Why a Company Penalty Doesn’t End Director Liability in Australia

13 hrs ago

A client handed $490,000 to her financial adviser with specific instructions to invest in named stocks. He took the money, traded it for himself, lost it, and then told her nothing had gone wrong.

That is the case ASIC (Australian Securities and Investments Commission) settled in March 2026 when it permanently banned Yanhua (Scott) Chen from the financial services industry, one of the most severe sanctions available to the regulator. The case is worth understanding not because of its headline, but because of what it reveals about how Australian financial regulation actually works when an adviser crosses the line from incompetence into dishonesty.

Here is what Chen did, why the regulator responded the way it did, and what practical steps you can take right now, using free government tools, to protect yourself from the same kind of failure. None of this is abstract policy. Every protective measure in this piece is a direct response to something that went wrong in this case.

The sequence matters here, because each step represents a deliberate choice rather than an error in judgement.

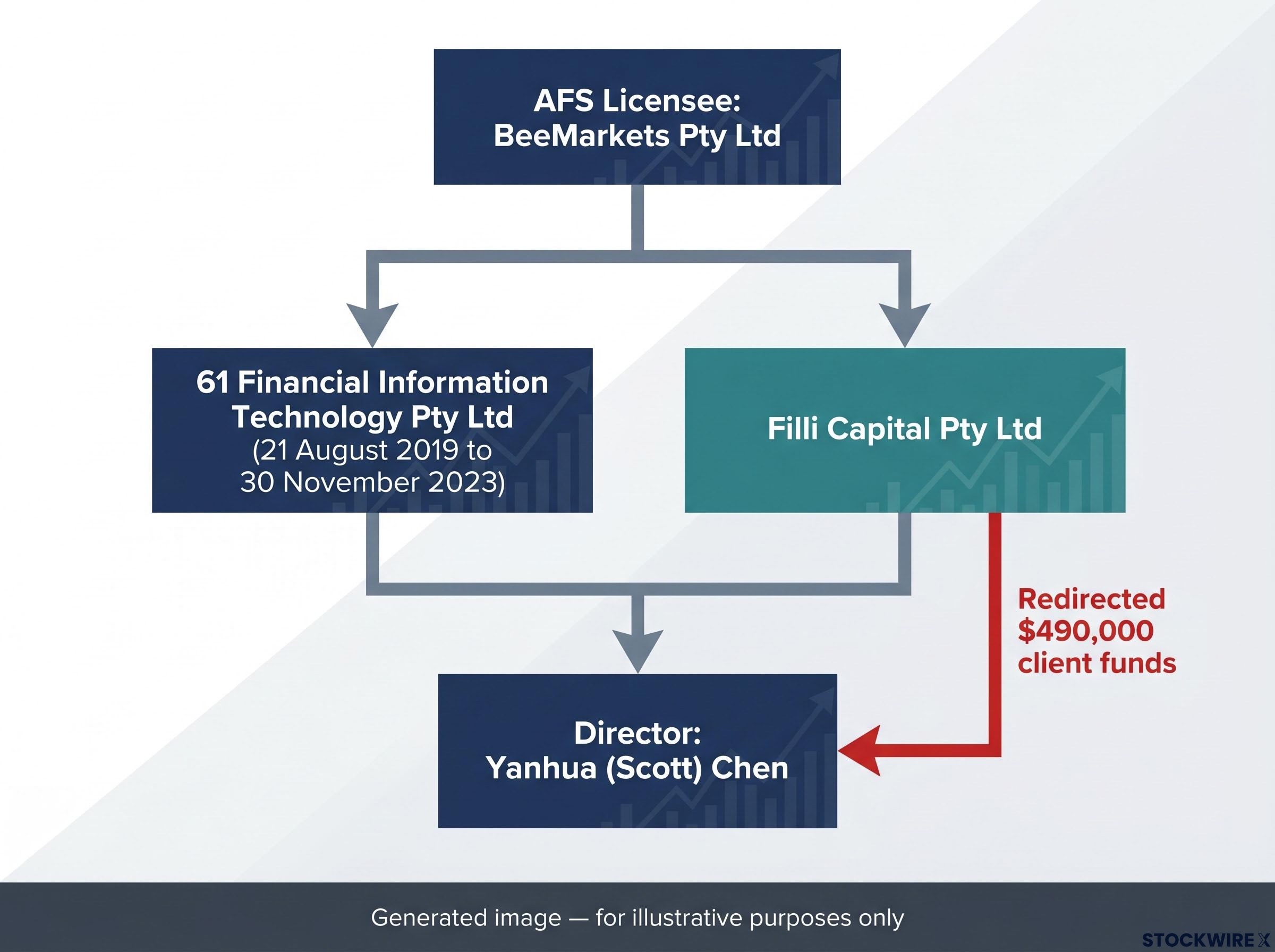

Chen received $490,000 from a client who gave him explicit instructions to invest in specific stocks. Those instructions were clear and documented. He did not follow them. Instead, he redirected the entire sum into personal trading activity, and those trades produced losses that consumed the client’s capital entirely.

That alone would constitute serious misconduct. What followed made it worse.

Chen then actively misled the client, allowing her to believe the money had not been lost. This was not a failure to disclose; it was a decision to deceive.

ASIC’s banning order found that Chen “breached the trust placed in him by his client and led her to believe the money had not been lost.”

ASIC identified two distinct failures in his conduct:

Both 61 Financial Information Technology Pty Ltd (which has since been deregistered) and Filli Capital Pty Ltd listed Chen as a director; the two firms were Melbourne-based financial services businesses. Throughout the period from 21 August 2019 to 30 November 2023, 61 Financial Information Technology Pty Ltd held authorised representative status under the Australian Financial Services (AFS) licence belonging to BeeMarkets Pty Ltd.

This was not a bad investment call or a compliance paperwork failure. It was theft followed by a cover-up, and the distinction matters for how the regulator responded.

On 3 March 2026, ASIC imposed a lifetime prohibition on Chen. The ban carries no end date and is designed to close every route he might use to re-enter the financial services industry.

The banning order covers three broad prohibitions: Chen is barred from delivering any financial service whatsoever; from holding control, whether individually or alongside others, over any business that carries on financial services activities; and from taking up any role, whether as an officer, manager, employee, contractor, or otherwise, that involves performing functions within a financial services business.

That third clause is the one that does the heaviest work. Without it, a banned adviser could re-enter the industry in a back-office role, as a consultant, or through a management position that avoids the title “adviser.” The “any function, any capacity” language eliminates that possibility entirely.

ASIC records the ban permanently on its Banned and Disqualified Register, which is publicly searchable and free to use. Chen’s entry shows a lifetime ban commencing 3 March 2026 with no end date.

ASIC’s Banned and Disqualified Register is publicly searchable at no cost and records every lifetime and fixed-term prohibition imposed by the regulator, including Chen’s entry showing a lifetime ban commencing 3 March 2026 with no end date.

For anyone who might encounter Chen in a professional context in the future, whether as a potential employer, business partner, or prospective client, that register entry is the single most important fact. It is accessible right now, costs nothing, and removes any ambiguity about his status in the industry.

ASIC did not arrive at a lifetime ban by default. It applied a specific test, one that separates conduct warranting permanent exclusion from conduct warranting lesser sanctions.

The test is the “fit and proper person” standard, a core principle in Australian financial services regulation. It assesses whether an individual possesses the honesty, integrity, judgement, and character required to participate in the industry in any role.

In Chen’s case, ASIC was explicit about the outcome.

ASIC concluded that Chen’s conduct “shows that he does not have the necessary judgement and character to operate in the financial services industry.”

His conduct failed the test on multiple grounds simultaneously. The misappropriation demonstrated a failure of integrity. The concealment demonstrated a failure of honesty. Together, they showed a pattern of deliberate wrongdoing that the regulator determined was incompatible with any role in financial services, not just an advisory one.

The fit and proper person threshold is applied consistently across different categories of misconduct, and the Hilellis director ban, which ASIC described as conduct in ‘the worst category of misconduct’ involving false tax returns and $12.4 million in creditor losses, shows how the same integrity standard operates at the ceiling of administrative power.

Understanding why ASIC applied a permanent ban rather than a temporary suspension or a fine comes down to one distinction: the difference between a competence failure and an integrity failure.

| Conduct type | Typical ASIC response | Example |

|---|---|---|

| Competence failure | Remediation, licence conditions, or temporary suspension | Poor-quality advice, inadequate record-keeping, documentation errors |

| Integrity failure | Permanent ban, civil penalties, court action | Theft of client funds, deliberate deception of clients, sustained dishonesty |

The distinction matters for you as an investor. Being bad at your job is a recoverable problem in regulatory terms. Deliberately stealing from a client and lying about it is not. If you ever suspect dishonesty rather than mere poor performance from an adviser, the regulatory system treats that as a categorically different situation, and your response should reflect that urgency.

Chen’s case involves a structural feature of Australian financial services that most investors encounter without fully understanding it. That feature is the authorised representative model, and knowing how it works gives you a clearer picture of who is responsible when something goes wrong.

An authorised representative is an individual or company permitted to provide financial services under another entity’s AFS licence. The licence holder, known as the licensee, is responsible for supervising the representative’s conduct and is ultimately accountable under the law.

In Chen’s case, 61 Financial Information Technology Pty Ltd operated as an authorised representative of BeeMarkets Pty Ltd from 21 August 2019 to 30 November 2023. That means Chen’s firm did not hold its own licence. It provided services under BeeMarkets’ licence, with BeeMarkets bearing supervisory responsibility.

For you as an investor, this creates an additional layer of complexity. You may deal primarily with the representative, the person sitting across from you, but the entity legally responsible for overseeing their conduct is the licensee behind them. If something goes wrong, complaints and claims can involve both the representative and the supervising licensee.

That is why checking both relationships before you commit funds is not a bureaucratic formality. It is a practical protective step.

AFS licence cancellation is a separate regulatory tool from banning orders, and the Capital Guard case illustrates a critical gap it can expose: a firm can hold a valid licence for years while new operators run fraudulent activity inside it, meaning a routine licence check returns a clean result throughout the period of misconduct.

ASIC’s Financial Advisers Register is free, publicly accessible through ASIC’s website and the government’s Moneysmart service, and requires no account to use. On it, you can confirm:

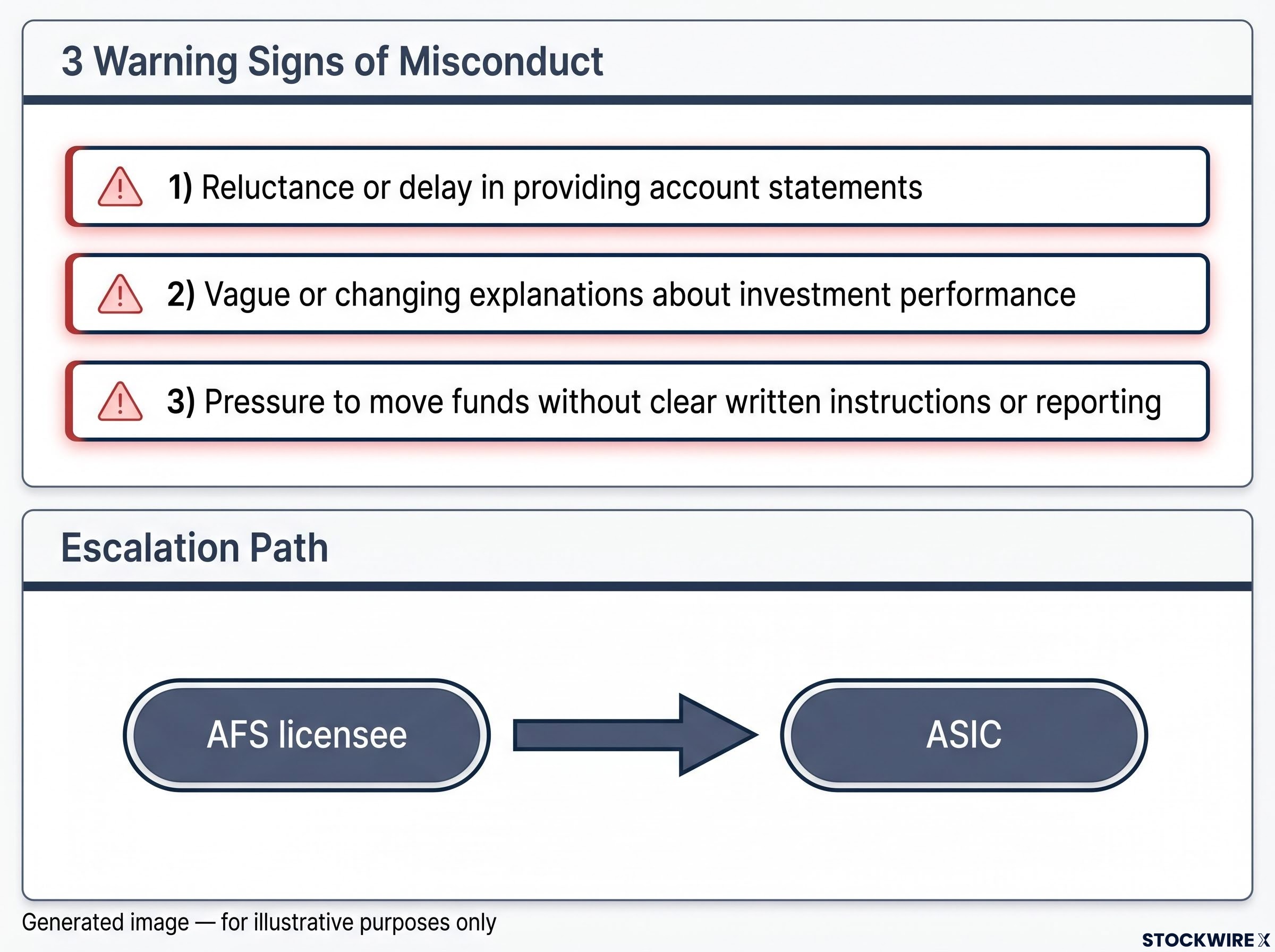

Run a separate search on ASIC’s Banned and Disqualified Register at the same time. The two registers serve different functions: the Financial Advisers Register confirms current authorisation, while the Banned and Disqualified Register reveals whether an individual has been prohibited from the industry.

Both searches take minutes. Both are free. Together, they give you the information Chen’s client did not have.

Every protective step below is a direct countermeasure to something that failed in Chen’s case. These are not generic financial hygiene recommendations; they are targeted responses to the specific ways this particular fraud succeeded.

Each of these steps existed before Chen’s case. His client’s experience is the clearest possible illustration of what happens when they are skipped.

The Chen case does not introduce new regulatory powers. ASIC’s ability to impose lifetime bans, maintain public registers, and pursue individual wrongdoers has been in place for years. What the case does is provide a concrete, specific example of those powers being applied at their fullest extent, and it demonstrates the threshold that triggers them: dishonesty, not just incompetence.

The infrastructure to protect yourself already exists. ASIC’s registers are free, public, and searchable right now. The documentation standards that would have exposed Chen’s fraud are available to any investor willing to request them. The escalation channels to report suspected misconduct are open and accessible.

The Chen case is not isolated. Adviser document fraud involving forged client signatures and fabricated file notes led to a separate ten-year ASIC ban in 2025, a case in which the perpetrator had operated for nearly a decade under a mainstream licensing network without detection.

What this case confirms is that the tools work, but only if you use them before the problem starts. The protective steps outlined in this article are available to you today. The Chen case is the strongest argument for acting on them.

“This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.”

—

An ASIC financial adviser ban is a formal prohibition that bars an individual from providing financial services, controlling a financial services business, or performing any function in any capacity within the industry. A lifetime ban has no end date and closes every re-entry route, including back-office, consulting, and management roles.

Search ASIC's Banned and Disqualified Register, which is free and publicly accessible through ASIC's website with no account required. Run a second search on ASIC's Financial Advisers Register at the same time to confirm current authorisation status; the two registers serve different functions and together give a complete picture.

Chen received $490,000 with explicit instructions to invest it in specific named stocks, redirected the entire sum into personal trading activity instead, lost it, and then actively misled the client into believing the money had not been lost. ASIC found he both misappropriated client funds and deliberately concealed the loss.

The fit and proper person standard is the test ASIC applies to determine whether an individual has the honesty, integrity, judgement, and character required to participate in the financial services industry in any role. In Chen's case, ASIC concluded his conduct showed he did not meet that standard, which is why a lifetime ban rather than a temporary suspension was imposed.

The Chen case highlights three specific red flags: reluctance or delay in providing account statements, vague or changing explanations about investment performance, and pressure to move funds without clear written instructions or reporting. Any of these should prompt immediate questioning and, if unresolved, a formal complaint to the AFS licensee or directly to ASIC.