Global X Releases 26 ASX ETF Distribution Estimates Ahead of 3 July

7 hrs ago

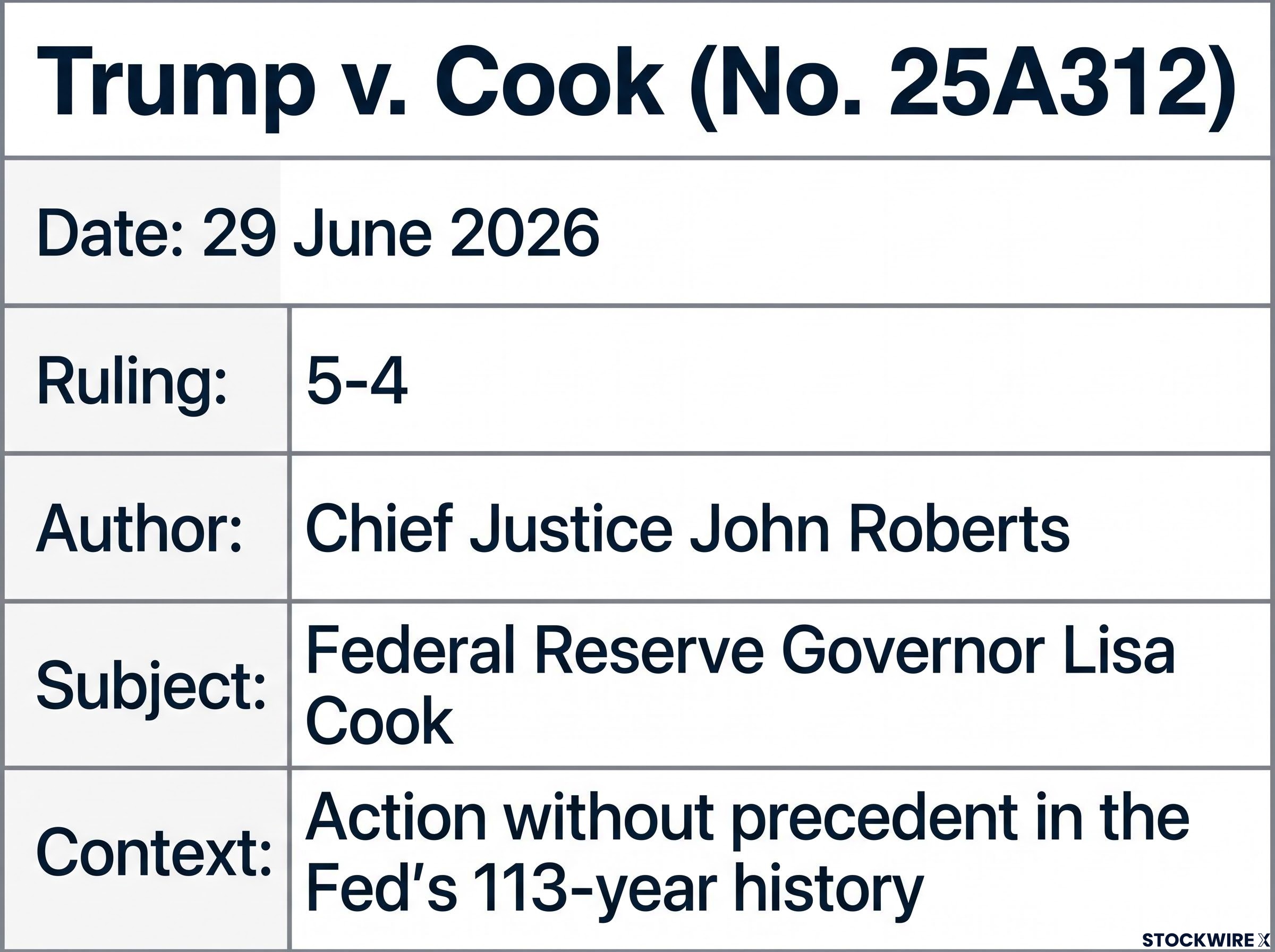

On 29 June 2026, the Supreme Court blocked President Trump from removing Federal Reserve Governor Lisa Cook, ending an action without precedent in the Fed’s 113-year history. The 5-4 ruling drew a sharp legal line around one of America’s most consequential institutions at the precise moment the reader might have expected the opposite.

No president had ever attempted to fire a sitting Fed governor before. The ruling, authored by Chief Justice John Roberts, arrived while the same Court was simultaneously expanding presidential removal power over other independent agencies, making the Fed’s protected status all the more striking. This was an interim decision on emergency relief, not a final merits ruling, but its immediate institutional force is real.

Here is what the Court actually decided, what procedural and substantive protections now exist for Fed governors, why the distinction between this ruling and the broader erosion of agency independence matters, and what it means for anyone tracking monetary policy or long-duration asset markets.

The ruling in Trump v. Cook (No. 25A312) was procedurally narrow but institutionally significant. President Trump asked the Court to suspend a district court injunction that was preventing Cook’s removal while her lawsuit proceeded. The Court denied that emergency stay application, 5-4, meaning the injunction stands and Cook remains in her position.

Chief Justice Roberts was explicit about the ruling’s scope:

“Today’s interim ruling does not decide whether the President may lawfully remove Governor Cook for cause. The ultimate decision will largely depend on the facts regarding the Governor’s actions. And those facts have yet to be determined.”

Three things follow immediately from the denial:

The interim nature of the ruling is not a qualification that softens its impact. It is the precise legal vehicle through which Cook stays in office and the removal question goes back for full factual litigation. For anyone assessing how durable this protection is, that distinction matters: the ruling is not a symbolic gesture, but it is not a permanent seal either. It is a live legal process with procedural teeth.

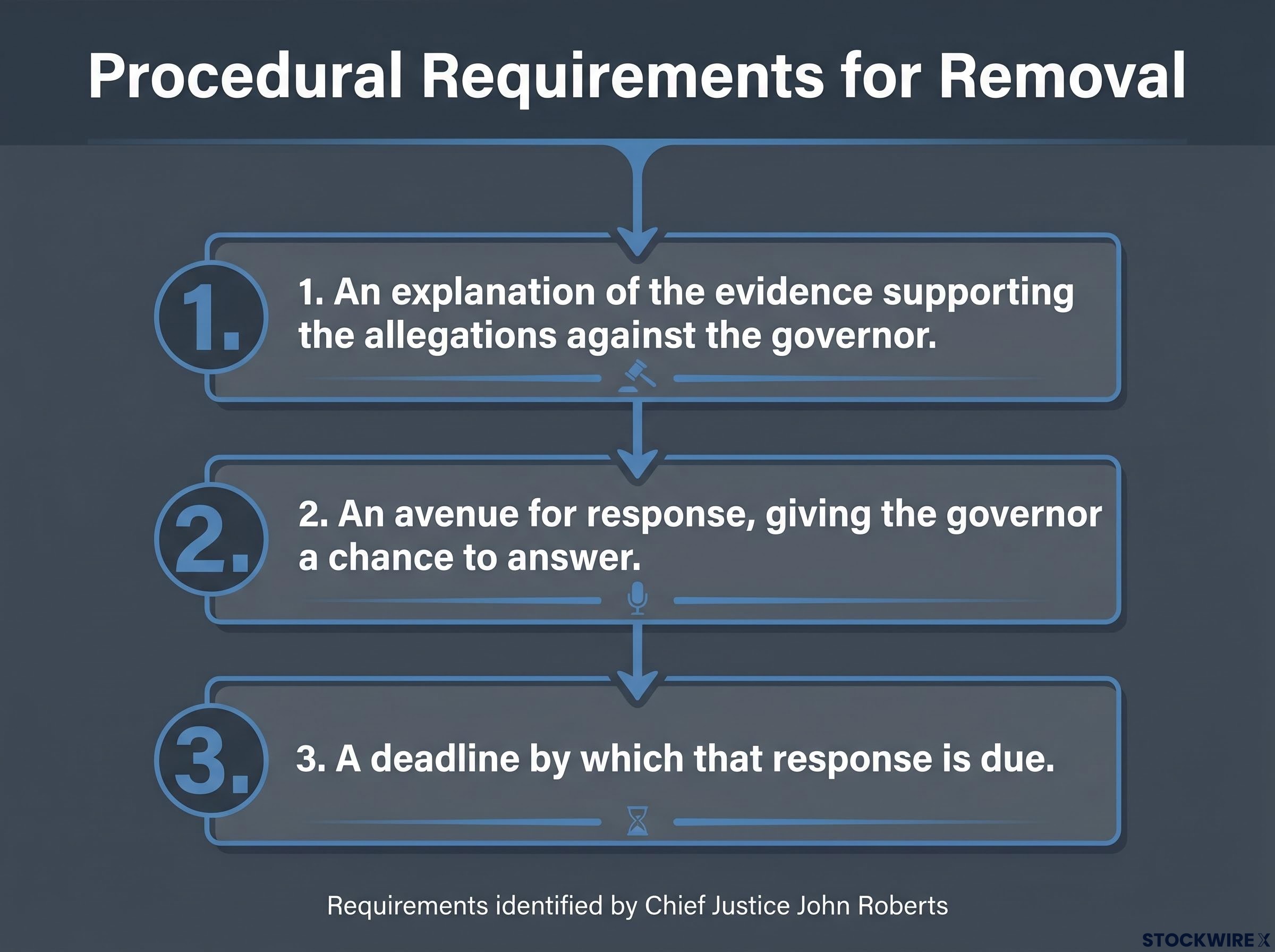

The Federal Reserve Act protects governors from removal except “for cause,” a phrase the statute never fully defined. The Court held that this protection implies concrete procedural safeguards, safeguards Cook did not receive before her termination.

Chief Justice Roberts identified three procedural requirements a president must satisfy before removing a Fed governor:

Because none of these steps were followed, the Court concluded Cook’s removal was “erroneous and void.” The majority treated her position as a protected property interest under the Federal Reserve Act, meaning she could not be deprived of it without due process.

What matters here is specificity. A president cannot fire a Fed governor in a weekend phone call over a policy dispute. The law now has explicit procedural teeth: documented allegations, a formal opportunity to respond, and a defined timeline. Each step is checkable. Each step, if skipped, gives a court grounds to block the removal.

On the substance of what constitutes “cause,” the Court did not issue a detailed test, but it narrowed the concept in important ways. The Court held that cause requires what Roberts described as a “substantial threshold,” rooted in the gravity of the alleged misconduct and whether it bears a genuine connection to the governor’s official responsibilities.

The Court rejected the argument that judges have no role in assessing whether cause actually exists. Trump’s stated basis for removing Cook, alleged mortgage fraud, was widely interpreted by analysts as a mechanism for reshaping the Federal Open Market Committee’s (FOMC) policy composition rather than a genuine governance action.

The full definition of “cause” will be shaped by factual litigation still ahead in the lower courts. But the directional signal is clear: policy disagreement alone does not meet the threshold.

The ruling reinforced a layer of protection that sits within a broader institutional architecture deliberately designed to insulate monetary policy from political pressure. Understanding that architecture explains why removing even one governor carries consequences beyond the individual.

The FOMC, the body that sets US interest rates, consists of 12 voting members. Seven are Board of Governors members appointed by the president and confirmed by the Senate. The remaining five are rotating regional Federal Reserve Bank presidents drawn from institutions with a degree of private-sector governance.

| Member type | Number of voting members |

|---|---|

| Board of Governors | 7 |

| Rotating regional bank presidents | 5 |

| Total | 12 |

The Fed chair holds one vote out of 12. A chair cannot dictate policy alone; any majority can override preferred positions. The Fed also operates outside the congressional appropriations process, insulating its budget from direct political leverage.

The suspected logic behind Cook’s removal was about reshaping the FOMC’s composition: push out governors resistant to rate cuts, seat replacements more receptive to them, and gradually assemble a policy majority favourable to the administration’s preferences. By requiring documented cause, formal evidence, and full due process for every removal, the ruling raises the cost and complexity of executing that approach, making it far more difficult to move swiftly against sitting governors.

The suspected logic behind Cook’s removal was directly tied to FOMC composition: the administration’s goal was to replace governors resistant to rate cuts with members more aligned with its preferences, a strategy that the 8-4 voting split in prior meetings had made appear both feasible and consequential.

“The decision affirms the Fed’s obligation to make policy decisions independently, free from political interference.” — Lisa Cook, public statement following the ruling

While protecting the Fed, the same Court was at that time broadening the president’s authority to dismiss leaders of other independent agencies. In a separate contemporaneous ruling, the Court made it easier for the president to fire leaders at agencies including the Federal Trade Commission (FTC), overturning a 1935 precedent that had protected independent agency heads for nearly a century.

That contrast is the analytical crux of the Cook decision. Multiple outlets accurately describe it as a “Federal Reserve exception” to the Court’s broader trend. The Fed gets statutory and structural protection that other independent agencies are now losing.

The Fed’s protection rests on enforcement of the Federal Reserve Act’s specific for-cause and procedural requirements. It is not a new constitutional doctrine that applies to all independent agencies. Framing the ruling as “a firm constitutional line” would overstate its scope. The protection is real but bounded by the statute.

What the ruling does and does not establish:

For anyone tracking regulatory agencies beyond the Fed, this ruling should not be extrapolated. The FTC, the Consumer Financial Protection Bureau, and other independent bodies now operate under a different and weaker set of removal protections than they did before. The Fed is the exception, not the new rule.

The Cook ruling sits within a broader 2026 pattern of judicial constraints on executive authority in courts, with separate rulings in the same period dismantling the statutory basis for unilateral tariff powers, a signal that judicial review of executive overreach is operating across multiple policy domains simultaneously.

The legal and institutional layers of this ruling connect directly to how long-duration assets are priced. Investors price Treasury yields, inflation expectations, and the dollar on the assumption that US monetary policy is set by an independent, politically insulated institution. That assumption is a foundational input to long-horizon financial models, not a background detail.

The central bank independence research published by the Peterson Institute for International Economics documents how erosion of monetary policy credibility raises inflation risk premiums and pushes long-term rates higher, the precise transmission channel that connects courtroom outcomes to Treasury yield pricing.

If presidents could remove Fed governors over rate policy disagreements without documented cause or process, the perceived stability of the monetary policy regime would weaken. The practical consequences would flow through three channels:

Because removal now requires serious, proven, duty-related misconduct and proper process, governors have reduced personal incentives to align votes with presidential preferences rather than economic judgement. That is not a finding from the Court’s opinion; it is a standard inference from the central-bank-independence literature. But it is the inference that connects the courtroom to your portfolio.

“The decision affirms the Fed’s obligation to make policy decisions independently, free from political interference.” — Lisa Cook

Concerns about Fed independence had been building for several months before the ruling. Reuters and NBC both reported that the decision “stood firm to preserve the central bank’s cherished independence” and “imposes a new barrier” to politicising the Fed. The ruling did not resolve every legal question about the Fed’s future, but it reinforced the institutional architecture that allows long-duration asset pricing to proceed on the assumption that monetary policy responds to economic conditions rather than political pressure.

Fed independence had been under documented pressure for months before the ruling, with Trump’s campaign against Powell establishing a concrete baseline of political interference that shaped market expectations heading into the Cook litigation.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The ruling’s immediate effect is that Lisa Cook remains in office while her legal challenge proceeds on the merits in the lower courts. The injunction blocking her removal is in force. The question of whether Trump can ultimately remove her “for cause” depends on factual findings about the alleged misconduct, findings that have not yet been made.

As Chief Justice Roberts wrote, the outcome “will largely depend on the facts regarding the Governor’s actions.” Three forward-looking events will shape what happens next:

Kevin Warsh’s confirmation as Fed Chair on 13 May 2026 by a 54-45 Senate vote means the institution Cook now remains part of is simultaneously navigating a new leadership transition, a $6.7 trillion balance sheet reduction pledge, and headline inflation still running above the 2% target.

This is a moment of institutional clarity, not finality. The Court established procedural requirements and a substantive threshold for the first time in the Fed’s history. The legal architecture around Federal Reserve independence is clearer than it was a week ago. But the full picture is still developing, and the next chapter depends on whether the facts of Cook’s case meet the bar the Court has now set. For anyone tracking monetary policy, this story is not over. It has a framework now, and a set of events worth watching.

These forward-looking statements are subject to change based on legal proceedings and future court decisions.

Federal Reserve independence means the Fed sets monetary policy based on economic data rather than political instruction. Markets price Treasury yields, inflation expectations, and the dollar on the assumption that this independence holds, so any erosion raises inflation risk premiums and pushes long-term rates higher.

The Court denied the Trump administration's emergency request to suspend a lower court injunction, meaning Lisa Cook stays in office while her legal challenge proceeds. The 5-4 ruling, authored by Chief Justice John Roberts, was an interim decision, not a final merits ruling, but it carries immediate institutional force by blocking her removal.

Chief Justice Roberts identified three requirements: the president must provide an explanation of the evidence supporting the allegations, give the governor a formal avenue to respond, and set a deadline for that response. Skipping any of these steps gives a court grounds to void the removal, as happened with Cook's termination.

No. The protection applies specifically to Fed governors under the Federal Reserve Act's for-cause removal standard. The same Court simultaneously expanded presidential power to dismiss leaders at other independent agencies, including the FTC, making the Fed a deliberate exception rather than a new general rule.

Cook's challenge returns to the lower courts for full factual litigation on whether the alleged misconduct meets the substantial threshold Roberts described. The outcome depends on findings about her specific actions, which have not yet been determined, and either side can pursue appellate review of whatever the lower court decides.