How to Tell if a Yield Surge Is Global or a Domestic Warning

31 mins ago

GameStop posted its highest first-quarter operating income in company history during Q1 2026, reporting $143.3 million in operating profit on $835.3 million in net sales. The company that most American investors still associate with a Reddit-fuelled short squeeze in January 2021 delivered record net income of $389.6 million, grew revenue 14% year-over-year, and sits on approximately $9.7 billion in total liquidity with zero debt.

Almost none of that led the financial coverage cycle.

The meme-stock identity has functioned as a narrative ceiling for GameStop, suppressing serious engagement with what the business actually looks like five years into Ryan Cohen’s tenure as CEO. Cohen has run the company through a genuine strategic repositioning, one that diverged sharply from his original e-commerce instincts and landed on a collectibles-led retail model that now accounts for 42% of quarterly revenue. The Q1 2026 data tells a materially different story than the one most investors carry. Here is what the numbers actually show, what the strategy behind them reveals, and what both mean for anyone trying to form a grounded view of where GameStop stands today.

Cohen was originally drawn to GameStop by the kind of setup that attracts contrarian capital: heavy short interest, negative media sentiment, and an anticipated console hardware cycle that historically benefits the retailer when new product availability is constrained. Management initially approached him to join the board as a counterweight to a different activist investor. Cohen has noted that his father’s recent passing affected his early decision-making, and that assuming the CEO role happened by necessity rather than original intent.

Once in control, he did what most founders do: he ran the playbook that had already worked. He hired from Chewy and Amazon, leaned into e-commerce, and pushed into broader consumer electronics categories. The problem was structural, and it took him roughly a year to recognise it.

The mismatch came down to inventory economics:

Cohen has spoken openly about this strategic misstep. What matters analytically is what came after: a deliberate pivot back to working with long-tenured internal staff who understood GameStop’s existing operational strengths, particularly the pre-owned merchandise model. The early 2021 capital raise of approximately $1.7 billion, which eliminated all outstanding debt, gave Cohen the financial room to absorb the detour and redirect.

The error is not a failure story. It is the analytical foundation for understanding why the current model works, because Cohen found the right strategic fit only after discovering what did not transfer from his prior success.

The collectibles pivot looks opportunistic if you encounter it cold. It looks logical once you understand the operational mechanics underneath it.

GameStop’s pre-owned trade-in business runs on three competencies: condition-sensitive pricing (every used game or console is graded individually), secondary-market price discovery (resale values fluctuate with demand and scarcity), and direct consumer sourcing (the customer walks in with the product; GameStop does not need a wholesale supply chain). These are specialist retail skills that the company has refined over decades of buying, grading, and reselling used merchandise.

Trading cards, particularly PSA-graded cards purchased directly from consumers for resale, map onto exactly the same competency set. The grading is condition-sensitive. The pricing requires secondary-market knowledge. The sourcing is consumer-direct. The demographic overlap between GameStop’s existing store customer base and the trading card collector community reinforces the fit further.

The U.S. trading cards market was estimated at $10.54 billion in 2025 and is projected to reach $17.82 billion by 2033, according to Grand View Research, which means GameStop’s collectibles expansion is tracking a category with substantial structural tailwinds rather than a fading novelty cycle.

The trajectory tells the story of a deliberate expansion, not a speculative bet:

| Period | Collectibles Revenue (approx.) | Share of Total Revenue |

|---|---|---|

| Pre-pivot baseline | Not disclosed | ~10-14% |

| FY 2024 | ~$718M | ~19% |

| Subsequent quarter | ~$211.5M | ~28.9% |

| Q1 2026 | ~$350M | ~42% |

Cohen’s stated target: Collectibles at “close to a third” of projected full-year revenue. Q1 2026’s 42% quarter already exceeds that target, though full-year mix may settle differently given seasonal variation.

The progression from 10% to 42% in a single category over several years is not a pivot in the speculative sense. It is a methodical expansion of a pre-existing operational model into an adjacent market. What makes it defensible is the competency match. What makes it fragile is the cyclical sensitivity of collector sentiment, a risk worth pricing in rather than dismissing.

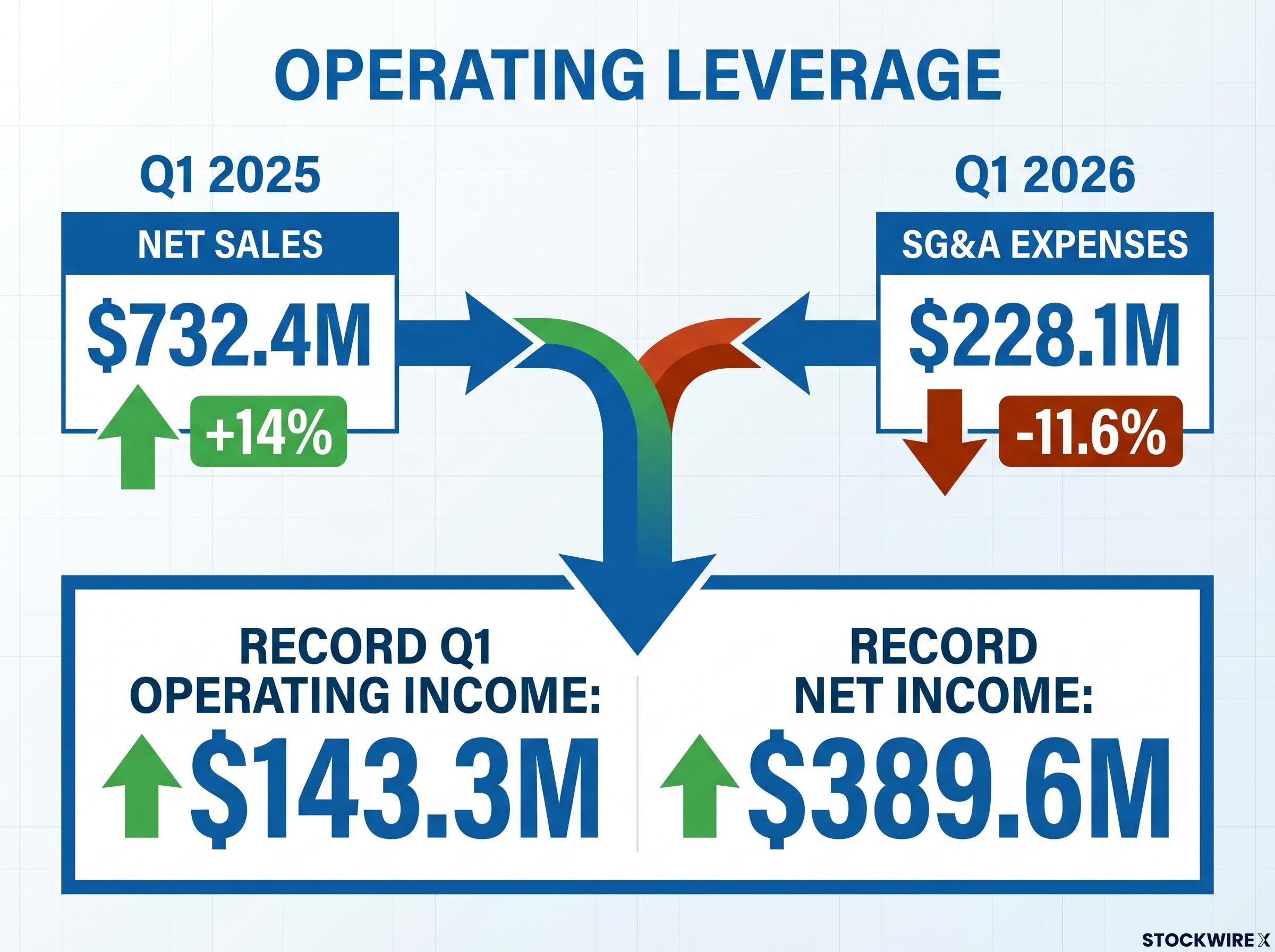

Start with the operating income figure, not the top line. $143.3 million in operating profit for a single quarter is the highest first-quarter result in GameStop’s history. That is the number that tells you whether the strategy is translating into sustainable economics, because operating income captures the relationship between revenue growth and cost discipline in a way that revenue alone does not.

The mechanism behind it is straightforward: selling, general, and administrative (SG&A) expenses, the fixed costs of running the business, fell from $228.1 million to $201.6 million year-over-year. Revenue grew 14% in the same period. When costs decline and revenue rises simultaneously, each incremental dollar of sales converts to profit at a higher rate. That is operating leverage, the financial term for a cost structure becoming more efficient as volume increases.

| Metric | Q1 2025 | Q1 2026 | Change |

|---|---|---|---|

| Net Sales | $732.4M | $835.3M | +14% |

| Operating Income | N/A | $143.3M (record) | Record Q1 |

| Net Income | N/A | $389.6M (record) | Record |

| Free Cash Flow | N/A | $332.9M | N/A |

| SG&A | $228.1M | $201.6M | -11.6% |

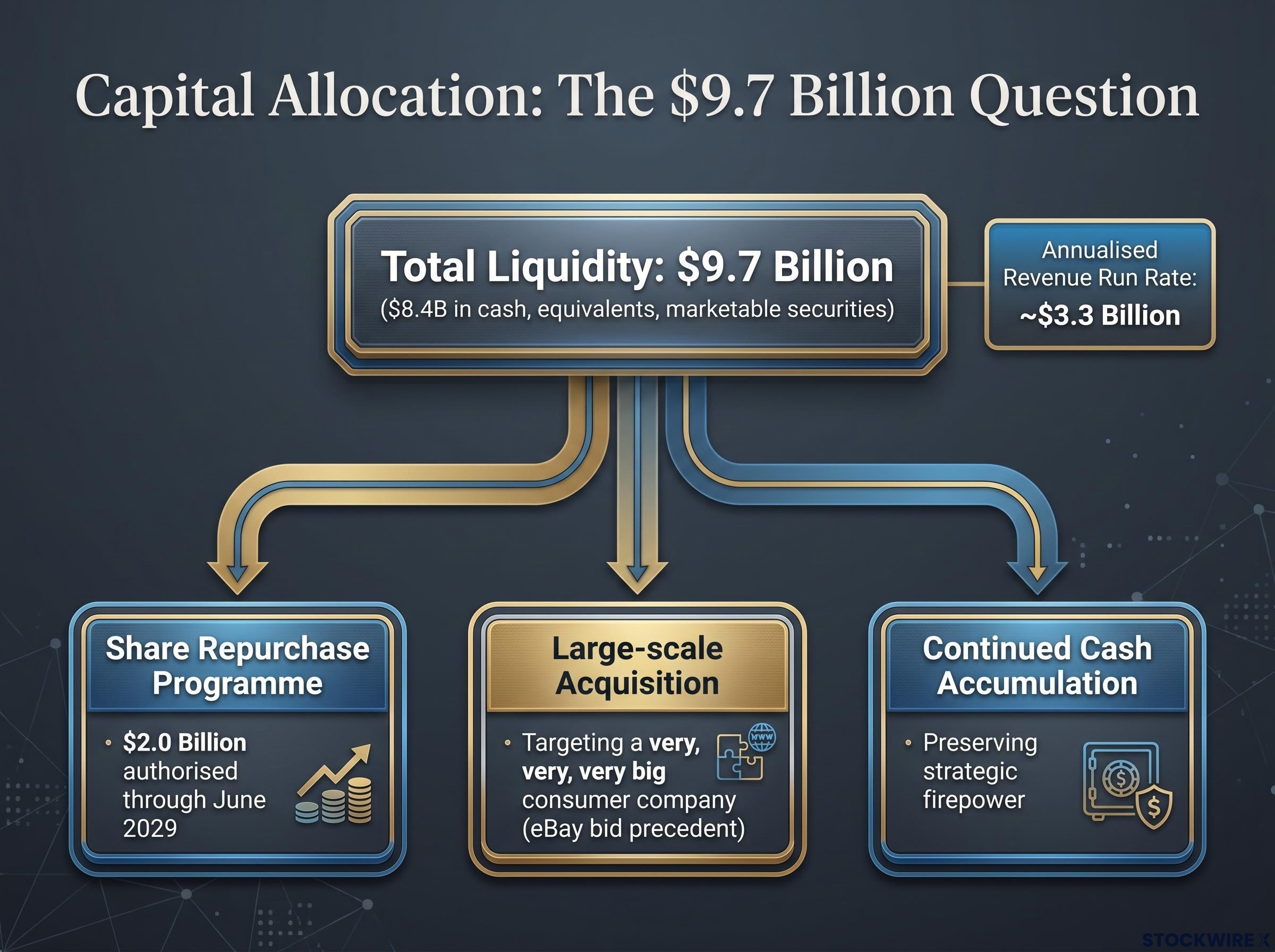

Balance sheet context: Total liquidity of approximately $9.7 billion, including $8.4 billion in cash, cash equivalents, and marketable securities. That figure exceeds the company’s annualised revenue run rate of approximately $3.3 billion.

The multi-year arc reinforces the single-quarter reading. Over that span, gross margin improved by approximately 7 percentage points, and net income swung from a loss of $31 million to a profit of $77.1 million before reaching Q1 2026’s record levels. GameStop reported consecutive annual net profits in fiscal 2024 and 2025 after several years of losses.

The combination of declining SG&A and growing revenue in the same quarter is the single clearest signal that this is structural operating leverage rather than a one-time benefit. If you are evaluating whether the turnaround is sustainable, that relationship is where to anchor.

GameStop’s 10-Q filing with the SEC for the period ended May 2, 2026 discloses the official SG&A, free cash flow, and total liquidity figures underlying the Q1 2026 results, providing the primary regulatory source for the operating metrics discussed here.

A $9.7 billion liquidity position in a retailer generating $3.3 billion in annualised revenue creates an unusual problem. The cash is simultaneously the company’s greatest strategic asset and the source of its most consequential uncertainty.

The conservative baseline is the $2.0 billion share repurchase authorisation confirmed in Q1 2026, running through June 2029. Buybacks are familiar, mechanical, and predictable in their effect on per-share economics. They represent a clear capital return path.

The higher-stakes variable is M&A. Cohen has stated his ambition publicly: a “very, very, very big” acquisition of a larger consumer company.

The deal arithmetic exposed a structural tension: GameStop’s market capitalisation of roughly $10.4 billion was approximately 4.4 times smaller than eBay’s $46.2 billion valuation at the time of the bid, meaning that executing a $56 billion transaction would require a financing structure of a scale Cohen has not previously attempted.

Cohen has described his target as a “very, very, very big” acquisition. For context, the company’s total liquidity of $9.7 billion is roughly three times its annualised revenue.

The eBay bid illustrates both the seriousness and the difficulty. Cohen withdrew a CEO performance award specifically to focus on operating performance and the proposed takeover, a confirmed action that signals genuine intent. eBay’s board rejected the approach. Cohen has publicly criticised the board’s compensation structure relative to its members’ personal share ownership, contrasting it with his own substantial personal stake in GameStop, a framing consistent with his owner-operator philosophy.

Three capital allocation pathways are currently in play:

For anyone holding or evaluating GameStop as an equity, the capital allocation question is ultimately more consequential than the operating results. A $9.7 billion deployment decision will determine whether the turnaround story compounds or gets diluted by an expensive and unfamiliar acquisition.

Cohen has suggested that financial media outlets are reluctant to acknowledge the operational turnaround because doing so would require conceding that the earlier meme-stock narrative was analytically inadequate. Whether you accept that framing or not, the gap between the narrative and the disclosed fundamentals has become substantial enough to constitute an analytical phenomenon in its own right.

The January 2021 episode worked through short squeeze mechanics that were entirely divorced from GameStop’s operating performance: forced covering by short sellers, layered on top of options market maker hedging, produced a self-reinforcing price spiral that embedded the meme-stock label so deeply that it has continued to suppress serious analytical engagement five years later.

The contrast, stated plainly:

Cohen has also expressed the view that proven founders who risk personal capital are systematically undervalued relative to professional managers by financial media coverage. Several external analyses now frame the company as transitioning “from meme stock to M&A machine,” suggesting the characterisation is beginning to shift.

The media narrative gap is not merely a curiosity. It means the market price has been set in part by a story that has diverged from operational reality. If you close that information gap now, you are working from a more accurate base than the prevailing consensus suggests, whether your conclusion is bullish, bearish, or somewhere between.

The turnaround thesis is supported by the data, but accepting it without pricing in specific vulnerabilities is a different analytical error than dismissing the business as a meme stock. Three risks warrant direct attention, ranked by current materiality:

The goal here is precision rather than scepticism. These are the specific places where the thesis could break, and knowing them is more useful than a general disclaimer.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The operational transformation is confirmed by the multi-year data arc. From the failed Chewy playbook through the collectibles pivot to record Q1 2026 results, GameStop under Cohen has built a demonstrably different business. Consecutive profitable years, record operating income of $143.3 million, and a collectibles segment that has grown from ~10% to ~42% of quarterly revenue represent facts, not speculation.

What remains contingent is whether the story compounds from here. The $2.0 billion buyback provides a capital return baseline. The M&A ambition introduces asymmetric outcomes. Cohen’s full-year collectibles target of “close to a third” of revenue sits below the Q1 2026 actual, which means subsequent quarters will reveal whether the first quarter was an outlier or a new baseline.

The most useful thing to carry forward is the specific variables to watch:

Forward-looking statements in this article are speculative and subject to change based on market developments and company performance. Past performance does not guarantee future results.

The turnaround is real. The next chapter is not yet written. The difference between a grounded assessment and a meme-stock reflex is knowing which questions to ask next.

—

Ryan Cohen repositioned GameStop around a collectibles-led retail model, leveraging the company's existing pre-owned merchandise competencies to expand into trading cards and graded collectibles. Collectibles now account for 42% of quarterly revenue, up from roughly 10% before the pivot.

As of Q1 2026, GameStop holds approximately $9.7 billion in total liquidity, including $8.4 billion in cash, cash equivalents, and marketable securities, on a balance sheet with zero debt.

GameStop reported record Q1 net sales of $835.3 million (up 14% year-over-year), record Q1 operating income of $143.3 million, record net income of $389.6 million, and free cash flow of $332.9 million, while SG&A expenses fell 11.6% to $201.6 million.

GameStop has authorised a $2.0 billion share repurchase programme running through June 2029, and CEO Ryan Cohen has publicly stated ambitions to make a very large acquisition of a consumer company, with a rejected approach for eBay serving as the most concrete precedent.

The three primary risks are collectibles cyclicality (the category is driven by collector sentiment and secondary-market pricing, not stable consumption), continued structural pressure on brick-and-mortar retail, and capital allocation uncertainty from Cohen's stated ambition to deploy the $9.7 billion liquidity position in a large-scale acquisition.