Every few months, a headline announces the dollar is losing its grip on the global financial system. The currency that underpins most of the world’s trade, debt, and reserves is supposedly on its way out, replaced by the Chinese renminbi, gold, or some yet-to-be-determined alternative. The story is compelling. The geopolitics are real. But the numbers tell a quieter, more complicated story.

The 2022 freezing of Russian central bank reserves gave the narrative its most powerful catalyst. If the United States could weaponise the dollar system against a major economy, wouldn’t every non-aligned central bank rush to diversify? That question has driven commentary ever since. The official data, however, through Q4 2025, show something more measured than the headlines suggest.

Here is what the reserve data actually show, why a significant portion of the measured decline is a statistical artefact most coverage ignores, what structural conditions a rival currency would need to meet, and how you can distinguish a cyclical dollar dip from genuine structural erosion. Think of this as an analytical toolkit for evaluating every de-dollarisation claim you encounter from here forward.

What the reserve data actually show

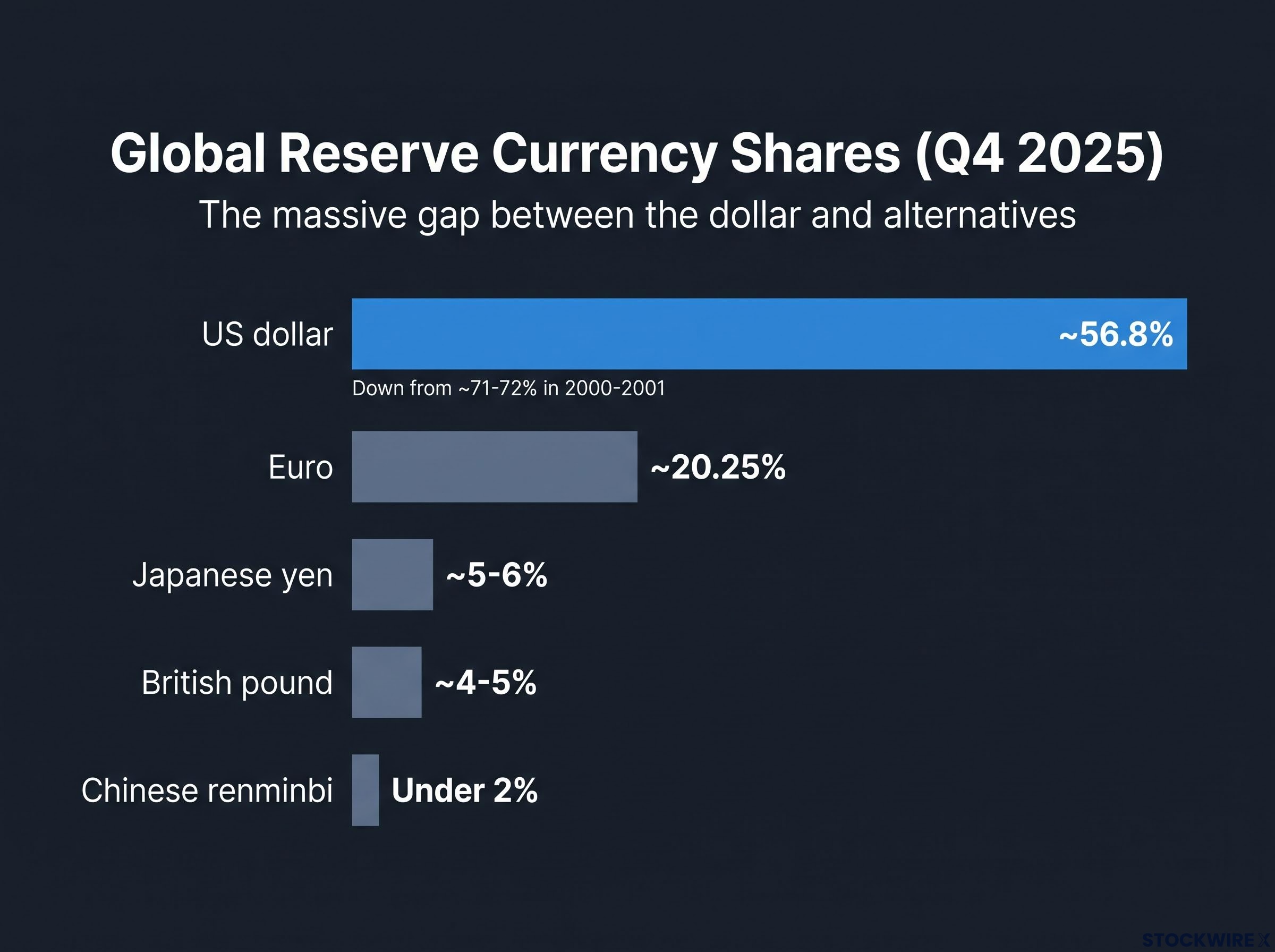

According to the IMF’s Currency Composition of Official Foreign Exchange Reserves (COFER) dataset for Q4 2025, the dollar accounts for approximately 56.8% of disclosed global reserves. That reading places the currency back at levels last seen in the mid-1990s, having retreated from a peak of around 71-72% in the 2000-2001 period.

A 14-percentage-point decline over two decades is genuine. It is also where most commentary stops. What rarely follows is the comparison that gives those numbers their proper scale.

| Currency | Q4 2025 reserve share | Approximate share circa 2000-2001 |

|---|---|---|

| US dollar | ~56.8% | ~71-72% |

| Euro | ~20.25% | N/A (euro introduced 1999) |

| Japanese yen | ~5-6% | N/A |

| British pound | ~4-5% | N/A |

| Chinese renminbi | Under 2% | N/A |

The dollar’s current share is still more than double the euro’s and more than 28 times the renminbi’s. The nearest competitor is not close, and no alternative has meaningfully closed the gap over the past two decades.

The Federal Reserve’s 2025 review concluded that the dollar’s international usage “is little changed over the past 5 years and far exceeds the U.S. share of global GDP and trade.”

That gap between the dollar and everything else is the number to hold in your mind before accepting any claim that the dollar’s dominance is collapsing.

When big ASX news breaks, our subscribers know first

Why the measured decline is partly a mirage

A 14-percentage-point decline sounds like a structural shift. But a meaningful portion of that measured movement was not caused by central banks selling dollar assets. It was caused by arithmetic.

Reserve shares are reported in dollars. This creates a mechanical distortion that most headline coverage either misses or ignores:

- A non-dollar currency (say, the euro) appreciates against the dollar.

- The dollar value of euro-denominated reserves rises in the reported dataset.

- The dollar’s proportional share falls, with no central bank having made a single portfolio decision.

When the euro strengthens by 5%, every euro-denominated reserve is suddenly worth more in dollar terms. The dollar’s share drops on paper without a single treasury being sold. Morningstar analysts have explicitly identified this as a statistical artefact in the measured decline of dollar reserves.

What the ECB data tell us about 2022

The 2022 sanctions episode is the event most frequently cited as a de-dollarisation turning point. The ECB examined what actually happened to reserve composition that year and found that active portfolio management “to a large extent offset” the valuation effects from exchange rates and bond prices.

In other words, what looked like sharp diversification in the headline data was substantially a currency-movement illusion. Once exchange-rate effects are stripped out, the true compositional shifts are significantly smaller than reported figures suggest. The concept is straightforward: a headline drop in dollar share can translate to a fraction of a percentage point of genuine reallocation once you remove the noise.

The IMF’s own analysis reinforces this. Statistical tests do not show an accelerating decline in the dollar’s reserve share tied to the 2022 sanctions episode. What you see in the data is continued gradual diversification, not a structural break.

The next time you see a headline claiming the dollar’s reserve share fell to a multi-decade low, the first question to ask is whether that figure has been adjusted for exchange-rate movements. Unadjusted numbers systematically overstate how fast diversification is actually happening.

The building blocks a rival reserve currency actually needs

If the dollar is losing ground, something has to be gaining it. To understand why no single currency has filled the gap, you need to know what reserve currency status actually requires. There are three non-negotiable structural conditions:

- Deep, liquid financial markets. A central bank holding reserves needs to buy and sell large quantities of assets without moving the price. That requires a bond market with enormous depth and consistent liquidity, the kind of market where billions can be deployed or withdrawn quickly.

- An open capital account. Money needs to flow freely in and out of the country. If a government restricts capital movements, foreign holders face the risk that they cannot access their reserves when they need them most.

- Institutional credibility at scale. Rule of law, independent central banking, transparent regulation, and legal protections for foreign holders. Reserve managers are not just buying a currency; they are trusting a legal and institutional system with their country’s savings.

The euro comes closest to meeting all three. It is backed by large sovereign and corporate bond markets, a major economic bloc, and reasonably strong institutions. Yet after more than 25 years, its reserve share has plateaued near 20.25%. ECB data show the euro has not gained ground against the dollar in global FX turnover either.

The renminbi is central to many de-dollarisation narratives, but the structural reality is stark. Its reserve share sits under 2% of global reserves. Persistent capital-account controls, limited legal independence, and shallower offshore markets explain the gap between China’s trade volumes and the renminbi’s reserve role. For you, if you are tempted by renminbi-as-reserve-currency narratives, that 2% share and those capital-account constraints reveal that the gap between ambition and structural reality remains very wide.

Morningstar currency research analyst Muhammad Hamza Saleem argues that no credible competing alternative to the dollar currently exists, a view consistent with the structural checklist above.

Gold and nontraditional currencies filling the gap

Some diversification flows have moved toward gold and a basket of nontraditional reserve currencies, including the Australian dollar, Canadian dollar, and other smaller advanced-economy currencies. Collectively, these nontraditional currencies account for a rising but still modest share of global reserves.

Gold has absorbed meaningful central bank buying, particularly from non-Western institutions seeking assets outside the Western financial system. But gold is not a currency. It does not function as a unit of account for trade and finance, cannot be used to settle cross-border transactions at scale, and offers no yield. Its role is as a diversification asset, not a reserve currency substitute. You can use the three-condition checklist above to evaluate any future contender, whether digital currency, commodity-backed token, or otherwise.

Central bank gold accumulation has roughly doubled over the past four years, reaching approximately 1,000 tonnes per year, driven in large part by institutions seeking reserve assets that carry no counterparty risk from a foreign government’s decisions.

Cyclical weakness versus structural erosion: why the distinction matters for your portfolio

When the dollar falls 5-8% against a basket of currencies over a few months, headlines tend to conflate two very different dynamics. The distinction between them matters more for your portfolio than almost any de-dollarisation commentary you will read.

Cyclical dollar weakness is driven by interest-rate differentials, shifts in risk appetite, and commodity cycles. These produce large but ultimately reversible swings in indices like the DXY. When the Federal Reserve pauses while other central banks hike, the dollar weakens. When risk appetite surges and capital flows into emerging markets, the dollar weakens. These are familiar, tradable moves.

Rate-differential dynamics remain the most powerful short-term driver of dollar moves, with the Fed’s June 2026 guidance shift repricing cut timelines more forcefully than any actual rate decision would have, pushing the DXY back above 100 and reinforcing the case for separating cyclical positioning from structural reserve-share analysis.

Structural reserve currency erosion requires something fundamentally different: sustained loss of confidence in U.S. fiscal and institutional management, combined with the emergence of a rival currency system offering comparable depth, openness, and legal protections. That is a much higher bar, and it is not visible in today’s data.

| Dimension | Cyclical dollar weakness | Structural reserve erosion |

|---|---|---|

| Cause | Rate differentials, risk appetite, commodity cycles | Loss of fiscal/institutional confidence plus rival currency emergence |

| Duration | Months to quarters | Decades |

| Market signal | DXY decline, rate-spread compression | Sustained reserve reallocation, non-dollar trade invoicing at scale |

| Investor response | Tradable via FX pairs and relative-rate views | Fundamental portfolio restructuring |

MUFG senior currency analyst Lee Hardman has pointed to the United States’ weakening fiscal position as a factor that could, if left unaddressed, erode confidence in the dollar over time, making U.S. fiscal management the single most important variable to track. But even Hardman frames this as a risk to monitor, not a crisis in progress.

The IMF’s characterisation remains “very gradual movement away from dollar dominance.” Conflating a cyclical downswing with structural erosion leads to either over-trading or misallocating to premature diversification themes. A cyclical move warrants tactical FX positioning. Structural erosion, if it comes, would demand something far larger in your portfolio, and the evidence for it is not yet in the data.

What conditions would actually signal a regime change

If the structural erosion scenario is not yet visible, what would you need to see before taking it seriously? Four high-threshold conditions would need to be approaching or crossed before the dollar’s reserve role is genuinely threatened. As of mid-2026, none is close to being met.

- Renminbi reserve share clearly and sustainably above 5%. The current share is under 2%. Reaching 5% would require significant capital-account opening, deeper offshore yuan markets, and sustained central bank confidence in Chinese institutional protections. The gap between here and there is enormous.

- Prolonged U.S. fiscal deterioration combined with rising real yields and political inability to stabilise debt dynamics. U.S. fiscal trends are concerning, but the market has not yet priced a sustained loss of confidence. Watch for a combination of rising real yields, failed Treasury auctions, and inability to pass fiscal stabilisation measures.

- Non-dollar commodity pricing at scale. Oil and gas contracts systematically invoiced in euros, renminbi, or other currencies, not marginal side deals but routine pricing. Currently, the dollar’s dominance in commodity invoicing remains firmly intact.

- Euro area institutional deepening. True fiscal union with joint safe assets and fully unified capital markets. The euro area has made incremental progress, but a genuine fiscal union with large-scale joint issuance remains politically distant.

U.S. fiscal deterioration is the variable analysts most consistently identify as capable of converting a slow structural trend into an accelerating one, with net interest payments already consuming roughly 13% of the federal budget and the Congressional Budget Office projecting defence spending to be overtaken by interest costs as a share of GDP by 2034.

The gap between where each condition currently sits and where it would need to reach tells you that de-dollarisation is a decades-long structural theme to monitor in the background, not a near-term trigger for portfolio repositioning. Track these four markers as events develop. When multiple conditions start approaching their thresholds simultaneously, the conversation changes.

The next major ASX story will hit our subscribers first

How the euro, yen, and pound actually trade in a dollar-centric world

Even if de-dollarisation continues its gradual path, the FX moves that matter to your portfolio over a one-to-three year horizon are driven by rate differentials, growth surprises, and political risk, not by reserve share movements. Here is what named analysts are saying about each of the three major non-dollar currencies.

Euro

MUFG’s Lee Hardman sees EUR/USD climbing back toward the upper end of the 1.14-1.18 band as the year progresses through 2026. Morningstar describes the euro as modestly undervalued relative to the dollar, with the USD/EUR exchange rate at approximately 0.87 as of 30 June 2026. The valuation case is constructive, but pushing EUR/USD decisively above 1.20 through the first half of 2027 is expected to prove harder, given that European political pressures are set to build during that period.

Japanese yen

The yen has depreciated to a 40-year low against the dollar, with USD/JPY at approximately 162.53 as of 30 June 2026. Between late April and late May, Japanese authorities committed a record 11.7 trillion yen (approximately $73 billion) to currency support operations, yet the yen has since given back all of those intervention-driven gains. UBP’s Peter Kinsella has lifted his USD/JPY forecast, now expecting the pair to climb to around JPY 164 by the close of 2026, which he views as sitting near the top of the 160-165 resistance zone. MUFG’s Hardman takes a more constructive medium-term view, expecting the pair to retreat into the low 150s by mid-2027, a scenario he ties to the Fed staying on hold and the Bank of Japan lifting its policy rate to 1.5%. Morningstar’s Hong Cheng views the yen as trading well below its fundamental value but notes that weak domestic demand and carry-trade dynamics temper the near-term recovery outlook; a sustained rebound, in her view, requires a more meaningful compression of rate differentials.

British pound

Sterling outperformed expectations through 2026, holding at USD/GBP of approximately 0.75 as of 30 June 2026, despite a backdrop of softer domestic data. Morningstar describes the pound as modestly undervalued against the dollar, though the UK’s underlying fundamentals offer little additional support. Weak productivity, the ongoing drag from post-Brexit trade arrangements, and exposure to energy price swings are structural constraints that keep the directional outlook largely range-bound.

| Currency | Spot (30 June 2026) | Morningstar valuation | Key analyst forecast | Primary risk |

|---|---|---|---|---|

| EUR | USD/EUR ~0.87 | Modestly undervalued | MUFG: upper end of 1.14-1.18 range (2026) | European political risk intensifying into 2027 |

| JPY | USD/JPY ~162.53 | Structurally cheap | UBP: up to JPY 164 (year-end 2026); MUFG: low 150s (mid-2027) | Rate-normalisation timing and carry trade persistence |

| GBP | USD/GBP ~0.75 | Modestly undervalued | Neutral; constrained range | Post-Brexit structural drag and energy vulnerability |

For your FX exposure, valuation supports a constructive medium-term view on all three currencies, but timing depends on rate paths and political developments rather than on de-dollarisation progress.

Non-dollar currency positioning is where the cyclical-versus-structural distinction becomes most practically relevant: UBS formally backed five currencies including the pound, Australian dollar, and Norwegian krone in June 2026, while Goldman Sachs issued a simultaneous counterpoint citing AI-driven growth and energy cost asymmetry as structural dollar supports.

Treating de-dollarisation as the background theme it actually is

The evidence lines up consistently. Over roughly two decades, the dollar’s share of global reserves has slid from around 72% to around 57%, a real but slow-moving shift that exchange-rate valuation effects cause the headline figures to overstate. No single rival currency meets the structural requirements to replace it. The IMF describes “very gradual movement away from dollar dominance.” The Federal Reserve concludes that the dollar’s international usage is “little changed over the past 5 years.”

The one variable that could change the trajectory is U.S. fiscal management. MUFG’s Hardman points to a sustained inability to bring debt dynamics under control as the scenario most likely to deepen any loss of confidence in the dollar beyond what current data capture, which is precisely why it deserves more attention than the factors most commentary fixates on.

Your practical takeaways:

- De-dollarisation is a slow structural trend to monitor over years and decades, not a catalyst for near-term portfolio repositioning.

- FX strategy should revolve around rate differentials, growth surprises, and risk sentiment rather than predictions of dollar collapse.

- The euro, yen, and pound trade primarily on their own macro and political stories; valuation supports a constructive medium-term view on each, contingent on rate paths.

- Incremental diversification, including exposure to nontraditional reserve currencies and gold, makes sense as a long-horizon risk-management choice but is not a substitute for dollar liquidity.

- U.S. fiscal management is the key risk variable: monitor it as a slow-burning condition, not an imminent trigger.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding currency forecasts and fiscal scenarios are subject to change based on market developments and policy decisions.