How Warsh’s 130-Word Statement Reshaped Federal Reserve Policy

1 hr ago

The week beginning 23 June 2026 opens with two forces pulling in the same direction, and no guarantee they will keep agreeing. Oil prices are falling on ceasefire optimism after the US and Iran signed a 14-point Memorandum of Understanding around 17 June. Wednesday’s release of May PCE inflation data, the price measure the Federal Reserve treats as its primary guide to inflation, sits on the calendar alongside a revised Q1 GDP print. The Fed holds rates at 3.50-3.75% and describes its next move as entirely data-dependent. Tuesday’s PMI readings and FedEx earnings add two more real-time reads on economic momentum before the main event. What follows lays out what each catalyst actually means for rates, equities, and commodities, and how the interaction between geopolitics and macro data shapes the risk calculus you face before the week is out.

The 14-point MOU, signed around 17 June 2026, is an interim framework, not a final settlement. It suspends fighting, lifts certain financial and energy restrictions, commits both sides to further negotiations on Iran’s nuclear programme, and reopens the Strait of Hormuz to normal shipping activity. Both parties accepted a two-month talks timetable giving diplomats until mid-August to convert framework commitments into binding terms.

The US-Iran ceasefire announcement on 17 June triggered an immediate 1.4% Nasdaq 100 futures surge and sent Brent crude down 2.31% to $77.71 on 18 June, with the VIX simultaneously rising 12.37% to 18.44, a divergence that signals markets priced relief on the diplomatic side while retaining residual uncertainty on the policy side.

The direct transmission mechanism from diplomacy to crude prices has been straightforward: reduced disruption risk through the Strait of Hormuz has pulled oil back toward pre-conflict levels. Markets are pricing in a lower probability of supply shock, and the geopolitical risk premium that had inflated crude for months is compressing.

Swiss talks on 22 June concluded with both parties signalling continued commitment to further technical discussions, with Qatari and Pakistani mediators confirming the outcome. Additional technical sessions were anticipated within days.

The decline in oil is real, but it rests on a diplomatic process with multiple points of failure. Investors treating it as a permanent supply-side improvement are mispricing the ongoing downside risk. The specific fragility factors worth tracking:

Lower oil functions as a quiet disinflationary input, but only if the framework holds. That makes the ceasefire’s durability a direct input into where PCE and Fed expectations land in the weeks ahead.

The Personal Consumption Expenditures (PCE) price index measures the prices paid for goods and services by consumers across the US economy. The Fed uses PCE rather than the more widely reported Consumer Price Index (CPI) because PCE captures a broader range of expenditures and adjusts for substitution behaviour: when consumers switch from an expensive item to a cheaper alternative, PCE reflects that shift while CPI does not. The Fed’s Summary of Economic Projections is framed explicitly around PCE and core PCE inflation paths, making Wednesday’s number the single most policy-relevant data point of the week.

The BEA’s PCE methodology explains the formula, weight, and scope effects that make PCE a broader and more responsive measure than CPI, capturing the substitution behaviour that causes the two indices to diverge during periods of relative price shifts across categories.

This release covers May data and lands on Wednesday 25 June. On the same day, a revised Q1 GDP print arrives with updated figures on consumption and business investment. Revisions in either direction can move cyclicals and yields independently of the inflation print, creating a dual-release moment with compounding market impact.

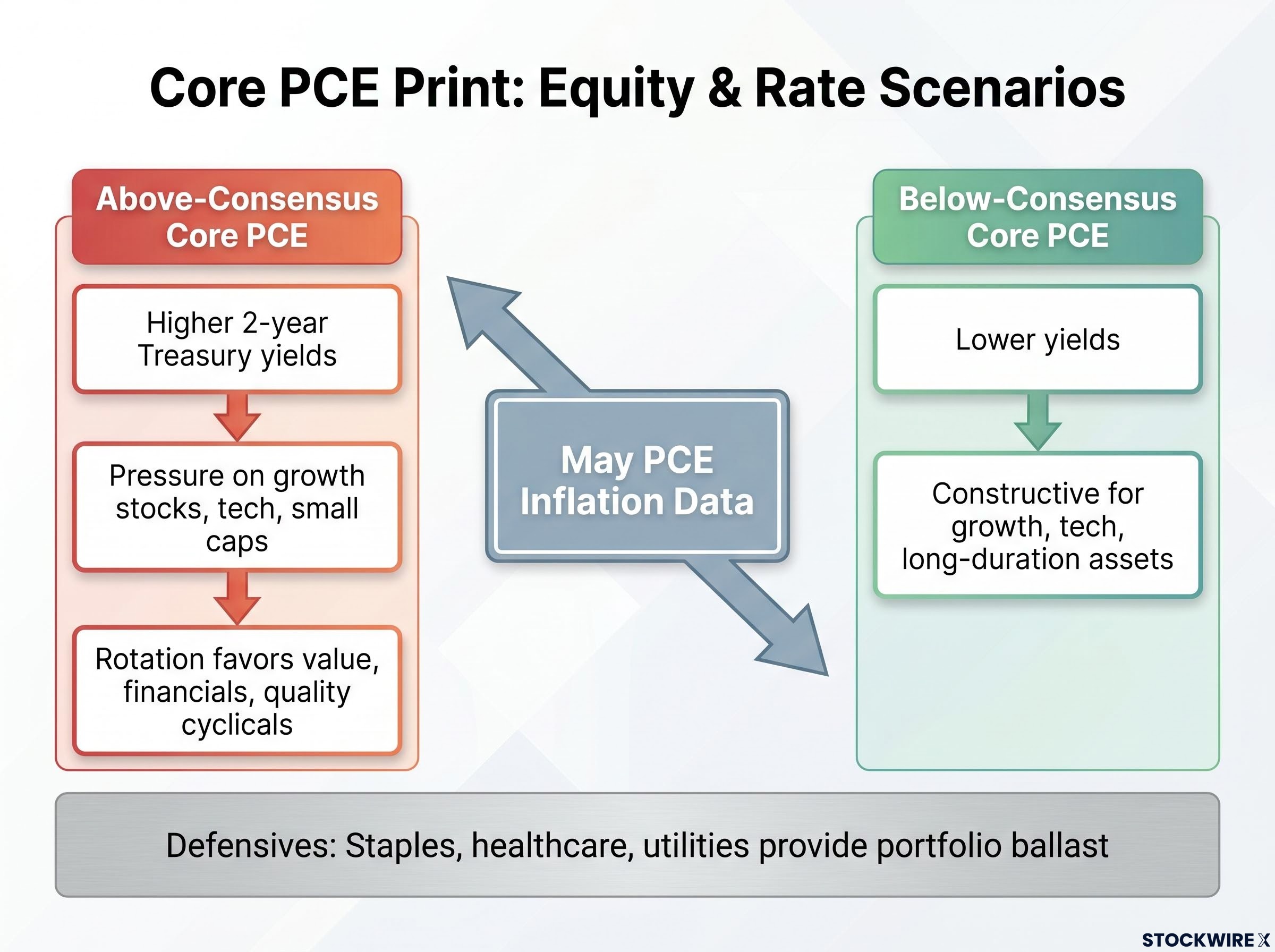

The market’s reaction function is two-sided, and the contrast matters for positioning:

For equity investors, Wednesday’s combined PCE and GDP release is effectively a policy recalibration moment. The numbers will tell you whether the Fed’s “data-dependent” posture leans dovish or hawkish into the second half of the year.

Warsh’s data-dependent framework, formalised at the 16-17 June FOMC meeting, replaced a two-decade communications architecture with a strict meeting-by-meeting posture; with 9 of 18 FOMC officials now projecting at least one rate hike in 2026, Wednesday’s PCE print arrives into a committee that is genuinely split rather than leaning toward any predetermined path.

Tuesday’s releases function as the economic canary before the main event. The June PMI (Manufacturing and Services), due Tuesday 24 June, is a forward-looking gauge that either reinforces or challenges the resilient-growth narrative underpinning current Fed caution. A soft reading would shift the odds before Wednesday’s inflation data even arrives.

The June PMI baseline for context: May 2026 PMI data showed US manufacturing at 55.3 and services at 50.9, making the US the only major developed economy with both sectors expanding simultaneously, which is why a softer June reading would represent a meaningful directional shift rather than a continuation of an already-weak trend.

FedEx reports Q4 FY2026 earnings on Tuesday 23-24 June, and its conference call is a real-time cross-check on consumer spending and freight demand that official data will not capture as quickly. The indicators worth watching inside the report: shipping volumes, package mix, international freight trends, pricing power, and management guidance tone. If FedEx volumes disappoint and PMI softens on Tuesday, Wednesday’s PCE release carries even higher stakes because the growth side of the equation will already look shakier.

| Release | Day | Date | Market Significance |

|---|---|---|---|

| FedEx Q4 FY2026 Earnings | Tuesday | 23-24 June 2026 | Real-time demand and shipping cross-check |

| June PMI (Manufacturing and Services) | Tuesday | 24 June 2026 | Forward-looking activity gauge |

| Revised Q1 GDP | Wednesday | 25 June 2026 | Growth revision with consumption and investment detail |

| PCE Price Index (May data) | Wednesday | 25 June 2026 | Fed’s preferred inflation gauge; the week’s main event |

Tracking Tuesday’s releases gives you an early read on economic momentum before the Fed’s preferred inflation gauge lands, allowing better-informed positioning ahead of Wednesday’s potential volatility.

The reason this week is more consequential than a typical data week is that geopolitical and policy signals are both pointing at the same inflation variable, and they are not guaranteed to keep pointing in the same direction.

Start with the cooperative scenario:

Then consider the collision:

Both forces are acting on the same variables, oil, inflation, and rate expectations, simultaneously. That amplifies the consequence of any outcome at either end of the spectrum. The 2-year Treasury yield is the cleanest real-time read on Fed expectations: watch for a sustained move higher post-PCE as a signal for duration caution. Strait of Hormuz shipping normalisation, visible through insurance and routing data, serves as a confirmatory signal that the risk premium is genuinely declining, not just being priced out temporarily.

Investors who understand the interaction between the ceasefire and the PCE print can frame their risk positioning around scenarios rather than reacting to individual headlines as they arrive.

With two high-impact drivers running simultaneously, position sizing and hedging discipline matter as much as directional conviction. The practical takeaway is not a single directional bet but a scenario-aware framework: know which assets benefit in each outcome, and size accordingly before Wednesday rather than after it.

| Asset Class | Hot PCE / Ceasefire Breakdown | Cool PCE / Ceasefire Holds |

|---|---|---|

| Energy | Crude spikes; nimble short-horizon upstream exposure rewarded | Oil stable or lower; lean tactical stance on upstream names |

| Rates and Duration | 2-year yields rise; caution on duration warranted | Yields fall; selectively adding high-quality duration supported |

| Equities | Bias toward value, financials, quality cyclicals | Constructive for growth, tech, long-duration assets |

| Defensives | Staples, healthcare, utilities provide portfolio ballast | Reduced urgency but still sensible as risk management |

The 2-year Treasury yield remains the key signal across scenarios. A sustained move higher after PCE argues for caution on duration. A downside surprise pulling that yield lower supports selectively adding high-quality duration.

In a hot-PCE environment with firm PMIs and GDP, the rotation favours value, financials, and quality cyclicals. Discipline on richly valued long-duration growth names matters most here because those are the equities most sensitive to rising discount rates. In a cool-PCE environment with benign oil, the bid moves toward growth, tech, and other long-duration assets, particularly if Fed rhetoric softens after the release.

For lower-risk investors, maintaining defensive exposure (staples, healthcare, utilities) alongside adequate liquidity or hedges such as index options remains sensible regardless of which scenario materialises. The simultaneity of geopolitical and policy risk is what makes hedging discipline the through-line of the week.

The week’s data and diplomacy do not exist in isolation. The two-month diplomatic timetable, initiated around 17 June 2026, runs through mid-August 2026. That means the Iran risk premium does not disappear after this week; it becomes a recurring variable you will need to re-evaluate with each significant diplomatic development through the summer.

The 60-day window is a countdown clock with compounding consequences: progress extends the disinflationary tailwind from lower oil, while a breakdown reinstates the risk premium quickly and feeds directly into inflation and rate expectations.

The three specific watchpoints to monitor as the week progresses and beyond:

Any Fed commentary released after Wednesday’s PCE data will be closely watched for whether policymakers treat the May reading as a trend signal or an outlier. Investors who track the right signals will have an earlier read on whether the disinflationary tailwind from diplomacy is durable or beginning to fade.

For investors who want to extend the scenario logic beyond this week’s data calendar, our comprehensive walkthrough of the probability-weighted scenario framework applied to 2026 macro risks covers how to assign explicit probability estimates across conflicting outcomes, size portfolio responses to actual likelihood rather than media coverage intensity, and identify which combinations of scenarios carry compounding tail correlation that single-event analysis misses.

Wednesday’s PCE print will move markets, but it is worth being precise about what it can and cannot settle.

What this week may resolve:

What it will not resolve:

The Fed’s stated data-dependent posture from the 17 June FOMC statement means no single print settles the outlook. And the two-month diplomatic timetable extending through mid-August means geopolitical risk remains in play well after this week’s calendar clears.

The most useful discipline for the weeks ahead is scenario-awareness and position-sizing, not directional conviction based on a single week’s outcomes. A framework for ongoing assessment is more valuable than a resolved outlook, because the resolution has not arrived yet.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

The PCE price index measures prices paid for goods and services across the US economy and adjusts for substitution behaviour, meaning it reflects when consumers switch to cheaper alternatives, which CPI does not. The Fed uses PCE because it is broader and more responsive, and the Fed's Summary of Economic Projections is framed explicitly around PCE and core PCE inflation paths.

The 14-point Memorandum of Understanding signed around 17 June reopened the Strait of Hormuz to normal shipping and compressed the geopolitical risk premium that had inflated crude for months, sending Brent down 2.31% to $77.71 on 18 June. Lower oil functions as a disinflationary input that could soften the May PCE print, but only if the ceasefire framework holds through its two-month timetable.

An above-consensus core PCE print would push 2-year Treasury yields higher, trigger hawkish repricing of Fed rate expectations, and apply direct pressure on growth stocks, tech, and small caps, with rate-sensitive sectors feeling the squeeze first. In that environment, the rotation favours value, financials, and quality cyclicals.

FedEx Q4 FY2026 earnings provide a real-time cross-check on consumer spending and freight demand that official data cannot capture as quickly, while June PMI is a forward-looking gauge of whether the resilient-growth narrative underpinning current Fed caution remains intact. If both disappoint on Tuesday, Wednesday's PCE release carries even higher stakes because the growth side of the equation will already look shakier.

The three most reliable signals are daily Brent and WTI price moves alongside implied volatility in oil options, shipping and insurance conditions in the Strait of Hormuz, and official statements from Washington, Tehran, Qatar, and Pakistan on progress or setbacks in technical negotiations. These provide earlier reads on ceasefire durability than headline diplomatic announcements alone.