For the second time in 2026, ASML has raised its full-year revenue outlook, lifting the midpoint by roughly €6 billion to a range that sat above even the most recently upgraded analyst models. The revision, announced on 15 July 2026, landed a Q2 revenue beat, Q3 guidance 11% above consensus, and implied Q4 figures that made the gap between management’s view and Wall Street’s look uncomfortably wide.

The reason this matters beyond a single stock: ASML is effectively the only company in the world that can supply the extreme ultraviolet lithography equipment needed to manufacture the most advanced AI chips. When it upgrades guidance, it is not reporting on its own business alone. It is registering something real about the pace of AI infrastructure spending globally.

Here is what the numbers reveal about AI capex momentum, which parts of the semiconductor supply chain are most exposed to the upside, and the specific metrics that will tell you whether this is a peak or the beginning of a longer move.

ASML’s Q2 results and what the numbers actually say

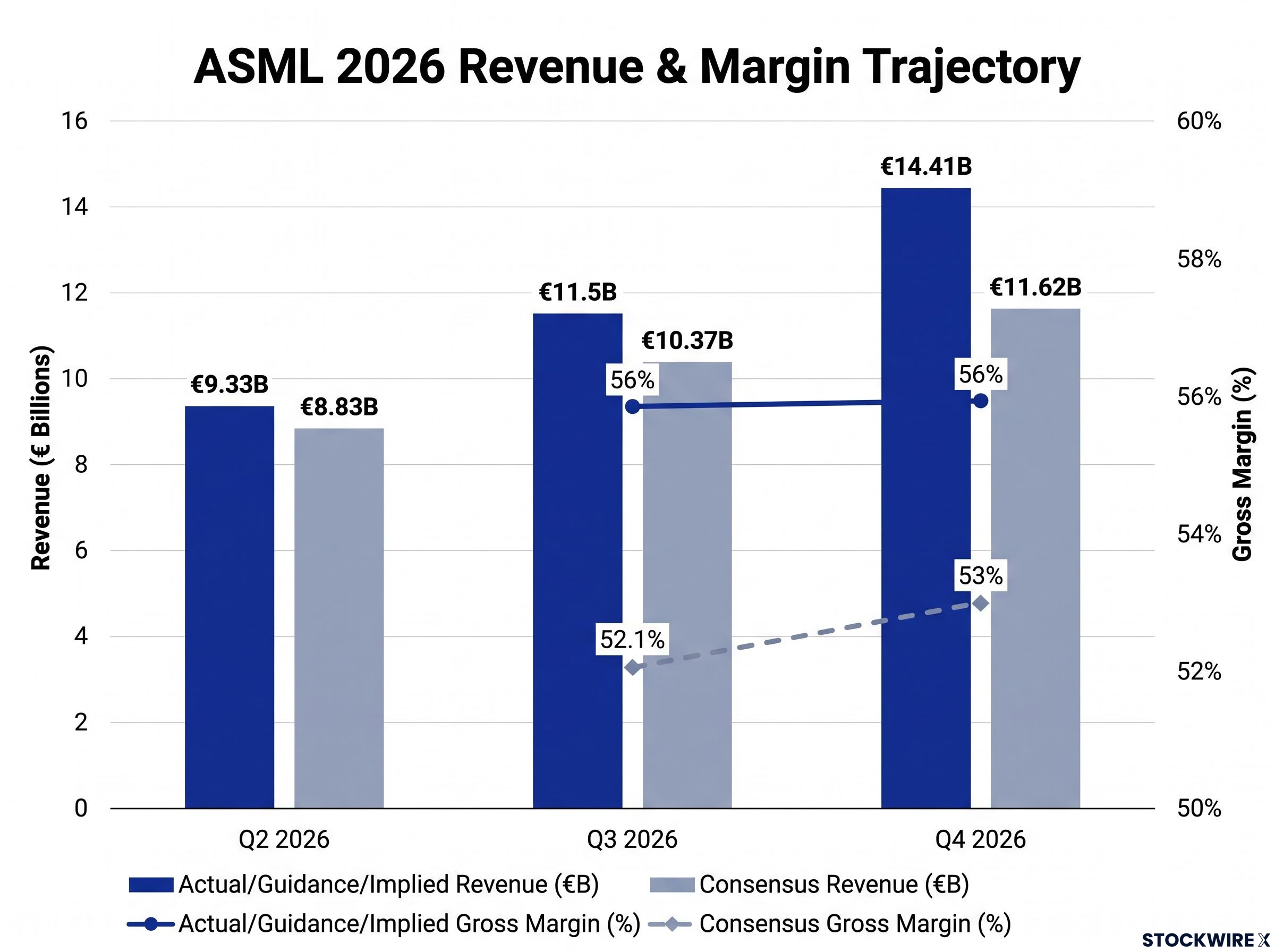

ASML’s second-quarter revenue landed at €9.33 billion, a 5.7% beat against the €8.83 billion Visible Alpha consensus and a meaningful step up from the €7.69 billion recorded in the same period a year earlier. That alone was a clean beat. Then the guidance arrived.

The full-year 2026 net sales target was lifted to a €43-€45 billion range, compared with the previous guidance band of €36-€40 billion, representing a substantial upward reset in a single announcement.

Third-quarter 2026 guidance pointed to €11.5 billion in revenue at a 56% gross margin, clearing the Visible Alpha consensus of €10.37 billion and 52.1% by a substantial margin on both measures.

Bank of America’s analysis of the implied Q4 2026 figures placed revenue at approximately €14.41 billion and gross profit at approximately €8.08 billion on a 56% margin, against consensus forecasts of €11.62 billion in revenue and €6.11 billion in gross profit at 53%.

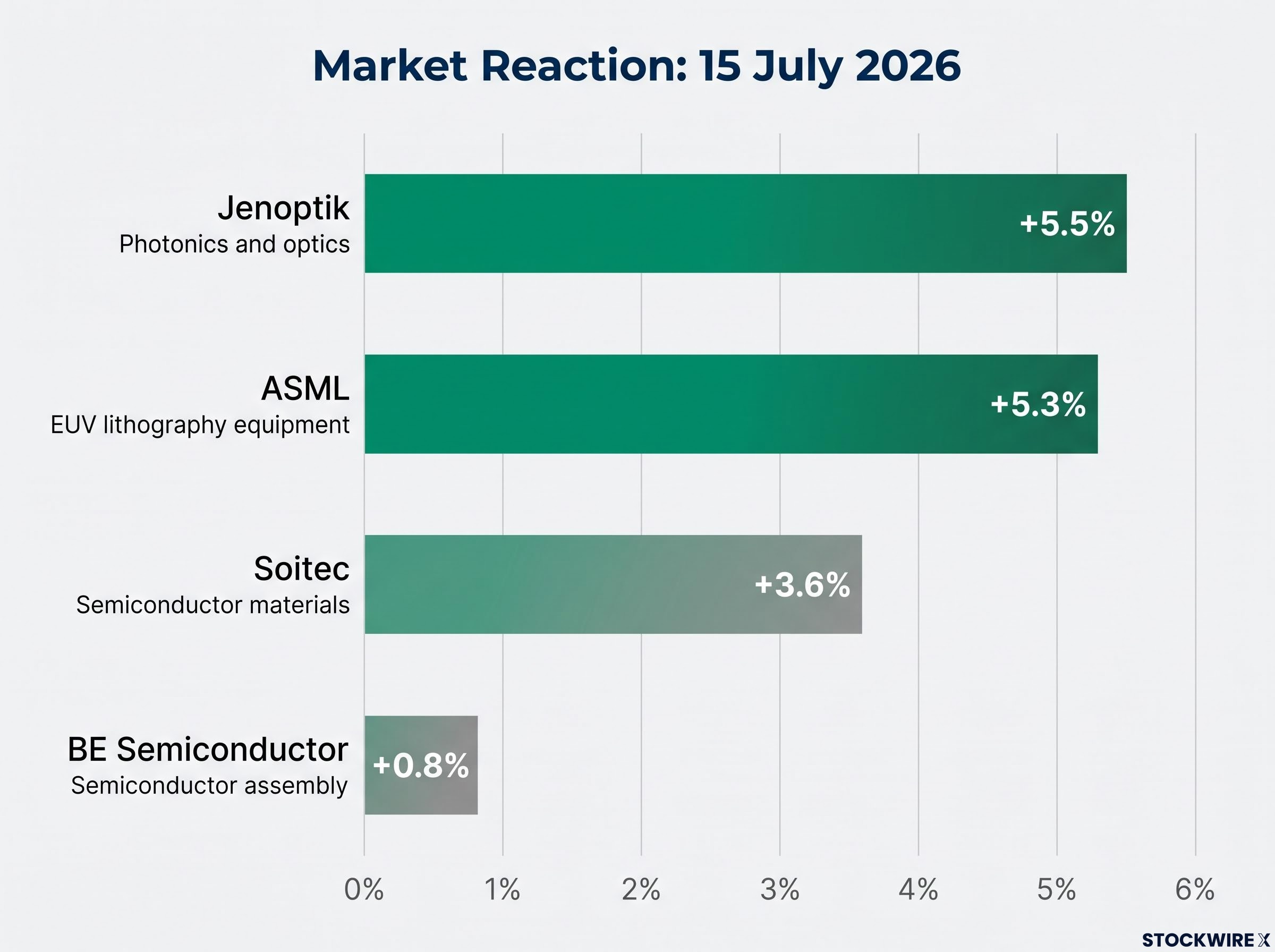

On the morning of 15 July 2026, ASML shares advanced 5.3% in Amsterdam, with the gains arriving in early trading.

The professional forecasting community was still underestimating the pace of AI-driven demand as recently as this week. These are not rounding errors between guidance and consensus. They are structural gaps that suggest analyst models have not yet caught up with what ASML is seeing in its order book.

| Period | Revenue (actual/guidance) | Revenue (consensus) | Gross margin (actual/guidance) | Gross margin (consensus) |

|---|---|---|---|---|

| Q2 2026 | €9.33B | €8.83B | — | — |

| Q3 2026 | €11.5B | €10.37B | 56% | 52.1% |

| Q4 2026 (implied) | €14.41B | €11.62B | 56% | 53% |

When big ASX news breaks, our subscribers know first

Why EUV lithography makes ASML’s guidance a proxy for AI capex

Extreme ultraviolet (EUV) lithography is the process used to print the finest circuit patterns on the most advanced semiconductors. The chips powering AI workloads, the ones inside data centre GPUs and high-bandwidth memory modules, require EUV to fabricate their most intricate layers. Without it, those chips cannot be made at the geometries that deliver the performance AI models demand.

ASML is the sole commercial producer of EUV lithography equipment at leading-edge specifications. No other company manufactures these machines. That monopoly position means ASML’s order book functions as a leading indicator for global AI infrastructure spending, not merely a company-specific data point.

The AI semiconductor supply chain that ASML anchors at the lithography layer is structured around a small number of non-interchangeable positions, with Nvidia, TSMC, and Broadcom occupying distinct roles that collectively determine how quickly AI infrastructure can scale from silicon to deployed compute.

CEO Christophe Fouquet confirmed on 15 July 2026 that the company has nearly finalised its order book for next year’s EUV systems, a disclosure that carries specific weight for how you assess risk in this name.

- Monopoly position: ASML is the only source for commercial EUV lithography at leading-edge specifications

- Record backlog: Approximately €39 billion in total backlog, with recent quarterly bookings of approximately €13.2 billion (roughly double expectations)

- Near-complete 2027 order coverage: CEO Fouquet confirmed orders for next year’s systems are largely secured

For a reader considering ASML stock, the near-complete coverage of 2027 orders means the revenue line for next year is largely set today. That is a different risk profile than most technology or industrial companies with shorter order cycles.

The AI memory surge and the capacity expansion plan through 2028

CEO Fouquet indicated that ASML’s memory-related revenue is on track to increase by approximately 75% in 2026, a figure that reflects the extent to which AI-driven demand for memory chips has exceeded available supply. That single figure captures how aggressively the semiconductor industry is building capacity to serve AI workloads, not just in logic chips but across the memory stack that feeds them.

The capacity expansion plan extends well beyond this year:

- 2026: Approximately 60 EUV systems shipped (approximately 25% year-on-year increase)

- 2027: Output targeted at approximately 80 systems, representing a planned uplift of around 30% on the prior year

- 2028: A further capacity step of roughly 30%, underpinned by substantial advance orders already received from customers

CEO Christophe Fouquet noted that AI-related capital spending and technological progress are strengthening the semiconductor industry’s overall growth trajectory.

Customer pre-orders already placed for 2028 EUV systems tell you something specific about how the buyers themselves are treating this cycle. Semiconductor fabs are committing capital two-plus years forward. That is the strongest available signal that AI infrastructure investment is being treated as structural rather than speculative by the companies actually writing the cheques.

SEMI’s 2028 equipment sales forecast, published the day before ASML’s results, projected global semiconductor manufacturing equipment sales reaching a record level by 2028, driven by AI-related foundry, logic, and advanced memory investment, providing independent industry confirmation that ASML’s multi-year capacity expansion plan is being built into sector-wide projections rather than treated as company-specific optimism.

Margins, services revenue, and what the upgraded profitability guidance signals

The formal gross margin guidance band was revised to 54-56%, stepping up from the previous 51-53% range. This is not a seasonal fluctuation. It is a step-change in the formal guidance framework, confirmed at a level that would have been considered aspirational even a year ago.

Four structural drivers sit behind the upgrade:

- EUV mix shift: EUV systems carry higher margins than older deep ultraviolet (DUV) equipment, and EUV’s share of revenue is growing

- Installed Base Management contribution: High-margin servicing revenue growing with the installed fleet

- Pricing power: Monopoly position in advanced lithography supports premium pricing

- Operating leverage: Volumes scaling against a largely fixed R&D and manufacturing cost base

Installed Base Management as a compounding revenue stream

Installed Base Management (IBM) covers servicing, upgrades, and support for ASML machines already operating in fabs worldwide. As more EUV systems enter the global installed base, IBM revenue grows structurally, independent of any single quarter’s new shipment volume.

Bank of America analysts described Q2 2026 results as driven in part by stronger IBM sales and margins. Higher fab utilisation driven by AI workloads accelerates both IBM revenue and margins simultaneously, because busier machines require more service hours and more frequent upgrades.

A confirmed move to 54-56% gross margins in formal guidance, not scenario analysis, tells you ASML is compounding its earnings quality at the same time it is compounding revenue. That has direct implications for how far valuation multiples can stretch before the stock becomes expensive on a forward earnings basis.

For investors wanting to assess whether the guidance upgrade has been adequately reflected in the share price, our deep-dive into ASML’s valuation discount versus U.S. peers examines why ASML’s forward P/E premium collapsed from a 10-year average of 84% to approximately 6-15%, and what the UBS earnings estimates sitting 15-20% above consensus imply for re-rating potential.

European chip stocks and the broader sector signal from ASML’s upgrade

The 15 July 2026 session showed the sector reaction in real time. Jenoptik, the German photonics and optics company, matched ASML’s gain. Soitec, the French semiconductor materials producer, followed closely. BE Semiconductor lagged.

| Company | Sector | 15 July 2026 move |

|---|---|---|

| ASML | EUV lithography equipment | +5.3% |

| Soitec | Semiconductor materials (France) | +3.6% |

| Jenoptik | Photonics and optics (Germany) | +5.5% |

| BE Semiconductor | Semiconductor assembly | +0.8% |

EUV system production draws on specialist suppliers across wafers, precision optics, and advanced components. When ASML upgrades volume guidance, the supply chain scales with it.

The differentiated moves across these names suggest the market is already pricing supply chain exposure with some precision. Jenoptik’s optics exposure tracked closely with ASML; BE Semiconductor’s assembly focus drew a far smaller reaction. If you hold European semiconductor supply chain names through funds or ETFs, understanding which category of supplier you own matters for interpreting whether your existing positions are exposed to the same AI capex tailwind.

The next major ASX story will hit our subscribers first

What the risks actually are, and which metrics to track from here

Demand is not the risk. The combination of record backlog, near-complete 2027 order coverage, and customer pre-orders already placed for 2028 makes a near-term demand shortfall the least likely scenario in current analysis. The risks that matter sit on the supply side and the policy side.

- Manufacturing capacity limits: Each EUV system contains over 100,000 components, many sourced from a small number of specialist suppliers. Scaling from 60 to 80 to 100-plus systems per year requires coordinated supply chain expansion that cannot be rushed.

- Broader supply chain bottlenecks: Advanced packaging capacity, memory supply, networking equipment, and power availability at data centres can all bottleneck AI infrastructure build-outs regardless of how many EUV tools ASML ships.

- Export control policy: Restrictions on sales to China represent a policy variable that could limit the addressable market irrespective of demand strength. ASML has previously identified export controls as a meaningful headwind.

ASML’s export control exposure gained a new dimension in June 2026 when U.S. Commerce Secretary Howard Lutnick personally raised concerns with company executives about a possible EUV system reaching China, an episode that ASML categorically denied but that illustrates how policy risk can move the stock independently of demand fundamentals.

The metrics that will tell you whether the structural case is holding:

- EUV shipments per year (2026: approximately 60; 2027 capacity: approximately 80): the primary volume indicator

- Quarterly order intake relative to revenue: backlog growth signals sustained demand; drawdown signals the order cycle may be peaking

- IBM revenue as a percentage of total revenue: a rising share signals deepening installed base monetisation

- Gross margin trajectory: whether 54-56% proves sustainable or represents a high-water mark

- Export control developments: any expansion or relaxation of restrictions on China sales materially affects the addressable market

The upside case is now supply-constrained and policy-constrained rather than demand-constrained. For a reader deciding whether to act on this guidance upgrade, the relevant due diligence is about execution risk and geopolitical exposure, not whether AI capex will continue.

Semiconductor cycle dynamics over 2027-2029 complicate the structural bull case: TSMC’s locked-in capital budget and Samsung’s estimated annual outlay confirm a supply wave is approaching, and the historical pattern shows that earnings disappointment and multiple compression tend to arrive simultaneously when the cycle turns, leaving investors who wait for quarterly red flags structurally too late to exit.

Whether this guidance cycle marks a turning point or confirms one already underway

The structural evidence is unusually concentrated: twice-upgraded guidance in a single year, a backlog of nearly €39 billion, near-complete 2027 order coverage, customer pre-orders already placed for 2028, memory revenue guided up 75%, an EUV capacity expansion plan extending through 2028, and gross margins step-changed to 54-56%.

The interpretive question is whether this moment marks the point at which the market recognised AI capex as a multi-year structural force, or the visible peak of a demand cycle that will normalise. The evidence above favours the structural reading, but the next two quarters of order intake data will test it directly.

Customer pre-orders already placed for 2028 EUV systems represent the strongest available evidence that the semiconductor industry itself is treating AI infrastructure investment as structural rather than cyclical.

The specific data point to watch: whether Q3 2026 order intake sustains or draws down the backlog relative to Q3 revenue of €11.5 billion. That single ratio will tell you more about ASML’s forward trajectory than any analyst revision.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including management guidance and capacity projections, are subject to change based on market developments and company performance.