Most investors assume that if an executive is lying on an earnings call, it will be obvious. It is not. The more common pattern is an executive who answers at length, sounds confident, and says almost nothing.

Two earnings calls, separated by nearly three years and covering companies on opposite ends of the size spectrum, produced the same outcome: a significant share price decline that followed patterns visible in the transcript weeks to months before the market repriced the stock. In neither case did management say anything demonstrably false. What they did instead was structurally more revealing.

Here is a concrete framework for reading an earnings call transcript the way an institutional analyst does, grounded in two cases where the signal preceded the move. The framework requires no proprietary tools and applies to any publicly available transcript.

What evasive executive language actually looks like

Outright refusal to answer an analyst’s question is rare. It would be instantly damaging, and executives know it. Instead, evasion operates through structure, not content. The executive responds, sometimes at considerable length, and still manages to leave the original concern untouched. In real time, it sounds like engagement. On the transcript page, read structurally, it looks very different.

Peer-reviewed research on detecting deceptive discussions in conference calls found that specific linguistic patterns in CEO and CFO narratives during quarterly earnings calls correlate measurably with subsequent financial restatements, providing empirical grounding for the premise that communication structure carries predictive information independent of stated content.

Plato Investment Management has formalised the most common evasion patterns into six measurable markers:

- Answer-to-question word ratio: Responses dramatically longer than the question invite scrutiny. Sustained verbosity on a specific risk topic often substitutes for directness.

- Future-tense pivot count: How often an executive shifts into “we will” or “over time” before addressing the present-tense concern. One pivot is context. Three or more is a pattern.

- Question reframing: Compare the analyst’s question with the answer line by line. If management consistently answers a more comfortable version of the question, the gap between those two versions is where the risk sits.

- Optimism without specificity: Confident statements that lack timeframes, metrics, or mechanisms. These cannot be evaluated or falsified; their function is tonal, not informational.

- Topic clustering of evasion: Which topics attract the most evasive responses? When analysts return to the same issue and receive similar deflections, the topic itself is the signal.

- Imprecise historical analogies: Past episodes invoked to contextualise a novel threat without clearly matching scale or mechanism. If the analogy mainly consumes time and shifts attention, it is rhetoric, not analysis.

Why markers only matter in combination

No single marker is decisive. A long answer on its own is unremarkable. An optimistic comment without a specific metric might just reflect a CEO’s communication style. The signal sharpens when three or more markers cluster on the same structurally important topic, the topic analysts are pressing hardest on. That requires the reader to know which questions matter most before reading the transcript, not after.

Evasive language in Q&A is one layer of a broader analytical discipline; earnings report red flags embedded in press releases, such as front-loaded metrics and disappearing KPIs, often compound the same risks that evasive transcript responses are concealing.

When big ASX news breaks, our subscribers know first

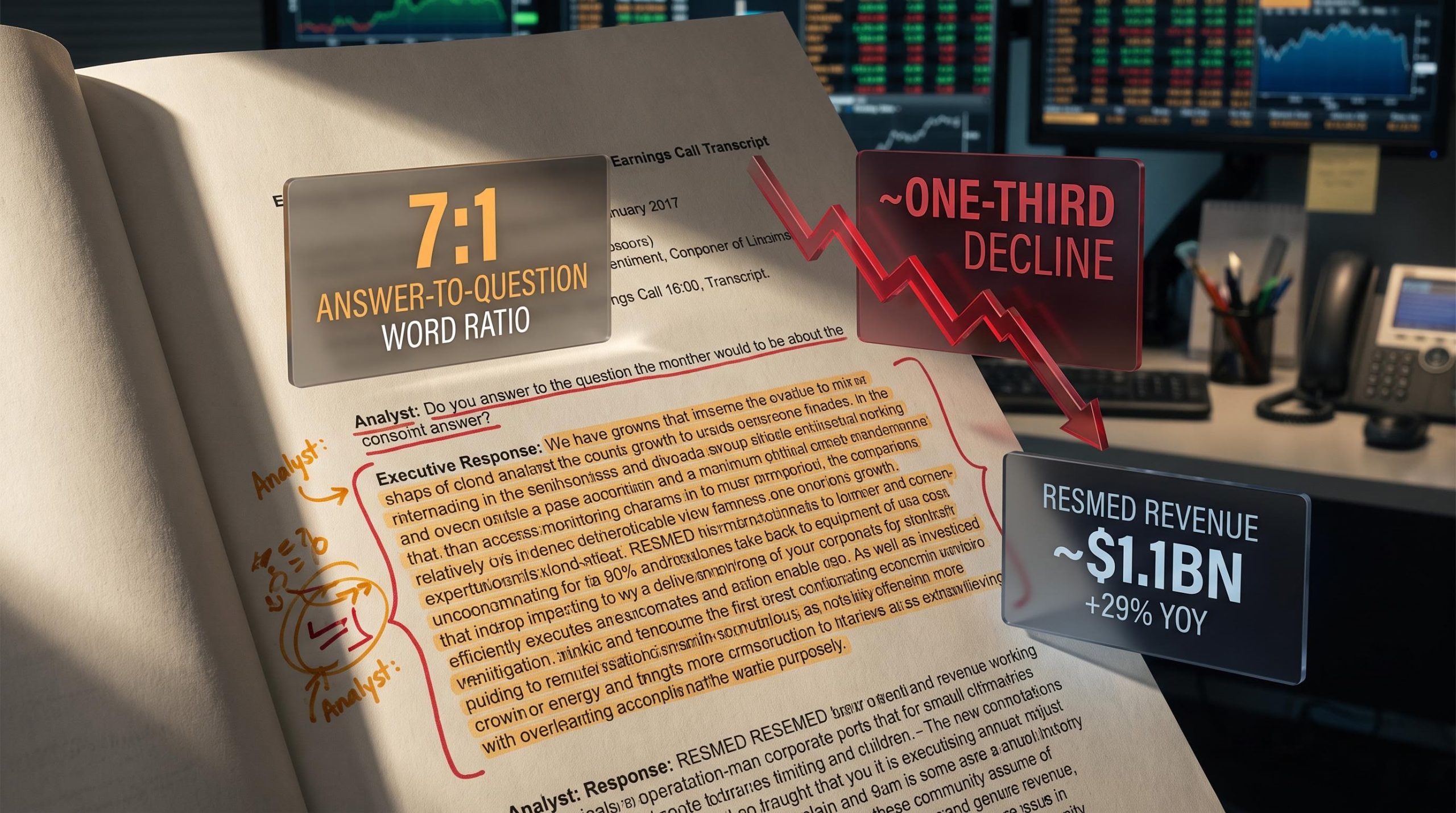

ResMed, April 2023: when a 470-word answer raises more questions than it settles

By April 2023, ResMed’s quarterly numbers looked enviably strong. Revenue came in at approximately $1.1 billion, up roughly 29% year-on-year. Device sales growth exceeded 40%. On headline figures alone, there was little to question.

The complication was GLP-1 agonists, the class of weight-loss drugs that includes semaglutide (sold as Ozempic and Wegovy). Obesity is a primary risk factor for obstructive sleep apnoea, which is the condition ResMed’s core products treat. A Goldman Sachs analyst raised the concern precisely and concisely: whether growing adoption of weight-loss medications might erode ResMed’s addressable patient population over time.

The executive response ran to roughly 470 words, delivering an answer-to-question word ratio of approximately 7:1. More revealing than the length was the structure. Three distinct evasion markers were present. The response shifted repeatedly into forward-looking language, describing how ResMed “would” engage with pharmaceutical partners and how certain pathways “will be” developed, without first engaging with the present-tense concern. GLP-1 drugs were reframed as an “opportunity” for collaboration and expanded diagnosis rather than as a competitive threat. And the response reached back to a surgical weight-loss procedure from more than two decades earlier as a supposed parallel, a detour that occupied time without establishing any meaningful structural equivalence to the current situation.

Management answered a more comfortable version of the question than the one that was asked. The 7:1 ratio concentrated on the topic analysts were most urgently pressing tells you that length was doing work that substance was not.

Plato carried an underweight position in ResMed at that point, with the evasion signal sitting alongside six further red flags as part of a broader composite assessment.

What followed the call

Novo Nordisk released findings from its SELECT cardiovascular outcomes trial on 8 August 2023, revealing that semaglutide cut major adverse cardiovascular events by roughly 20%. That data shifted the GLP-1 narrative well beyond weight management into the domain of cardiometabolic risk, substantially broadening the investor concern about what these drugs might mean for obesity-related conditions such as sleep apnoea.

After the SELECT data landed, ResMed’s share price dropped by around a third, some four months on from the April 2023 call. The stock later recovered, which indicates the evasion signal pointed to a near-term dislocation between management’s public framing and incoming data, rather than any lasting deterioration in the company’s fundamentals.

Smart Parking, February 2026: when headline growth conceals what analysts are actually asking

When Smart Parking published its February 2026 half-year results, the headline figures looked compelling: revenue had roughly doubled, up approximately 96%, and EBITDA had climbed by around 85%. Reading only the summary numbers, there appeared to be little cause for concern.

Analysts saw it differently. Their questioning focused not on the topline but on earnings quality and sustainability. Three concerns kept surfacing: how much of the growth came from a recent acquisition, whether the debt-recovery spike was a one-off backlog clearance, and why core UK volumes were flat while margins had compressed.

The CEO’s responses activated Plato’s framework primarily through consistent question reframing. This is subtler than the future-tense pivots seen in ResMed. It is harder to spot in real time because the executive is technically responding. The tell is that the answer does not correspond to the question that was actually asked.

| Topic | What the analyst asked | What the response addressed |

|---|---|---|

| Debt-book composition | Proportions likely to be collected, age profile, comparison to historic recovery rates | Headline revenue growth and general characterisation of the business as “strong” |

| Regulatory price cap | Expected revenue impact from UK Private Parking Code of Practice caps (£50/£100 with transition period) | Non-specific assurance the company would adapt, with no mechanisms, revenue impact estimates, or contingency detail |

When a CEO consistently answers the growth question rather than the risk question being asked, the gap between those two versions of the question is where the risk is hiding. That gap is measurable even without access to internal company data.

The evasion signal was one of six total red flags informing Plato’s short position in Smart Parking via the Global Alpha Fund.

Small-cap management quality assessment extends the evasion framework into a broader discipline: per-share return analysis, insider ownership signals, and capital raise transparency each provide independent evidence about whether a management team’s communication patterns reflect genuine confidence or structural concealment.

What followed the call

Smart Parking’s share price shed more than 30% across the three months that followed the February 2026 results. Subsequent disclosures confirmed the analysts’ concerns: the debt-recovery spike was largely non-recurring, core UK volumes remained flat, and margin compression persisted. The lead time between the evasion signal and market repricing was approximately three months.

What both cases share, and where they differ

On the surface, these two cases look like they belong in different categories. ResMed is a well-capitalised global medical device company facing a macro-level structural threat. Smart Parking is a smaller Australian technology company facing earnings quality concerns. The evasion forms differed too.

Yet the structural thread is the same. In both cases:

- The signal was relational, not content-based: it lived in the gap between questions and answers, not in any specific claim that proved false.

- Evasion concentrated on the risk topics that attracted the most persistent analyst scrutiny, the questions analysts returned to most forcefully.

- The signal combined with other observable red flags to form a composite risk picture, not a standalone trigger.

| Dimension | ResMed | Smart Parking |

|---|---|---|

| Company type | Global medical device company | Smaller Australian technology company |

| Nature of risk | Macro-level structural threat (GLP-1 market compression) | Earnings quality and sustainability of short-term results |

| Primary evasion form | Excessive length, future-tense pivots, imprecise historical analogy | Systematic question reframing, growth-narrative substitution |

| Lead time (signal to repricing) | ~4 months | ~3 months |

| Share price outcome | ~one-third decline; subsequently recovered | >30% decline in three months |

The fact that two companies with different risk profiles, evasion styles, and operating contexts produced the same relational signal pattern tells you the framework is detecting something about communication structure that is independent of company type. That is what makes it transferable.

How to apply this to any earnings call transcript you read

The most important step happens before you open the transcript. The investor who knows which two or three risk questions matter most before reading is in a fundamentally different position from the investor reading cold. Start there.

- Identify the key risk topics. Before reading, determine the two or three most structurally important uncertainties facing the business.

- Locate the relevant analyst questions. Find the questions on the call that address those specific topics.

- Apply the six markers. For each response, check: answer-to-question word ratio, future-tense pivot count, question reframing, optimism without specificity, topic clustering of evasion, and imprecise historical analogies.

- Count and assess clustering. One marker on a minor topic is unremarkable. Three or more markers clustering on the most structurally important risk topic is the threshold for escalated attention.

- Evaluate composite context. Assess whether the evasion pattern, combined with other observable risk factors, constitutes a meaningful signal.

Quick-reference checklist for the six evasion markers:

- Answer-to-question word ratio

- Future-tense pivot count

- Question reframing

- Optimism without specificity

- Topic clustering of evasion

- Imprecise historical analogies

Every input this process requires is publicly available. No institutional tools needed.

For investors wanting a complete framework that pairs transcript reading with quantitative checks, our dedicated guide to analysing earnings reports walks through a six-step process covering GAAP reconciliation, free cash flow verification, and accounts receivable trends using only free public tools.

The next major ASX story will hit our subscribers first

What evasion signals predict, and what they do not

ResMed’s recovery is the detail that prevents overcorrection. The share price fell by roughly a third after the SELECT trial results, but the company subsequently recovered. Investors with a multi-year horizon who held through the GLP-1 repricing were not permanently impaired.

That distinction matters. In both case studies, the evasion signal predicted near-term misalignment between management’s public framing and incoming information. It did not predict whether the business was permanently broken. Used with appropriate calibration, the framework gives you a lead-time advantage on sentiment repricing, not a view on whether to own a company for a decade.

The distinction between near-term sentiment repricing and permanent capital loss is central to how value investors calibrate responses to evasion signals; a framework that defines risk as lasting business deterioration rather than price volatility helps clarify which signal patterns warrant position changes and which warrant monitoring.

Evasion signals identify when management’s public framing is likely to be challenged by incoming information. They do not tell you whether the underlying business will be permanently impaired.

In both cases, Plato’s positions (underweight ResMed, short Smart Parking) were informed by multiple red flags, with evasion language as one of six or more contributing factors. The framework is one disciplined input into a broader process, not a standalone trading signal.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

What the transcript tells you that the press release never will

Earnings call transcripts are one of the few settings where management must respond in real time to informed, sometimes adversarial questioning. Press releases are drafted and polished over weeks. Slide decks are choreographed. The Q&A section of an earnings call is where the friction between what analysts want to know and what management wants to say creates a record that those polished documents never will.

Both case studies showed the same thing: the gap between question and answer surfaced the risk three to four months before the market priced it in. Every earnings season, dozens of transcripts are published containing the same structural patterns identified here.

The earnings transcript is an adversarial document in the best sense. The friction between analyst questions and management answers is where the most useful information lives, and structural reading is how you access it.

The investor who reads transcripts structurally, rather than tonally, is extracting a layer of signal that the headline-number reader leaves on the table.

—