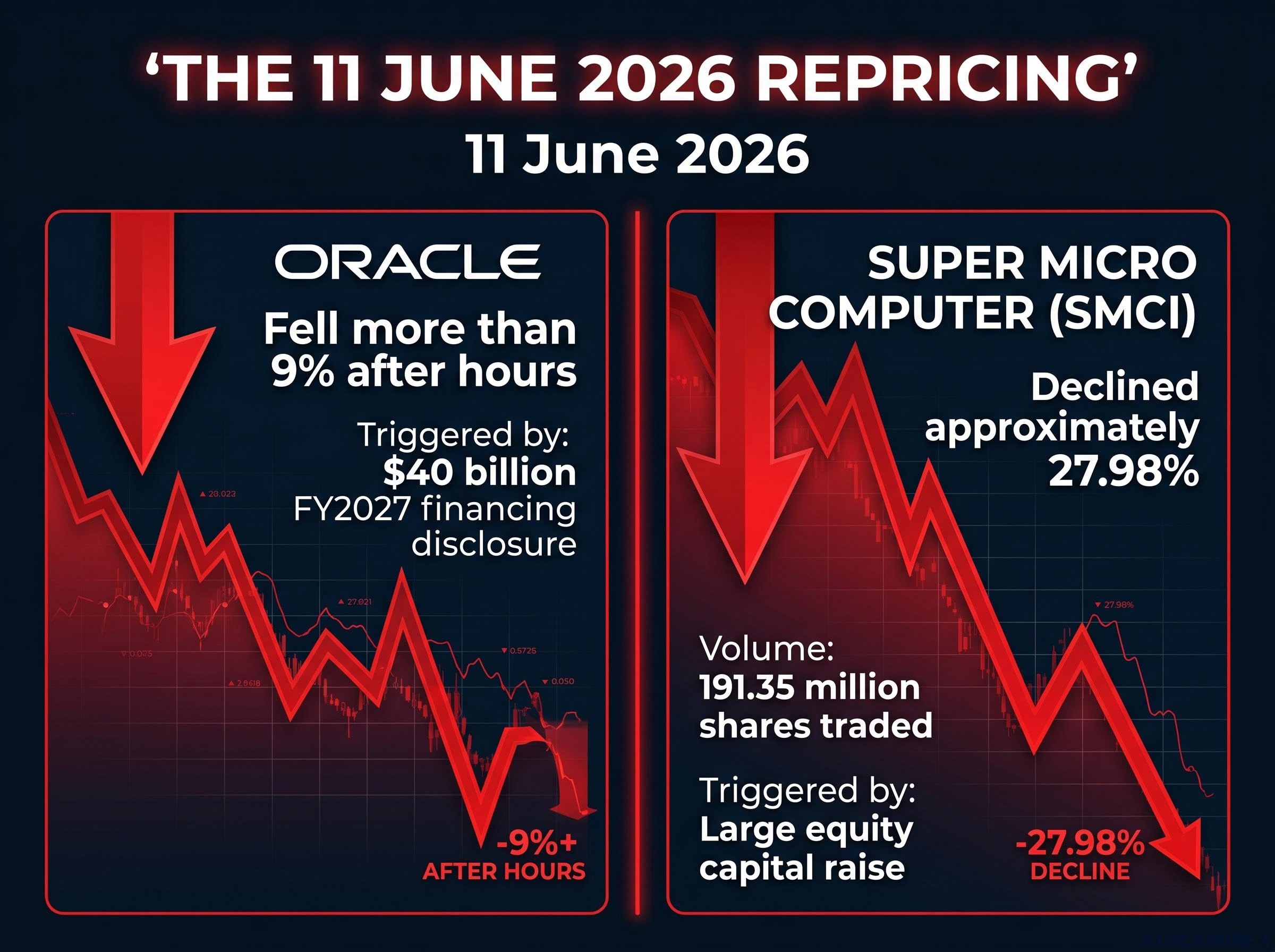

Oracle beat earnings expectations and still lost more than 9% in after-hours trading on 11 June 2026. Revenue topped consensus. Profit exceeded forecasts. Management raised full-year adjusted earnings per share guidance. None of it mattered. What mattered was the $40 billion financing plan Oracle announced for fiscal 2027, a figure that forced the market to confront a question the income statement could not answer: how much debt is too much debt when the cash flows meant to service it have not yet materialised? The AI debt problem facing infrastructure investors is no longer theoretical. In the same session, Super Micro Computer shares collapsed nearly 28%, triggered not by missed results but by another large capital raise. This article examines the financial mechanics behind why strong earnings prints are now being punished across the AI infrastructure sector, what Oracle’s balance sheet and margin data reveal about the sustainability of the current build-out cycle, and what the pattern signals for investors evaluating any name in this category.

When beating expectations is not enough

On every conventional metric, Oracle’s quarterly report delivered. Revenue beat. Profit beat. Full-year adjusted EPS guidance was raised. For investors trained to read earnings through the lens of beat-or-miss, the report should have been a buy signal.

It was not. The $40 billion fiscal 2027 financing announcement arrived alongside those numbers, and the market’s reaction was immediate: it ignored the income statement and repriced the balance sheet.

“The steep price of AI spooks investors.” MarketWatch, reporting on Oracle’s after-hours decline

Vital Knowledge described the quarter as adequate, noting continued strong backlog growth and better-than-feared cash performance. The caveat was blunt: prolonged heavy cash outflows lie ahead, and the financing announcement confirmed it. The analyst community’s focus had shifted from what Oracle earned to what Oracle owes and plans to borrow.

This was not an isolated reaction. The same session produced a parallel signal:

- Oracle fell more than 9% after hours following its $40 billion FY2027 financing disclosure

- Super Micro Computer (SMCI) declined approximately 27.98% in a single session on 191.35 million shares traded, triggered by its own large equity capital raise

Two companies, two different products, one shared catalyst: the market repricing the cost of AI ambition in real time.

When big ASX news breaks, our subscribers know first

The balance sheet behind the sell-off

Oracle did not enter the $40 billion financing announcement from a position of balance sheet strength. It entered from a position that was already deeply leveraged and cash-negative, which is why the additional raise compounded rather than initiated concern.

The numbers tell the story in sequence.

The AI investment boom now accounts for 4.9% of US GDP, a share that has surpassed both the dot-com era peak of approximately 4.2% and the cloud buildout peak of approximately 3.8%, placing the current cycle in historically unprecedented territory for capital deployment relative to the size of the economy.

| Metric | Figure |

|---|---|

| Long-term debt | ~$124.7 billion |

| Trailing 12-month free cash flow | ~negative $24.7 billion |

| Calendar 2026 CapEx | $55.66 billion |

| 2026 combined debt and equity financing | $45-50 billion |

| FY2027 additional financing plan | $40 billion |

Each row adds pressure to the one above it. Approximately $124.7 billion in long-term debt is already on the books. Free cash flow is running at roughly negative $24.7 billion on a trailing basis, driven by data centre and server spending. The company has already raised or planned $45-50 billion in combined financing for 2026. And now it has signalled another $40 billion for fiscal 2027.

TheStreet has characterised Oracle as a “risky bet on artificial intelligence” whose stock is disproportionately sensitive to AI sentiment shifts precisely because of this leverage profile. The characterisation is difficult to dispute on the numbers alone.

From $50 billion to $55 billion: when CapEx targets become floors

Oracle’s calendar 2026 capital spending of $55.66 billion exceeded its own earlier internal target of $50 billion. This is not a rounding error. It establishes a pattern in which Oracle’s spending projections function as a lower bound rather than a ceiling.

For investors evaluating the $40 billion FY2027 financing plan, the implication is direct: the announced figure is likely a minimum commitment, not a cap, given this track record of exceeding its own targets.

What AI infrastructure actually costs to run

The assumption underpinning the AI infrastructure investment thesis has been straightforward: build data centres, fill them with Nvidia-powered servers, rent out the capacity, and collect margins that justify the capital deployed.

CNBC reporting, citing internal documents, challenged that assumption directly. Oracle’s fast-growing AI cloud business was shown to carry razor-thin gross profit margins, lower than analysts had modelled. This is not a minor data point. At the gross profit line, thin margins have a multiplier effect on the revenue volume required to justify the CapEx and debt being deployed to build and maintain capacity.

CNBC commentators described the shift from free-cash-flow-funded to debt-funded capital expenditure as “troubling for the market,” noting it signals a structural change in how the build-out is being financed.

Debt-funded capex sustainability concerns extend well beyond Oracle: the four largest hyperscalers collectively issued $121 billion in debt in 2025, approximately four times the five-year average, with another $100 billion projected for 2026, establishing a sector-wide pattern of financing infrastructure commitments through capital markets rather than operating cash flow.

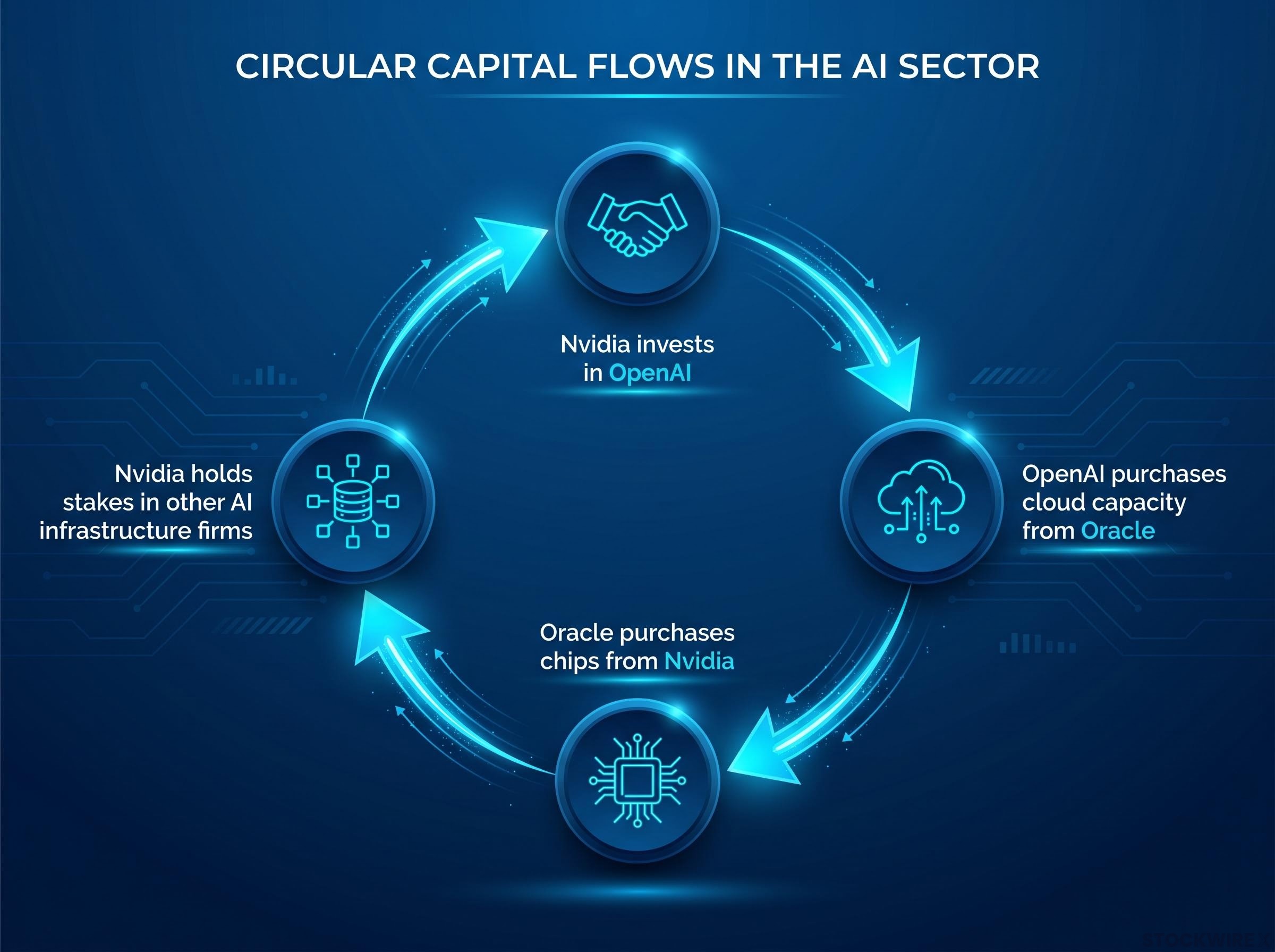

The margin question becomes more uncomfortable when paired with the structure of Oracle’s demand. CNBC commentators flagged a pattern of circular capital flows running through the AI infrastructure ecosystem:

- Nvidia invests in OpenAI

- OpenAI purchases cloud capacity from Oracle

- Oracle purchases chips from Nvidia

- Nvidia holds stakes in other AI infrastructure firms

Each node in this loop generates revenue that originates, in part, from spending by other nodes in the same loop. The apparent strength of Oracle’s AI backlog and demand signals may overstate the quality and independence of those cash flows. If one participant in the circle stumbles, multiple revenue projections compress simultaneously.

For investors, the question this raises is fundamental: if AI infrastructure margins are structurally thin and the demand signals are partially circular, the entire thesis built on the assumption that cloud capacity generates outsized returns needs recalibration.

The timing problem at the heart of AI infrastructure investing

The structural risk embedded in Oracle’s balance sheet is not leverage in isolation. Debt is a tool. The risk is a mismatch between two timelines: when obligations fall due and when revenues mature.

Minsky’s speculative financing stage, in which borrowers can service interest but must roll over principal or raise new capital to cover it, maps directly onto Oracle’s current profile: the company can service near-term interest on its $124.7 billion in long-term debt, but the free cash flow deficit means principal obligations require continuous access to capital markets, precisely the refinancing dependency that makes the position vulnerable to a sentiment-driven liquidity squeeze.

Oracle’s debt service obligations are immediate and certain. Interest payments on $124.7 billion in long-term debt do not wait for AI demand to ramp. The revenue that is supposed to cover those obligations, however, is back-loaded, uncertain, and dependent on a set of assumptions that have not yet been stress-tested at scale.

NBER research on corporate leverage risk in capital-intensive sectors identifies the timing mismatch between debt service obligations and revenue maturation as one of the primary mechanisms through which infrastructure build-outs that are fundamentally sound can still produce severe investor losses.

Three conditions must hold for Oracle’s AI revenue to justify the capital being deployed:

- AI demand must materialise at scale with consistently high utilisation rates across Oracle’s data centre capacity

- Margins on rented AI compute capacity must expand from their current razor-thin levels to generate meaningful returns on invested capital

- Customers, including financially fragile AI startups, must continue paying through economic cycles and periods of tightened funding

If any one of these conditions fails to materialise on the timeline Oracle’s debt obligations require, the financial outcome deteriorates rapidly regardless of whether the underlying technology ultimately succeeds.

Historical precedent: infrastructure winners, infrastructure investors

The railroad and late-1990s telecommunications build-outs offer a structural parallel. Both technologies ultimately transformed their respective sectors. Both created enormous long-term value. And in both cases, investors who financed the original infrastructure phase suffered severe losses, because the technology thesis and the investment thesis were two distinct questions with different answers and different timelines.

Why the sell-off can overshoot even sound analysis

Oracle’s trading multiple heading into this earnings release had incorporated a narrative premium. The AI backlog was growing. The OpenAI relationship provided a high-profile anchor tenant. Investors were pricing in a future profit ramp that had not yet appeared in reported cash flows.

As margin data, debt sustainability questions, and circular demand concerns have become louder, this narrative premium has begun compressing. The compression produces outsized stock moves even when reported earnings meet or beat expectations, because the repricing is occurring on a different layer of the valuation than the one the income statement addresses.

The market’s instinct in these moments is to mark down equity first and refine the analysis later. This means the sell-off can exceed what a careful fundamental assessment would predict.

Super Micro Computer’s 27.98% single-session collapse illustrates the same mechanism at work: a different company, a different product, the same capital raise trigger, the same sentiment-driven repricing. Analysts have flagged a broader pattern of AI-linked companies flooding capital markets with large equity and debt raises as a warning sign about sector-wide financial sustainability.

The interpretive question for investors is whether this repricing represents:

- Sentiment overshoot: a temporary compression that reverses as earnings eventually grow into the valuation, creating a potential re-entry window for investors with a longer horizon

- Fundamental re-rating: a structural compression of the narrative premium as margin and debt data accumulates, signalling a permanent reset in how the entire category should be valued

Distinguishing between these two frameworks matters for how investors respond. The former suggests patience; the latter suggests recalibration.

For investors wanting to apply a more structured analytical lens to the repricing question, our full explainer on AI stock bubble frameworks examines four distinct methodologies, including the Shiller CAPE ratio at 40.11 and Minsky’s financing stages, each of which produces a different verdict on whether current AI valuations reflect genuine revenue inflection or dangerous speculative excess, along with specific portfolio actions readers can take under each scenario.

What the Oracle reckoning means for the AI investment cycle broadly

Oracle is not an outlier. It is a concentrated, high-beta expression of a structural profile shared across the AI infrastructure sector: front-loaded CapEx, debt-funded expansion, thin margins on AI cloud capacity, and revenue dependency on a customer base that includes financially fragile AI startups.

The 11 June session did not deliver a verdict on whether AI infrastructure spending will ultimately pay off. What it delivered was a clear market signal that the original narrative, that every dollar of AI CapEx is a high-margin, fast-payback investment, is under active revision.

Three signals worth watching in the next reporting cycle

A more sustainable version of this investment cycle would demonstrate measurable progress on three fronts. These serve as a forward-looking checklist investors can apply to any AI infrastructure name:

- Gross margin trajectory in AI cloud segments: Are margins expanding as scale increases, or are they remaining structurally thin as competition for tenants intensifies?

- CapEx funding source: What proportion of capital expenditure is funded from operating cash flow versus new debt or equity raises? A shift toward internally funded spending signals financial durability.

- Customer concentration and credit quality in AI backlog: How dependent is the revenue pipeline on a small number of financially fragile AI startups versus diversified, creditworthy enterprise customers?

These are the signals that will determine whether the 11 June sell-off was a sentiment-driven correction or the opening phase of a fundamental re-rating of the entire AI infrastructure category.

The AI debt reckoning has arrived, but the verdict is still open

The market is not punishing AI ambition. It is repricing the gap between the cost of building AI infrastructure and the demonstrated quality of the cash flows that infrastructure is supposed to generate. Oracle’s $124.7 billion in long-term debt, negative $24.7 billion in trailing free cash flow, razor-thin AI cloud margins, and $40 billion in additional planned financing made it the clearest expression of this repricing on 11 June 2026.

The timing mismatch, thin margins, and circular demand loops are structural risks, not a guaranteed outcome of failure. If utilisation ramps, margins improve, and customer quality strengthens, the debt being deployed today could still prove justified. The companies that survive this phase will be those that can demonstrate margin expansion and free cash flow inflection before their debt service obligations outpace revenue growth.

The next several quarters of reporting represent the most consequential stress test the AI infrastructure thesis has yet faced.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.