SEC Moves to End Mandatory Quarterly Reporting After 50 Years

13 hrs ago

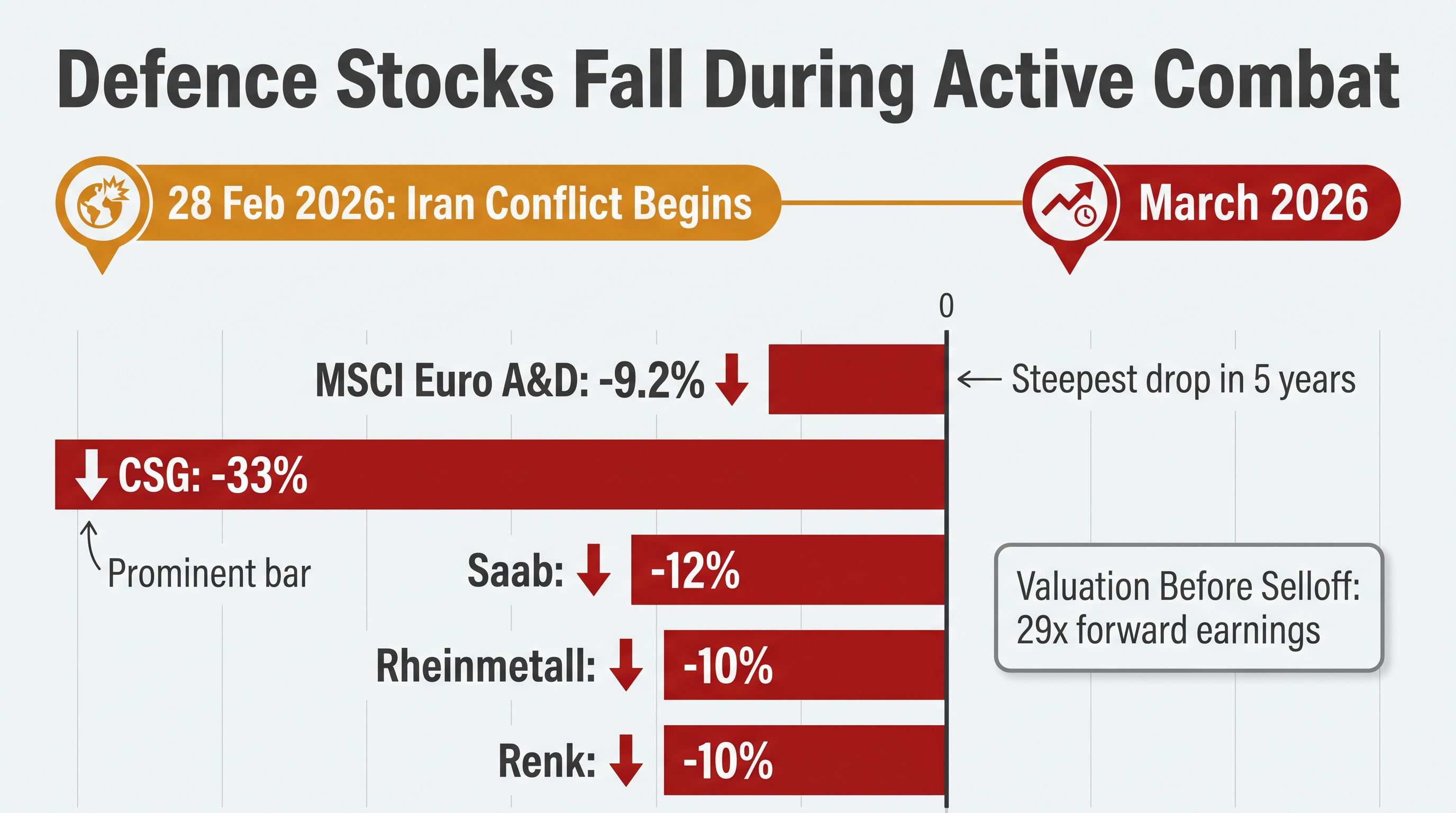

European defence stocks fell hard in March 2026 even as Iranian forces clashed with coalition naval units in the Strait of Hormuz. The MSCI European Aerospace and Defence benchmark declined 9.2% that month, the steepest monthly drop in five years. The selloff landed during active combat, inverting the wartime equity behaviour that typically lifts manufacturers of tanks, missiles, and interceptors. The divergence signals something structural: investors reassessing which technologies will capture the $2.6 trillion in global defence spending projected for 2026.

This analysis examines why traditional defence equities face headwinds even as military budgets surge, what the spending data reveals about procurement priorities, and where capital is actually flowing. The narrative arc runs from the March correction through the drone disruption thesis to budget realignment evidence, finishing with the investment positioning that emerged from the selloff. The core components of defence spending and drone technology converge in a sector rotation that is rewriting decades of procurement logic.

The Iran conflict began on 28 February 2026. By mid-March, European defence names had fallen sharply. CSG shares dropped roughly one-third. Rheinmetall and Renk each lost approximately 10%. Saab declined around 12%. The sector traded near 29 times forward earnings before the correction, close to all-time highs, pricing in future growth that had not yet materialised in contracts.

The 450% gain European defence stocks logged from Russia’s February 2022 Ukraine invasion through early 2026 compared to 40% for the broader MSCI Europe index. That outperformance built crowded positioning. When sentiment shifted, the unwind magnified the move. Citigroup analysis noted how overcrowded bullish bets amplify downside swings once conviction cracks.

Martin Frandsen, portfolio manager at Principal Asset Management, attributed the selling to institutional uncertainty:

“The market faced uncertainty around the durability of defence spending commitments and concerns about how quickly new contracts would translate into revenue.”

Investors often assume geopolitical tension automatically lifts defence equities. March demonstrated that valuation discipline and positioning dynamics can override conflict catalysts. The sector had priced optimism; the correction repriced reality.

For readers wanting to understand the broader multi-asset market implications of the Iran conflict that triggered the March defence selloff, our full explainer on how US-Iran tensions are moving oil, equities, and bonds examines cross-asset correlations, sector rotation patterns, and risk-off positioning across equities, commodities, and fixed income during the conflict period.

U.S. Patriot interceptors cost approximately $4 million per unit. Gulf nations deployed large numbers of Patriots during the Iran conflict, underscoring the expense of defending against aerial threats. The cost asymmetry became visible: affordable drones and loitering munitions demonstrated battlefield effectiveness in both Ukraine and the recent Middle East exchanges, forcing a reassessment of where military value lies.

The consumption rate problem compounds the unit cost issue. Expensive munitions deplete rapidly under sustained attack. Scalability favours cheaper platforms. Joint Interagency Task Force 401 (JIATF-401) committed over $600 million in counter-unmanned aerial system defences for Operation Epic Fury as of 10 April 2026, with $350 million allocated in the prior 30 days alone. That urgency reflects lessons learned from six weeks of high expenditure in contested Middle East environments.

The operational urgency driving JIATF-401’s $600 million commitment materialised commercially in contracts like EOS’s US$45 million in counter-drone orders announced in March 2026, demonstrating how Middle East combat experience accelerates procurement for systems proven under fire.

Rheinmetall and Anduril announced a partnership to co-develop Barracuda and Fury drone platforms for European markets, positioning the legacy manufacturer to capture demand for autonomous systems. Ciaran Callaghan, portfolio manager at Amundi, described the shift:

“There has been a perception change towards cheaper drone technologies being more effective than traditional expensive weapons systems.”

If procurement priorities rotate toward lower-cost drone systems, traditional platform manufacturers face margin compression and reduced visibility on large orders. The selloff may reflect more than profit-taking. It may encode a structural rethink about which capabilities governments will fund at scale.

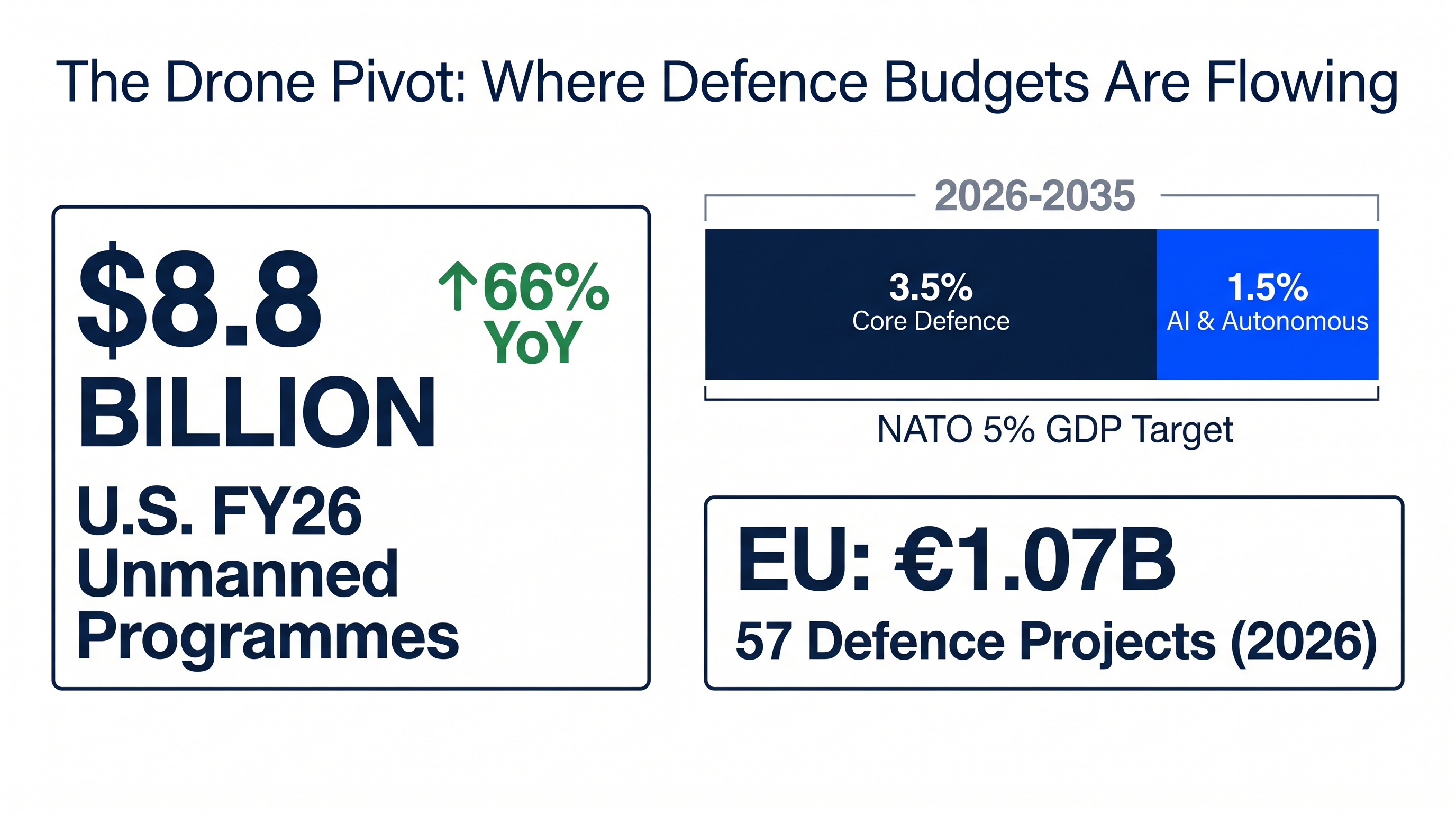

The U.S. FY26 Defence Appropriation Bill allocated $8.8 billion for unmanned programmes, a 66% increase year-on-year. That funding targets imminent deployments for systems like AeroVironment’s Switchblade loitering munitions and BlueHalo-powered Titan ground systems designed to defeat drone swarms. The scale of the increase signals where Pentagon priorities lie.

The EU announced €1.07 billion ($1.26 billion) for 57 defence projects on 15 April 2026. Loitering munitions projects, EURODAMM, LUMINA, SKYRAPTOR, and TALON, are designed for large-scale affordable production. Counter-drone systems tie to initiatives like the European Drone Defence Initiative, which integrates AI capabilities and draws from Ukraine cooperation. Europe’s E5 LEAP programme targets low-cost air defence deployment by 2027.

NATO shifted its target to 5% of GDP for defence by 2035, up from the longstanding 2% guideline. The framework splits spending into 3.5% for core defence and 1.5% earmarked for non-traditional areas including AI and autonomous technologies. The 2026 U.S. National Defence Strategy emphasises cost-effective defeat of missile barrages and aerial attacks, prioritising homeland defence and deterrence against China.

The budget realignment is not confined to Europe or the United States. Australia’s A$425 billion defence allocation over the next decade similarly prioritises unmanned systems and counter-drone capabilities, reflecting the global nature of the procurement pivot.

| Region | Programme | Allocation | Focus Area | Timeline |

|---|---|---|---|---|

| United States | FY26 Unmanned Programmes | $8.8 billion | Switchblade, Titan, MQ-1C Gray Eagle | 2026 deployments |

| European Union | 57 Defence Projects | €1.07 billion | Loitering munitions, counter-drone, AI | 2026-2027 |

| Europe | E5 LEAP | Undisclosed | Low-cost air defence | 2027 target |

| NATO | 5% GDP Target | Varied by nation | 3.5% core, 1.5% AI/autonomous | By 2035 |

Budget documents reveal procurement priorities before contracts materialise. These allocations show capital flowing toward drone platforms, counter-drone capabilities, and AI integration. The spending shift is not rhetorical. It is encoded in appropriations bills and multi-year frameworks.

A loitering munition is an autonomous or semi-autonomous aerial system that hovers over a target area before engaging. It combines surveillance and strike capabilities in a single platform. These systems wait, observe, and then execute precision attacks when conditions align. They fill the operational gap between traditional missiles, which follow fixed trajectories, and manned aircraft, which require pilots and extensive support infrastructure.

Counter-drone systems address the threat that cheap drones pose. The goal is to defeat low-cost aerial threats without expending expensive interceptors. Technologies range from electronic warfare systems that jam drone signals to directed energy weapons and kinetic interceptors optimised for small targets. The operational challenge is matching the cost of defence to the cost of the threat.

JIATF-401 fielded counter-unmanned aerial system capabilities in U.S. Central Command following six weeks of heavy Middle East expenditure during Operation Epic Fury. FY26 funding accelerates deployments for Switchblade loitering munitions and Titan ground systems designed to defeat swarms. EU loitering munitions projects, EURODAMM, LUMINA, SKYRAPTOR, and TALON, target large-scale affordable production to supply European forces with scalable strike options.

Drone system categories:

Understanding these operational categories helps evaluate which companies and capabilities align with procurement priorities. Treating drones as a monolithic category misses the distinct missions and funding streams each system addresses.

The March selloff did not trigger a sector-wide exit. ETF flow data shows continued conviction, selectively deployed. The WisdomTree Europe Defence ETF attracted $1.32 billion in net inflows year-to-date through 2026, with $377 million arriving after the Iran conflict began. iShares Europe Defence and HANetf Future of Defence combined for $355 million in 2026 inflows, with $124 million flowing in since the conflict onset.

Jane Edmonson, research analyst at VettaFi, described the rotation:

“The global market is now favouring unmanned aerial systems over things like expensive fighter jet programmes and missile programmes, with investments flowing into drone swarms, surveillance capabilities, counter-drone technologies, and AI for autonomous decision-making.”

AeroVironment benefits directly from Switchblade demand and FY26 funding acceleration. U.S. reshoring initiatives and Federal Communications Commission bans on foreign drones create tailwinds for domestic producers. Supply chain providers for drone components also capture demand as production scales. Defence technology firms with AI and edge computing capabilities align with the autonomous systems mandate embedded in NATO’s 5% framework and the 2026 National Defence Strategy.

ETF inflows (2026):

The data shows investors buying the dip selectively. Capital is rotating within defence, not abandoning it. The beneficiaries are firms aligned with drone platforms, counter-drone systems, and AI-enabled autonomy.

Morgan Stanley analysts observed that contract awards have materialised more slowly than investors anticipated. Budget constraints in France and the UK have stretched or postponed deals that markets expected to close earlier. That timing gap creates near-term pressure on revenue visibility for traditional prime contractors.

The slower award pace does not negate the structural thesis. Budget allocations confirm the spending direction. Delivery timelines are extending, not disappearing. The gap between appropriations and contracts means investors must distinguish between firms capturing immediate orders and those positioned for multi-year procurement cycles that have not yet commenced.

The March 2026 selloff in European defence stocks reflected crowded positioning colliding with peak valuations, not a rejection of the defence investment thesis. The 9.2% decline occurred during active conflict because the sector had priced years of growth into current multiples. When contract timing disappointed and positioning unwound, the correction was swift.

The underlying capital flows and budget allocations confirm a structural shift toward drone systems, loitering munitions, and counter-drone capabilities. The U.S. FY26 allocation of $8.8 billion for unmanned programmes, a 66% year-on-year increase, and the EU’s €1.07 billion for 57 projects including drone-focused initiatives encode the procurement pivot. NATO’s 5% of GDP target by 2035, with 1.5% earmarked for AI and autonomous technologies, establishes a multi-year framework that will drive demand regardless of near-term contract timing gaps.

The Pentagon’s FY27 budget proposes further counter-drone spending increases. EU production initiatives target 2027 delivery for low-cost air defence platforms. The reallocation is real, but it is a rotation within defence spending, not a reduction.

Investors evaluating defence exposure should distinguish between legacy platform manufacturers facing demand uncertainty and drone-focused firms positioned to capture the reallocation. The March correction repriced valuations. The budget data confirms the direction of the capital.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The March correction forced investors to reconsider sector allocations beyond pure defence exposure. Broader defensive stock positioning strategies during market turbulence, including essential services and consistent-earnings anchors, provide portfolio protection mechanisms that complement cyclical defence holdings.

A loitering munition is an autonomous or semi-autonomous aerial system that hovers over a target area before executing a precision strike, combining surveillance and attack capabilities in one platform. Investors should note that governments are scaling procurement of these systems rapidly, with the US FY26 budget allocating $8.8 billion for unmanned programmes, a 66% year-on-year increase.

European defence stocks fell 9.2% in March 2026 despite active combat because the sector had already priced in years of future growth at near all-time high valuations of 29 times forward earnings, and crowded institutional positioning amplified the selloff when contract timing disappointed investor expectations.

Capital is rotating toward drone platforms, loitering munitions, and counter-drone systems, as evidenced by the US FY26 $8.8 billion unmanned programme allocation, the EU's 1.07 billion euros for 57 drone-focused defence projects, and NATO's framework earmarking 1.5% of GDP for AI and autonomous technologies by 2035.

The WisdomTree Europe Defence ETF attracted $1.32 billion in net inflows year-to-date through 2026, with $377 million arriving after the Iran conflict began, while iShares Europe Defence and HANetf Future of Defence combined for $355 million in 2026 inflows, signalling selective conviction rather than a sector-wide exit.

Investors should distinguish between legacy platform manufacturers facing margin pressure and demand uncertainty, and drone-focused firms, counter-drone technology providers, and AI-enabled autonomy companies that are directly aligned with the procurement priorities confirmed in US, EU, and NATO budget frameworks.