Turn Your Tech Stack Knowledge Into an Early Investment Edge

1 hr ago

Australia’s equity market has been running on the same core plumbing since the early 1990s. When ASX announced in 2016 that it would replace that plumbing using blockchain-adjacent technology, the project looked like one of the boldest infrastructure bets in global finance. Nearly a decade, an approximately $250 million write-off, a Federal Court penalty, and a complete redesign later, clearing services finally went live in April 2026.

The CHESS replacement is not just a corporate technology story. It is a case study in what happens when a systemically important piece of financial infrastructure meets an unproven technology, optimism bias in large-scale project governance, and regulatory scrutiny that ultimately ended in court. For Australian investors and finance professionals, understanding what went wrong and what the redesign achieved matters because CHESS underpins every equity trade settled on the ASX.

Here is the full arc of this project: what CHESS does, why replacing it proved so difficult, what the failure cost, and what the scaled-back but functioning system means for Australian markets going forward. This gives you a clear framework for evaluating large technology transformation risks in financial infrastructure, with a live example that is still unfolding.

CHESS, the Clearing House Electronic Subregister System, is the infrastructure that sits behind every equity trade on the ASX. It has been operating since the early 1990s, when it replaced paper-based settlement processes. Every time you buy or sell shares on the ASX, CHESS is doing three things:

That third function is what most investors never think about. Your broker shows you a portfolio. But the legally authoritative record of your ownership sits in CHESS.

The T+2 settlement cycle means the cash from a sale is not available for two business days, and shares must be cleared and settled before the record date to qualify for a declared dividend, so the infrastructure running beneath every trade has direct consequences for your portfolio timing decisions.

CHESS is classified as systemically important market infrastructure. That classification, overseen by both ASIC and the Reserve Bank of Australia, means its failure or disruption would have consequences far beyond ASX itself: brokers, custodians, fund managers, and millions of individual investors all depend on it.

In practice, “systemically important” imposes resilience, uptime, and audit requirements that go well beyond what most enterprise technology needs to satisfy. The system must be available when the market is open, it must settle correctly every time, and its integrity must withstand independent scrutiny. That gap between what a technology can do in a pilot and what it must do at infrastructure scale is exactly where the original replacement design failed.

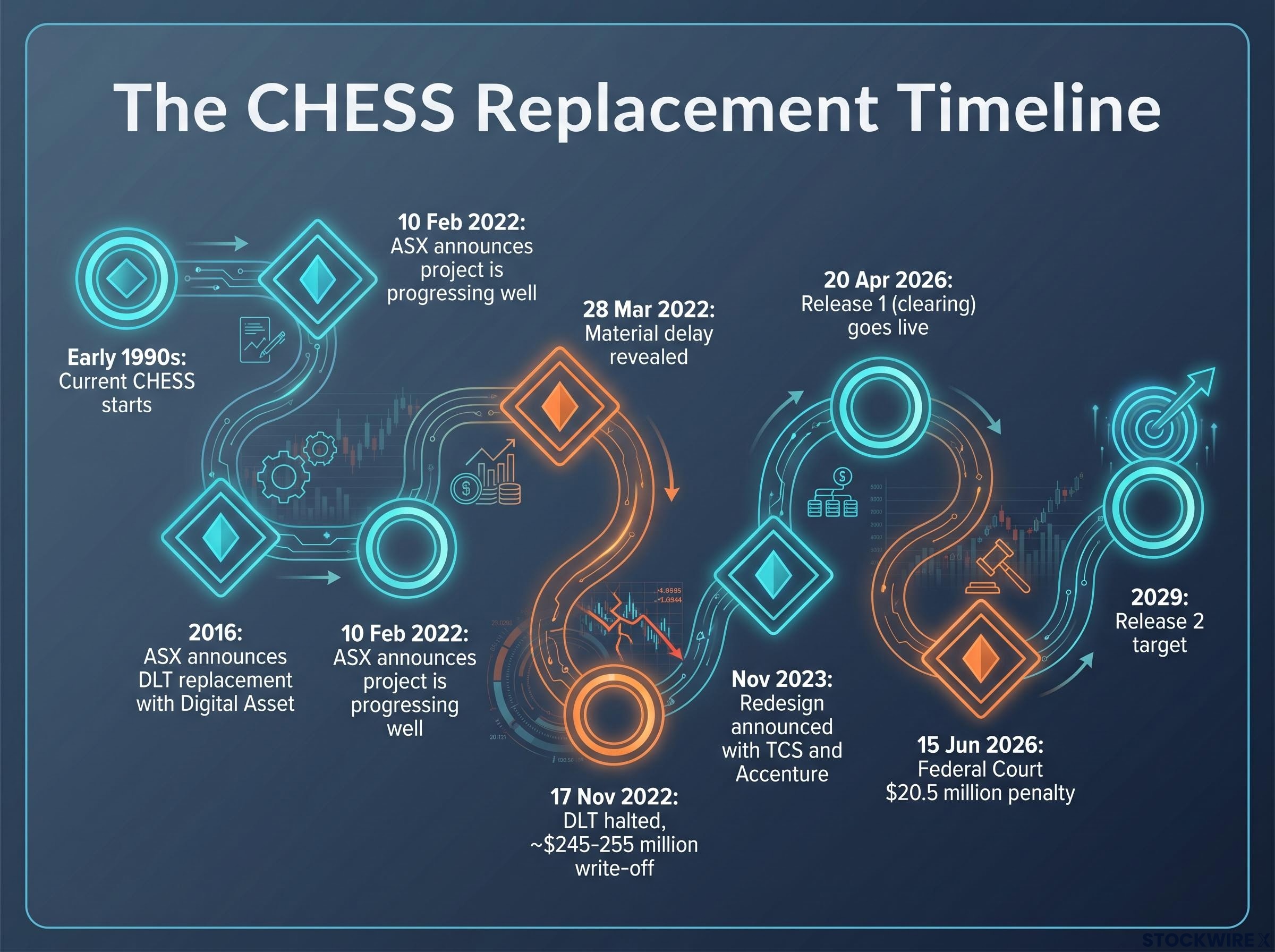

In 2016-17, ASX announced it would replace CHESS using distributed ledger technology (DLT), a shared, tamper-resistant database structure related to blockchain. Digital Asset was selected as the technology partner.

The logic was genuine. DLT promised a shared, immutable ledger across all market participants, which could theoretically reduce the reconciliation work that every broker, custodian, and registry provider had to do separately. Instead of each party maintaining their own records and cross-checking against CHESS, a single distributed ledger could serve as the common source of truth. In 2016, that sounded like a generational upgrade.

The original intended go-live was April 2023. That date itself had already been revised multiple times from even earlier targets, a pattern of slippage that was visible long before the project’s public collapse. If you were watching the timeline move repeatedly before 2022, you already had an early signal that forecasting on this project was unreliable.

DLT in 2016 had not been proven at the scale, resilience, and reliability standards required for systemically important market infrastructure. The gap between a promising technology and a production-ready one proved wider than anyone involved publicly acknowledged.

The collapse did not arrive gradually. It arrived in a sequence so compressed that it reshaped how regulators viewed ASX’s governance.

That six-week gap between “on track” and “significant delay is highly probable” is the single most consequential moment in this story. It is the moment that turned a project setback into a regulatory enforcement matter.

Independent testing and regulatory review identified four interconnected root causes. Each one was serious individually. Together, they were disqualifying.

| Root Cause | What It Meant |

|---|---|

| Technology immaturity | DLT had not been proven at the scale and resilience required for systemically important infrastructure. Novel technology carried production-readiness risks that proved disqualifying. |

| Extreme scope and complexity | The replacement required coordination across the entire industry, touching brokers, custodians, registries, and numerous external systems. This complexity was consistently underestimated. |

| High resilience and audit standards | Core market infrastructure must meet uptime, integrity, and audit standards that commercial technology does not typically need to satisfy. The DLT design struggled to meet these requirements. |

| Governance and transparency failures | Overly optimistic status reporting and inadequate independent assurance meant the market and regulators did not have an accurate picture of project health. Regulators treated this as a conduct issue, not just a project management shortcoming. |

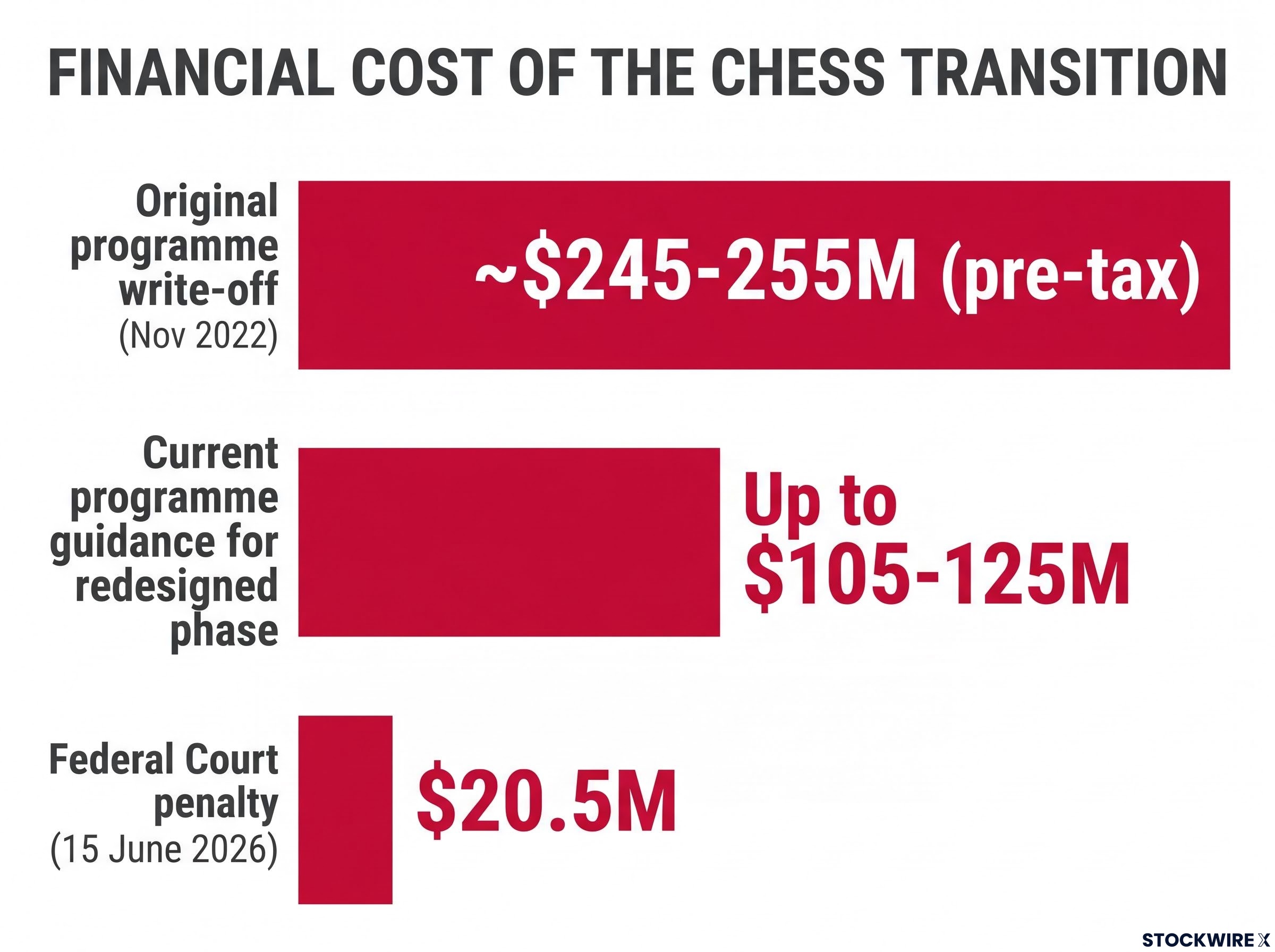

The write-off of approximately $245-255 million largely reflected internal costs: capitalised labour, development, and testing rather than solely vendor payments. It was material relative to ASX’s normal profitability.

For any listed company running a large technology programme, this sequence carries a direct lesson: misleading market communications about material project status carry legal consequences, as ASX later discovered in court.

The technical collapse was only the beginning of the cost.

The $245-255 million pre-tax write-off announced in November 2022 represented the capitalised costs of the failed programme. But total programme investment significantly exceeds that figure. The redesigned replacement programme carries its own guidance of up to $105-125 million in additional expenditure for the current phase alone. The cumulative financial commitment across the full project lifecycle is substantially larger than any single figure suggests.

The capex guidance impact on ASX shares was severe: when the company disclosed FY27 capital expenditure of approximately $180-200 million for ASIC-driven CHESS spending, the market read it as catch-up investment on deferred obligations rather than a growth allocation, contributing to a reported 13.2% single-day share price fall on 26 May 2026.

| Financial Item | Amount | Context |

|---|---|---|

| Original programme write-off | ~$245-255M (pre-tax) | Capitalised costs of the suspended DLT programme (November 2022) |

| Current programme guidance | Up to $105-125M | Additional expenditure for the redesigned programme phase |

| Federal Court penalty | $20.5M | Ordered 15 June 2026; recognised as a non-recurring item in FY26 |

Following a court process that concluded on 15 June 2026, ASX acknowledged that the statement in its 10 February 2022 market announcement that the CHESS replacement was “progressing well” had been misleading. The Federal Court imposed a $20.5 million penalty on ASX for that misleading conduct in connection with the project’s progress.

That admission is worth sitting with. A listed exchange operator, the entity responsible for overseeing market disclosure standards for every other listed company, admitted to publishing a misleading announcement about its own project. The court treated this as an enforceable conduct matter, not an unfortunate communications misstep.

The ASIC settlement proceedings confirmed that ASX admitted to one contravention only, the ‘progressing well’ representation, while ASIC dropped allegations relating to two other statements, a distinction that matters for how investors read the scope of conduct that regulators were ultimately prepared to litigate.

For you as an investor, the combination of a $250 million write-off, substantial ongoing capital expenditure, and a court penalty illustrates that technology transformation risk for a listed company is not confined to project failure. It cascades into earnings, capital allocation, and regulatory standing. If you hold shares in ASX Limited or any listed company undertaking large infrastructure programmes, this is a documented case study in how that risk translates into tangible financial and legal exposure.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

After suspending the DLT-based programme, ASX conducted a strategic review and announced a fundamentally different approach in November 2023. The bespoke distributed ledger was abandoned. In its place, ASX selected a product-based solution from Tata Consultancy Services (TCS), with Accenture serving as solution integrator. This was a deliberate shift toward proven, conventional technology rather than a novel design.

The redesigned programme is structured as two discrete releases:

The shift from a single “big bang” cutover to a staged, two-release delivery model reflects a direct lesson from the original failure. For systemically important infrastructure, the regulator-endorsed approach is incremental validation at each stage, not full replacement in one step.

When you read that CHESS replacement “went live,” that headline captures only half the picture. Clearing functions are on the new system. Settlement and the official subregister of shareholdings are not. The original CHESS platform has not been decommissioned and continues to operate for those functions.

This means a dual-running period is underway, with the legacy system and the new system operating in parallel across different functions. Full decommissioning of legacy CHESS remains tied to the 2029 Release 2 timeline. From the 2016-17 announcement to the 2029 target, the full project lifespan spans over a decade for a single infrastructure replacement.

Your clearing is now on the new system. Your ownership records are still on the old one.

The CHESS replacement is a single project, but the patterns it exposed apply whenever a listed company undertakes a large technology programme. Here are five diagnostic signals you can draw from it.

ASIC enforcement patterns in 2025-2026 show a regulator increasingly willing to pursue civil penalties for systemic reporting failures, with Macquarie Securities facing a $35 million penalty for 14 years of corrupted short sale transactions, suggesting the CHESS action sits within a broader shift toward assertive conduct regulation across Australian market infrastructure.

Optimism bias in complex programmes is a governance failure, not just a forecasting error. When internal teams consistently report progress that does not withstand independent scrutiny, the assurance framework has broken down.

The arc from the 2016-17 announcement to the April 2026 clearing go-live resolved one question: whether ASX could deliver a functioning replacement for any part of CHESS. It did.

The questions that remain are specific. Will Release 2 deliver settlement and subregister functions against the 2029 target? Can the dual-running period be managed without disruption to either system? And will legacy CHESS be safely decommissioned without affecting the official record of share ownership for millions of Australians?

Clearing is live. The court matter is resolved. But the full replacement of Australia’s equity settlement and subregister infrastructure remains a multi-year exercise with real execution risk. The project that began as a bold technology bet is now, finally, an infrastructure delivery programme. Whether it finishes as one depends on whether the lessons from its first decade were absorbed or merely acknowledged.

Past performance does not guarantee future results. Financial projections and programme timelines referenced in this article are subject to change based on operational conditions and regulatory requirements.

The ASX CHESS replacement is the multi-year programme to modernise the Clearing House Electronic Subregister System, the infrastructure that clears, settles, and records ownership of every equity trade on the ASX. It matters because CHESS underpins every share transaction in Australia, and its replacement directly affects brokers, custodians, fund managers, and millions of individual investors.

The original distributed ledger-based programme resulted in a write-off of approximately $245-255 million (pre-tax) in November 2022, the redesigned programme carries additional guidance of up to $105-125 million for the current phase, and a Federal Court penalty of $20.5 million was imposed in June 2026, making the cumulative financial commitment across the project substantially larger than any single figure.

ASX abandoned the distributed ledger technology design because independent testing revealed the technology had not been proven at the scale, resilience, and audit standards required for systemically important market infrastructure, compounded by extreme industry-wide coordination complexity and governance failures in how project progress was reported to the market.

Clearing services went live on the new system on 20 April 2026, with ASX confirming transition to business-as-usual support on 9 June 2026. However, settlement and subregister functions remain on the legacy CHESS platform and are not targeted for migration until Release 2, which is scheduled for 2029.

The $20.5 million Federal Court penalty confirmed that misleading market announcements about material project status carry enforceable legal consequences for listed companies, not just reputational damage. Combined with the write-off and ongoing capex, the CHESS case shows that technology transformation risk cascades into earnings, capital allocation, and regulatory standing in ways investors need to factor into their assessment of any listed company running a large infrastructure programme.