Why ASIC Issued a Lifetime Ban After a $490,000 Client Fraud

14 hrs ago

A $4 million corporate penalty and a separate personal legal action against the former CEO, both arising from the exact same set of facts. Most investors assume that once the company pays, the regulatory chapter closes. It does not.

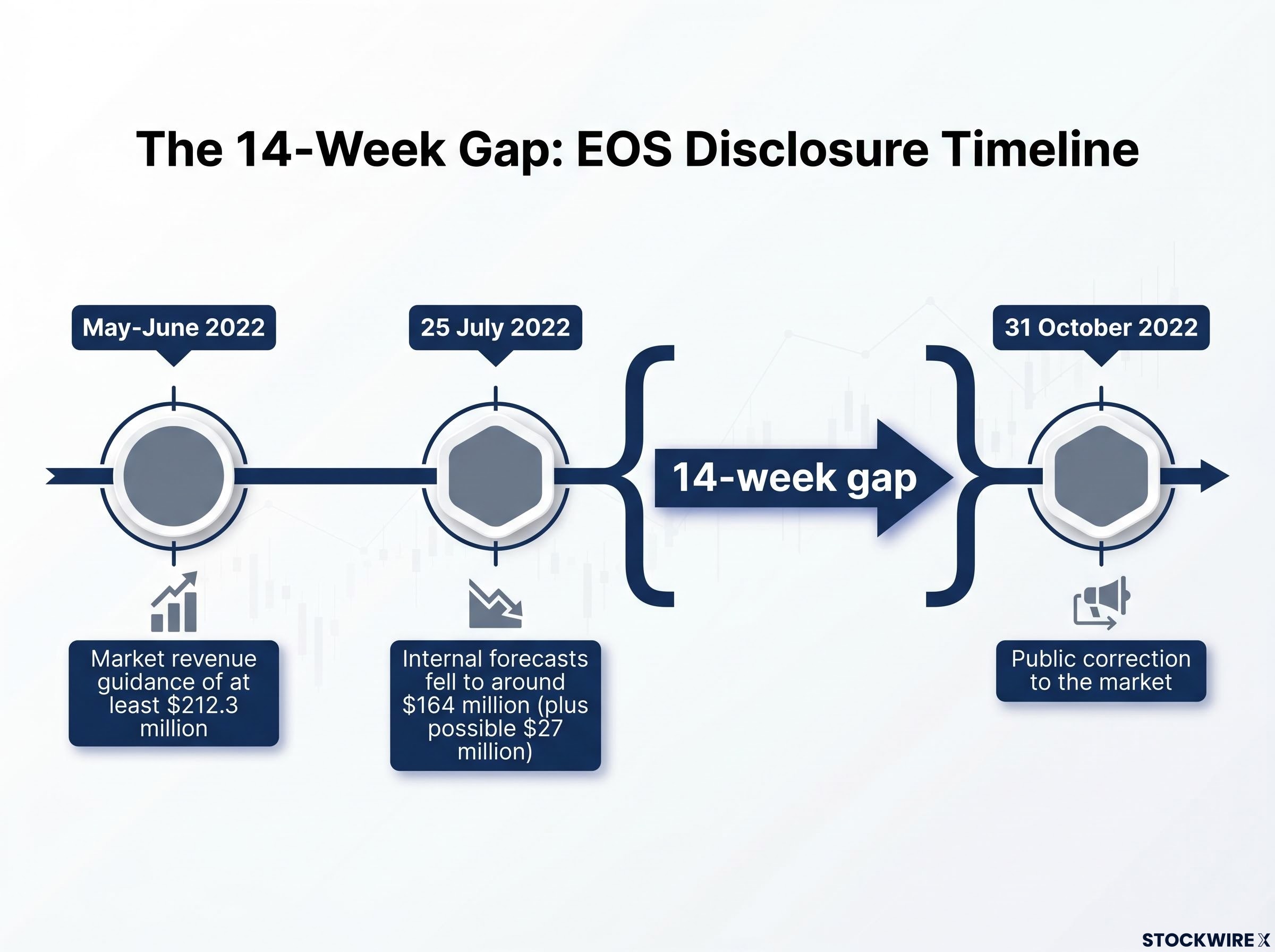

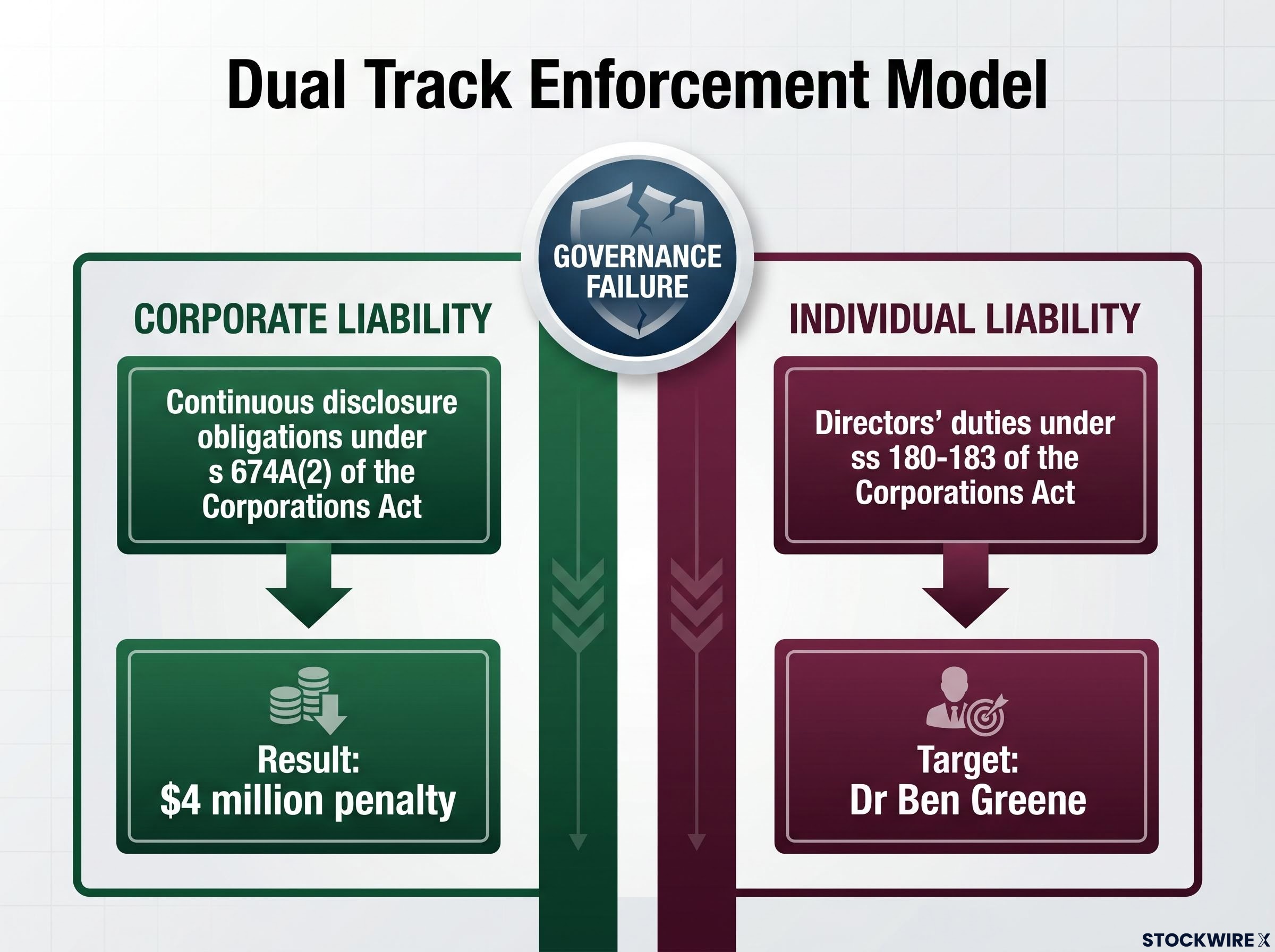

Electro Optic Systems Holdings Limited (ASX: EOS) gave the market revenue guidance of at least $212.3 million between May and June 2022. By 25 July 2022, internal forecasts had dropped to approximately $164 million. The company did not correct the market until 31 October 2022, a gap of roughly 14 weeks. Declarations were made by the Federal Court that EOS had contravened s 674A(2) of the Corporations Act, with the Court ordering a $4 million pecuniary penalty as a consequence. On a separate track, ASIC brought its own proceedings against former CEO and Director Dr Ben Greene, targeting alleged directors’ duties violations connected to the same underlying events.

Here is how that dual accountability system works, and what it tells you about governance risk in the companies you hold. After this, you will understand that Australian corporate law runs two parallel enforcement tracks over the same governance failure, what personal duties directors owe, and what to look for in board conduct when assessing ASX-listed companies.

The sequence matters here, because it is the sequence that created the legal exposure.

That 14-week gap between internal awareness and public disclosure is the factual core of everything that followed. It is the gap that created exposure at both the corporate and individual level.

The disclosure obligation attaches at the point of internal awareness, not at the point of board sign-off or formal announcement preparation, a distinction at the heart of how continuous disclosure obligations are interpreted and enforced across ASX-listed companies.

The Federal Court, with Justice Ian Jackman presiding, issued formal declarations that EOS had breached s 674A(2) of the Corporations Act 2001 (Cth). The proceedings were resolved on the basis of facts and admissions that both parties had agreed upon. The Court imposed a $4 million pecuniary penalty on EOS, plus costs, calibrated to the company’s size and financial capacity.

ASIC’s media release on the EOS penalty confirms the agreed facts underlying both enforcement tracks, including the specific 14-week disclosure gap and the existence of separate proceedings against Dr Greene as an individual respondent.

ASIC Chair Joe Longo provided public commentary on the outcome, reinforcing the regulator’s position that timely disclosure of material information is a cornerstone of market integrity.

But the corporate penalty was not the end of the matter. ASIC initiated a separate action against Dr Ben Greene personally, alleging that his conduct during the relevant period amounted to breaches of directors’ duties. The corporate outcome settled the company’s liability. The individual proceedings address whether the person at the centre of the failure met his personal legal obligations. Those are two distinct questions under Australian law, and they are answered in two separate actions.

You do not need a law degree to understand what directors owe. There are four core statutory duties under the Corporations Act 2001 (Cth), and each one is a distinct obligation you can name and recognise.

| Section | Duty name | What it requires | Relevance to disclosure |

|---|---|---|---|

| s 180 | Care and diligence | Act with the care and diligence of a reasonable director in similar circumstances | A director who knows of material undisclosed information must actively ensure the market is informed; passivity can itself constitute a breach |

| s 181 | Good faith and proper purposes | Act in good faith in the best interests of the company and for proper purposes | Withholding material information from the market can conflict with the company’s interests and its listing obligations |

| s 182 | Not to improperly use position | A director must not use their position to gain an advantage or cause detriment | Controlling the timing or content of disclosure for improper purposes is a potential breach |

| s 183 | Not to improperly use information | A director must not use information obtained through their role for improper purposes | Access to material non-public information creates obligations around its handling and disclosure |

The detail that changes how you should think about these duties is their non-delegable character. A director cannot discharge their legal obligation by delegating disclosure oversight to management and assuming it is handled. Relying on a company’s disclosure framework or taking management representations on trust does not protect a director from personal liability if something goes wrong.

The Star Entertainment proceedings extended section 180 liability beyond financial compliance failures, confirming that executives who control the flow of risk information to the board can be held personally responsible even when the board itself is cleared, a principle that applies with equal force to disclosure decisions.

Three characteristics make these duties personally enforceable:

When you are evaluating governance quality in an ASX-listed company, knowing these duties exist and are personal gives you a framework for assessing whether a board is actively engaged or passively compliant. That distinction matters most when bad news is emerging inside the company.

Knowing that duties exist is one thing. Understanding what happens when they are breached is what makes the stakes real.

A director found to have breached their duties can face four categories of consequence:

These are not theoretical possibilities. They are the tools ASIC uses in enforcement proceedings, and the EOS matter illustrates how they apply in practice. The proceedings against Dr Greene carry the potential for personal financial penalties and professional consequences that are entirely separate from the $4 million penalty the company has already absorbed.

This is the counterintuitive point that catches many investors off guard. Liability attaches to conduct during tenure, not to current employment status. Dr Greene’s departure from EOS did not extinguish his exposure. The proceedings against him are separate from and persist independently of the corporate penalty already applied to the company.

Australian enforcement timelines mean investigations or proceedings can continue for years after a director leaves. A “management clean-up” following a governance failure is a beginning of accountability, not the end of it. If you are assessing a company that has recently replaced senior leadership after a disclosure issue, any ongoing regulatory proceedings should remain part of your risk assessment. An executive resignation is not a governance reset; it is a personnel change.

Australian corporate enforcement is designed with two deliberately separate channels, and the EOS case is the worked example of both operating simultaneously.

| Track | Legal basis | Who bears the consequence |

|---|---|---|

| Corporate liability | Continuous disclosure obligations under s 674A(2) of the Corporations Act | The listed company (and by extension, its shareholders through the financial penalty) |

| Individual liability | Directors’ duties under ss 180-183 of the Corporations Act | The individual director or officer personally |

The logic behind pursuing individuals as well as companies is straightforward. Company penalties are ultimately borne by shareholders. A $4 million fine comes out of the company’s cash, which means the people who already suffered from the disclosure failure (shareholders who traded on incomplete information) bear the cost again. Individual proceedings place consequences directly on the decision-makers, strengthening deterrence where it is most effective.

ASIC’s stated enforcement rationale centres on market integrity and investor protection. When specific individuals are central to a failure, separate actions target responsibility precisely rather than distributing it across the corporate entity. This is proportionate accountability by design, not an accidental doubling of punishment.

What this means for you in practice: a company settlement, however large, is not a reliable signal that individual accountability has been resolved. If you are following an enforcement case, treat the corporate and personal proceedings as independently live until both are concluded. One resolving does not predict or accelerate the other.

The legal mechanics matter, but they translate into three specific signals you can monitor from publicly available information. You do not need insider knowledge to apply this framework; you need to know what to look for in the materials that are already available.

The 14-week gap in the EOS case is a concrete benchmark for what “material delay” looks like in a real enforcement context. When you see a company revise guidance months after the internal numbers changed, the EOS precedent tells you exactly how regulators view that behaviour.

Governance risk is about people, not just policies. Board charters and risk frameworks only work if individual directors actively engage with their duties. Your assessment should focus on track records, how boards respond to bad news, and whether disclosure patterns suggest active oversight or passive reliance on management. The fact that a passive or hands-off stance can itself constitute a breach of the duty of care and diligence under s 180 tells you where the legal line sits.

A structured governance risk assessment for ASX holdings goes beyond reviewing board charters; it requires examining how risk information travels from operational teams to senior executives, whether escalation failures are disclosed, and whether recent regulatory history suggests a pattern rather than an isolated event.

The $4 million penalty against EOS and the separate proceedings against Dr Ben Greene together confirm a structural feature of Australian markets that every investor should understand: enforcement operates at both the corporate and personal level over the same governance failure. These are not redundant actions. They are two different questions, directed at two different entities, with two different sets of consequences.

For you as an investor, understanding director liability in Australia is not a niche legal concern. It is part of how you assess governance risk in ASX-listed companies. The existence of personal liability for directors is one of the mechanisms that creates an incentive for boards to disclose promptly and accurately. When that mechanism works, it directly affects the reliability of what listed companies tell the market.

Systemic governance failures at the operator level, where risk management is not integrated into daily operations and culture reinforces passive oversight rather than active challenge, represent the environment in which individual directors are most exposed to personal liability when a specific disclosure event occurs.

Continuous disclosure exists to keep all investors equally informed. Individual director accountability is part of the system that makes that obligation credible. The EOS matter confirms that the system has teeth at both levels, and that you should assess governance accordingly.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements regarding ongoing proceedings are based on publicly available information and are subject to change based on future court outcomes and regulatory developments.

Director liability in Australia refers to the personal legal obligations directors owe under the Corporations Act 2001, including duties of care and diligence (s 180), good faith (s 181), and prohibitions on improperly using their position or information (ss 182-183). Breaching these duties can result in personal financial penalties, disqualification, compensation orders, or criminal prosecution, entirely separate from any penalty imposed on the company.

Continuous disclosure obligations require ASX-listed companies to immediately inform the market of any material information that a reasonable investor would expect to affect the share price. The disclosure obligation attaches at the point of internal awareness, not when the board formally approves an announcement, a distinction confirmed in the EOS case where a 14-week gap between internal knowledge and public correction formed the basis of the breach.

Yes. Liability under Australian directors' duties law attaches to conduct during tenure, not to current employment status. The separate proceedings against EOS former CEO Dr Ben Greene confirm that an executive departure does not extinguish personal regulatory exposure, and ASIC can continue pursuing individuals for years after they leave the company.

EOS was ordered to pay a $4 million penalty for a continuous disclosure breach under s 674A(2) of the Corporations Act, arising from a 14-week gap between an internal revenue downgrade and public guidance correction. Separately, ASIC brought its own proceedings against former CEO Dr Ben Greene personally for alleged directors' duties violations connected to the same events, demonstrating that corporate and individual liability operate on independent tracks.

Three observable signals are the most reliable indicators: long gaps between internal recognition of material changes and public disclosure, executive departures paired with ongoing regulatory investigations, and repeated patterns of optimistic guidance followed by sharp downward revisions. The EOS case provides a concrete benchmark, a 14-week disclosure delay, for what regulators classify as a material breach.