Why the Mid-Cap Rotation Beat Mega-Cap Tech in June 2026

2 hrs ago

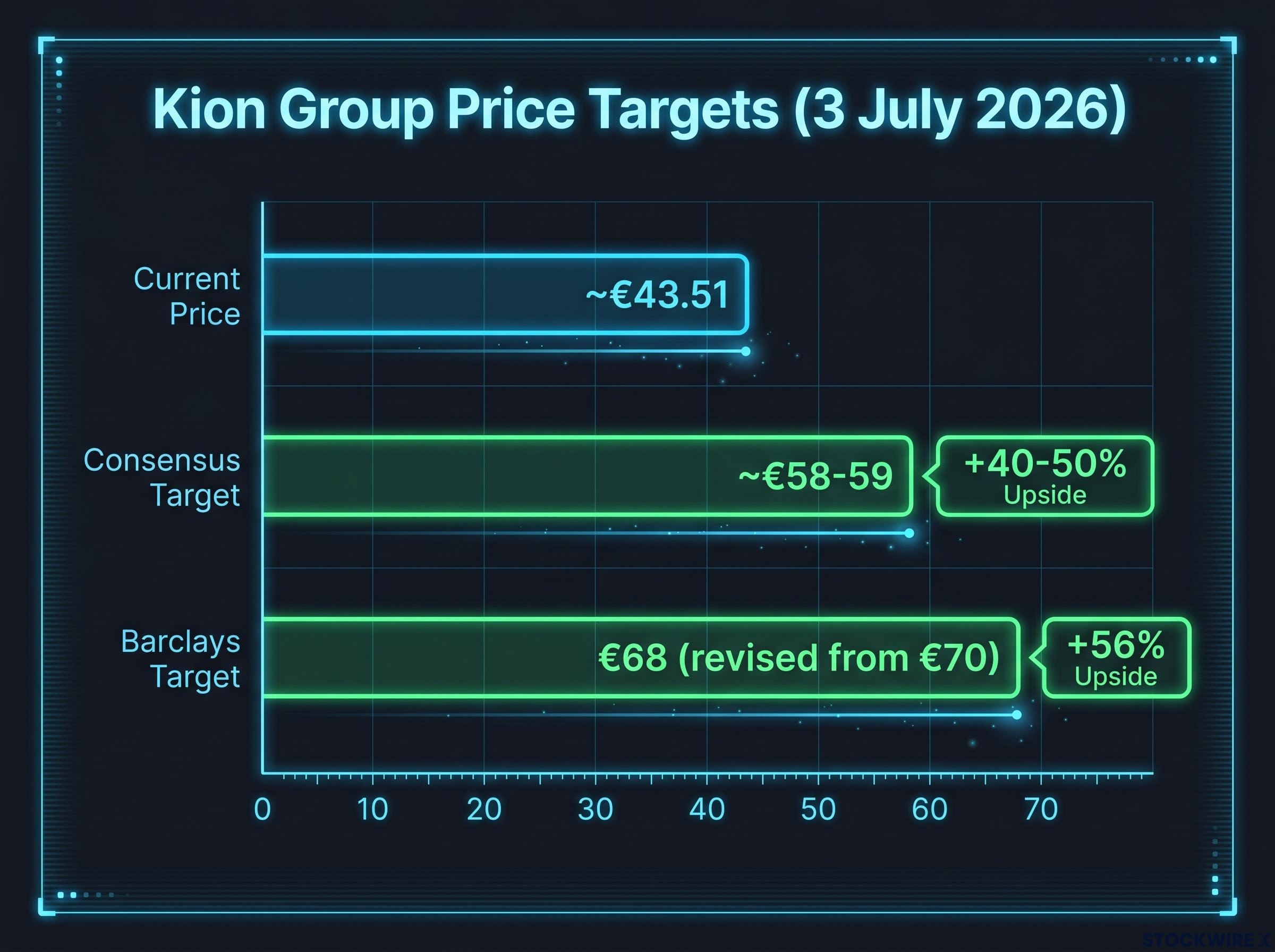

Kion Group shares trade at roughly €43.51. Barclays thinks they should trade at €68. That gap, approximately 56%, is the entire argument compressed into two numbers: either the market has accurately priced a company facing real headwinds, or it has overcorrected into a valuation that already assumes the worst.

On 3 July 2026, Barclays issued a revised note keeping its overweight rating on Kion while cutting its price target from €70 to €68, a reduction that reflects scaled-back earnings assumptions rather than a change in directional conviction. The move is deliberate. The bank is not dismissing the problems in European warehouse automation stocks. It is arguing that investors who sold through the drawdown have left an entry point that is now closing.

Here is what the Barclays thesis actually rests on, where the numbers support it, where the risks sit, and what conditions need to hold for the trade to work. This is a decision-support piece, not a summary of a broker note.

Three overlapping pressures have pushed valuations down across the sector, and none of them are subtle:

These headwinds did not arrive one at a time. They stacked. The macro slowdown reduced demand, inflation ate into margins on the demand that remained, and Chinese competition threatened to make the margin compression structural rather than cyclical. That accumulation is why sentiment turned as sharply as it did.

Kion Group shares have traded in a range of approximately €41-44 in recent sessions, well below levels that prevailed before the sector drawdown began. Barclays itself trimmed earnings estimates and lowered its Kion price target from €70 to €68, explicitly accounting for slower expansion and margin compression. The bank is not ignoring the headwinds. It is pricing them in and then asking: is there still upside from here?

This is where the Barclays thesis either holds or breaks. If the demand case for warehouse automation is structurally impaired, meaning companies no longer need to automate at the same rate, then the current valuations are not a discount. They are a correction to a lower reality.

Barclays argues the opposite. Order activity within warehouse automation has held steady, which is the single most important data point separating a demand-destruction story from a margin-compression story. Demand is intact; it is margins and sentiment that have compressed.

The thesis does not require a European macro recovery. It requires stabilisation. That distinction matters for timing: you are not waiting for a growth reacceleration. You are waiting for conditions to stop deteriorating, which is a lower bar and, historically, a more predictable one.

The logic assembles in three steps. First, the observation: valuations across European warehouse automation have compressed to levels that reflect a deeply pessimistic earnings outlook. Second, the inference: the negative forces that drove the selloff, spanning broader economic uncertainty, cost pressures, and the advance of Chinese forklift rivals, have been absorbed into share prices rather than sitting as unpriced future risk. Third, the implication: the risk-reward has shifted, because the downside scenarios are already in the price while the structural demand drivers remain.

Barclays took the view that sector headwinds had been fully reflected in current stock prices, making this the thesis-defining claim: the market has done the discounting work, and what remains is asymmetric upside.

“Buying into weakness” is the phrase Barclays uses, and it means something specific. It is not a call to buy ahead of a near-term catalyst. It is a recommendation to enter after a valuation reset, with a medium- to long-term horizon, on the basis that structural demand from e-commerce growth, labour shortages, rising wages, and throughput efficiency requirements will reassert itself as the cycle normalises.

Barclays’ view is explicitly more bullish than the analyst consensus. Consensus targets sit at approximately €58-59 (unverified), implying roughly 40-50% upside from recent trading levels. Barclays’ €68 target implies approximately 56%. What this tells you is that even the more cautious analyst community sees material upside from current levels. The direction of the trade is not in dispute; the magnitude is.

The Kion thesis does not exist in isolation: on the same date Barclays revised its Kion target, the bank also formally upgraded European equities more broadly, citing wider sector participation and upward-turning economic surprise indices, while institutional European equity positioning remained near its most underweight since December 2024, a gap that defines the broader context in which this specific stock call sits.

| Reference Point | Price (€) | Implied Upside |

|---|---|---|

| Kion current share price (3 July 2026) | ~€43.51 | — |

| Analyst consensus target (unverified) | ~€58-59 | ~40-50% |

| Barclays price target | €68 | ~56% |

The gap between all three numbers narrows the range of scenarios in which this trade fails outright. Even if Barclays is too aggressive and the consensus is closer to correct, the implied upside from current levels remains substantial.

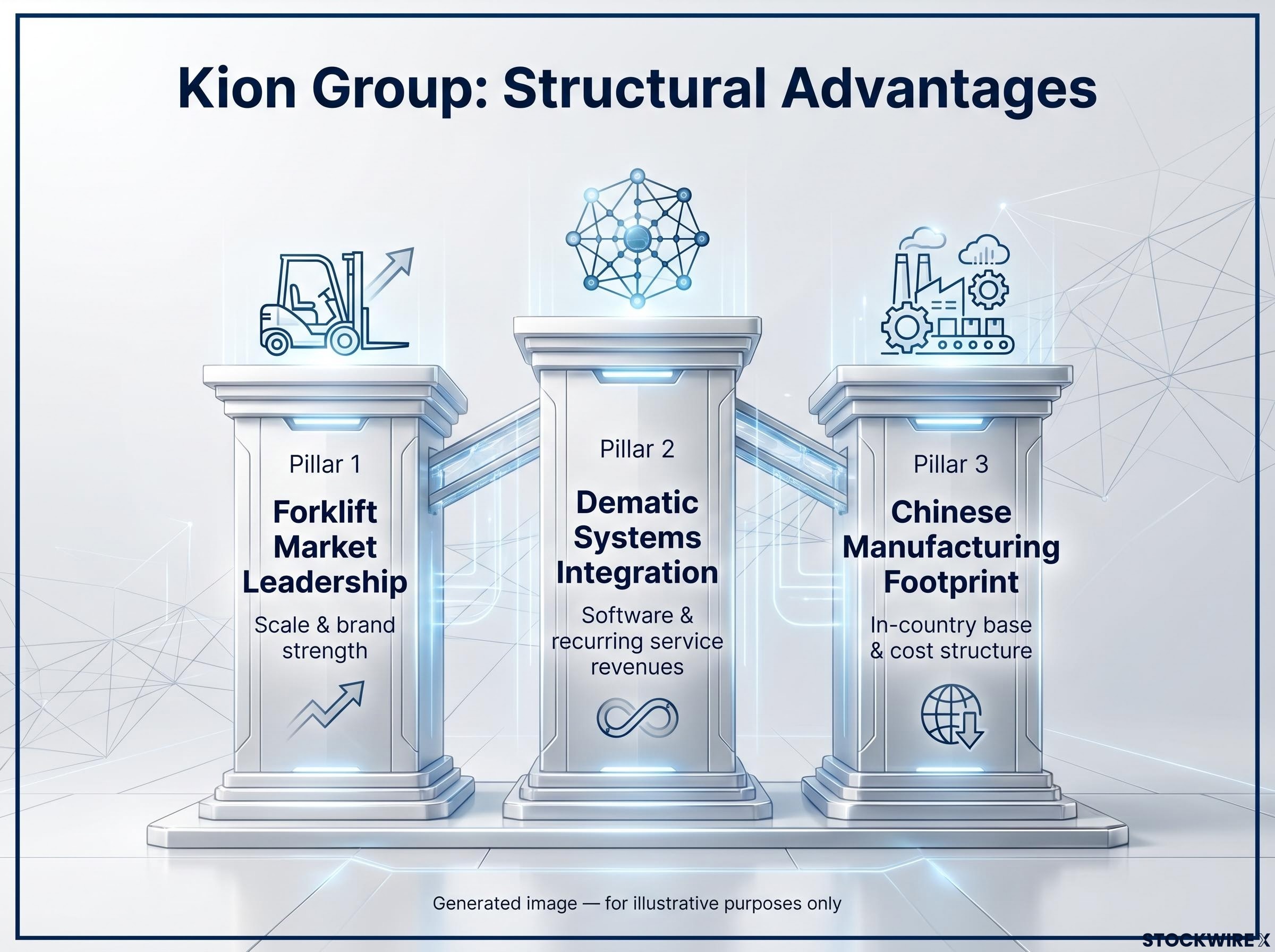

Owning the warehouse automation sector and owning Kion Group specifically are not the same trade. Barclays selected Kion as its top pick for structural reasons that go beyond the sector-level contrarian call.

Kion stands out from peers on three dimensions:

What this means for you as an investor is that buying Kion gives you exposure to both the equipment cycle and the faster-growing automation software and services layer. That is a materially different risk and return profile than owning a pure-play equipment manufacturer. The equipment cycle is volatile; the software and services layer is stickier and higher-margin.

For investors approaching industrial sector investing through ETFs or thematic vehicles rather than individual stock selection, the automation, reshoring, and energy transition tailwinds that support the Kion thesis operate across the broader sector, not just in warehouse automation, and the risk profile varies significantly by sub-industry.

As of 3 July 2026, Barclays held its overweight rating on Kion, judging that the company’s structural strengths keep potential margin deterioration within bounds that the business can absorb, even if pressure from Chinese forklift producers continues to build.

A normalised price-to-earnings (P/E) ratio of approximately 13-14 (Morningstar, unverified) tells you the market is pricing Kion as a company in earnings recovery, not as a structural compounder. A P/E ratio measures how much investors pay for each dollar of a company’s earnings; a lower number generally implies lower expectations baked into the price.

If earnings normalise toward historical levels, a re-rating from recovery-level multiples toward something closer to fair value for a market leader with a systems-integration business could drive material share price appreciation, independent of any change in market sentiment toward the broader sector.

Barclays’ downward revision from €70 to €68 reflects conservative earnings assumptions rather than deteriorating conviction. The bank is telling you it expects less near-term earnings power but still sees a stock trading well below its estimate of intrinsic value.

The Barclays thesis is not a guaranteed outcome. It is a conditional view, and the conditions it requires can be monitored. Four specific risk categories could break the argument:

Chinese robotics manufacturing dominance extends well beyond forklift pricing: Chinese manufacturers controlled an estimated 93% of the global permanent magnet market as of mid-2026, a supply-chain position that shapes hardware costs and competitive dynamics for any Western automation business operating in adjacent categories.

The thesis requires macro stabilisation, not recovery. That is the most important distinction for any investor considering this position: the bar is lower than a full cyclical upturn, but it is not zero.

Each of these risks is a specific signal to watch. If European industrial orders weaken further, or if a major Chinese competitor launches a pricing offensive, the timeline extends and the entry point may no longer look as attractive.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

As of 3 July 2026, Kion Group trades at approximately €43.51. Barclays sees €68. The consensus sees approximately €58-59. Even the more conservative view implies roughly 40-50% upside.

The investor profile this thesis is designed for is specific: medium- to long-term horizon, comfortable with cyclical and competitive risk, looking for automation exposure after a valuation reset rather than at peak multiples. If that describes your situation, the risk-reward mathematics are difficult to ignore.

What would need to change for the thesis to deteriorate? European industrial activity would need to weaken further rather than stabilise. Chinese competition would need to accelerate rather than hold at current intensity. Kion’s earnings would need to disappoint again beyond the already-trimmed estimates. Those are the three signals to monitor.

Whether the Barclays thesis works for you depends less on whether you agree with the €68 price target and more on whether you are willing to hold through additional near-term volatility to reach a medium-term normalisation. The structural demand for warehouse automation has not gone away. The question is whether the current price adequately compensates you for the cyclical risk you are taking on while you wait.

Investors wanting to compare Kion’s structural position against a different model of European industrial exposure will find our deep-dive into Investment Latour instructive, which examines how a niche industrial rollup strategy using pricing power and non-cyclical demand can insulate proprietary subsidiaries from the same macro pressures weighing on listed peers.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Warehouse automation stocks are shares in companies that manufacture and integrate equipment and software systems for logistics and distribution centres. They have fallen due to three overlapping pressures: weaker European industrial demand cutting capital expenditure budgets, cost inflation squeezing margins, and aggressive pricing from Chinese forklift manufacturers raising fears of structural margin erosion.

Barclays trimmed its Kion price target from €70 to €68 to reflect scaled-back near-term earnings assumptions, not a change in directional conviction. The bank still sees the stock trading well below its estimate of intrinsic value and views the post-selloff entry point as attractive for medium- to long-term investors.

Kion combines forklift market leadership with its Dematic subsidiary, which provides full-stack warehouse automation spanning hardware, software, and integration services, generating stickier customer relationships and recurring service revenues. Kion also has an in-country manufacturing footprint in China, giving it a cost structure that pure European producers cannot easily replicate.

The thesis requires European industrial activity to stabilise rather than deteriorate further, Chinese competitive pressure to remain at current intensity rather than accelerate, and Kion's earnings to meet the already-trimmed projections Barclays has built into its revised €68 target. It does not require a full macro recovery, only that conditions stop getting worse.

Analyst consensus targets sit at approximately €58-59, implying roughly 40-50% upside from the current share price of around €43.51, while Barclays' target of €68 implies approximately 56% upside. Even the more conservative consensus view points to material upside from current levels, meaning the direction of the trade is broadly shared across the analyst community.