ASX 200’s Calm June Hides a 22-Point Sector Divide

56 mins ago

High-quality Australian bonds, the kind issued by major banks and large corporates, are now generating portfolio income of 6-7%. That is a number most conservative investors associate with equities or high-yield debt, not investment grade credit.

This is not a single-issuer anomaly or a hidden risk premium. It reflects a structural reset in Australian risk-free rates combined with credit spreads that, while tight, remain within a historically sane range. For context, comparable bonds barely cleared 3% for most of the decade between the Global Financial Crisis and COVID-19. The gap between then and now is not a market quirk; it is a regime change.

Here is what the current configuration actually means for Australian investors weighing a fixed income allocation, whether you are an SMSF trustee reassessing your defensive holdings or a retiree trying to determine if these yields are a genuine income opportunity or a spread-compression trap waiting to snap.

The income figure surprises people. 6-7% from investment grade credit sounds like it must involve meaningful credit risk. It does not, and the composition of the yield explains why.

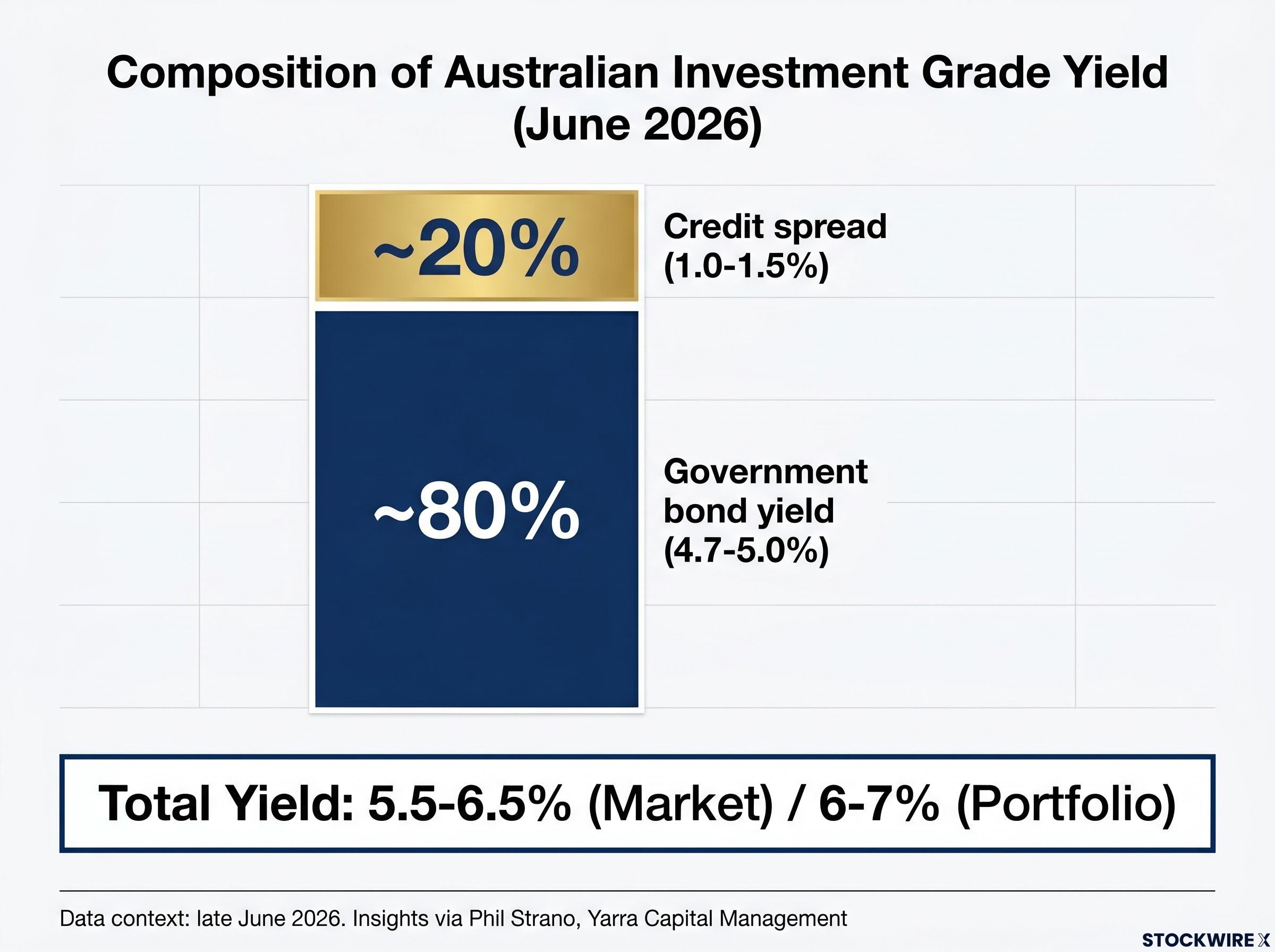

Australian 10-year government bond yields sit at approximately 4.7-5.0% as of late June 2026, according to RBA statistical tables and corroborated by Bloomberg and Trading Economics. That is the risk-free base rate, the foundation on which every investment grade yield is built. When you add the credit spread, the premium investors receive for lending to a corporation instead of the government, total yields on BBB-rated Australian corporates reach 5.5-6.5% depending on tenor and issuer.

The income figure becomes clearer once you work through bond yield mechanics: the coupon payment is fixed at issuance, so a lower purchase price automatically produces a higher yield, and the government bond rate sets the floor on which every corporate spread is then layered.

The critical detail is the ratio between those two components.

Phil Strano, Head of Australian Credit Research at Yarra Capital Management, estimates portfolio-level income from high-quality Australian investment grade credit at 6-7%, noting that credit spreads for BBB-rated corporates currently represent approximately 20% of total outright yield.

That 20% figure is worth pausing on. It means roughly 80% of the income you earn from an investment grade bond portfolio is coming from the government yield component, not from credit risk.

| Yield Component | Approximate Level | Share of Total Yield |

|---|---|---|

| Government bond yield (risk-free rate) | 4.7-5.0% | ~80% |

| Credit spread (risk premium) | 1.0-1.5% | ~20% |

| Total investment grade yield | 5.5-6.5% (market); 6-7% (portfolio) | 100% |

When you are earning most of your income from rate exposure rather than credit risk, the primary risk you are running is rate volatility, not default. That distinction changes how you should think about portfolio construction, and it reframes the tight-spread debate entirely.

The 20% spread-to-yield ratio is not a comfortable number. According to Phil Strano of Yarra Capital Management, this is a level not seen since 2007, the year before the Global Financial Crisis. For investors who remember that period, the comparison lands hard.

It should. Pricing is not generous. Spreads are compressed relative to long-term averages, and there is limited room for further tightening to generate capital gains. Anyone expecting to profit from additional spread compression at these levels is likely to be disappointed.

The 2007 parallel carries genuine weight, but it only tells part of the story. Today’s structural backdrop differs from the pre-GFC era in several respects that bear directly on how much weight to place on the spread comparison.

These are not minor footnotes. They represent a structurally more challenging macro backdrop than the one that preceded the GFC, which is precisely why treating the spread comparison as a prediction rather than a reference point overstates the parallel.

One feature of the current environment that has no pre-GFC equivalent is the scale of AI-related capital expenditure. Heavy investment in data centres, power infrastructure, and semiconductors is sustaining corporate earnings and demand across multiple sectors. This is providing a legitimate support mechanism for tight spreads, one grounded in real capital deployment rather than the speculative leverage and underwriting deterioration that characterised 2006-2007.

The distinction matters. Spreads can be tight without a credit bubble when the earnings backdrop genuinely supports the pricing. The risk, however, is that this AI-driven cycle is not guaranteed to persist. Any meaningful deterioration in the growth backdrop, whether from a slowdown in AI capital expenditure or a broader macro shock, would likely trigger spread widening from levels that offer limited cushion.

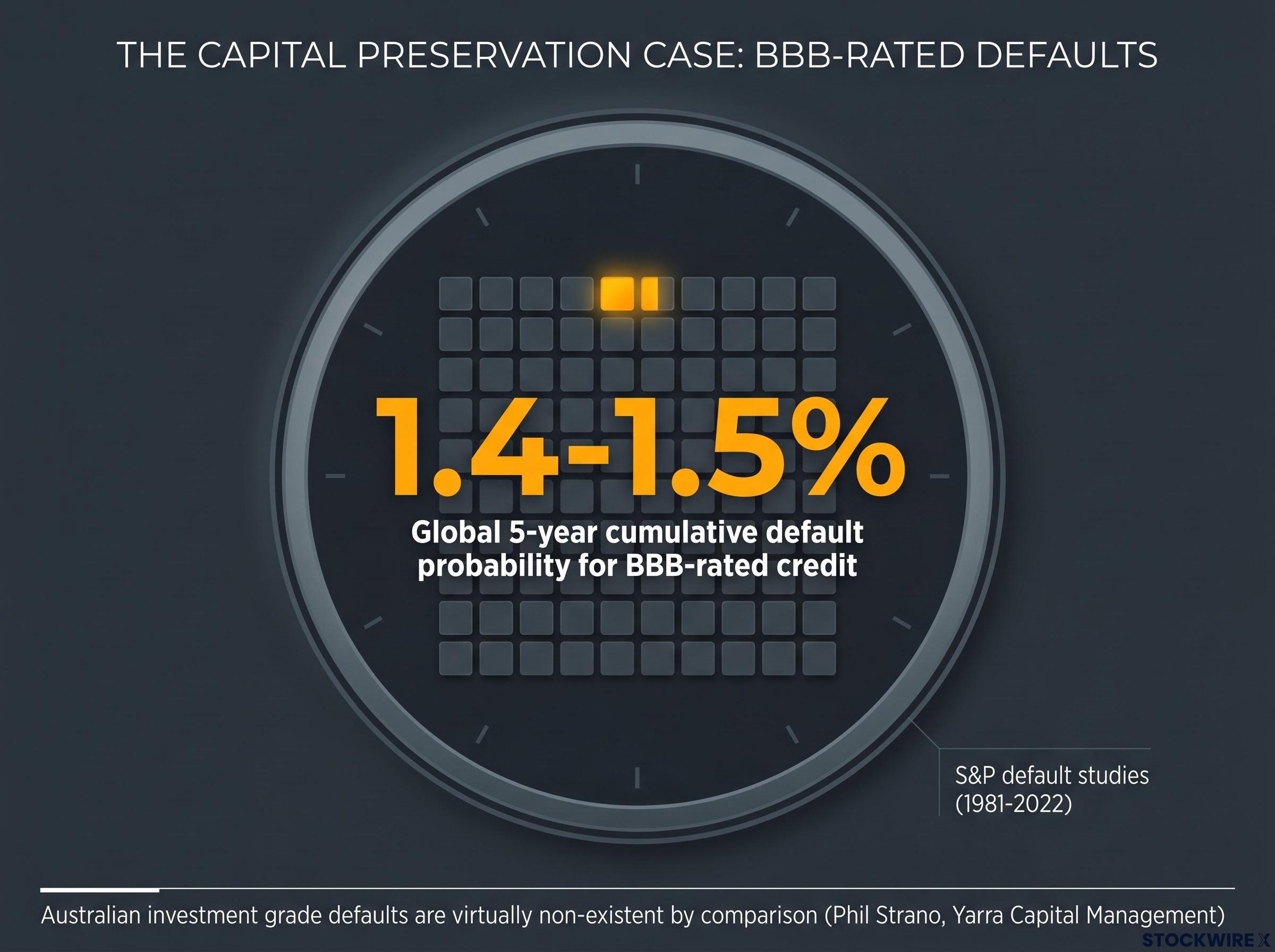

The tight-spread conversation, for all its analytical importance, can obscure the most powerful argument for investment grade credit: the asset class almost never loses your capital permanently.

S&P default studies covering 1981-2022 and subsequent updates place the BBB-rated five-year cumulative default probability at approximately 1.4-1.5% globally. A cumulative default probability measures the percentage of issuers within a given credit rating that default over a specified period, in this case five years.

BBB-rated 5-year cumulative default probability: approximately 1.4-1.5% globally (S&P default studies, 1981-2022 and subsequent updates).

The Australian experience is likely even lower than this global figure. Australian investment grade issuance is heavily concentrated in major banks and large infrastructure entities, sectors with structural earnings stability and regulatory oversight. Phil Strano of Yarra Capital Management characterises investment grade defaults in Australia as virtually non-existent by comparison to high yield.

The distinction between investment grade and high yield on this dimension is stark:

For an SMSF member or retiree, the near-zero default record is not a dry statistic. It is the reason you can treat investment grade credit as a defensive income engine rather than a risk asset that might not return your capital. Spreads matter for short-term mark-to-market performance, but the absence of defaults is what allows income to compound and capital to be preserved across a full cycle.

If you managed a conservative or balanced portfolio through the 2010s, your relationship with bonds is probably damaged. For the better part of a decade, high-quality Australian bonds yielded below 3%. That was not enough to meet income targets for retirees, not enough to justify the allocation cost for SMSF trustees, and not enough to compete with the dividend yields available from listed equities or property trusts.

The result was predictable. Conservative portfolios reached into equities, listed property, and hybrid securities to generate the income that bonds could no longer provide. That worked, until it did not, and it introduced risk profiles that many income-focused investors were not well positioned to absorb.

The structural reset in base rates has changed this equation materially:

A 6-7% income yield from defensive assets changes the portfolio construction calculus. You face less pressure to reach into equities, listed property trusts, or hybrid securities for cash flow. For SMSF members drawing regular income, this means the portfolio can meet spending requirements from a lower-risk allocation, reducing overall portfolio volatility for a given income target.

Re-engaging with investment grade credit now is not a defensive retreat. It is an active income decision supported by the data, and for income-oriented, capital-preserving investors, this represents one of the more attractive entry points in the past 15-20 years.

The Australian bond market has undergone a structural reclassification over this period, growing three to four times in size since 2021 and now ranking alongside the Canadian dollar and sterling markets globally, a development that has deepened secondary liquidity and increased the range of investment grade issuers available to domestic investors.

The income case is strong. That makes it even more important to name the risks clearly, because the moment you treat any asset class as risk-free, you have already made a positioning error.

Duration risk in practice was on display during the May 2026 ASX sell-off, when the US 30-year Treasury yield reaching a post-GFC high of 5.20% wiped approximately 151 points from the ASX 200 in a single session, demonstrating how directly Australian portfolio valuations now transmit global rate moves.

Tight spreads combined with elevated macro headwinds define the central tension of the current environment. The income is genuine; the margin for error on the capital appreciation side is not.

These risks are not reasons to avoid Australian investment grade credit. They are reasons to focus on income and capital preservation over the full investment horizon rather than positioning for capital gain from further spread compression, which is unlikely to materialise at scale.

The practical question is not whether to own investment grade credit, but how to own it well. In a tight-spread environment, the quality and diversification of your exposure matter more than they do when spreads are wide and the margin for error is larger.

Portfolio construction should prioritise:

This allocation suits a specific investor profile:

What it does not solve: growth, inflation protection beyond the income yield itself, or liquidity at very short horizons. Investment grade credit is an income and capital preservation tool, not a total-return substitute for equities.

For investors wanting to see how duration differences play out across specific Australian bond ETFs, our dedicated guide to Australian bond ETF duration risk examines how effective duration separated fund returns by as much as 3.6 percentage points on a single trading day in February 2026.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Australian investment grade credit is offering yields not seen in over a decade, driven by a structural reset in base rates rather than by excessive credit risk-taking. The near-zero historical default rate underpins the capital preservation case. Most of the income is coming from rate exposure, not from credit risk premia.

The tension is real: spreads are tight, the macro backdrop carries structural headwinds, and further capital appreciation from spread compression is unlikely. These are not reasons to avoid the asset class; they are reasons to own it for the right purpose.

For SMSF trustees, retirees, and conservative investors, this is primarily an income decision. On that basis, the current configuration is as compelling as the Australian investment grade market has been in 15-20 years. The opportunity is in the income, not the trade.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

Australian investment grade bonds are debt securities rated BBB or higher, issued primarily by major banks, large corporates, and infrastructure entities. The Australian investment grade market has grown three to four times in size since 2021 and now ranks alongside the Canadian dollar and sterling markets globally.

Yields of 6-7% are being driven primarily by a structural reset in the risk-free rate, with Australian 10-year government bond yields sitting at approximately 4.7-5.0% as of late June 2026. Credit spreads add a further 1.0-1.5%, meaning around 80% of the total yield comes from government rate exposure rather than credit risk.

S&P default studies covering 1981-2022 place the BBB-rated five-year cumulative default probability at approximately 1.4-1.5% globally, and the Australian experience is likely lower given the heavy concentration in major banks and large infrastructure entities with structural earnings stability.

The key risks are spread widening if growth slows or the AI capital expenditure cycle fades, duration risk from rate volatility given higher base rates, and broader macro shocks from geopolitical disruption or fiscal deterioration. Credit spreads are at their tightest level relative to total yield since 2007, leaving limited cushion for capital gain from further spread compression.

The article recommends prioritising quality issuers such as major Australian bank Tier 2 instruments and solid BBB-rated corporates, using diversified fund structures rather than concentrated single-name exposure, and aligning duration to your spending horizon and liquidity needs. This allocation suits investors with a medium-term horizon of at least two to three years who prioritise income and capital preservation over total-return growth.