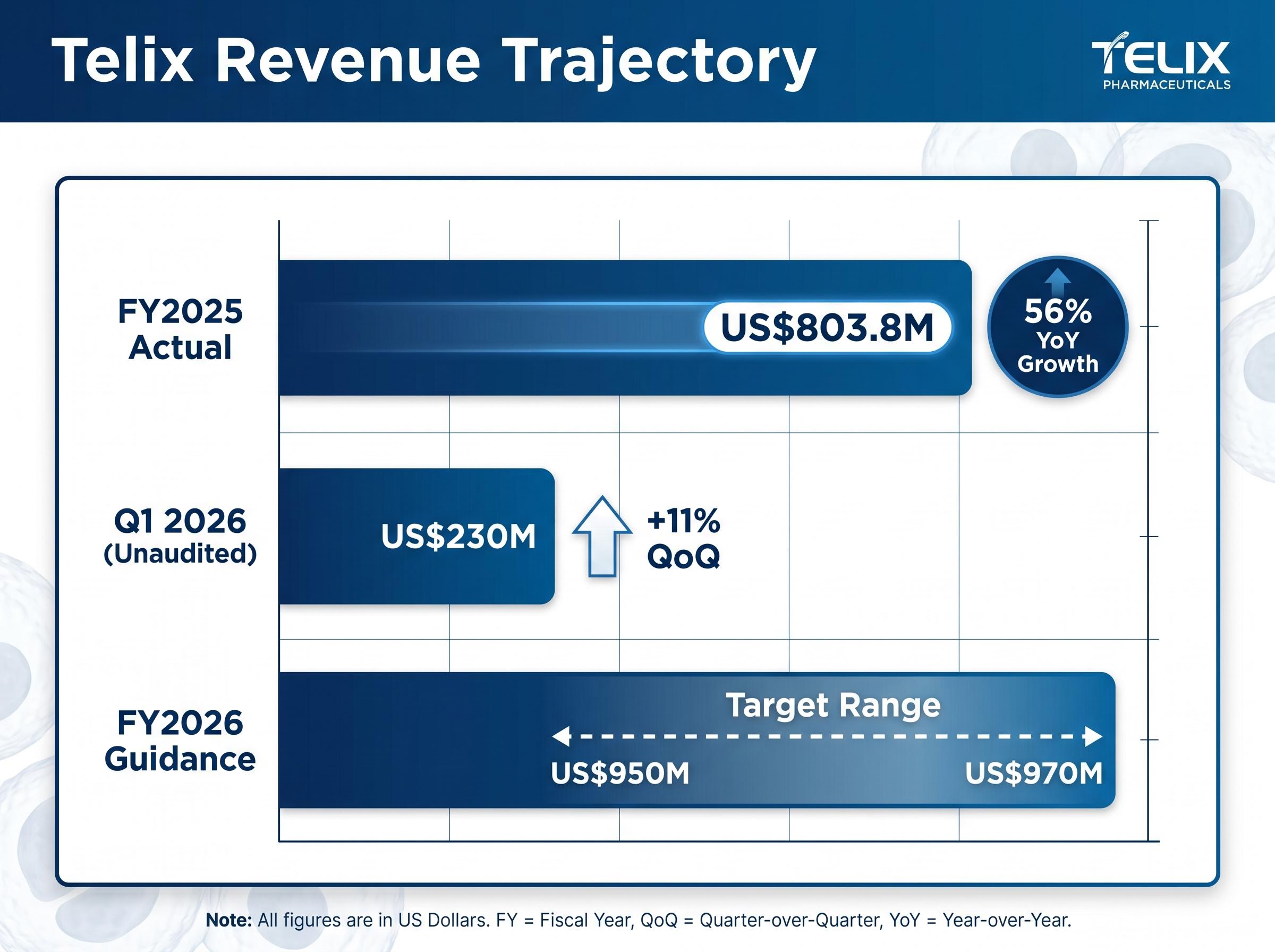

Telix Pharmaceuticals closed 2025 with US$803.8 million in revenue. The company is now guiding for nearly US$1 billion in 2026, a commercial trajectory that almost no ASX-listed biotech has ever traced. That performance is unfolding inside a global radiopharmaceutical sector where Novartis, Eli Lilly, and Bristol-Myers Squibb have collectively deployed billions in acquisition capital, making Telix’s scale as an Australian-origin company structurally unusual. This analysis moves through what is driving the revenue, what the pipeline adds to the valuation case, and what the current share price setup means for investors evaluating Telix Pharmaceuticals stock today.

From near-zero to nearly US$1 billion: what Telix’s 2025 revenue result actually means

56% year-over-year revenue growth in FY2025, a pace of commercial scaling that places Telix in rare company among ASX-listed healthcare names.

The headline numbers tell a story that most ASX biotechs never get to tell:

- FY2025 revenue: US$803.8 million

- Q1 2026 unaudited revenue: US$230 million (up 11% quarter-over-quarter)

- FY2026 guidance: US$950-970 million

This is not a pre-revenue pipeline bet. The 56% year-over-year growth rate delivered in 2025 reflects a company with commercially approved products generating real, recurring income at a scale that compresses the gap between Telix and global specialty pharma names.

Q1 2026 matters because it demonstrates the growth rate is holding, not fading. US$230 million in a single quarter, tracking on pace with full-year guidance of US$950-970 million, suggests the demand environment for Telix’s core products has not yet plateaued. At a market capitalisation of approximately A$4.78 billion as of May 2026, the stock is priced well below the revenue multiple that a global specialty pharma peer growing at this rate would command. Whether that discount is justified requires looking at what is actually generating the revenue, and where the vulnerabilities sit.

When big ASX news breaks, our subscribers know first

The two products carrying nearly US$1 billion in annual revenue

Two products form the commercial backbone of this business: Illuccix and Gozellix, both prostate cancer imaging agents approved in the US market. These are PSMA PET imaging agents, meaning they help clinicians visualise prostate cancer cells with high precision for staging, recurrence detection, and therapy selection. The US is the primary revenue geography, and the clinical utility of PSMA imaging in prostate cancer management has driven rapid adoption.

| Product | Indication | US Approval Status | Key Commercial Risk |

|---|---|---|---|

| Illuccix | PSMA PET imaging for prostate cancer | Commercially approved | ASP pressure from pass-through reimbursement expiry |

| Gozellix | PSMA PET imaging for prostate cancer | Commercially approved | No switching costs for end users; pricing vulnerability |

The concentration is worth naming directly. Essentially all of Telix’s revenue comes from two products in a single disease area. That concentration is simultaneously the source of the company’s commercial strength and its most identifiable business risk.

The Gozellix launch dynamics, including CMS reimbursement timing, dose volume growth, and the pricing power signal embedded in revenue outpacing volume by a wide margin, provide important context for reading the FY2025 result as a structural rather than one-off outcome.

The reimbursement cliff: what ASP pressure means for forward revenue

Illuccix benefited from pass-through reimbursement status in the US Medicare system, a temporary pricing protection that allows new medical products to be reimbursed at a higher rate during their initial period on the market. That status expired post-2025, which means the average selling price (the price hospitals and imaging centres pay per dose) is normalising toward standard reimbursement rates. In plain terms, Telix was selling Illuccix at a premium price while the protection lasted; that premium is now shrinking. Combined with the absence of switching costs for imaging centres (they can move between competing products without penalty), this dynamic creates pricing pressure that investors should factor into any forward revenue model.

What radiopharmaceuticals are and why the world’s largest drug companies are paying billions to enter the space

Radiopharmaceuticals, sometimes called targeted nuclear medicines, deliver radiation directly to cancer cells via a targeting molecule. The targeting molecule finds the cancer cell; the attached radioactive payload destroys it. This approach serves two functions: diagnostic imaging (finding cancer with precision) and therapy (treating it at the cellular level), sometimes using the same targeting platform for both.

Three structural reasons explain why the sector has attracted major pharmaceutical capital:

- Precision delivery: Radiation reaches cancer cells directly rather than affecting surrounding healthy tissue, reducing side effects compared to conventional radiation therapy.

- Diagnostic-therapeutic combination: A single molecular platform can both image cancer and treat it, creating clinical and commercial synergies that traditional drug development does not offer.

- Growing FDA approval pipeline: Regulatory approvals for targeted radiotherapies have accelerated, expanding the addressable market across multiple cancer types.

Novartis, Eli Lilly, and Bristol-Myers Squibb have all deployed substantial acquisition capital to enter the radiopharmaceutical sector, signalling that the world’s largest drug companies view this category as a strategic priority for the next decade of oncology.

Telix holds a dual listing on both the ASX and Nasdaq, a structure partially driven by the need to access capital markets at the scale where this sector competes. As the commercially leading Australian entrant in a space otherwise defined by US and European majors, the company occupies a position that the analyst community views as structurally significant, even as the share price has weakened over the past twelve months.

Pipeline beyond the core: ProstACT Phase 3 and the Pixclara FDA decision

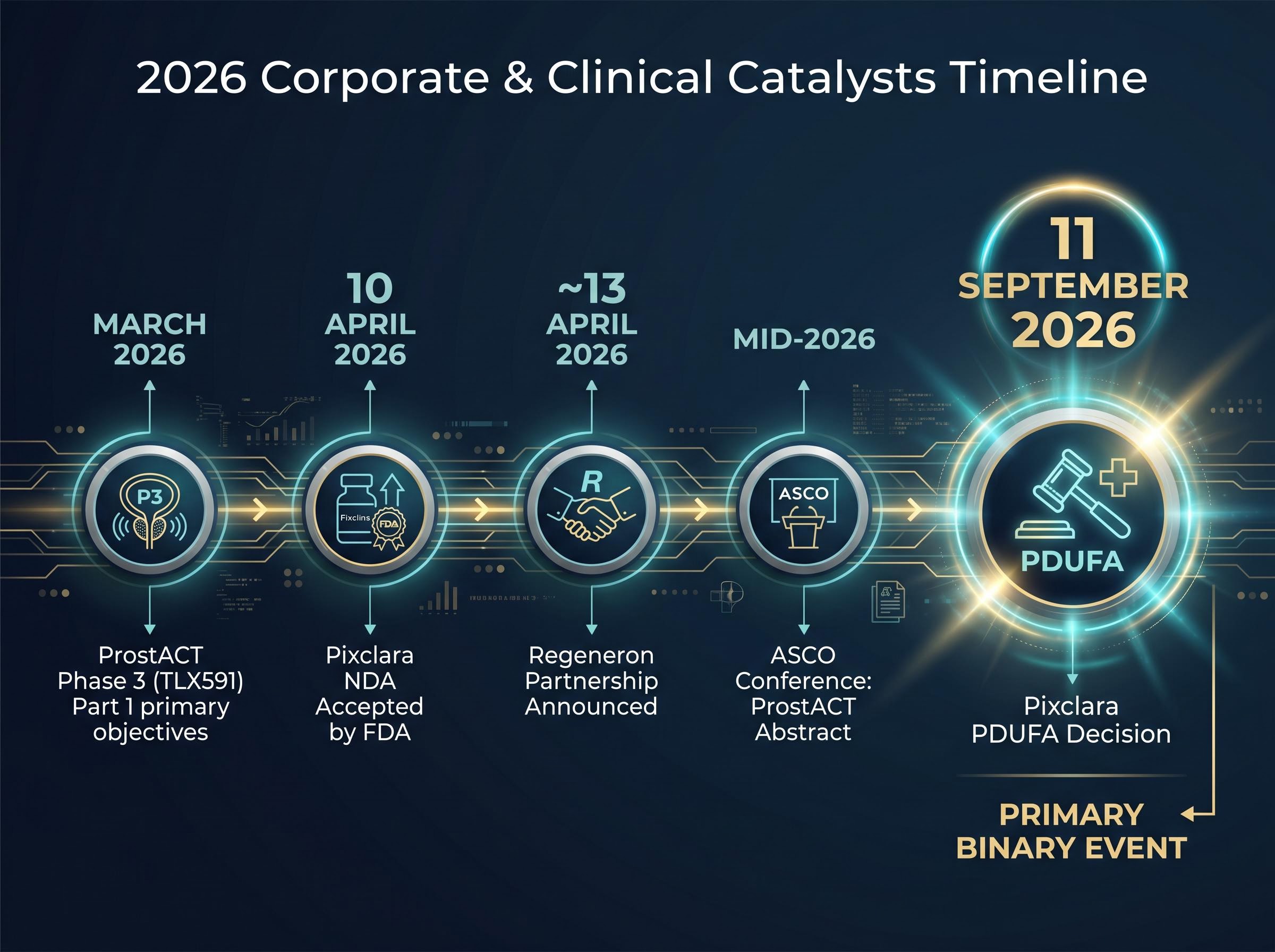

The pipeline converts the commercial present into forward-looking optionality, and the catalysts are specific and dated.

ProstACT Phase 3 (TLX591) achieved its Part 1 primary objectives in March 2026. Safety data from the programme was subsequently selected as a late-breaking abstract at ASCO 2026, a distinction that signals clinical credibility and peer validation. Late-breaking abstracts at ASCO are competitively selected and indicate data the oncology community considers noteworthy.

Pixclara (TLX101-Px) is a different proposition entirely. The FDA accepted its New Drug Application (NDA) on 10 April 2026, with a PDUFA decision date of 11 September 2026. Pixclara is an imaging agent for recurrent and progressive glioma, a brain cancer indication that sits outside Telix’s prostate cancer core. Approval would add a new commercial revenue stream in a distinct oncology segment.

The Pixclara resubmission addressed a Complete Response Letter issued by the FDA in April 2025, meaning the September 2026 PDUFA decision represents a second-attempt regulatory outcome rather than a first-pass review, a distinction that shapes how investors should weight the binary risk of that date.

| Catalyst | Expected Timing | Investor Significance |

|---|---|---|

| ProstACT ASCO abstract | Mid-2026 (ASCO conference) | Visibility for TLX591 therapeutics programme; peer validation of safety profile |

| Pixclara PDUFA decision | 11 September 2026 | Binary catalyst: approval adds new revenue stream; rejection resets timeline |

| Regeneron collaboration milestones | Ongoing 2026 | Development updates on next-generation radioligand pipeline |

The 11 September PDUFA date is the nearest binary event on the calendar. It is directly relevant to position-sizing and timing decisions for investors considering entry or addition.

The FDA PDUFA review timelines for NDAs establish a standard 10-month review window from the filing date for most new drug applications, which places the 11 September 2026 Pixclara decision date within the expected regulatory calendar following the April 2026 NDA acceptance.

Share price, analyst targets, and the Regeneron effect: how investors are reading Telix today

TLX closed around A$14.75-A$14.95 in early May 2026, approximately 43% below its 12-month high, with a one-year return of approximately negative 37.75%. Weekly price volatility sits at roughly 9.6%.

The Regeneron partnership, a global co-development agreement for next-generation radiopharmaceuticals announced around 13 April 2026, drove shares to a 2026 high of approximately A$15.77. The rally reflected the market’s reading of a tier-1 pharmaceutical validation: non-dilutive capital and a credible development partner. Then, within days, Telix announced a US$600 million convertible bond raise (1.50% bonds due April 2031), upsized from US$550 million. Shares dropped approximately 4.21% to around A$14.80. The Regeneron optimism absorbed a dilution event almost immediately.

Analyst consensus price targets sit at A$23.34-A$24.22, implying approximately 57-62% upside from current levels.

That gap between analyst targets and the share price is not a simple arbitrage opportunity. Three distinct headwinds are holding the price below where fundamentals might otherwise suggest:

- Convertible bond dilution overhang from the US$600 million raise

- Elevated short interest and arbitrage activity driven by dual-listing dynamics

- Pass-through reimbursement expiry on Illuccix, creating ASP pressure on core revenue

Against these sit three identifiable positive catalysts:

- Regeneron partnership validating the next-generation pipeline

- Pixclara PDUFA decision on 11 September 2026

- ProstACT ASCO data presentation at mid-year

The coexistence of a constructive analyst community and a negative 37.75% one-year return reflects this tension. Structural dynamics are suppressing the price independently of fundamental views.

What Telix’s trajectory signals for ASX investors weighing the stock now

The bull case compresses into a single paragraph: Telix is guiding for nearly US$1 billion in 2026 revenue, analyst consensus sits at a 57-62% premium to the current share price, two near-term pipeline catalysts (PDUFA in September, ASCO data mid-2026) could serve as re-rating triggers, and Regeneron provides tier-1 pharmaceutical validation of the technology platform.

The bear case demands equal weight. Revenue is concentrated in two prostate cancer imaging products facing ASP pressure from reimbursement changes. A US$600 million convertible bond raise has introduced dilution and ongoing arbitrage headwinds. The one-year return of negative 37.75% has punished holders, and the short interest data suggests sophisticated participants remain positioned for further weakness.

Before taking a position, investors may wish to consider:

Binary catalyst position-sizing is one of the more consequential decisions ASX biotech investors face, and the discipline of pre-defining exit conditions before a PDUFA or interim analysis date applies as directly to Telix’s September decision as it does to any earlier-stage catalyst-driven name.

- Can the FY2026 guidance of US$950-970 million be achieved if Illuccix ASPs decline materially from pass-through levels?

- What does a Pixclara approval (or rejection) on 11 September 2026 mean for the revenue diversification thesis?

- How much of the analyst consensus upside is already contingent on pipeline success rather than the commercial base alone?

- Is the current share price reflecting structural dual-listing headwinds that will persist regardless of business performance?

- Does the US$600 million convertible bond maturity in 2031 create a manageable or constraining capital structure?

The dual-listing dynamic: what ASX investors should understand about Nasdaq-driven volatility

Telix trades on both the ASX and Nasdaq. When events such as convertible bond raises occur, sophisticated traders use Nasdaq-listed shares and options as hedging instruments. The resulting short positions often land on ASX-listed shares, creating selling pressure that is disconnected from Telix’s underlying business performance. This dynamic is not unique to Telix; it is structurally present for any ASX-listed security that also trades on a major US exchange with active derivatives markets. For Australian retail investors, it means that short-term ASX price movements may reflect hedging mechanics rather than changes in fundamental value.

Revenue momentum is real, but the re-rating requires a catalyst

The commercial foundation is genuine and quantified: US$803.8 million in 2025, nearly US$1 billion guided for 2026, with Q1 tracking on pace. This is not a speculative story.

FY2026 guidance: US$950-970 million. The commercial scale argument rests on whether this target is delivered amid reimbursement headwinds on the core product.

The 11 September Pixclara PDUFA decision and the ASCO 2026 data release are the most proximate events that could serve as re-rating triggers. The market appears to be in a wait-and-see posture ahead of these dates. The gap between analyst targets and the current price is either an opportunity, if catalysts deliver, or a fair reflection of risk, if they disappoint. The next three to six months will clarify which reading is correct.

The Illuccix China filing, accepted by the NMPA with Phase 3 data showing 94.8% detection accuracy and treatment decision changes in 67.2% of cases, represents a geographic diversification move that sits entirely outside the US reimbursement dynamics currently pressuring the core revenue base.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.