What a Random ASX Backtest Reveals About Managing Market Risk

5 hrs ago

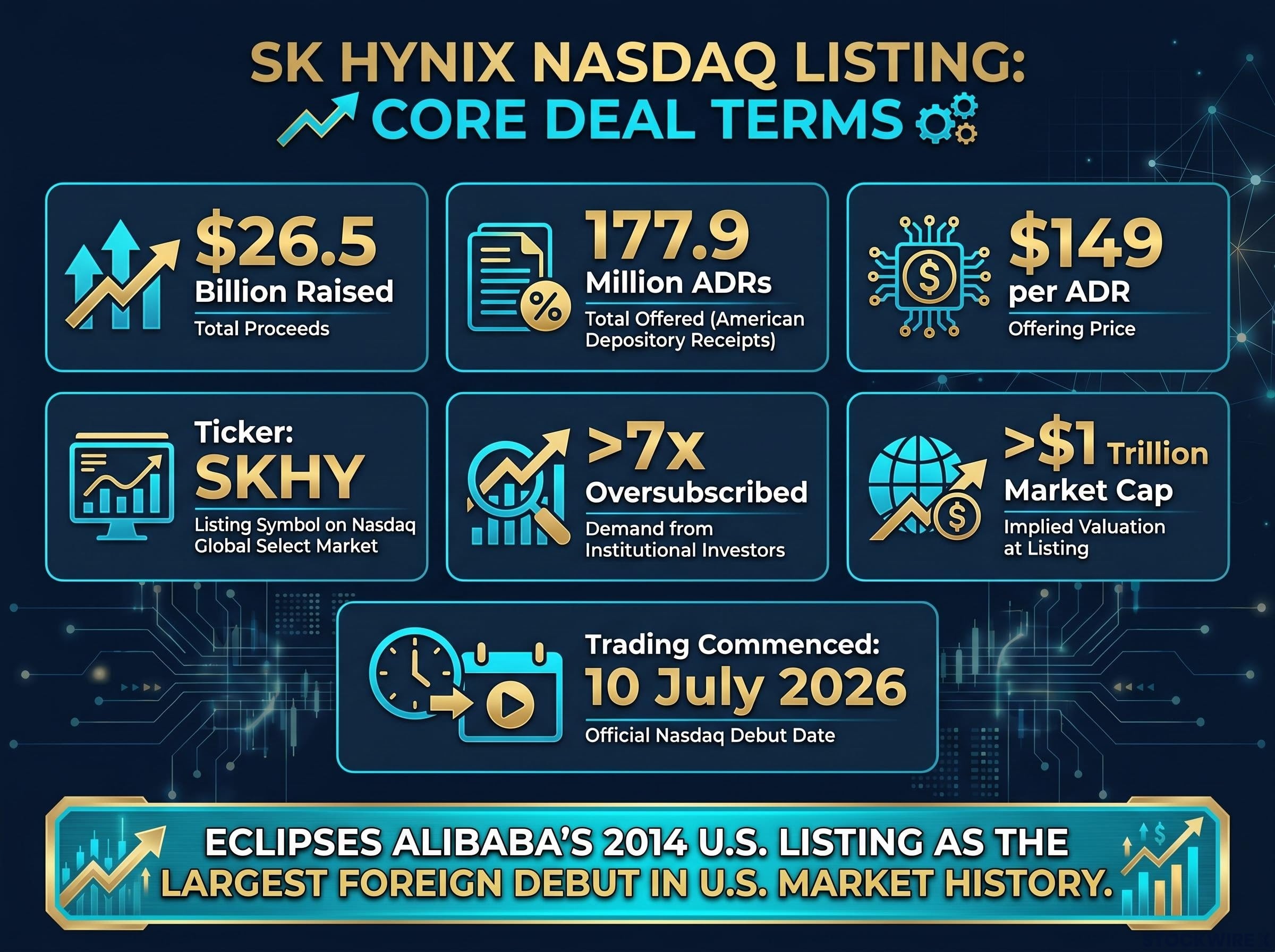

SK Hynix raised $26.5 billion on Nasdaq overnight, pricing 177.9 million American Depositary Receipts at $149 each in an offering that attracted demand exceeding available supply by a factor of more than seven. It is the largest foreign debut and the largest ADR offering in U.S. market history.

This is not a generic chipmaker arriving on an American exchange. SK Hynix is the dominant supplier of high-bandwidth memory (HBM), the specialised chip architecture that sits inside every Nvidia AI accelerator powering the global data-centre build-out. That position explains why institutional demand overwhelmed supply by a factor of seven, and why the listing matters well beyond the corporate finance headline.

Three things determine whether this listing is relevant to your portfolio: what the ADR structure actually gives you access to, what is driving the demand behind a record-breaking raise, and what the risks look like once the enthusiasm fades from the price. Here is the full read.

The numbers land first. SK Hynix priced 177.9 million ADRs at $149 each, raising approximately $26.5 billion in total proceeds. Trading commenced on 10 July 2026 on Nasdaq under the ticker SKHY.

Core deal terms at a glance:

For context: the raise eclipses Alibaba’s 2014 U.S. listing, making it the largest foreign debut in U.S. market history. That record stood for more than a decade.

The company’s market capitalisation now sits above $1 trillion, supported by a share price that had already climbed approximately 273% year-to-date in Seoul as of early July. The more than 7x oversubscription is not a marketing number. It tells you that institutional investors competed aggressively just to secure allocation, a direct signal of how seriously the professional capital community is treating AI memory as a structural investment theme rather than a momentum trade.

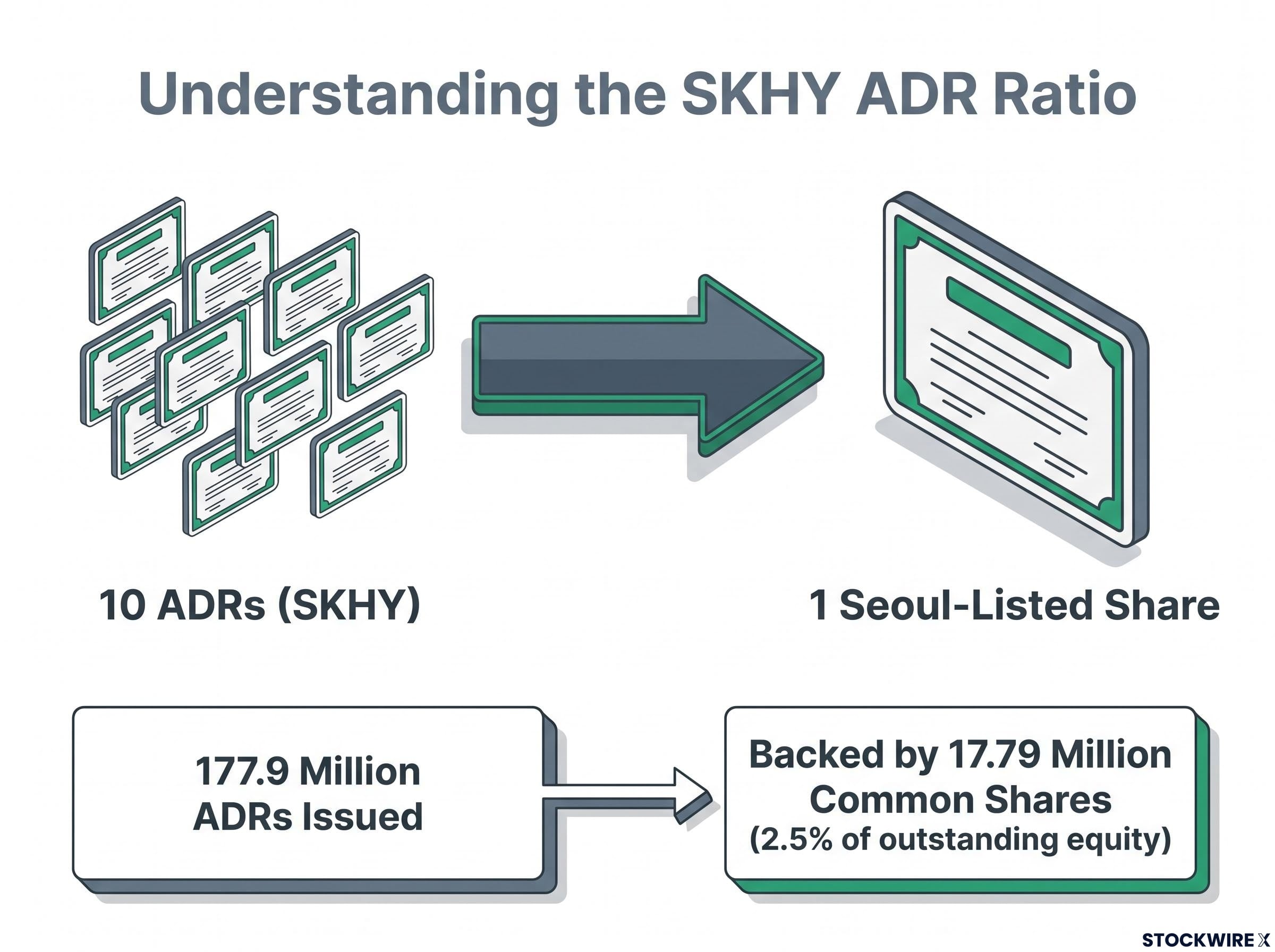

When you buy SKHY on Nasdaq, you are buying an American Depositary Receipt, a U.S.-dollar-denominated security that represents a fractional ownership claim on shares listed in Seoul. A depositary bank holds the underlying Korean shares and issues ADRs against them. In this case, 10 ADRs equal one Seoul-listed SK Hynix share.

The ADRs are backed by 17.79 million newly issued common shares, representing approximately 2.5% of outstanding equity. Dividends paid on the Korean shares are converted from Korean won to U.S. dollars by the depositary bank before reaching ADR holders.

| What the ADR structure removes | What it does not remove |

|---|---|

| Need for a Korean brokerage account | Underlying exposure to KRW/USD exchange rate movements |

| Foreign settlement logistics and direct FX conversion | Korean withholding tax on dividends |

| Operational barriers for U.S. funds and ETFs | Price gaps between Nasdaq and Seoul trading sessions |

Understanding the 10:1 ratio and the currency pass-through is worth your time. If the Korean won weakens against the U.S. dollar, your dollar-denominated return from SKHY will lag the Seoul share performance even if the underlying business is executing well. The reverse also applies: a strengthening won amplifies your dollar return.

Korean withholding tax applies to dividends. U.S. investors may typically recover this through foreign tax credits, though the mechanics depend on individual tax circumstances. For non-U.S. global investors, tax treatment varies by jurisdiction and should be assessed with a local tax adviser.

The demand case starts with a specific competitive position, not broad semiconductor optimism.

SK Hynix holds approximately 50-60% market share in high-bandwidth memory, the stacked DRAM architecture that powers AI GPU clusters. That share makes it the single largest supplier of the memory component most constrained in the current AI build-out.

HBM is the memory architecture sitting directly alongside GPUs in data-centre AI accelerators. It is not interchangeable with standard DRAM. SK Hynix’s role as a primary supplier to Nvidia places it at the centre of the most capital-intensive technology investment theme active today.

Three structural drivers explain the oversubscription:

South Korea’s Kospi index posted a gain of around 5% on 10 July 2026 as chip stocks drove broad market strength on the day trading commenced. The 273% year-to-date run in Seoul is not simply a momentum trade. It reflects a structural repricing of memory from a commodity-cycle asset to a component investors now view as critical AI infrastructure. That repricing is what the current valuation asks you to pay for.

The risk case deserves the same precision as the upside case. Three mechanisms could undermine the thesis, and each operates independently.

It is also worth noting that the Kospi’s 5% session gain on 10 July reflected broader Asian equity market sentiment and strong Wall Street tailwinds, not solely SK Hynix fundamentals.

SKHY is a concentrated play on HBM and DRAM specifically. Investors seeking broader AI semiconductor exposure may consider combining it with logic chip designers, foundries, equipment makers, or diversified semiconductor ETFs to spread single-segment risk.

The convergent signals from 10 July are hard to dismiss. A 5% Kospi session gain. A more than 7x oversubscribed offering. A 3% pricing premium to Seoul shares that buyers willingly paid. And the largest foreign debut in U.S. market history. Taken together, they point to a structural capital rotation into AI memory, not a speculative one.

That consensus, however, is precisely what makes the forward question harder. The AI memory supercycle thesis is now the institutional consensus position. The upside surprise scenario from here requires AI capex to exceed current elevated expectations, not merely meet them. When the professional money community has already expressed its conviction this clearly in both price and allocation demand, the reader’s relevant question shifts. It is no longer “should I follow institutional capital?” It is “what would need to be true for this consensus to be wrong?”, and whether the answer makes you uncomfortable.

The listing is the largest foreign debut in U.S. market history. The access question is now settled. The conviction question is not.

SK Hynix’s Nasdaq listing permanently changes access for global investors, regardless of what the stock does from here. That structural shift is real.

But a strong thesis at a demanding price is a different proposition from a strong thesis at fair value. The AI memory case is credible and well-supported. The price already reflects that credibility.

Two questions determine whether SKHY belongs in your portfolio: how much confidence do you have that HBM demand stays tight enough to sustain current margins, and how much single-company, single-segment concentration can your portfolio absorb? The answers are yours.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The SK Hynix ADR (ticker: SKHY) is a U.S.-dollar-denominated security listed on Nasdaq where 10 ADRs represent one Seoul-listed SK Hynix share; a depositary bank holds the underlying Korean shares and converts any dividends from Korean won to U.S. dollars before passing them to ADR holders.

SK Hynix raised approximately $26.5 billion by pricing 177.9 million ADRs at $149 each, making it the largest foreign debut and the largest ADR offering in U.S. market history, eclipsing Alibaba's 2014 listing.

Institutional demand was driven by SK Hynix's 50-60% market share in high-bandwidth memory, the specialised chip architecture inside every Nvidia AI accelerator, combined with the fact that U.S. funds and ETFs previously unable to hold Korean local shares gained direct access to that position for the first time through the Nasdaq listing.

The three primary risks are memory cyclicality (HBM pricing can compress sharply if capacity overshoots demand), competitive erosion from Samsung and Micron pursuing HBM aggressively, and valuation concentration (a market cap above $1 trillion already prices in sustained AI capex growth and HBM pricing discipline).

Because SKHY dividends and underlying share value are tied to Korean won, a weakening won relative to the U.S. dollar reduces dollar-denominated returns even if the business performs well, while a strengthening won amplifies them.