How to Choose Between VAS and A200 for Your Portfolio

1 hr ago

You want your portfolio to pay you now. You also know that a portfolio built entirely around today’s highest-yielding ETFs can quietly erode the capital that was supposed to fund the next thirty years. That tension is not a sign you are doing something wrong. It is the single most important design question a dividend-focused investor has to answer.

The good news: you do not have to choose one objective over the other. The core and satellite portfolio strategy exists precisely to hold both, current income and long-term income growth, inside a single structure that does not need to be rebuilt every time market conditions shift. Institutional investors and professional wealth managers have used this framework for decades, which tells you it is tested across real market cycles, not just modelled in theory.

Here is a clear framework for deciding which ETFs belong at the centre of your portfolio, which ones belong at the edges, and how to calibrate the balance based on where you actually are in your financial life.

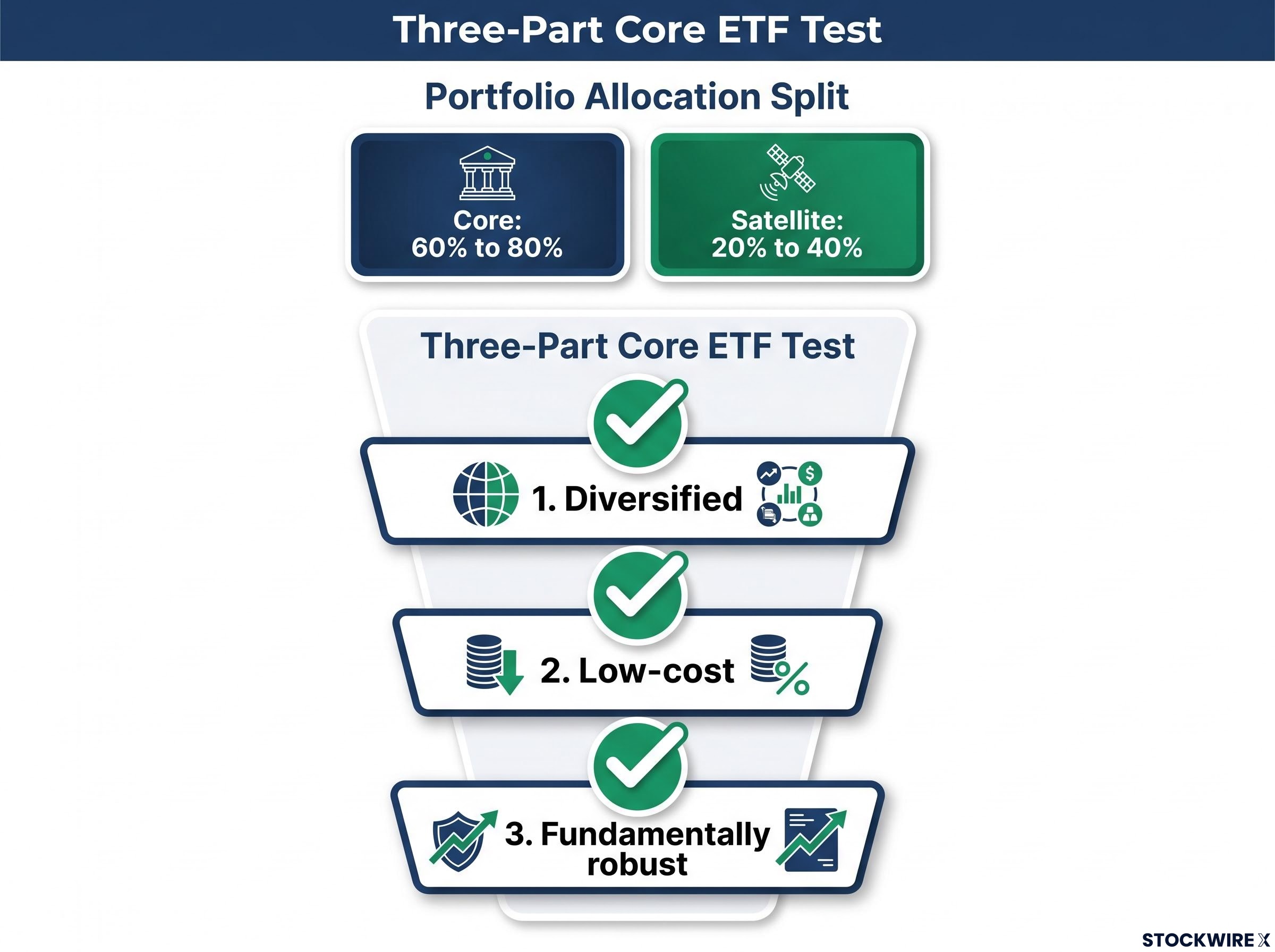

Your core is the majority of your portfolio: broadly diversified, low-cost index funds you intend to hold for decades, across multiple market cycles, with minimal changes. The satellite is everything else, the intentional, supplementary positions that target goals your core does not fully address on its own.

The practical power of this framework comes from a single, testable standard you can apply to any ETF you already own. A holding qualifies as core if it meets all three criteria:

Any ETF that fails even one of those three tests belongs in your satellite sleeve, not at the centre. That filter is something you can apply to every holding in your account right now, not a concept to revisit later.

The recommended core allocation typically sits between 60% and 80% of the total portfolio, a range consistent with how advisor model portfolios and institutional wealth managers are constructed.

The remaining 20% to 40% is your satellite sleeve, allocated based on specific income or growth goals your core does not address. If you need current cash flow, satellites might be higher-yielding income ETFs. If you are pursuing tactical growth exposure, they might be sector-specific or thematic funds.

The satellite sleeve’s purpose is not fixed. It changes as your circumstances evolve, and that flexibility is a feature of the framework, not a weakness.

Run the three-part test against a dividend growth ETF like SCHD (Schwab U.S. Dividend Equity ETF) or DGRO (iShares Core Dividend Growth ETF), and each criterion is met by the fund’s structure.

Diversified? Both hold broad baskets of U.S. companies across multiple sectors. Low-cost? Their expense ratios sit well below the industry average for actively managed income funds. Fundamentally robust? Their index methodologies screen for profitability, dividend sustainability, and consistent payout growth, which creates built-in value and quality factor tilts.

Those quality tilts mean dividend growth ETFs may underperform during speculative rallies driven by unprofitable or non-dividend-paying companies. That underperformance is acceptable within the plan if the holding is meeting its designated role as your decades-long anchor.

The lower current yield is a feature, not a flaw. Dividend income from quality dividend growth ETFs is expected to grow faster than CPI over multi-year periods. That means the income you receive in year ten is materially higher than the income you receive in year one, and the compounding effect on your purchasing power is where the real value sits.

The yield today is the wrong metric. The income trajectory over a decade is the right one. A modest starting yield that grows every year will outpace a high starting yield that stagnates or declines.

SCHD’s Q2 2024 distribution came in roughly 3% below the equivalent payout from the same quarter a year earlier. That is one data point, not a trend. Quarterly variability is normal for dividend growth ETFs because distributions depend on underlying holdings’ payout decisions, index methodology adjustments, and the timing of constituent changes.

The distinction that protects you from reactive decisions is this: quarterly variability within a multi-year upward income trend is normal operation. A multi-year decline in distributions is a genuine concern requiring review. One soft quarter does not tell you the strategy is broken; it tells you the strategy operates in the real world.

A covered call ETF owns a basket of equities and then sells call options against those positions. When you sell a call option, you collect a premium, which is cash income, but you agree to give up gains above a certain price. That premium is what gets distributed to you as income.

This is why covered call ETFs can offer higher current yields than dividend growth ETFs. The income is not coming solely from the underlying companies’ dividends. It includes option premiums, and in some cases, return of capital, meaning a portion of what you receive as a “distribution” may actually be your own invested capital being returned to you, not income generated from business earnings. Understanding that distinction changes how you should interpret a high yield number from these funds.

Now apply the three-part core test. Covered call ETFs fail it. Their income is not reliably growing over time because option premiums fluctuate with market volatility and pricing conditions. Their capital growth is structurally constrained because the sold options cap upside participation. And their distribution variability makes them unsuitable as a foundational, decades-long anchor.

Failing the core test does not make these ETFs bad. It means they serve a specific, legitimate purpose: generating current cash flow for investors who need income now. That purpose belongs in the satellite sleeve.

| Dimension | Dividend growth ETFs | Covered call ETFs |

|---|---|---|

| Current yield | Moderate | Higher |

| Expected income growth | Rising over time, typically above CPI | Limited; tied to option premiums, not earnings growth |

| Price return potential | Full market participation | Capped by options overlay |

| Distribution variability | Moderate; quarterly fluctuations within upward trend | Higher; sensitive to volatility and options pricing |

| Portfolio role | Core: decades-long anchor | Satellite: current income generation |

Consider an investor who left full-time work in their late thirties and now relies entirely on portfolio distributions to cover living expenses. Their allocation places 60% into dividend growth ETFs (SCHD and DGRO) and directs the remaining 40% toward covered call ETFs.

Each sleeve has a distinct, intentional job:

This split sits within the 60-80% core range that institutional and advisor model portfolios use as a structural benchmark, though at the lower end of that range because this investor’s current income needs are unusually high relative to a typical accumulator.

The appropriate core-to-satellite ratio is personal, not universal. It evolves with your life. This investor needs cash flow today at an unusually early retirement age. Your appropriate ratio depends on whether you need income now or are still building wealth for the future.

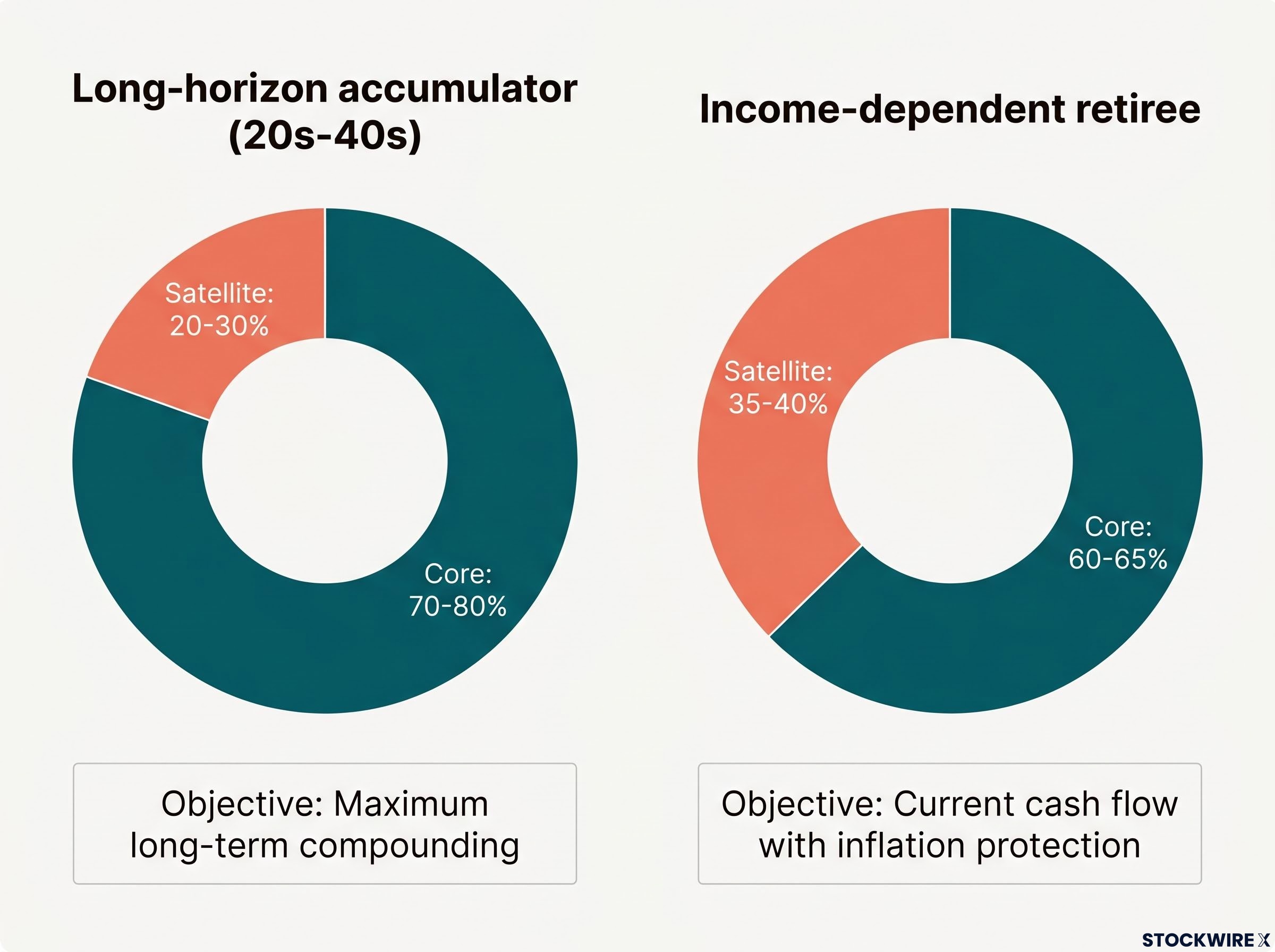

Your income needs and time horizon determine where you start. Two investor profiles illustrate the range.

| Investor stage | Income need | Suggested core % | Suggested satellite % | Primary objective |

|---|---|---|---|---|

| Long-horizon accumulator (20s-40s) | Minimal; reinvesting income | 70-80% | 20-30% | Maximum long-term compounding |

| Income-dependent retiree or early retiree | Significant; funding living expenses | 60-65% | 35-40% | Current cash flow with inflation protection |

These profiles are illustrative, not prescriptive. Most investors will move between profiles over their investing lifetime as income needs, time horizons, and circumstances evolve.

If you are in your thirties with a steady salary and no near-term income dependency, the 70-80% core weighting gives your dividend growth ETFs maximum runway to compound. The satellite sleeve can be small or even tilted toward growth-oriented positions rather than income.

If you are closer to or already in retirement and depend on your portfolio to pay bills, a larger satellite allocation of 35-40% in covered call or high-yield ETFs generates the cash flow you need today, while retaining a meaningful 60-65% core for inflation protection and capital preservation.

Increasing the weighting of low-cost ETFs in your core is generally viewed as favourable. For most long-term investors, there is rarely such a thing as too much in high-quality, low-cost core holdings.

The ratio is not permanent. As your income needs grow or shrink, as your portfolio size changes, as your timeline shifts, you adjust the balance. That adjustment is not a sign something went wrong. It is the framework working as intended.

A high distribution yield is not the same as a high income yield if the excess is a return of your own capital.

The tension this article opened with, wanting income today while protecting the engine that produces income tomorrow, is real. The core-satellite framework resolves it structurally. Your core in dividend growth ETFs compounds wealth and grows income over time. Your satellite in covered call or high-yield ETFs generates the current cash flow your core does not yet provide. Both sleeves work simultaneously, serving different purposes without requiring you to choose one objective over the other.

The one action you can take right now: apply the three-part core test, diversified, low-cost, and fundamentally robust, to every ETF currently in your portfolio. Identify which sleeve each holding actually belongs in. If your satellites are sitting in the core position, you have a clear first adjustment to make.

The appropriate balance will evolve. Revisiting your allocation as income needs, time horizon, and market conditions shift is not a sign the strategy is failing. It is evidence that it is working as designed.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Dividend income, option premium distributions, and return of capital may be taxed differently depending on your jurisdiction and account type. Consult a qualified tax professional regarding your specific situation.

The core and satellite portfolio strategy divides your portfolio into two sleeves: a large core of broadly diversified, low-cost, fundamentally robust ETFs held for decades, and a smaller satellite sleeve of targeted positions that address specific income or growth goals the core does not fully cover on its own.

Most institutional and advisor model portfolios place 60-80% in the core and 20-40% in satellites; long-horizon accumulators in their twenties to forties typically weight the core at 70-80%, while income-dependent retirees may run a 60-65% core to generate more current cash flow from a larger satellite allocation.

Covered call ETFs fail the three-part core test because their income does not reliably grow over time, their capital appreciation is structurally capped by the options overlay, and their distributions vary with market volatility; they belong in the satellite sleeve as a current income tool, not a decades-long anchor.

SCHD and DGRO meet all three core criteria: they hold broad baskets of U.S. companies across multiple sectors, carry expense ratios well below the industry average for actively managed income funds, and use index methodologies that screen for profitability, dividend sustainability, and consistent payout growth.

Return of capital occurs when a portion of an ETF's distribution is actually your own invested capital being handed back to you rather than income generated from business earnings; if an ETF's net asset value is declining while paying distributions, the headline yield overstates the true income being produced.