The label “five years away” has followed quantum computing for the better part of three decades, a stretch long enough that scepticism became the default posture. For most of that stretch, the delay was real and rooted in unsolved physics: nobody could build a qubit stable enough to correct its own errors at scale. That problem has not disappeared, but its character has changed. The barrier now is engineering and capital, not fundamental science. Engineering problems behave differently. They resolve on a curve investors can model.

The question for mid-2026 is not whether quantum becomes commercially relevant. Multiple independent roadmaps now converge on approximately 2030 for first useful applications, and the National Institute of Standards and Technology (NIST) finalised post-quantum cryptography (PQC) standards in 2024. The Cloud Security Alliance (CSA) has set a hard enterprise readiness deadline of 14 April 2030. The question is how much of this transition the market has already priced in, and whether your portfolio sits ahead of or behind the institutional response.

Here is a three-tier exposure map, organised by how soon each layer is likely to pay off. It gives you a framework for evaluating your current holdings against the timeline rather than against the hype.

Why this time the “five years away” problem is actually a capital problem

The prior era of quantum delay was defined by a single constraint: error correction was an unsolved physics problem. Qubits were too fragile, too noisy, and no one had demonstrated that errors could be systematically corrected at scale. That is no longer the binding constraint. Error correction has been demonstrated across multiple hardware modalities, including superconducting, trapped ion, and photonic architectures. The field has shifted from “can this work?” to “which architecture scales fastest?”

That distinction matters because it changes how you should think about timeline reliability. When the barrier is fundamental physics, timelines are speculative. When the barrier is engineering scale-up, timelines become at least partially predictable, closer to how semiconductor roadmaps have historically behaved.

The roadmap commitments are now specific enough to evaluate. IBM targets its Starling system for 2029: approximately 200 logical qubits capable of running circuits with 100 million gates. Its Blue Jay programme targets up to 2,000 logical qubits and billion-gate circuits by 2033 and beyond. French hardware startup Alice & Bob has published a roadmap to build a useful quantum computer by 2030, defining “useful” as 100 high-fidelity logical qubits capable of solving real-world problems.

IBM’s prominence in the roadmap commitments above is reinforced by its policy footprint: the company received the single largest allocation under CHIPS Act quantum funding announced in May 2026, with the Department of Commerce taking minority equity stakes rather than issuing conventional grants, a structure that creates sustained financial alignment between the government and funded firms.

Forrester’s State of Quantum Computing, 2026 concludes that the fault-tolerant foundation era has arrived sooner than expected, with practical business uses likely to emerge by 2030.

| Dimension | Prior constraint era (pre-2024) | Current engineering era (2024 onwards) |

|---|---|---|

| Primary barrier | Unsolved physics (error correction unproven) | Engineering scale-up (capital and manufacturing) |

| Timeline predictability | Low; speculative estimates with wide variance | Moderate; staged roadmaps with specific milestones |

| Investor mental model | Biotech-era: fundamental uncertainty dominates | Semiconductor-era: scaling curves are partially modelable |

The semiconductor-era framing does not eliminate risk. It changes the type of risk, and that changes how you should size and stage your positions.

When big ASX news breaks, our subscribers know first

The encryption clock is already running, whether or not Q-Day arrives in 2030

The most common misunderstanding about quantum cybersecurity risk is that it is future-dated. It is not. Adversaries are already collecting encrypted data under the assumption they will be able to decrypt it once quantum capability matures. This is the “harvest now, decrypt later” threat model: any data with long-term sensitivity, including state secrets, intellectual property, health records, and financial histories, is exposed today if it is protected only by classical encryption algorithms.

That means the threat is not hypothetical. It is active. The data being harvested today cannot be un-harvested once PQC migration is complete. The window of vulnerability is open now.

The urgency shaping PQC procurement is compounded by a parallel dynamic in AI cybersecurity spending: AI-enabled vulnerability scanning has compressed what previously took years of conventional discovery into weeks, accelerating the offensive capability curve that defenders, including those relying on classical cryptographic infrastructure, are racing to outpace.

What the mandates actually require enterprises to do

Institutional mandates have crystallised the urgency into concrete deadlines:

- NIST finalised its post-quantum cryptography standards in 2024, providing a concrete basis for product roadmaps and procurement requirements across federal agencies and their supply chains.

- The Cloud Security Alliance set 14 April 2030 as the Y2Q deadline, framing that date as a hard enterprise planning deadline for full quantum-readiness.

- Google accelerated its own internal migration target, aiming to complete its transition to PQC by 2029, setting a de facto industry pace for large technology companies.

History provides the urgency calculation. Even incremental cryptographic upgrades, such as the transition from SHA-1 to SHA-256 or from 1,024-bit to 2,048-bit RSA, took close to a decade to fully propagate through large infrastructures. A full PQC migration is significantly more complex than either of those transitions. It spans software libraries, hardware security modules, PKI and certificate authorities, network security appliances, and specialised migration consulting.

A large organisation that begins serious PQC migration planning in 2027 or 2028 is, by historical standards, already behind the curve. Sector-specific exposure is concentrated in financial services, defence, healthcare, and critical infrastructure, which are the sectors most likely to be early, mandated buyers.

What this tells you is that cybersecurity vendors with established PQC offerings are entering a demand environment shaped by urgency rather than discretion. That makes PQC a procurement story driven by compliance deadlines, not a speculative bet on breakthrough timing. According to Forrester, Q-Day could arrive as early as 2030, with a wider range of experts placing RSA-2048 breakability somewhere in the 2030-2035 window.

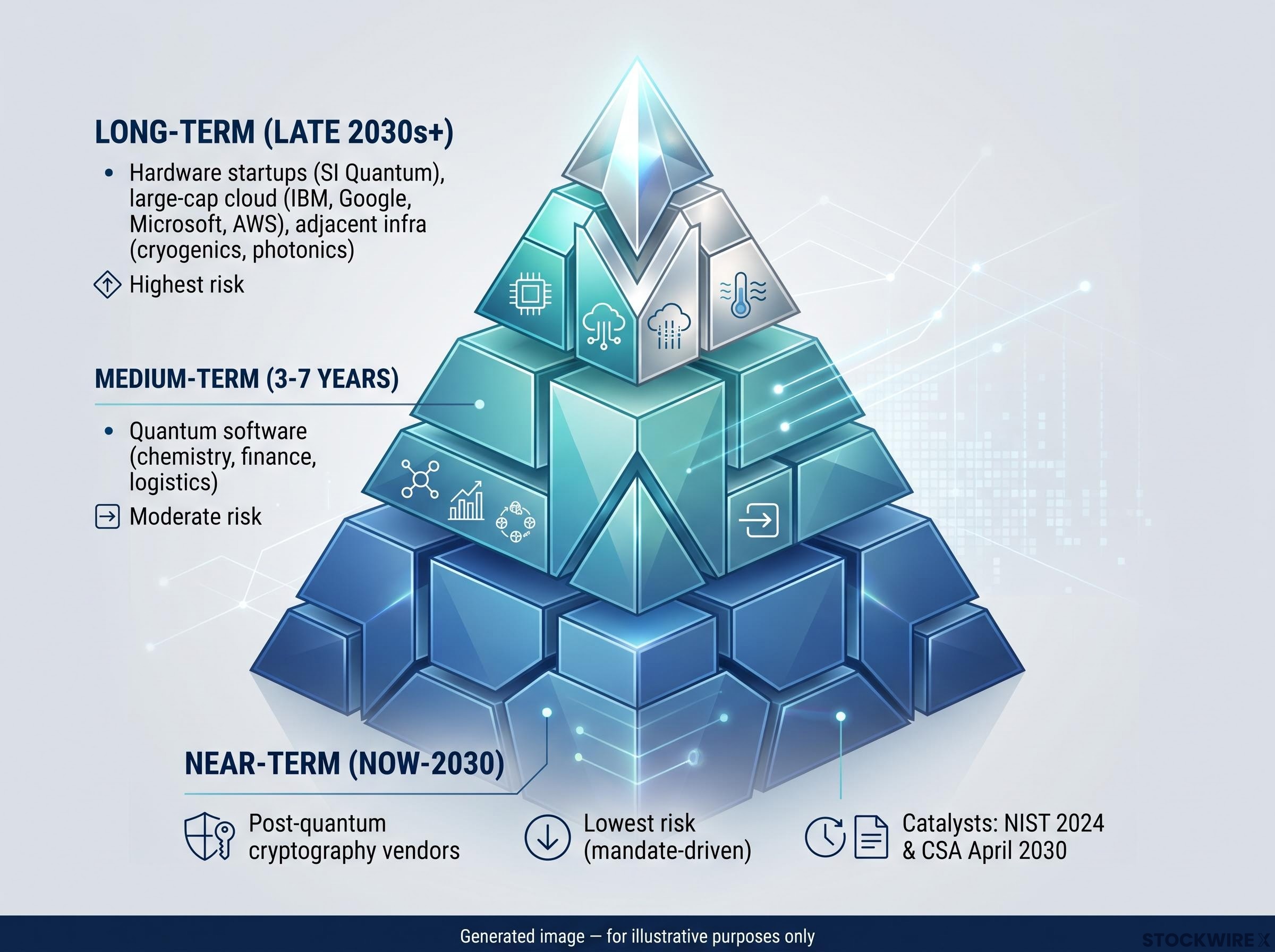

A three-tier map of quantum investment exposure by time horizon

The investment framework below is organised by time horizon rather than by company or technology type, because horizon alignment is what determines position sizing discipline. A 2029 PQC vendor with mandated demand belongs in a different allocation category than a hardware startup whose revenue depends on engineering breakthroughs in the late 2030s, regardless of which ticker generates more excitement.

| Time horizon | Opportunity category | Key demand catalyst | Risk profile |

|---|---|---|---|

| Near-term (now to 2030) | Post-quantum cryptography vendors | NIST standards (2024) and CSA April 2030 deadline | Lowest: mandate-driven revenue with institutional procurement cycles |

| Medium-term (3-7 years) | Quantum software and applications | NISQ and early fault-tolerant system availability | Moderate: hardware-agnostic platforms reduce single-bet risk |

| Long-term (late 2030s onwards) | Hardware startups, large-cap quantum cloud, quantum-adjacent infrastructure | Fault-tolerant system commercialisation | Highest: breakthrough-dependent timelines with widest uncertainty bands |

The near-term PQC tier is the most quantifiable because the demand catalysts are already in place. Specific product categories driving that demand include:

- Software libraries and cryptographic algorithm implementations

- Hardware security modules requiring PQC upgrades

- PKI and certificate authority infrastructure

- Network security appliances

- Specialised PQC migration consulting

The medium-term tier covers quantum software in chemistry, finance, and logistics optimisation, where hardware-agnostic and vertically specialised platforms are emerging. The long-term tier includes large-cap quantum cloud programmes (IBM, Google, Microsoft, AWS), hardware startups such as SI Quantum (a portfolio company of the venture investor whose timeline projections appear in the original analysis), and quantum-adjacent infrastructure spanning cryogenics, specialty materials, photonics, and secure networking.

The tiered structure reflects the actual risk gradient: from mandate-driven revenue to engineering-dependent revenue to breakthrough-dependent revenue. Your position sizing should mirror that gradient explicitly. Most investors who audit their quantum exposure will discover it skews toward the long-horizon hardware narrative while the near-term PQC layer, where institutional capital is most likely to move first, is underrepresented.

How quantum fits alongside classical and AI computing, not against them

The most common mental model investors carry into quantum computing is a displacement story: quantum replaces classical, or quantum replaces AI. That model will misprice both classical computing incumbents and quantum’s actual commercial ramp.

The more accurate framing is one of three complementary pillars: classical, AI, and quantum computing each address distinct problem types and are converging into a unified infrastructure layer rather than competing for the same workloads.

The current AI infrastructure buildout is characterised as the largest technology investment cycle in history, with a projected duration of approximately two decades. With worldwide energy capacity expanding at roughly 4-5% per year, that constraint acts as a ceiling on runaway overbuilding, making a sudden dot-com-style collapse considerably less likely. Quantum enters this cycle as an additional layer, not a replacement wave. Classical computing continues to handle the vast majority of commercial workloads. AI handles pattern recognition and prediction. Quantum targets a specific class of problems where classical approaches are computationally intractable.

Quantum enters a computing landscape already absorbing the largest single technology investment cycle in history: AI infrastructure capital expenditure is redirecting hundreds of billions from software toward physical power and hardware, and the energy constraints shaping that buildout will apply equally to the cryogenic and photonic infrastructure quantum computing requires at scale.

The near-term application areas where quantum delivers an advantage at scale are narrower than the hype implies, but commercially meaningful:

- Logistics optimisation: Problems in the travelling salesman class, where the number of possible solutions scales exponentially and classical methods produce approximations rather than optimal solutions.

- Chemistry and materials science simulation: Molecular interactions that are currently intractable for classical systems, opening pathways in drug discovery and materials design.

- Finance optimisation: Portfolio optimisation and risk modelling problems where quantum algorithms may deliver faster, more precise solutions than current methods.

What this means for you is that quantum-adjacent infrastructure (cryogenics, photonics, specialty materials, secure networking) offers a way to gain exposure to rising quantum capital expenditure without betting on a single hardware modality surviving to commercialisation. These components support all three pillars simultaneously.

Where the bull case might be running ahead of the evidence

The thesis above is directionally supported by roadmaps, policy guidance, and analyst consensus. But the specific timing carries genuine uncertainty, and investors who size positions based on the most optimistic projections will get hurt if the timeline stretches.

Timeline uncertainty is the most consequential risk. Many expert surveys place the 50% probability mark for cryptographic-breaking capability in the mid-2030s, not 2030. The plausible outer range extends toward 2040. Forrester’s projection of Q-Day as early as 2030 represents the aggressive end of the consensus.

Expert consensus on when cryptographically relevant quantum computers arrive is wider than most portfolio frameworks assume, and quantum threat timeline research from institutions tracking hardware progress places the 50% probability mark for RSA-2048 breakability in the mid-2030s rather than at the 2030 boundary the CSA deadline implies.

Definition-of-utility risk is subtler. Early quantum advantages may appear in narrow optimisation or simulation tasks that are technically impressive but generate limited near-term revenue. A quantum computer that solves a chemistry problem faster than a supercluster is a milestone. It is not necessarily a revenue event.

Adoption lag compounds both of the above. Even when quantum hardware crosses capability thresholds, broad integration runs through hybrid quantum-classical infrastructure that takes years to mature. Most serious analyses place mainstream commercial integration in the 2040s.

Market overpricing risk is concentrated in small quantum pure-plays, where narrative momentum can inflate valuations well ahead of any revenue. This is the segment most likely to see significant corrections before commercialisation.

Valuation risk versus technology risk: two different problems

Technology risk, the risk that the technology takes longer than expected, is managed by patience and staged entry. Valuation risk, the risk that current prices already embed success that has not materialised, is managed by position sizing and entry discipline. The two can coexist in the same position. Pure-play hardware startups currently carry both simultaneously.

The gap between “technically demonstrated quantum advantage” and “meaningful revenue event” is where most investor losses in pure-play quantum positions are likely to occur. Sizing discipline in that segment matters more than stock selection.

The next major ASX story will hit our subscribers first

Building a position before the market prices in the shift

The practical framework maps directly onto the three-tier structure above, and it starts with a question most investors have not yet asked: do your current cybersecurity holdings have credible, public PQC migration roadmaps?

- Audit existing cybersecurity exposure. Review your current holdings in endpoint security, network security, and identity management. Determine whether those companies have published PQC roadmaps aligned with NIST standards. If they have not, the quantum transition represents a displacement risk to those positions, not an upside.

- Stage new quantum exposure across the three tiers in proportion to their risk profiles. Near-term PQC vendors (highest conviction) should receive the largest allocation. Medium-term quantum software platforms warrant moderate allocation. Long-term hardware and quantum-adjacent infrastructure should be sized as venture-scale positions regardless of their market capitalisation.

- Treat quantum pure-plays as venture-like positions. This applies even if the company is publicly listed and trades at a multi-billion-dollar valuation. Revenue timelines in the late 2030s and beyond carry venture-scale uncertainty.

The staging principle is straightforward: near-term PQC carries the highest conviction and warrants the largest allocation. Hardware carries venture-scale uncertainty and warrants venture-scale sizing. The two should never occupy the same allocation tier in your portfolio.

Most finance-educated readers will discover, on audit, that their cybersecurity exposure skews toward endpoint and network security rather than cryptographic infrastructure. Cryptographic infrastructure is the layer where quantum-driven displacement is most direct and most immediate. That is the gap to address first.

The window for positioning ahead of institutional capital is mid-2026 through 2028. Once enterprises respond en masse to the 2030 deadlines, the near-term PQC opportunity will be significantly more expensive than it is today.

For investors wanting to understand how the largest asset manager is repositioning around these same technology transition themes, our full explainer on BlackRock’s geopolitical risk reclassification covers the firm’s elevation of AI-enabled cyber threats and US-China technology decoupling to its highest risk tier, with direct implications for semiconductor and cybersecurity allocation.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

These statements include forward-looking projections and timelines subject to change based on market developments, technological progress, and company performance. Past performance does not guarantee future results.

What 2030 changes and what it does not

2030 is not the date quantum becomes relevant. It is the date when the distance between quantum-ready and quantum-unprepared portfolios becomes measurable in returns, not just in theory.

| What changes by 2030 | What stays the same through 2030 |

|---|---|

| PQC adoption becomes a procurement requirement, not a discretionary upgrade | Classical and AI infrastructure remain the dominant compute layers |

| Early quantum software revenue emerges in specific verticals (chemistry, finance, logistics) | Hardware pure-plays remain largely pre-revenue |

| Institutional awareness of quantum risk is priced into large-cap quantum programmes | Broad commercial integration remains a 2040s story |

| Cybersecurity vendors without PQC offerings face measurable displacement risk | The computing trinity (classical, AI, quantum) does not collapse into quantum dominance |

PQC adoption is the most near-term, measurable transition, with the clearest demand catalysts already in place. The computing trinity framing remains durable: quantum adds a third layer to computing infrastructure without displacing the first two, and quantum-adjacent infrastructure gains value across all three.

The investor who acts on this framework in 2026 and 2027 is positioning ahead of the institutional reallocation that the NIST standards and CSA deadlines will trigger. The investor who waits for confirmation is likely paying a premium for certainty.