South32 Shareholders to Receive Alcoa Shares in $5.6B Sale

5 hrs ago

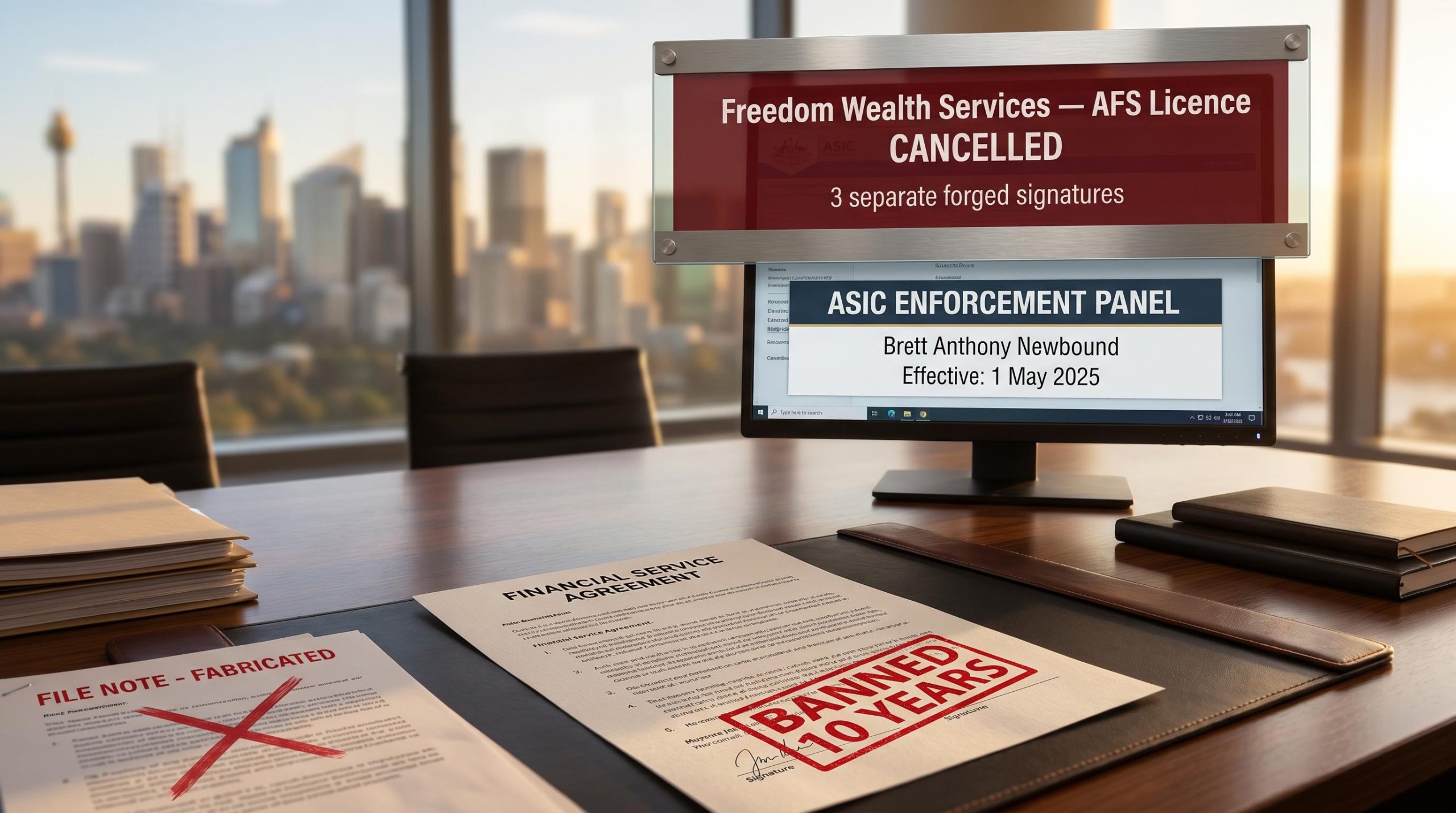

Clients of a Sydney financial planner discovered their signatures on service agreements they had never signed. File notes recorded interactions that never happened. Those fabricated records were then used to justify ongoing fee deductions from their accounts. The planner responsible was Brett Anthony Newbound, sole director of Freedom Wealth Services Pty Ltd.

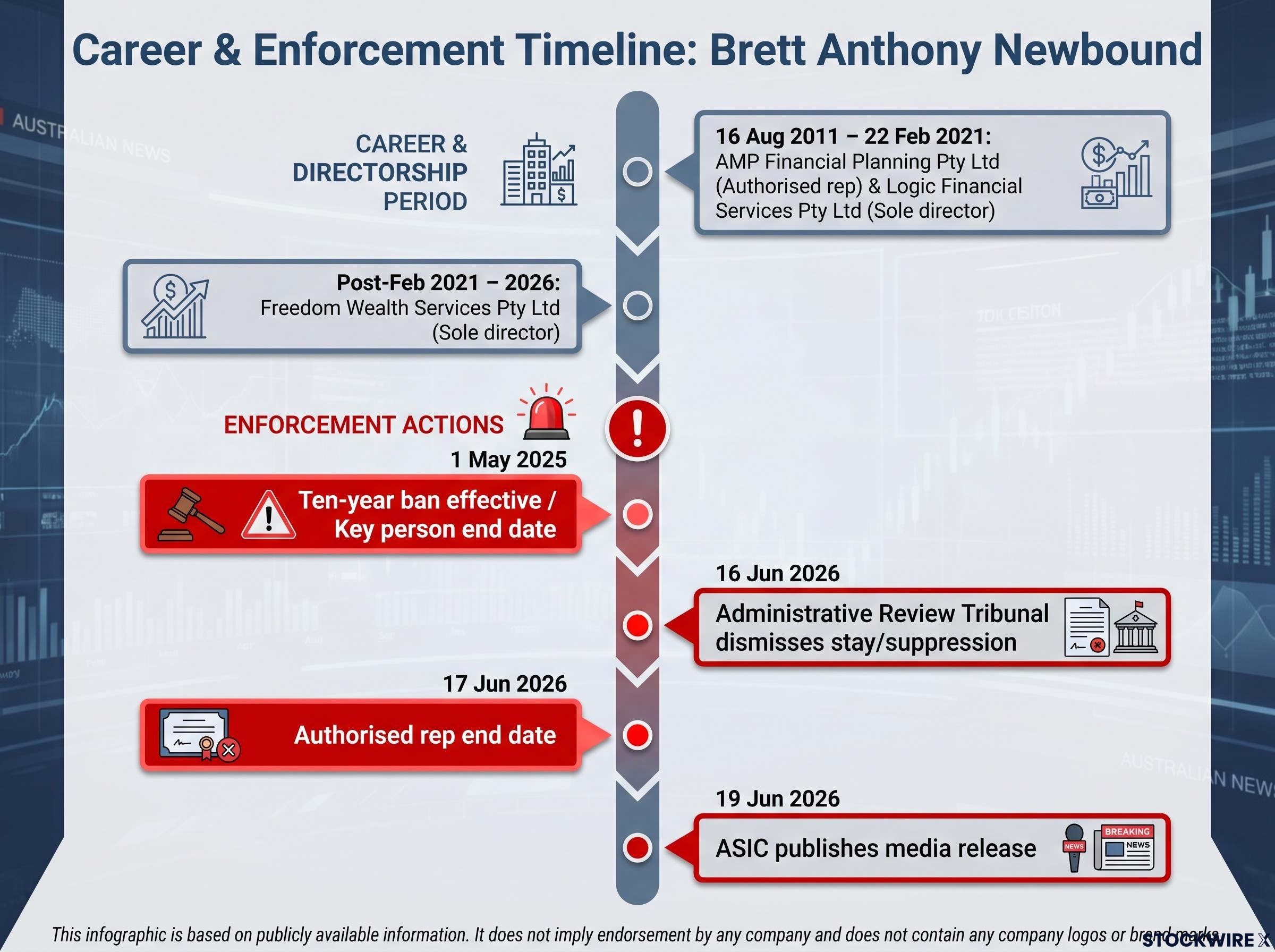

ASIC has now responded. Newbound is banned from the financial services and credit industries for ten years, effective 1 May 2025. Both of Freedom Wealth Services’ licences, its Australian Financial Services (AFS) licence and its Australian Credit Licence (ACL), have been cancelled. An attempt by Newbound and the firm to suppress public reporting of the matter was dismissed by the Administrative Review Tribunal on 16 June 2026, three days before ASIC published its media release.

This case lays out how document fraud works inside licensed financial advice, what the regulator does when it finds it, and, most importantly, how you can check whether your own adviser’s records and fees are legitimate.

ASIC’s findings identify two distinct categories of misconduct, and the specificity of each tells you this was not a single lapse in judgment.

The first involved forged client signatures. Across three separate instances, client signatures appearing on Freedom Wealth Services service agreements were not genuinely provided by those clients. The signatures had been improperly obtained or fabricated outright.

The second involved fabricated file notes. Newbound produced, or directed the production of, file notes whose contents bore no accurate relation to what had actually occurred in client interactions. Those false records were then used to support and justify the charging of ongoing service fees.

The two misconduct categories, side by side:

Both categories involve the deliberate falsification of documents that clients would reasonably rely on as proof that services were requested, agreed to, and delivered. The false file notes tied to fee deductions carry a direct financial consequence: clients may have been charged for services that were never provided, with no genuine record of interaction to show for it.

Before you can understand why the penalty is as severe as it is, you need to understand the test ASIC applied. The “fit and proper person” assessment is the statutory threshold that determines whether someone is legally permitted to provide financial advice or engage in credit activities. It sits under two pieces of legislation: the Corporations Act 2001 and the National Consumer Credit Protection Act 2009. The test evaluates honesty, integrity, competence, and compliance history.

The fit and proper person test sits alongside ASIC banning powers that operate entirely outside the courts, allowing the regulator to remove a person’s legal authority to operate across financial services and credit activities through an administrative process governed by the Corporations Act 2001.

Deliberate document falsification goes to the core of this threshold. This is not an administrative error or a record-keeping failure. Forging client signatures and fabricating file notes to justify fees are acts of dishonesty that directly engage the integrity dimension of the test.

Deliberate dishonesty findings have consistently placed ASIC enforcement outcomes at the ceiling of available penalties; in a separate 2026 case involving four corporate collapses and $12.4 million in creditor losses, comparable findings pushed the banning outcome to the statutory maximum under s 206F.

ASIC stated its approach reflects a commitment to protecting consumers and to intervening where conduct fails to meet the standards required of those operating in the financial services industry.

Because the test applies to both financial services and credit activities, the same factual findings triggered both Newbound’s personal ten-year ban and the cancellation of Freedom Wealth Services’ dual licences, all effective 1 May 2025. Failing this test is not a regulatory technicality. It is the mechanism by which ASIC removes someone’s legal authority to operate. A ten-year ban represents one of the most serious non-criminal outcomes available to the regulator.

Newbound was not operating on the fringes. His career spanned more than a decade within mainstream advice networks before the enforcement action landed.

| Period | Entity | Role | Licensing arrangement | End date |

|---|---|---|---|---|

| 16 August 2011 to 22 February 2021 | AMP Financial Planning Pty Ltd | Authorised representative | AFS licence held by AMP Financial Planning | 22 February 2021 |

| 16 August 2011 to 22 February 2021 | Logic Financial Services Pty Ltd | Sole director | Corporate authorised representative of AMP Financial Planning | 22 February 2021 |

| Post-February 2021 to 2026 | Freedom Wealth Services Pty Ltd | Sole director, financial planner, credit representative | Own AFS licence and ACL | Key person: 1 May 2025; Authorised rep: 17 June 2026 |

Nearly a decade under AMP Financial Planning’s licence, then a transition to his own firm. The career timeline matters because it shows that mainstream licensing networks do not automatically prevent this type of misconduct. That makes the consumer-checking steps later in this article relevant to anyone using a financial adviser, not only those using smaller or independent firms.

The enforcement did not land without a fight. Both Newbound and Freedom Wealth Services challenged ASIC’s decisions, and the procedural sequence matters because it explains why this article exists at all.

The substantive appeal remains pending, with no hearing date set as of the media release date. But the ban is operative now, not deferred. The Tribunal’s refusal to suppress reporting means you can legally check Newbound’s status on ASIC’s registers, and you should.

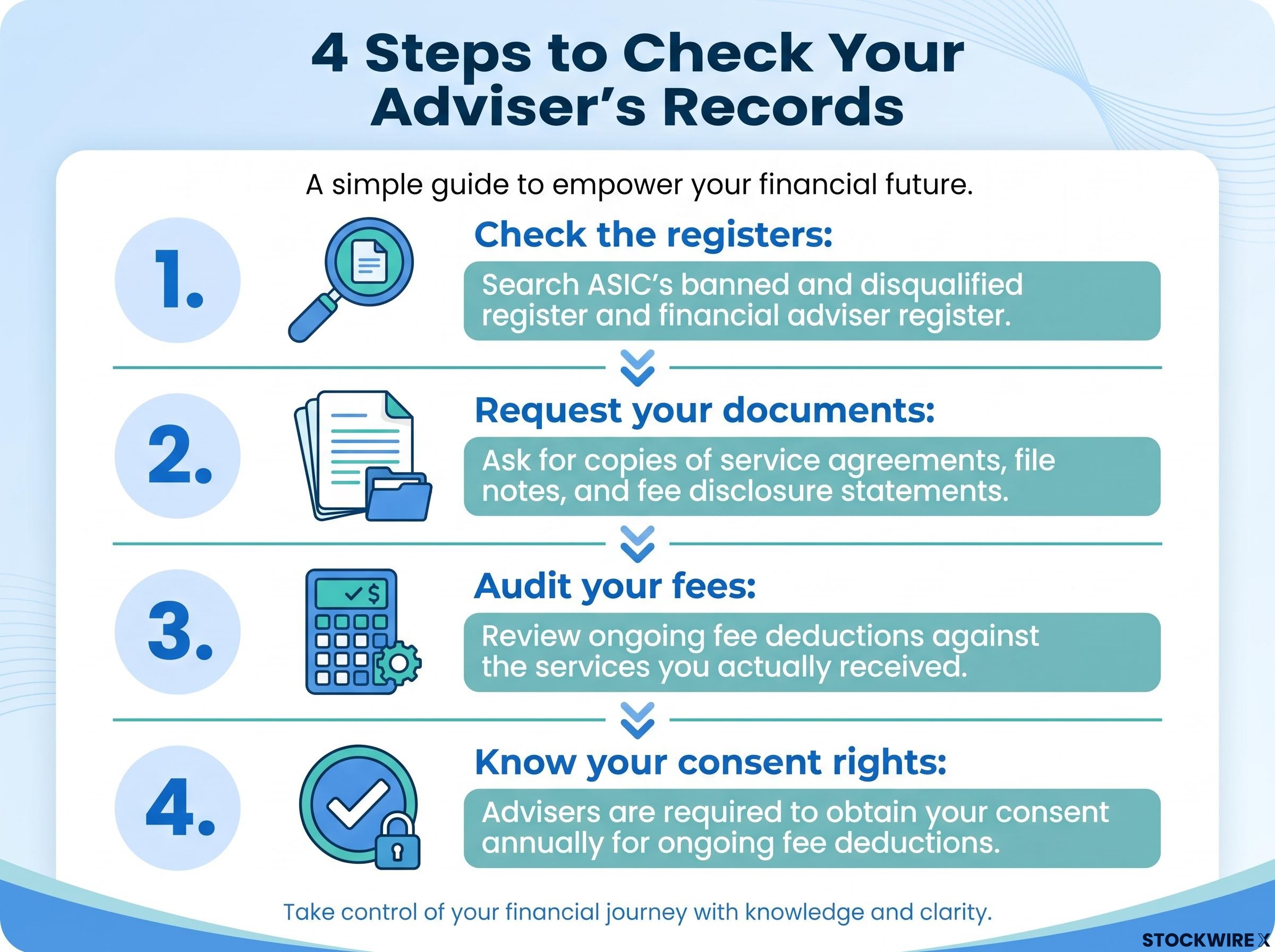

Misconduct of this type is typically uncovered through client complaints, ASIC surveillance, whistleblower reports, or a licensee’s internal review process. But there are steps you can take before it reaches that point.

Annual fee consent: Under current regulations, your adviser must obtain your consent each year before continuing to deduct ongoing service fees. If you have not been asked, your adviser may not be complying.

These are not steps reserved for people who suspect fraud. They are routine due diligence that ASIC’s own regulatory infrastructure makes straightforward.

The combined outcome, a personal ban, dual licence cancellations, and a defeated attempt to suppress reporting, sends a clear signal about how seriously ASIC treats falsified consent and fabricated service records. The ten-year duration is not a default. It reflects the gravity of findings that go directly to dishonesty under the fit and proper person test.

ASIC’s willingness to pursue both the ban and full public disclosure, including opposing confidentiality orders, means enforcement actions of this type are designed to be visible. That visibility is itself a consumer protection tool. If you have any doubts about your own adviser’s status, their record-keeping, or fees being deducted from your account, the registers are there for you to use.

ASIC stated the action is consistent with its obligation to safeguard consumers who use financial advisory services. The registers are free, the annual consent right is yours, and the documents are yours to request.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

—

ASIC found that Newbound forged client signatures on service agreements across three separate instances and fabricated file notes recording interactions that never happened, which were then used to justify ongoing fee deductions from client accounts.

The ban is ten years in duration and took effect on 1 May 2025, covering both the financial services and credit industries. Both of Freedom Wealth Services' licences, its AFS licence and its Australian Credit Licence, were also cancelled on the same date.

The fit and proper person test is the statutory threshold under the Corporations Act 2001 and the National Consumer Credit Protection Act 2009 that determines whether someone can legally provide financial advice or engage in credit activities, evaluating honesty, integrity, competence, and compliance history.

ASIC maintains a free, publicly accessible banned and disqualified register that confirms whether an adviser has been subject to enforcement action, and a separate financial adviser register that shows current licensing status. Both are available on ASIC's website.

Yes. You are legally entitled to request copies of your service agreements, file notes, and fee disclosure statements from your adviser, and you can audit ongoing fee deductions against services you actually received to check whether charges are justified.