Vanguard VIHY Declares First Distribution at 49.49 Cents per Unit

2 hrs ago

Australia’s capital gains tax discount sits at the centre of one of the country’s most persistent investment policy debates. In May 2026, that debate intensified again, with investment strategists fielding a surge of questions about how a potential reduction or removal of the 50% CGT discount would alter the relative appeal of growth assets versus income-producing equities. The discussion has direct, structural implications for how Australian investors think about franked dividend stocks, not because reform is confirmed, but because the underlying tax mechanics reward those who understand them before policy shifts arrive. What follows is an analytical framework for assessing the franked dividend advantage under both the current system and a range of potential CGT scenarios, grounded in verifiable tax rules and the structural logic of Australia’s globally unusual imputation system.

The CGT discount has not been legislated away. No Bill sits before Parliament. No Treasury consultation document proposes a specific replacement structure as at 26 May 2026. And yet the investment logic of preparing for a structural tax shift does not require a confirmed law; it requires an understanding of what the current system actually does and what changes would mean in practice.

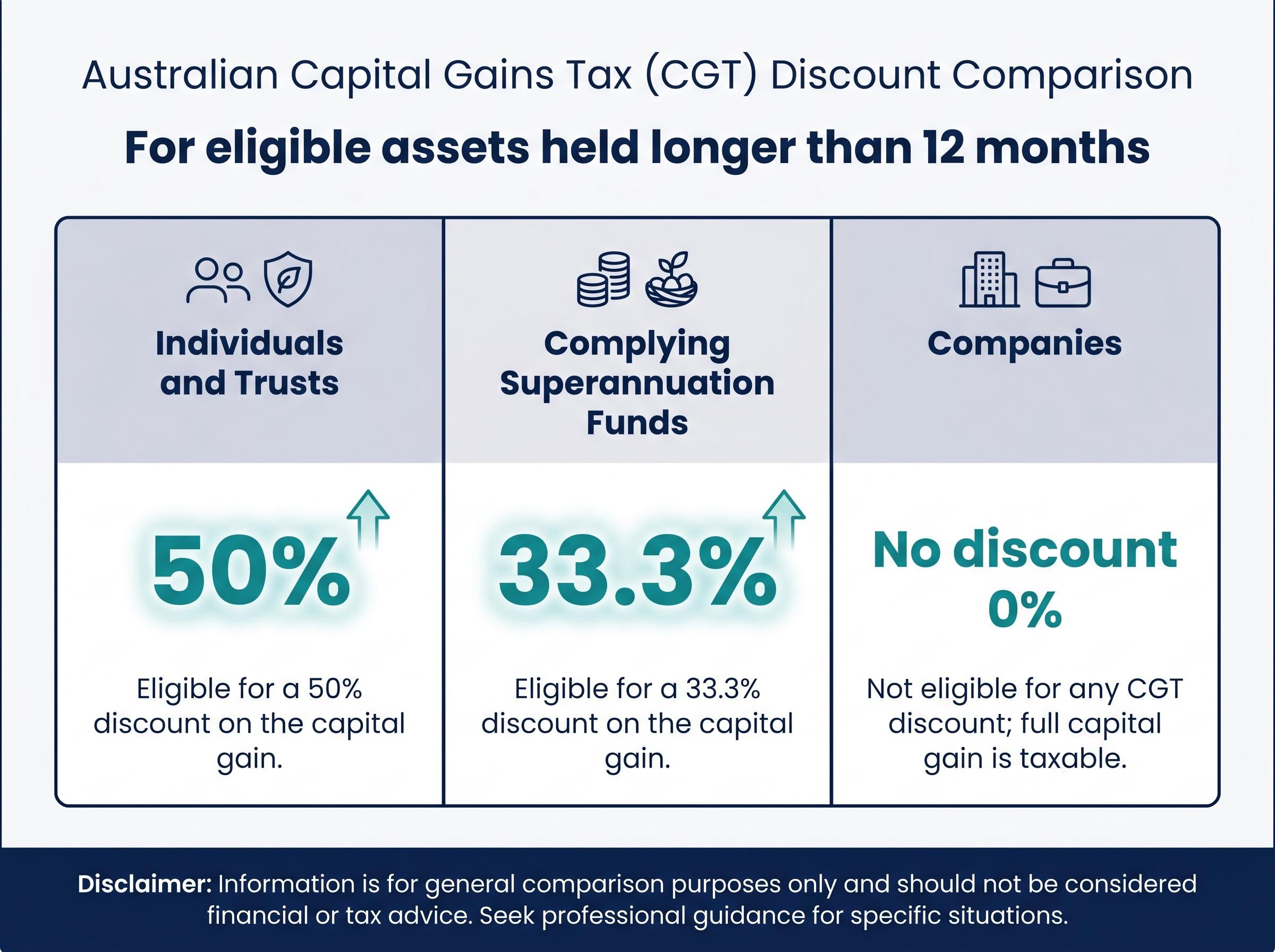

Australia’s existing CGT framework provides the following discounts for eligible assets held longer than 12 months:

These rates are confirmed by current ATO guidance and have remained unchanged for over two decades.

Commentary reported by Bloomberg on 13 May 2026, citing Rob Wilson, Director of Investment Strategy at Selfwealth by Syfe, characterised proposals to reduce or replace the discount as among the most significant potential restructurings of Australia’s CGT framework in recent memory. The proposals remain in the realm of public policy debate rather than active legislation, but the analytical exercise they prompt is real.

The 50% discount converts effective tax rates on long-held capital gains. An individual on the top marginal rate of 47% (including the Medicare levy) pays an effective rate of approximately 23.5% on a qualifying capital gain, roughly half what they would pay on salary or interest income at the same marginal rate.

This preferential treatment has historically tilted portfolios toward capital-growth assets. Reducing or eliminating that discount would narrow the gap between growth and income in after-tax terms, a shift with direct portfolio construction consequences.

Australia’s dividend imputation system operates on a simple principle: corporate profits should not be taxed twice. When an Australian company pays tax on its earnings at the corporate rate, it attaches franking credits to dividends distributed to shareholders. Those credits represent tax already paid. Shareholders then use the credits to offset their personal income tax liability on the dividend.

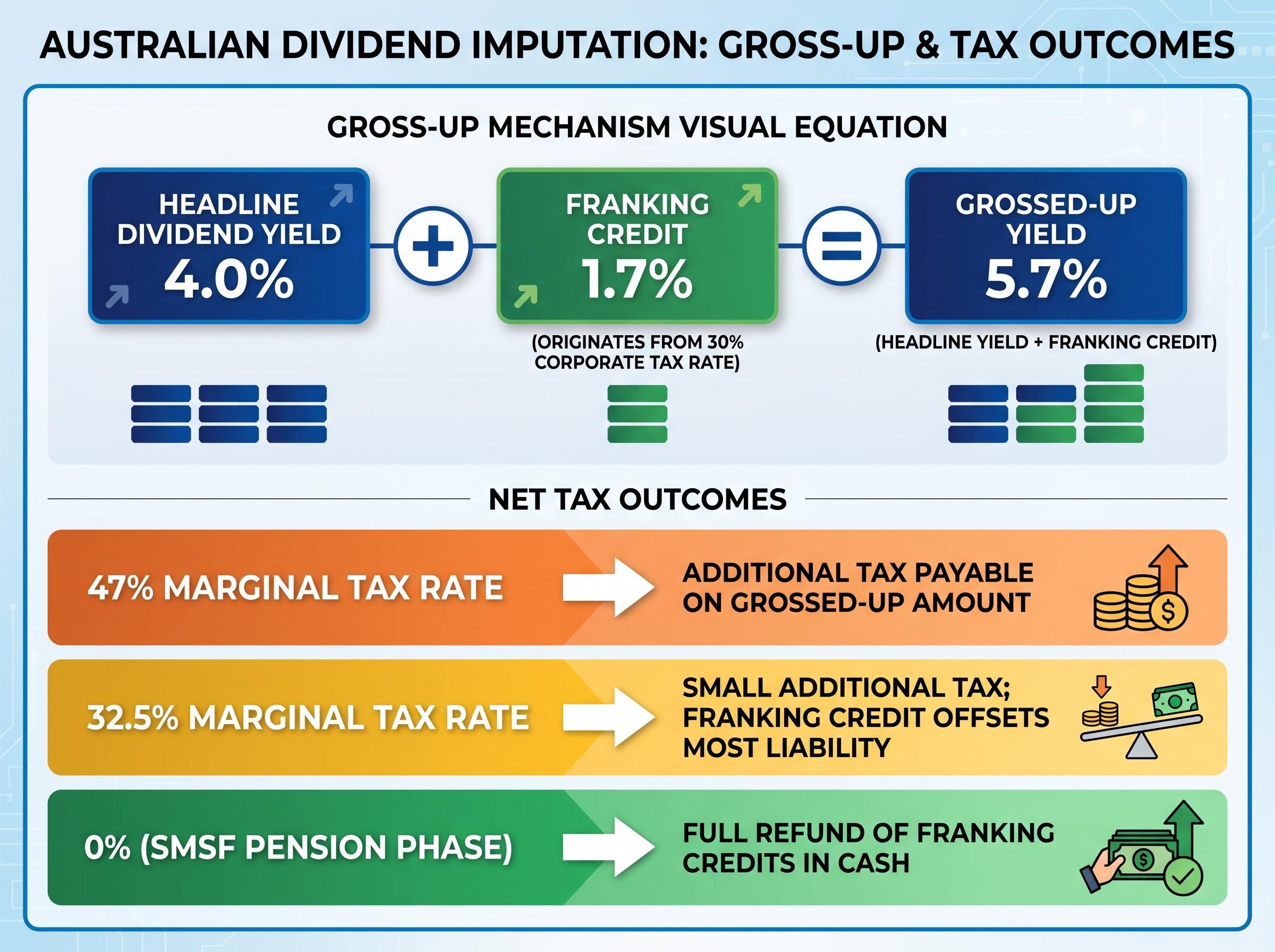

The franking credit mechanics that govern this system are more precise than most investors realise: a company paying 30% corporate tax on $100 of profit distributes $70 in cash to shareholders along with a $30 credit, which the ATO then applies against the shareholder’s personal tax liability on the grossed-up $100 amount.

The mechanism produces a measurable after-tax advantage that varies by marginal tax rate. Consider a 4% headline dividend yield from a company paying the standard 30% corporate tax rate, fully franked.

Grossed-up yield illustration: A 4% fully franked dividend from a company paying 30% corporate tax equates to a grossed-up yield of approximately 5.7% for an Australian resident shareholder. The franking credit effectively returns a portion, or in some cases all, of the corporate tax already paid.

The following table illustrates how the after-tax benefit shifts across different marginal tax rates:

| Marginal tax rate | Headline dividend yield | Franking credit value | Grossed-up yield | Net tax outcome |

|---|---|---|---|---|

| 47% (top bracket) | 4.0% | 1.7% | 5.7% | Additional tax payable on grossed-up amount |

| 32.5% (middle bracket) | 4.0% | 1.7% | 5.7% | Small additional tax; franking credit offsets most liability |

| 0% (SMSF pension phase) | 4.0% | 1.7% | 5.7% | Full refund of franking credits in cash |

The ATO confirms the dividend imputation system operates unchanged as at May 2026, with no proposed alterations to its mechanics.

Self-managed superannuation funds in pension phase pay zero tax on earnings. Excess franking credits are fully refunded in cash under current rules, making fully franked dividends exceptionally efficient for this cohort. This refund mechanism is a key reason the franking credit debate remains politically sensitive: the beneficiaries represent a large and well-organised segment of the electorate.

The comparative logic runs in three steps:

Rob Wilson of Selfwealth by Syfe, as reported by Bloomberg on 13 May 2026, characterised the proposed reforms as potentially altering the balance of appeal between high-growth shares and steady income-producing investments. Wilson’s commentary framed the changes as supportive of the existing tax rationale for holding quality Australian dividend-paying stocks.

These proposals remain unconfirmed as at 26 May 2026. No Bill or exposure draft has been tabled. The analytical value, however, lies in understanding the directional shift: any reduction in the CGT discount tilts the after-tax comparison toward income assets.

The broader investment tax changes announced in the 2026-27 Federal Budget extend well beyond the CGT discount, with negative gearing quarantined on established residential properties effective 12 May 2026 and franked-dividend-paying equities identified by major bank economists as likely beneficiaries of the reallocation of investor capital away from residential property.

Investment property has historically benefited from two concurrent tax advantages: negative gearing deductions against rental income and the 50% CGT discount on eventual sale. Proposals to restrict negative gearing on existing residential dwellings, combined with a less favourable CGT structure, would reduce the after-tax return profile of investment property relative to fully franked ASX equities.

This framing remains conditional. Investors should monitor official Treasury and Parliamentary channels for any confirmed legislative developments before drawing firm conclusions.

The franking credit system delivers its largest after-tax advantage to investors whose marginal tax rate sits furthest below the corporate tax rate. Not all investors benefit equally.

The franking credit system delivers its largest after-tax advantage to investors whose marginal tax rate sits furthest below the corporate tax rate at which the credits were generated.

High-growth-oriented investors and those with significant property portfolios face the most material reassessment if CGT reforms proceed, as the structural tilt that currently favours their strategy would narrow.

The structural tax case for high-quality franked dividend stocks is strong under current law. It becomes relatively stronger under any scenario in which the CGT discount is reduced, because the franking credit advantage is independent of CGT settings.

Three steps provide a practical starting point:

Repositioning a portfolio before legislation is confirmed carries its own risks, including the possibility that reforms do not proceed or are substantially altered during the legislative process. ATO guidance and Treasury consultation documents remain the primary sources for tracking confirmed developments.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

These reform scenarios are speculative and subject to change based on political developments and legislative outcomes. Past performance does not guarantee future results.

Australia’s dividend imputation system is a globally unusual feature. Few developed markets operate a full imputation framework, making ASX income stocks relatively distinctive in international terms. The structural advantage for resident shareholders exists entirely independent of any CGT reform debate.

Whatever its outcome, the reform discussion has performed a useful function: prompting investors to re-examine whether their portfolio’s current tilt toward capital growth is actually tax-optimal for their personal circumstances. That question has value regardless of what Parliament ultimately decides.

For investors who want to stress-test whether the proposed replacement actually achieves its stated policy goals, our deep-dive into the structural design flaws of the proposed CGT replacement models a tapered alternative against the government’s indexation-plus-floor approach, showing a projected tax difference of more than $104,000 over 20 years on a $100,000 portfolio at 10% annual growth.

The franked dividend advantage is not a bet on a particular policy outcome. It is a feature of the current Australian tax system that already rewards income-focused investors, and which becomes more compelling the more the CGT discount on capital gains is reduced.

The ATO confirms the imputation system remains fully operational as at May 2026. Bloomberg’s characterisation of the proposed reforms as potentially among the most significant restructurings of Australia’s CGT framework reinforces why the debate prompted broad reassessment, but the structural logic of franking credits does not depend on that debate’s resolution.

The structural tax advantage of fully franked Australian equities is real under current law and amplifies if CGT reforms reduce the discount on capital gains. That finding holds whether the current policy debate produces legislation or subsides without action.

The investors best positioned to respond to any eventual reform will be those who already understand the mechanics of franking credits, their personal marginal rate, and how both interact with their portfolio construction. Treating the policy debate as a prompt for review, rather than a trigger for hasty repositioning, is the more defensible approach.

As Treasury and Parliamentary developments unfold, related analysis on Australian dividend investing, SMSF tax strategy, and portfolio income allocation may warrant further reading. Official ATO and Treasury channels remain the authoritative sources for confirmed legislative updates.

Australia's CGT discount allows individuals and trusts to reduce a capital gain by 50% on assets held for more than 12 months, effectively halving the tax payable. Complying superannuation funds receive a one-third discount, while companies receive no discount at all.

Franking credits represent corporate tax already paid by an Australian company on its profits. When a fully franked dividend is paid, shareholders can use those credits to offset their personal income tax liability on the grossed-up dividend amount, with low-tax investors and SMSFs in pension phase often receiving a cash refund of excess credits.

If the 50% CGT discount were reduced or removed, the after-tax advantage of capital growth assets would narrow, making the income return from fully franked dividend stocks relatively more attractive by comparison. Franking credits are independent of CGT settings, so their benefit is unaffected by any changes to the discount.

SMSFs in pension phase benefit most because they pay zero tax and receive excess franking credits as a full cash refund. Retirees and low-bracket individuals also gain significantly, while top-bracket investors at 47% still receive a partial offset though additional tax remains payable on the grossed-up dividend.

Investors should review the current split between growth assets and franked-dividend-paying equities in their portfolio, assess their marginal tax rate to estimate the franking credit benefit, and monitor official ATO and Treasury channels for any confirmed legislative changes before repositioning.