What Rex’s 60-Day Guidance Silence Means for ASX Investors

17 mins ago

The window to buy Australian government bonds at yields above 5% has closed. Yields have pulled back to roughly 4.73%, global equities remain broadly expensive (technology in particular), and Australian shares look relatively decent mostly because they missed the rally. This is the late-cycle allocation problem: nothing looks obviously cheap, but the decisions you make here still matter.

This is the environment where poor portfolio decisions compound quietly. Investors who move to cash waiting for a clearer signal often wait indefinitely. Investors who pile into the same overvalued index exposure they already hold take on concentration risk they never explicitly chose. The current moment rewards deliberate composition management, not paralysis.

This piece works through each major asset class in the current environment and builds toward a practical framework for how Australian investors can position portfolios when the easy signals are gone. Here is a structured way to think about the trade-offs, not a prediction about what markets will do next.

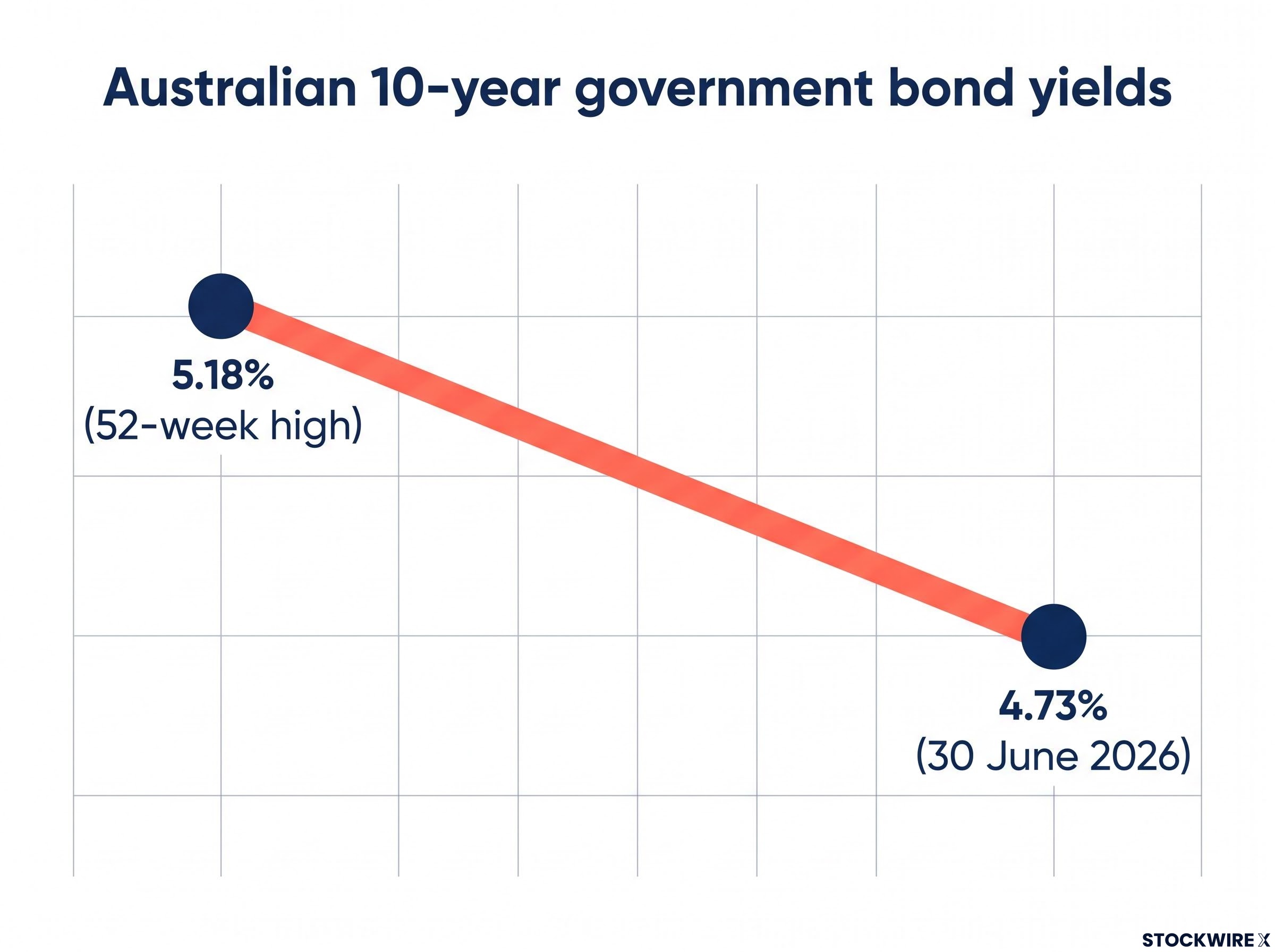

In the weeks before 30 June 2026, Australian 10-year government bond yields hit a 52-week high near 5.18%. At that level, the investment case was straightforward: you were being paid generously for holding a sovereign-backed instrument, with a meaningful cushion against inflation risk. The yield made bonds one of the clearest opportunities in the Australian market.

Then, over the course of roughly a month, yields fell to approximately 4.73%.

Yield snapshot: Australian 10-year government bond yields declined from a 52-week high of approximately 5.18% to roughly 4.73% as of 30 June 2026.

The decline was counterintuitive. Underlying inflation data deteriorated over the same period, which would normally push yields higher, not lower. Yet market expectations for an August RBA rate increase diminished, and bond prices rallied. The result is a bond market that moved from clearly attractive to approximately fair value in a matter of weeks.

If you bought bonds when yields were above 5%, that position is worth holding as a strong anchor in your portfolio. The yield you locked in provides a genuine buffer, and unnecessary trading would only erode the advantage.

For investors allocating fresh capital today, the calculus has shifted. At 4.73%, bonds remain a reasonable holding for income and diversification, but the margin of safety is thinner. Your outcome now depends more heavily on how inflation actually evolves. That does not mean avoiding bonds; it means thinking more carefully about duration and the inflation assumptions you are implicitly accepting.

When you buy a nominal Australian government bond today, you are not making a neutral decision. You are making an implicit forecast about future inflation. The number that reveals that forecast is the break-even inflation rate: the yield difference between inflation-linked bonds and nominal bonds, which represents the market’s embedded inflation expectation.

As of late June 2026, the 10-year break-even rate was sitting in a range of approximately 2.2% to 2.35%, consistent with both the RBA’s 2-3% target band and the levels observed over longer historical periods. Market-implied inflation expectations over the decade ahead have not moved materially higher.

The RBA’s inflation target framework sets the 2-3% band that nominal bond break-even rates are being priced against, making it the foundational reference point for evaluating whether current bond yields offer an adequate real return given the inflation assumptions embedded in them.

What this means in practice is that buying a nominal bond today is a bet that long-term inflation will average close to the RBA target. If it does, you earn an acceptable real return. If it does not, you may be better served by inflation-linked bonds, known as Treasury Indexed Bonds (TIBs), or shorter-duration instruments. Understanding that bet helps you decide whether to blend some inflation protection into your fixed income allocation.

| Scenario | Nominal bond outcome | TIBs / short-duration outcome |

|---|---|---|

| Realised inflation averages below ~2.2% | Acceptable real returns; nominal bonds perform well | TIBs underperform nominal bonds; shorter duration adds less value |

| Realised inflation persistently above ~2.2% | Real returns erode; purchasing power risk increases | TIBs outperform; shorter duration reduces inflation sensitivity |

Whether inflation remains persistent will be the critical determinant. Your bond allocation should reflect which scenario you find more probable, or better yet, blend instruments so you are not making an all-or-nothing bet.

Global equity markets were broadly expensive as of late June 2026, with technology sector valuations the primary driver. Even after a sell-off in the prior week, technology equities continued to appear overvalued, according to analysis from Morningstar Investment Management.

As of late June 2026, global equity markets carried elevated valuations overall, with the technology sector the principal contributor to that premium, a picture that held even following the prior week’s pullback.

That characterisation matters, but “expensive” alone is an incomplete observation. The more specific risk sits in the structure of how most investors access global equities. Cap-weighted global index funds give you large, concentrated exposure to a small set of US technology names, regardless of whether you consciously chose that exposure. If most of your equity allocation sits in those index funds, you have already made a significant bet on expensive US technology stocks.

Index fund concentration has reached a point where a standard global equity allocation is, in practice, a large leveraged position on a handful of US technology companies; five mega-cap stocks controlled roughly 23% of the broad US market index as of mid-April 2026, a level that exceeds historical precedents from prior bubble periods.

The constructive response is not to abandon equities. It is to change the composition of your equity exposure. Within equities, healthcare and consumer-oriented stocks were identified as offering more balanced earnings exposure without the same valuation premium. Options for adjusting include:

ASX healthcare and consumer sectors have posted their steepest declines of 2026, with healthcare stocks down 20-30% year-to-date and consumer discretionary off roughly 12%, creating a situation where Morningstar’s four-step valuation framework identifies potential gaps between current market price and through-cycle intrinsic value in exactly the sectors the article above recommends tilting toward.

The guiding principle: stay invested if your horizon is long, but be deliberate about how you are invested.

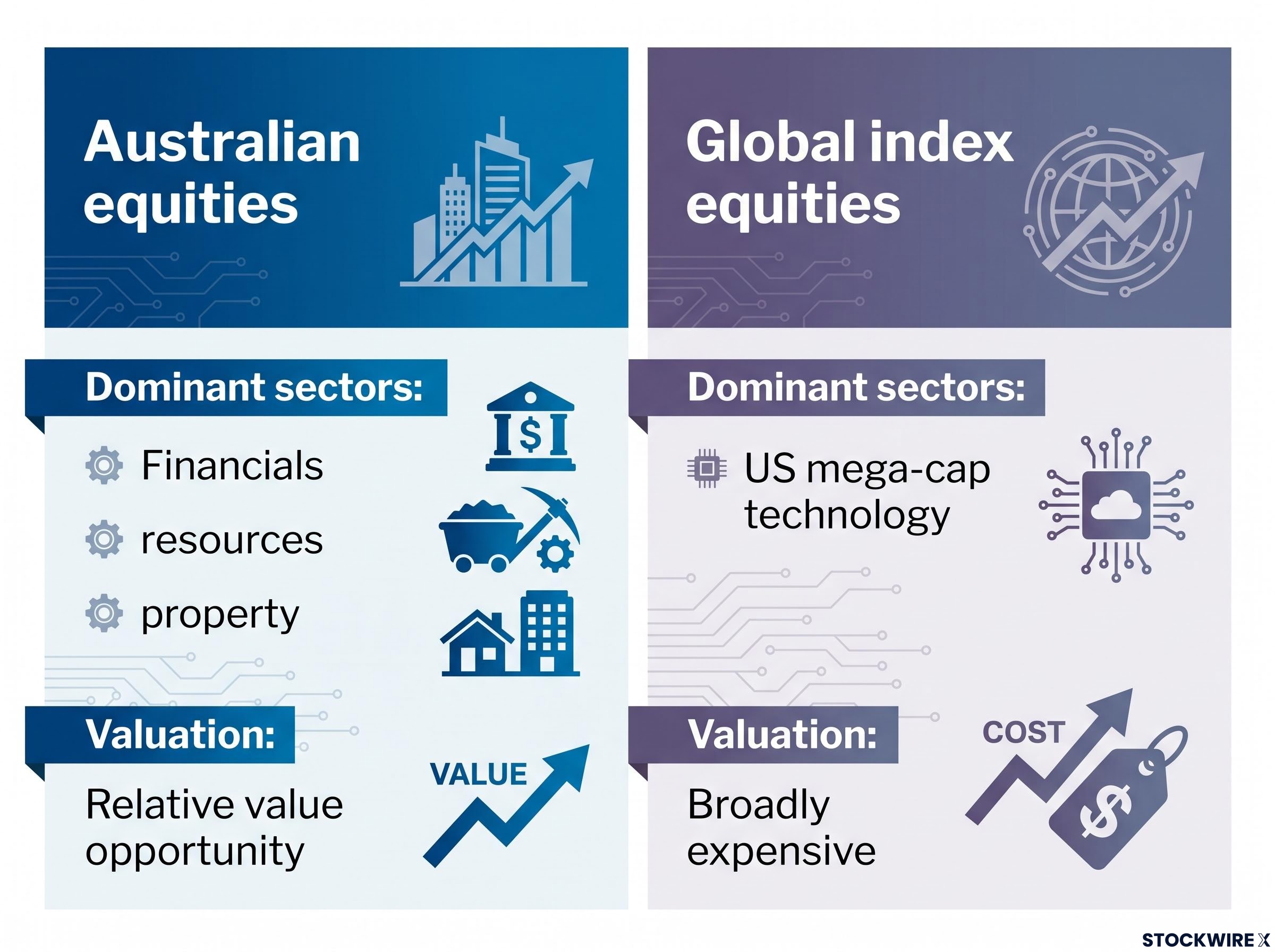

According to Joel Grosvenor, Portfolio Manager at Morningstar Investment Management, the valuation gap between domestic and international shares had shifted in Australia’s favour by late June 2026. That shift reflects a specific structural factor: the ASX largely sat out the technology-led surge that drove global index returns over the preceding months.

That absence is precisely what makes them interesting now. The ASX is heavily weighted toward financials, resources, and property, sectors that missed much of the tech-driven multiple expansion that inflated global index valuations. The result is a domestic market sitting at more defensible valuations on a risk-adjusted basis.

| Characteristic | Australian equities | Global index equities |

|---|---|---|

| Dominant sectors | Financials, resources, property | US mega-cap technology |

| Recent valuation characterisation | More reasonable; relative value opportunity | Broadly expensive; tech-driven premium |

| Role in a blended portfolio | Structural counterbalance to tech concentration | Core growth exposure with concentration risk |

For an Australian investor, a moderate tilt toward domestic equities is not a parochial call. It is a deliberate valuation adjustment that also happens to reduce concentration in the most expensive part of global markets. This is a tilt, not a wholesale move; global diversification should be maintained. The point is to improve the risk-return mix, not to bet solely on Australia.

A value tilt toward Australian equities has a macro-structural rationale beyond the near-term relative valuation gap: research from multiple asset managers shows value stocks have historically outperformed growth when inflation runs persistently above trend, the exact regime that Australian trimmed-mean inflation at 3.8% in March 2026 represents.

“Fairly valued” is a precise descriptor, not a warning signal. It means you are being paid roughly the expected return for the risk taken. That is not the same as “expensive” and is not a reason to exit.

Core reframing: “Fairly valued” means you are being paid the expected return for the risk taken. It is a description of your compensation, not an instruction to leave.

The actual portfolio risks in this environment are different from what many investors assume. They are:

Bonds and equities with different sector exposures behave differently through the cycle. That is the point of holding both. The current environment calls for active composition management, not a defensive rotation to cash.

The stock-bond correlation has behaved erratically during recent inflation shocks, turning positive in 2022 and again in 2025, which means the traditional assumption that bonds automatically cushion equity drawdowns no longer holds unconditionally and adds a layer of complexity to any blended portfolio construction decision.

Everything above builds the analytical case. This section translates it into a structured sequence of decisions you can apply to your own portfolio. Analysis here is attributed to Joel Grosvenor, Portfolio Manager at Morningstar Investment Management, as of late June 2026.

Inflation anchor: Track where realised inflation trends over the next 3-5 years relative to the approximately 2.2% break-even level. This is the central variable that determines whether your current bond allocations deliver the returns being priced in.

If inflation looks persistent and recurrent across multiple shocks, gradually increase TIBs, short-duration fixed income, and real assets with pricing power: selected infrastructure, resources, and some consumer staples.

If inflation convincingly settles near the RBA target, nominal bonds at current yields and a standard equity mix remain appropriate core holdings. The framework is designed to adjust with conditions, not to predict them.

In a late-cycle, mixed-signal environment, the edge comes from portfolio composition and inflation awareness, not from predicting the next market move. Nominal bonds at fair value remain reasonable but demand explicit inflation scenario awareness. Global equity exposure needs conscious management of tech concentration. Australian equities offer a genuine relative value tilt worth using.

The forward-looking variable to watch is whether realised inflation in Australia trends persistently above the approximately 2.2% break-even. That single measure will be the most important determinant of whether current bond allocations deliver the returns being priced in today. The portfolio that is well composed for both outcomes will not need to guess which one arrives.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

Break-even inflation is the yield difference between inflation-linked bonds and nominal bonds, representing the market's embedded inflation expectation. For Australian investors, the 10-year break-even rate sat near 2.2% to 2.35% in late June 2026, meaning a nominal bond buyer is implicitly betting that long-term inflation averages close to that level; if inflation runs persistently higher, real returns erode and inflation-linked bonds (TIBs) outperform.

At 4.73%, Australian government bonds remain a reasonable holding for income and portfolio diversification, but the margin of safety is thinner than it was at the 5.18% peak. Investors who locked in yields above 5% should hold those positions; those allocating fresh capital now need to be more deliberate about duration and the inflation scenario they are implicitly accepting.

The ASX missed most of the technology-led rally that inflated global index valuations because it is heavily weighted toward financials, resources, and property rather than US mega-cap technology. That sector composition means Australian equities are sitting at more defensible valuations on a risk-adjusted basis, making a moderate domestic tilt a deliberate valuation adjustment rather than a home-bias call.

Cap-weighted global index funds give disproportionately large exposure to a small number of US technology stocks; as of mid-April 2026, five mega-cap stocks controlled roughly 23% of the broad US market index. Investors who hold standard global index funds have effectively made a significant bet on expensive US technology companies, often without consciously choosing that exposure.

The recommended approach is disciplined composition management rather than moving to cash or maintaining concentrated index exposure. This means blending nominal bonds with inflation-linked instruments, tilting equity exposure toward healthcare and consumer sectors or valuation-aware active managers, adding a modest Australian equity overweight for relative value, and rebalancing systematically toward a chosen strategic allocation when markets move sharply.