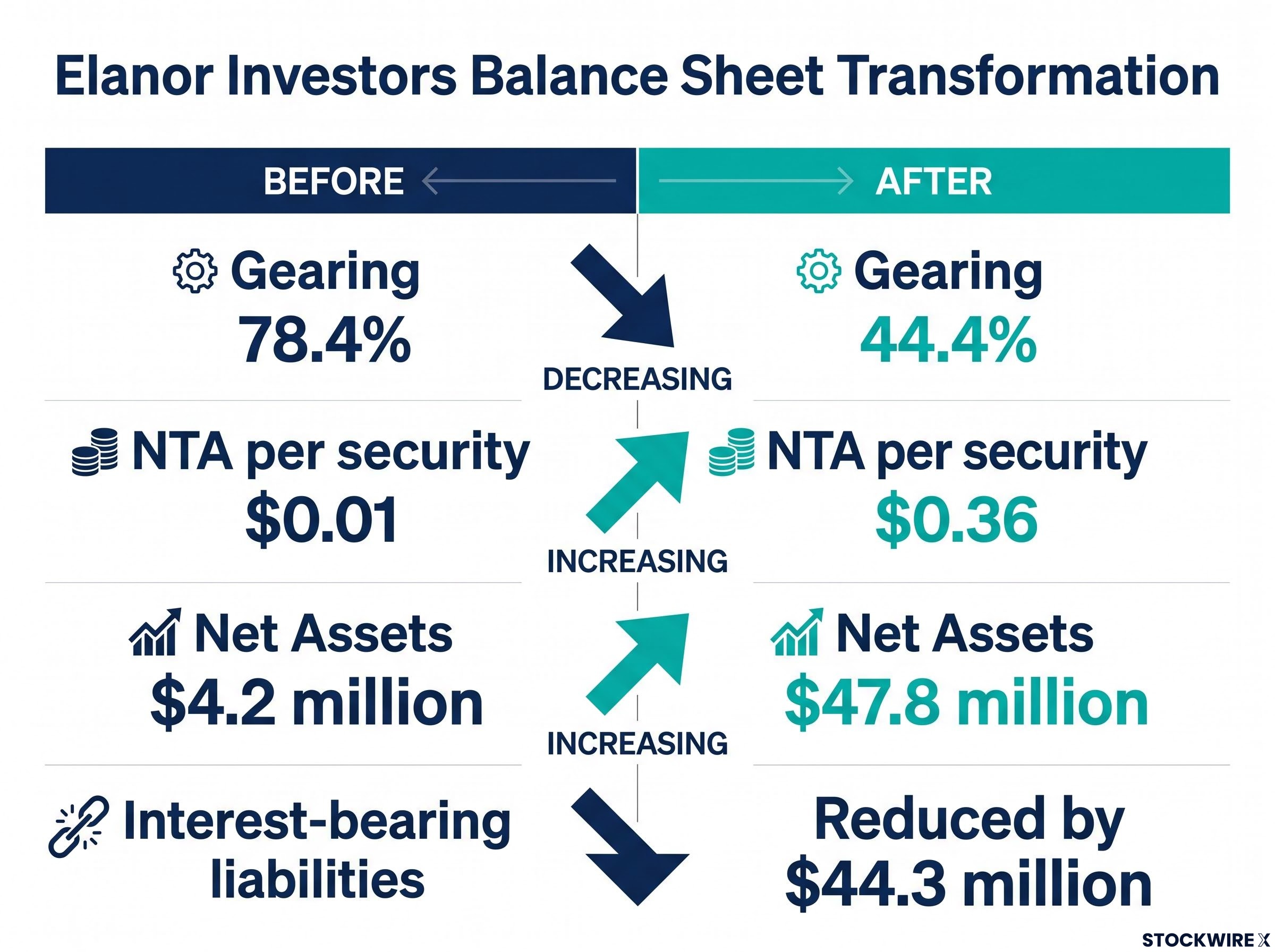

Balance sheet transformation delivers dramatic gearing reduction

Management highlighted a substantial improvement in the Group’s financial position post-recapitalisation. Gearing—defined as gross borrowings less cash divided by total tangible assets less cash—fell from 78.4% to 44.4%, representing a halving of leverage ratios. Net tangible assets (NTA) per security improved from $0.01 to $0.36, or $0.30 on a diluted basis including the 30 million warrants.

Net assets increased from $4.2 million to $47.8 million following the transaction. The presentation noted that 7.9 million securities were clawed back and cancelled on 23 April 2026 as the final stage of unwinding the Challenger mandate. Interest-bearing liabilities reduced by $44.3 million through the combination of debt repayments from transaction proceeds and asset sale receipts.

The update stated that securityholder distributions remain suspended until certain Loan Note financial covenants are met and Perpetual Notes distributions are paid. This prioritises debt reduction and covenant compliance over immediate shareholder returns.

The gearing halving removes balance sheet stress that had compressed valuation multiples and constrained operational flexibility. The improved NTA provides a more stable equity base from which to rebuild the platform.

Asset realisations reshape $1.9 billion AUM platform

The presentation detailed approximately $880 million in assets under management (AUM) transacted since December 2025 across three major transactions. Management outlined that these realisations released capital for deleveraging while refocusing the platform on core sectors.

Following Elanor Commercial Fund Property (ECF) securityholder approval on 30 January 2026, Elanor was replaced as Responsible Entity effective 4 February 2026. The company received $8.5 million in compensation for termination of the investment management and property management agreements, paid on 5 February 2026.

The Group’s co-investment in Elanor Wildlife Park Fund (EWPF), together with management rights and related receivables, was sold in February 2026 for $13.0 million. In April 2026, ADIC mandate assets Paradise Centre and Novotel Surfers Paradise were divested for approximately $352 million as part of mandate capital management strategies. The presentation noted that ADIC continues to retain its holding in Elanor securities.

Current AUM stands at $1,855 million as at 31 May 2026, distributed across five core sectors:

- Retail: $910 million

- Office: $323 million

- Healthcare: $274 million

- Hotels, Tourism & Leisure: $270 million

- Industrial: $81 million

The asset realisations released capital to deleverage whilst refocusing the platform on core sectors with clearer growth pathways.

Strategic growth priorities and leadership renewal

Management outlined the Group’s transition to a capital-light, scalable institutional-grade funds management platform. The presentation detailed a dual capital strategy combining re-engagement with domestic institutional investors alongside targeted Pan-Asian capital inflows through the Rockworth partnership.

The update announced CEO David McNamara’s appointment to drive the growth strategy, whilst Su Kiat Lim stepped down from the board. Corporate governance was strengthened through implementation of an independent managed fund trustee board. In April 2026, ASIC granted a new AFSL to Group Funds Management Limited.

David McNamara’s appointment brings more than 34 years of institutional property and funds management experience from Vicinity Centres and Lendlease, a background suited to rebuilding institutional investor relationships as Elanor pursues domestic and Pan-Asian capital inflows.

The presentation confirmed that the Firmus Capital acquisition is not progressing, as announced on 29 May 2026, and therefore no consideration securities will be issued. Near-term focus areas include operating cash flow management, asset realisations, debt reduction, and AUM growth initiatives.

The Firmus Capital acquisition lapsing after the 31 May 2026 sunset date removes a near-term source of Pan-Asian AUM growth, though Rockworth’s warrant position and board nomination rights keep the strategic alliance firmly in place as the vehicle for future offshore capital partnerships.

The presentation stated that the Group’s balanced short to medium term investment strategy will focus on deploying capital across core real estate sectors in Australia and New Zealand through a combination of domestic institutional and Pan-Asian capital partnerships, leveraging the Group’s repositioning as a capital light, scalable institutional funds management platform.

Leadership renewal and governance strengthening signal commitment to rebuilding market credibility alongside the financial restructuring.

Cash flow demonstrates operational stabilisation

The presentation reported $5.8 million in positive operating cash flow for Q3 FY26, with year-to-date FY26 operating cash flow of $8.7 million positive. Receipts included the $8.5 million ECF termination compensation received on 5 February 2026.

Investing activities generated $14.2 million in Q3 from EWPF sale proceeds of $13.0 million, whilst financing activities consumed $21.3 million primarily through debt repayments. Cash at the end of Q3 stood at $4.1 million, improving to a pro forma $14.8 million post-recapitalisation after including the Rockworth transaction proceeds.

The presentation outlined near-term priorities centred on operating cash flow management, asset realisations releasing balance sheet capital, debt and Perpetual Note reduction, and strategic AUM growth initiatives through the Rockworth alliance.

Positive operating cash flow supports the stabilisation narrative and provides a foundation for organic debt reduction alongside asset sales.

Receivables recovery pathway

Management detailed total receivables of $36.3 million on a pro forma basis, concentrated across managed fund exposures linked to planned asset realisation programmes. The presentation stated that EHAF receivables of $16.1 million are expected to be recovered through a combination of planned asset realisations and improved Fund performance focusing on a core portfolio of hotel assets.

Other syndicate receivables—Belconnen Markets $4.8 million, Fairfield Centre $4.1 million, Hunters Plaza $3.4 million—form part of divestment strategies. The update noted that other managed fund trade debtors of $2.0 million are expected to be recoverable through the ordinary course of business.

Financial assets include subordinated loans totalling $11.6 million, comprising $9.3 million relating to Belconnen Markets Syndicate and $2.3 million deferred settlement from the Bluewater Square sale (September 2025), to be realised 12 months post-settlement.

Management cautioned that carrying values of financial assets subject to potential asset realisation may vary based on final divestment outcomes.

Recovery of managed fund receivables represents additional balance sheet upside as asset realisations progress, though final recovery values depend on execution of divestment programmes within underlying funds.

Get Breaking Consumer News Before the Market Reacts

Join 20,000+ investors receiving FREE ASX consumer sector alerts delivered within minutes of release, complete with in-depth analysis. Click the “Free Alerts” button at StockWire X to access breaking news and expert coverage the moment market-moving announcements hit the ASX.