Australia’s trimmed mean inflation is already running at 3.5% year-on-year, and the most disruptive effects of the Middle East oil shock have not yet hit the data. That is the uncomfortable starting point facing the Reserve Bank of Australia (RBA) ahead of its May 5, 2026 board meeting.

The March 2026 Consumer Price Index (CPI) data, released April 29, showed headline inflation surging to 4.6% year-on-year, driven by a 32.8% monthly spike in automotive fuel costs. NAB economists Gareth Spence and Michael Hayes argue the Q1 figures are already backward-looking: the bigger inflationary wave from second-round energy pass-through is still building and will be most visible in Q2 and Q3 2026. All four major Australian banks now forecast a 25 basis point rate hike at the May meeting, which would bring the cash rate to 4.35%.

What follows unpacks why that consensus exists, explains how second-round inflation works and why it matters more than the headline fuel number, and translates the rate outlook into concrete terms for mortgage holders, savers, and investors navigating a tightening cycle that may not end until mid-to-late 2027.

The inflation picture heading into May is worse than the headline number suggests

What the Q1 quarterly result actually showed

At first glance, the Q1 2026 trimmed mean CPI print looked manageable. The quarterly figure came in at 0.8%, with the annual rate tracking at 3.5% year-on-year. Both readings sat marginally below NAB’s 0.9% quarterly forecast and the RBA’s own February Statement on Monetary Policy projection.

The modest undershoot, however, was driven by travel-related price volatility rather than any genuine softening of broad price pressures. Strip out that noise and the underlying picture looks far less comforting.

The distinction between trimmed mean versus headline CPI is central to how the RBA reads the current environment: headline CPI captures the full fuel price spike, while trimmed mean strips out the most volatile items to reveal the persistent price pressures the board is actually targeting.

Approximately two-thirds of tracked CPI basket items are still rising at an annualised pace above 3%, a signal of inflationary breadth that a single quarterly beat cannot mask.

Why March monthly data changes the picture

The March monthly data tells a materially different story:

- Headline CPI jumped to 4.6% year-on-year (from 3.7% in February), above NAB’s 4.7% forecast and consensus expectations of 4.8%

- Monthly trimmed mean edged up to 3.3% year-on-year, rising on a month-on-month basis from 3.2% the prior month

- Electricity prices held flat month-on-month in March but remained 25.4% higher year-on-year following the January spike when government rebates lapsed

For anyone monitoring the RBA’s next move, the raw quarterly headline beat is misleading. The board will be reading the breadth and persistence of underlying price pressures, and those readings point in one direction.

When big ASX news breaks, our subscribers know first

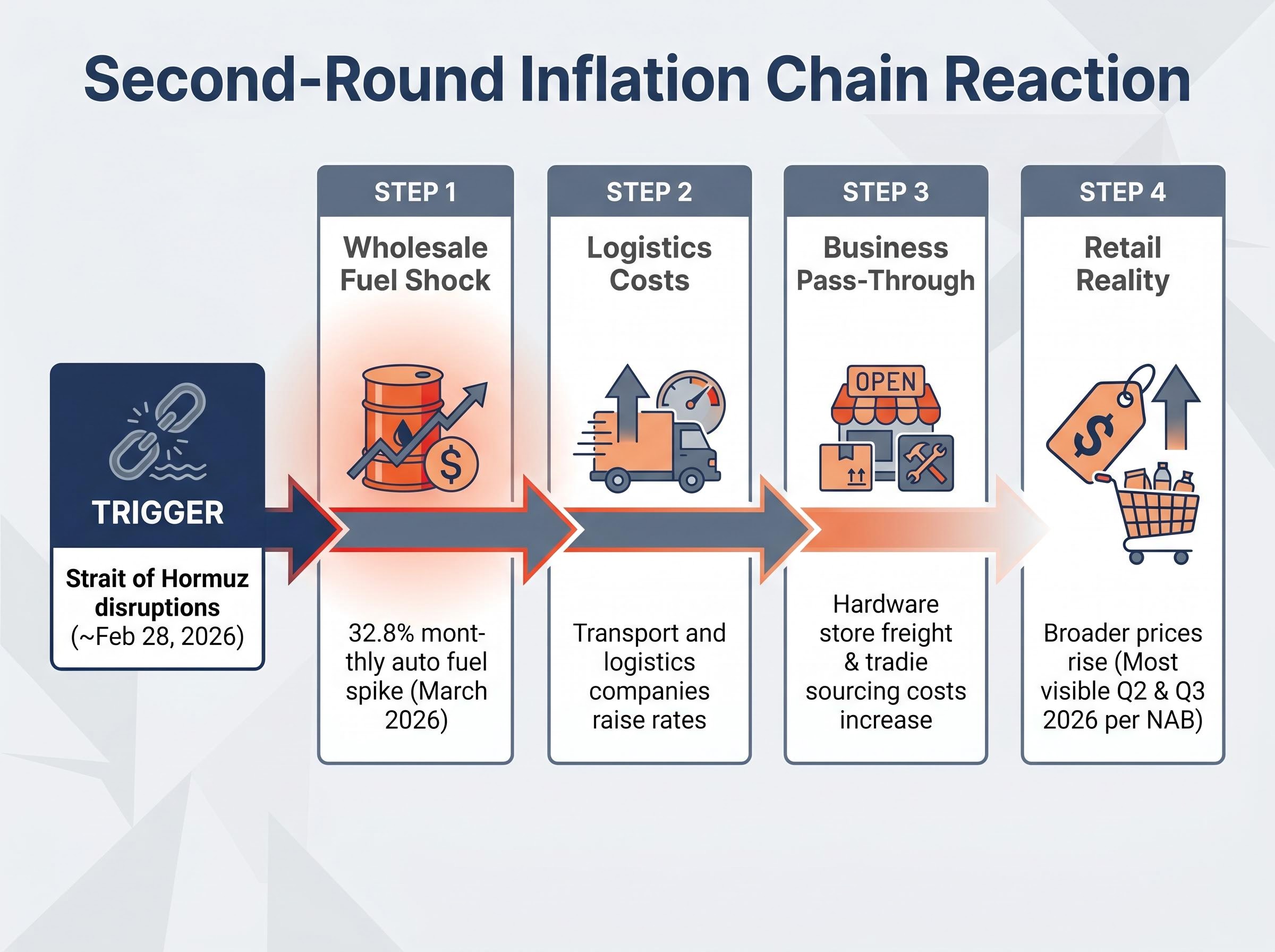

How a 32.8% fuel price spike becomes a services inflation problem six months later

What “second-round inflation” means and why it matters more than the initial shock

Second-round inflation is what happens after the initial commodity price shock works its way through the broader economy. The first-round effect is the direct price increase: fuel at the bowser costs more. The second-round effect is the chain reaction that follows, as businesses absorb higher energy and logistics costs and pass them through to customers across sectors that have nothing to do with petrol.

The sequence runs in a predictable order:

- Fuel costs rise at the wholesale level

- Transport and logistics companies raise their rates to cover higher fuel bills

- Businesses across goods and services, from supermarkets to construction firms, face increased production and delivery costs

- Retail prices rise across the broader economy

Consider a practical example: a logistics company’s fuel bill rises, so it charges more to deliver goods. A hardware store raises shelf prices to cover the higher freight cost. A tradie quotes higher for a renovation because materials cost more to source and transport. The initial shock at the bowser has become a services inflation problem months later.

Central banks find second-round effects harder to manage than first-round shocks. Commodity prices can reverse quickly if supply disruptions ease; embedded business cost structures are stickier and take longer to unwind.

The global inflation transmission channels triggered by crude above $100 per barrel extend well beyond fuel at the bowser: aviation fuel pricing, industrial feedstock costs, and logistics contract rates are all repricing simultaneously, and central banks across developed markets are being forced to reassess their rate paths in response to a supply shock that domestic policy tools cannot directly address.

NAB explicitly identifies Q2 and Q3 2026 as the quarters when second-round effects will be most visible, because supply chain cost increases take time to work through to retail pricing.

The 32.8% monthly surge in automotive fuel costs recorded in March 2026 followed Strait of Hormuz disruptions that began around February 28, 2026 and have continued for approximately 4-5 weeks, with projections for a further 3-6 months of disruption.

The ABS March 2026 CPI release confirmed the 32.8% monthly surge in automotive fuel costs that sits at the centre of the current inflation debate, alongside the trimmed mean and headline figures that have shifted the RBA’s risk calculus toward further tightening.

Early signals of pass-through are already appearing. New dwelling purchase costs accelerated to 0.48% month-on-month in March, up from 0.15% in February, an early indicator of oil-derived materials and logistics costs feeding into construction. Market services inflation (excluding rents) held at 0.27% month-on-month in March, remaining above 3% year-on-year.

The government’s halving of the fuel excise (announced around March 30, 2026) addresses only one channel of transmission. Several others sit entirely outside its scope:

| Inflation Channel | Why Fuel Excise Cut Does Not Help |

|---|---|

| Automotive fuel | Partially offset at the bowser, but does not address wholesale cost increases already embedded in logistics contracts |

| Aviation fuel | Jet fuel is not covered by the excise measure; airlines face full cost pass-through from higher crude prices |

| Plastics and petrochemicals | Industrial feedstock costs are set by global crude and refining margins, not domestic fuel excise policy |

| Construction materials | Bitumen, PVC, and transport-intensive building supplies are priced off oil and logistics costs beyond the excise’s reach |

Understanding second-round effects is why economists look beyond the fuel line item. The real inflation risk from the oil shock will be measured in non-energy prices across mid-2026, not in the petrol price at the bowser today.

Why the RBA is caught between persistent domestic inflation and a new external shock

The starting position was already uncomfortable

Core inflation was tracking at approximately 3.5% year-on-year before the oil shock arrived. The RBA had not returned inflation to its 2-3% target band prior to the new external disruption, leaving the board with less room to absorb upside surprises than it had in prior tightening cycles.

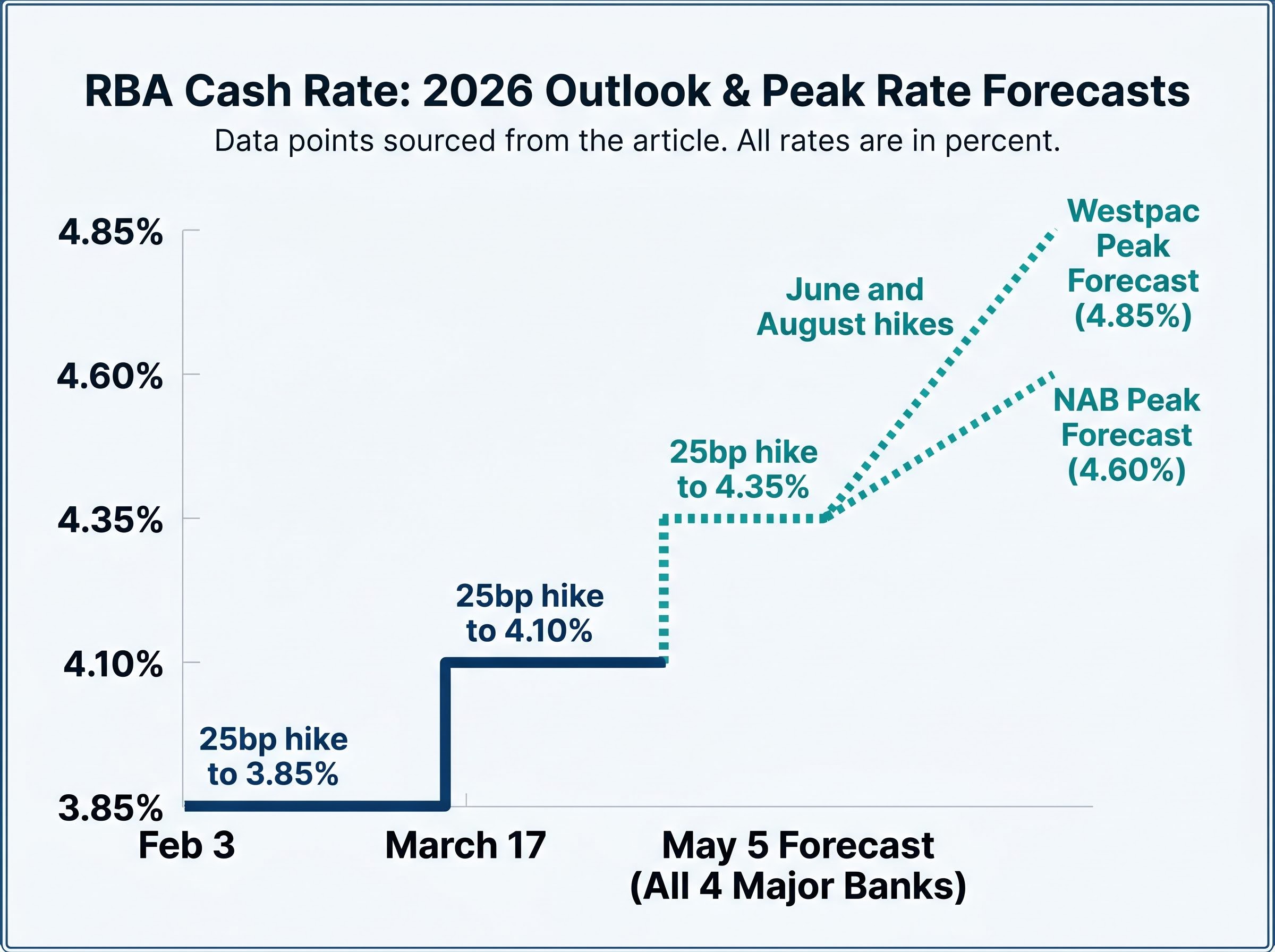

The February and March hikes, a 25bp increase to 3.85% on February 3 followed by another 25bp to 4.10% on March 17, represented consecutive tightening moves that reversed the 2025 rate cut cycle and reset borrower expectations.

The forward signalling has been unambiguous

The RBA’s March 17 media release (MR-26-08) confirmed the hike to 4.10% and flagged four specific risk factors:

The RBA’s March monetary policy decision confirmed the board’s explicit concern about second-round effects flowing through to non-fuel prices, placing the burden of proof firmly on incoming inflation data to justify any pause rather than continued tightening.

- Sharply higher fuel prices adding to inflation if sustained

- Greater capacity pressures in the economy

- Rising short-term inflation expectations

- Concern about second-round effects flowing through to non-fuel prices

That combination of signals constitutes a clear forward bias toward further tightening. The RBA is not hiking from a position of comfort; it is responding to an external shock while already battling persistent domestic inflation. That narrowing of options increases the risk of a longer tightening cycle than markets had priced in during 2025.

Where the major banks diverge on how far rates will go

All four major banks, Commonwealth Bank of Australia, Westpac, ANZ, and NAB, forecast a 25bp hike at the May 5 meeting. Market pricing assigns approximately 72-85% probability to the move. The cash rate would reach 4.35%.

That consensus is settled ground. The real tension lies in the divergence on the peak rate and how long it persists.

| Bank | May 5 Forecast | Peak Rate Forecast | When Relief Arrives |

|---|---|---|---|

| CBA | +25bp to 4.35% | Not specified | Not specified |

| Westpac | +25bp to 4.35% | 4.85% (further hikes in June and August) | Extended cycle; no near-term relief |

| ANZ | +25bp to 4.35% | Not specified | Not specified |

| NAB | +25bp to 4.35% | 4.60% | Hold extending to mid-to-late 2027 |

Westpac’s trajectory is the most aggressive, citing prolonged Strait of Hormuz disruptions and rapid second-round pass-through as the basis for additional 25bp hikes in June and August, pushing the cash rate to a peak of 4.85%. NAB’s central forecast sits at 4.60%, with an extended hold through mid-2027 before any relief.

NAB has explicitly acknowledged upside risk to its own central forecast, framing the 4.60% peak as a base case rather than a ceiling.

The gap between 4.60% and 4.85% is not academic. It represents a material difference in mortgage repayments and investment return assumptions for Australian households and businesses planning through 2026 and into 2027.

The next major ASX story will hit our subscribers first

How Australian households should plan their finances in a sustained high-rate environment

The institutional forecasts translate into specific financial pressure for Australian households. Approximately one-third of Australian borrowers hold variable rate mortgages and face immediate pass-through from each 25bp increase.

The cumulative effect is substantial. Three consecutive hikes (February, March, and May) add 75 basis points to variable mortgage costs in the space of three months, reversing the relief borrowers had anticipated from the 2025 rate cut cycle.

The impacts differ across borrower categories:

- Variable rate holders face immediate monthly repayment increases with each hike, and no near-term prospect of relief under any major bank forecast

- Fixed-rate borrowers approaching rollover will refinance into a materially higher rate environment than when their fixed terms began

- Savers and deposit holders benefit from higher term deposit and savings account rates, partially offsetting the cost-of-living squeeze

NAB’s hold-to-mid-2027 scenario is the key planning horizon. There is no near-term relief cycle to anticipate, and household budgets need to be stress-tested against rates remaining at 4.35%-4.85% for 12-18 months.

Financial planners warn that tighter policy through 2027 will delay meaningful mortgage cost reduction, straining budgets already under pressure from sticky services inflation.

Labour market conditions have remained broadly intact through the current tightening phase, providing some household income support even as mortgage costs rise. That partial offset, however, does not change the core planning requirement: Australian households should be budgeting for the upper end of the forecast range rather than the base case.

For investors wanting to translate the rate outlook into specific portfolio action, our dedicated guide to ASX portfolio positioning for inflation covers a scenario-balanced approach spanning bonds, credit, global equities, and cash equivalents, with analysis of how each allocation performs under both a sustained 4.85% peak and a faster-than-expected rate reversal driven by growth weakness.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The RBA’s May decision will set the tone for Australian monetary policy through 2027

The May hike itself is widely expected and is no longer the story. What matters is what it signals about the length and severity of the tightening cycle ahead.

The oil shock has shifted the inflation risk distribution upward, extending the period of restrictive monetary policy well beyond what markets had priced in mid-2025. The fuel excise halving provides temporary headline CPI relief but will not alter the RBA’s view of underlying inflation momentum, particularly as second-round effects build through Q2 and Q3 2026.

Structural deflationary forces, including AI-driven productivity gains and global supply chain rebalancing, are creating long-run counterweights that sit entirely outside the current oil shock narrative, and the tension between these forces and the near-term commodity spike will shape how long the RBA needs to hold restrictive policy before inflation returns sustainably to target.

Westpac has revised its headline CPI forecast to peak at approximately 6% year-on-year in mid-Q2 2026, with trimmed mean CPI reaching approximately 4% year-on-year later in 2026.

The next inflection point for markets and households will be the RBA’s updated Statement on Monetary Policy, released alongside or following the May 5 decision. Three signals deserve close attention in the weeks ahead:

- The updated SoMP inflation and growth forecasts, which will embed the oil shock’s arithmetic into the official policy path

- The June board meeting decision, which will reveal whether the RBA views May as a pause point or a stepping stone

- The Q2 CPI release timeline, which will provide the first hard data on second-round pass-through effects

The RBA’s revised forecasts in the May SoMP will be the most consequential economic document for Australian households and investors in the first half of 2026. The May rate decision sets the tone; the SoMP will define the trajectory.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.