Orthocell Ltd Posts Record A$13.2M FY26 Revenue as US Adoption Builds

Record FY26 revenue and building US momentum

In its Q4 FY26 investor presentation, released on 14 July 2026, Orthocell reported record full-year revenue and accelerating US commercial traction for its flagship nerve-repair product, Remplir™.

The Australian medical technology company posted FY26 revenue of A$13.2M, up 44% year-on-year, with Q4 FY26 revenue of A$3.8M representing a 20% increase on the prior quarter.

Management highlighted a strong balance sheet, with A$44.1M in funds available and approximately 4.6 years of cash runway. Combined with accelerating US adoption, this positioning underpins the company’s stated path toward cash breakeven.

When big ASX news breaks, our subscribers know first

Q4 FY26 performance across six key metrics

The presentation detailed six headline metrics, extending what management described as a three-year track record of consistent commercial growth. Remplir US sales contributed the vast majority of the 44% year-on-year revenue uplift.

| Metric | Result | Growth | Notes |

|---|---|---|---|

| FY26 Revenue | A$13.2M | +44% YoY | Record full-year result |

| Q4 FY26 Revenue | A$3.8M | +20% QoQ | Record quarterly revenue |

| Remplir US Revenue (Q4) | A$0.33M | +10% QoQ | A$0.92M since launch |

| Cumulative US Hospitals | 70 | +27% QoQ | 100+ VAC approvals in process |

| Cumulative US Surgeons | 76 | +55% QoQ | Exceeding initial expectations |

| Funds Available | A$44.1M | 4.6yr runway | No financial debt |

The breadth of growth across revenue, hospital access and surgeon adoption reflects execution across all key drivers within the quarter.

Understanding the nerve repair opportunity

Remplir™ is a collagen nerve-repair product used in peripheral nerve repair procedures.

Remplir clinical outcomes from an expanded 66-patient real-world study recorded an 89.7% overall treatment success rate across 78 nerve repair procedures, with zero post-treatment complications reported across the entire cohort.

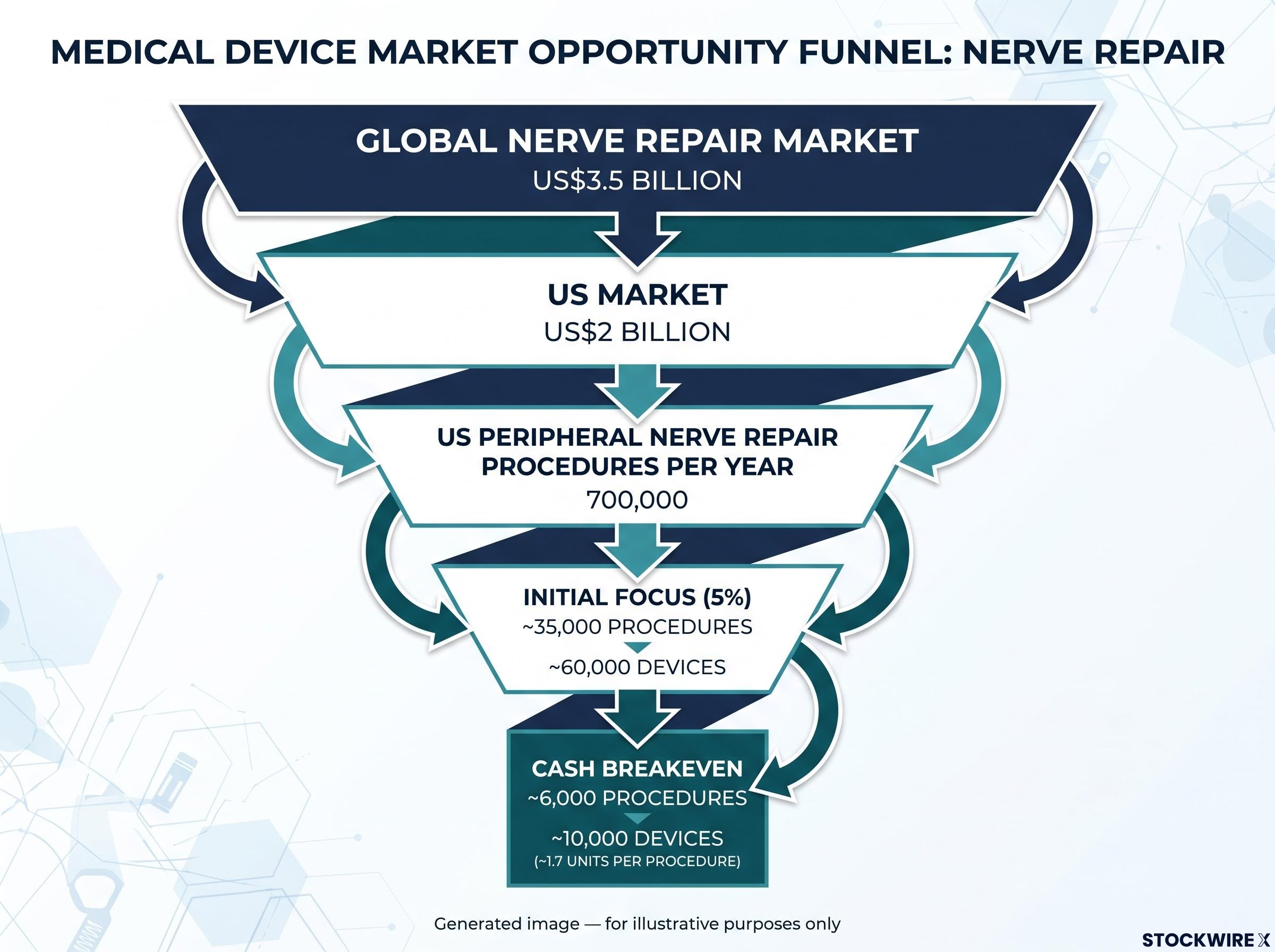

Management framed the commercial opportunity around a large and established market. According to the presentation, the global nerve repair market is estimated at US$3.5 billion, with the US market alone valued at approximately US$2 billion.

The company outlined the following market-sizing figures:

-

Approximately 700,000 US peripheral nerve repair procedures per year

-

Targeting 10% of the market (initial focus of 5%, equating to ~35,000 procedures / ~60,000 devices)

-

Cash breakeven at ~6,000 procedures / ~10,000 devices (~1.7 units per procedure)

The significance for investors lies in the leverage: capturing even a modest share of this large market could drive a material revenue step-up, with breakeven framed as a near-term operational target.

US commercial momentum builds since June 2025 launch

A standout of the presentation was the early traction achieved since the first US sale on 26 June 2025. Management noted that commercialisation in the US continues to track ahead of expectations.

Distributor coverage now spans 18 distributors across 20+ states, reaching approximately 50% of the US population. According to the presentation, this exceeded the company’s target by 25%.

The US military hospital network representing 51 DoD facilities and 170 VA medical centres was approved as a procurement channel for Remplir earlier in 2026, more than doubling the addressable US hospital footprint beyond the civilian rollout covered in this presentation.

The company highlighted the following cumulative momentum metrics, measured as compound quarterly growth rates (CQGR) over five quarters rather than single-quarter growth:

-

Hospitals: 70 cumulative (+189% CQGR), with 100+ VAC approvals submitted, in process or approved

-

Surgeons: 76 cumulative (+195% CQGR)

-

Unit sales: 119 in Q4 (+230% CQGR)

Rapid distributor expansion and surgeon adoption serve as leading indicators for the anticipated US revenue uplift management flagged in upcoming quarters.

Financial position and cash runway

Chief Financial Officer Jim Piper framed the balance sheet as sufficient to fund commercialisation through to anticipated breakeven, with no additional funding required.

Funds available stood at A$44.1M as at 30 June 2026, comprising A$9.4M in cash and cash equivalents plus A$34.7M in security and term deposits with maturities ranging from 3 to 12 months. The company reported no long-term secured debt and no royalty liabilities.

Normalised operating cash burn held steady quarter-on-quarter at A$2.4M in Q4 FY26, compared with A$2.5M in Q3 FY26. Capital expenditure is funding manufacturing capacity expansion, described as on time and on budget, alongside an increased equity position in Marine Biomedical.

CFO Commentary

Sustainable cash reserves are in place to fund the commercialisation of Remplir™ and support the business to cash flow breakeven, with no additional funding required.

FY27 targets and upcoming catalysts

Management outlined a forward roadmap targeting continued US penetration through FY27. The company anticipates a material uplift in US revenue in upcoming quarters as commercial coverage builds.

The FY27 US commercialisation targets include:

-

Distributor coverage of 80% of the US population (30+ states)

-

Cumulative hospitals of 100–150

-

Cumulative surgeons of 150–200

The presentation flagged several near-term catalysts, all anticipated in 2H CY26, with the company noting timelines may be subject to change due to circumstances outside its control:

-

Initial prostate (nerve-sparing prostate cancer surgery) patient data

-

EU and UK market clearance

-

SmrtWrap™ tendon repair US FDA pre-submission

Recent achievements included the appointment of a Thai distributor for Remplir, strengthening the company’s Asia-Pacific footprint, and a humanitarian initiative delivering Remplir to victims of war in Ukraine. The company has also appointed an exclusive distributor in the UK.

The next major ASX story will hit our subscribers first

Why the growth story matters for investors

Orthocell’s July 2026 presentation combined a record revenue base with accelerating US adoption and a balance sheet management describes as sufficient to reach anticipated breakeven without additional funding.

The near-term catalysts flagged for 2H CY26, spanning prostate surgery data, EU and UK clearance, and the SmrtWrap™ regulatory pathway, add multiple potential inflection points. With breakeven targeted at a small share of a US$3.5 billion global market, the operating leverage embedded in continued US penetration remains central to the growth thesis.

Don’t Miss the Next Healthcare Breakout

Big News Blast delivers FREE breaking ASX healthcare news directly to your inbox within minutes of release, complete with in-depth analysis. Join 20,000+ subscribers already staying ahead of the market. Click the “Free Alerts” button at Big News Blast to get the next market-moving announcement the moment it drops.