What Rex’s 60-Day Guidance Silence Means for ASX Investors

5 mins ago

On the last day of Q2 2026, two assets that had each served as a portfolio answer were being repriced simultaneously and in the same direction. AI mega-cap equities, the consensus growth trade for eighteen months, faced another wave of valuation scrutiny. Gold, the supposed macro hedge, was closing its worst quarter in roughly a decade. Neither move, on its own, qualified as a crisis. Together, they amounted to something more disorienting: two formerly reliable convictions failing at the same time.

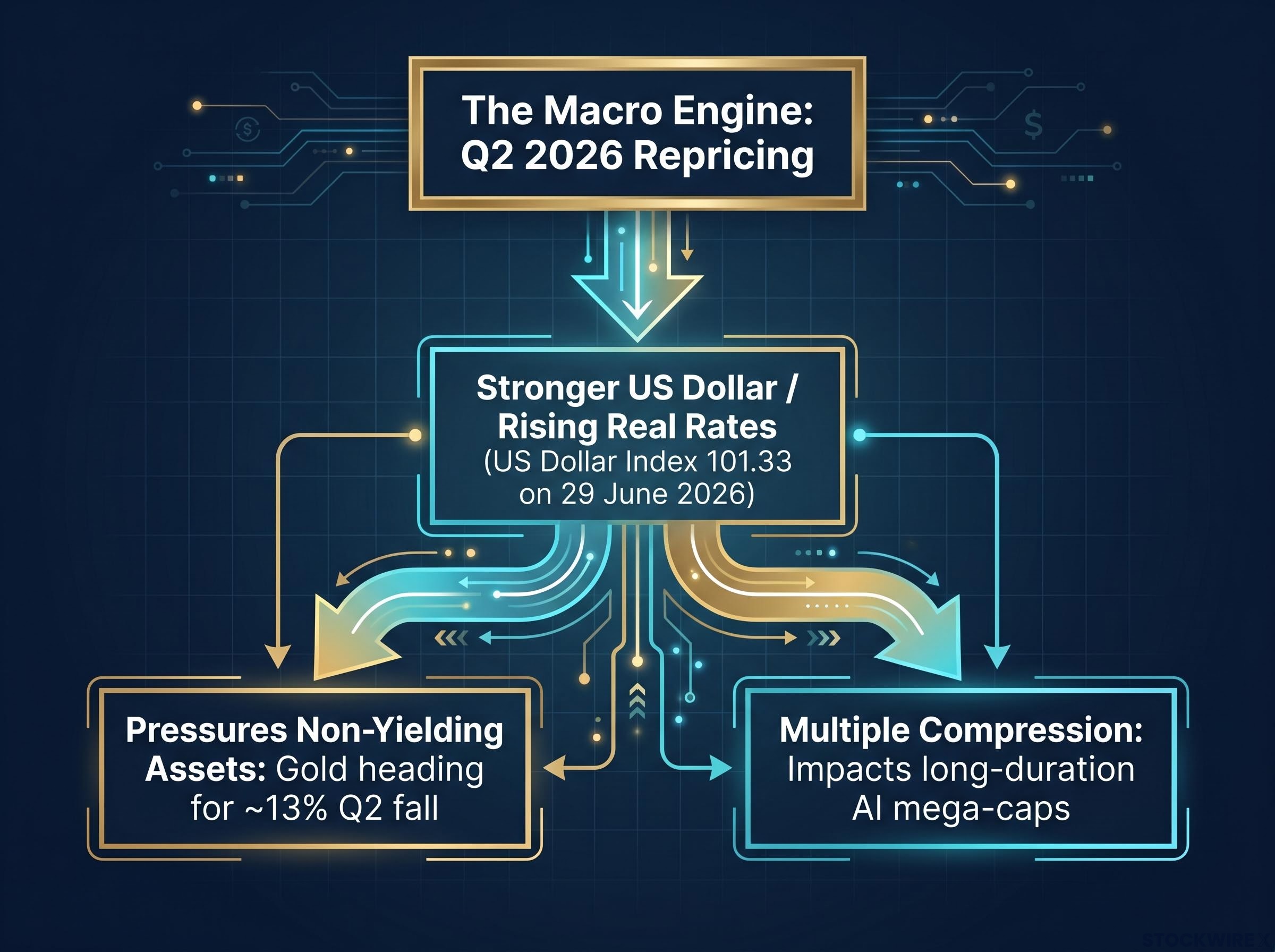

The timing is not a coincidence. Both repricing events share a common engine: Federal Reserve rate hike expectations and the dollar strength that follows. This is one macro mechanism producing two asset-class consequences at precisely the moment investors are making Q3 allocation decisions.

Here is what is actually driving both moves, what the convergence reveals about the current regime, and what it means for where capital should be positioned heading into the second half of 2026. Not a prediction. A framework for reading the signal.

The connection between gold’s collapse and the AI valuation reset runs through a single causal chain. Start with the Fed: futures markets have already factored in a minimum of one rate rise across 2026, with longer-term commentary pointing to limited easing and inflation remaining the primary concern. That rate expectation sets three things in motion.

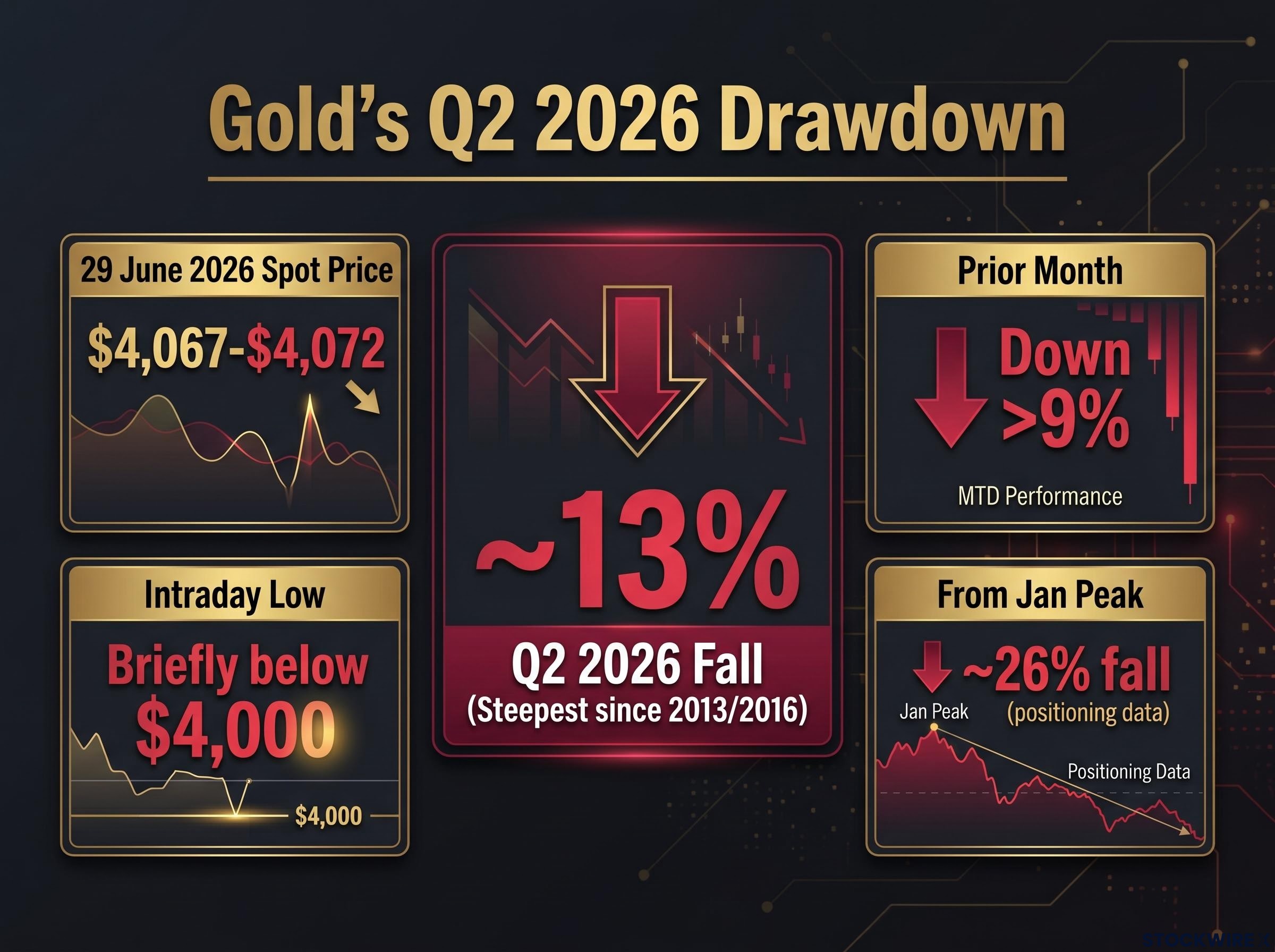

The US Dollar Index stood at 101.33 on 29 June 2026, just under the one-year peak reached the prior week (Reuters, Ankur Banerjee).

That reading is not a technical footnote. It is the barometric pressure telling you which macro regime you are operating in: a strong-dollar, rising-real-yield environment with direct consequences for every high-multiple or non-yielding position in your portfolio.

The Fed’s June 17 decision held the funds rate at 3.50%-3.75%, but the dot plot revision to a 3.8% year-end median put at least one additional hike into the Fed’s own baseline, hardening the rate expectations that are now compressing both gold and long-duration growth equities simultaneously.

Investors who are tracking the gold story and the tech story as separate headline risks are likely misreading both. The dollar index near a one-year peak is the shared variable, and it makes both repricing events not just simultaneous but structurally linked.

The scale of the drawdown deserves a moment to register.

Reuters reported that gold was heading for a quarterly fall in the region of 13% through Q2 2026, a loss the outlet described as the steepest in any single quarter since 2013, and by Moneycontrol as the steepest since late 2016. Either comparison lands the same conclusion: this was not a routine dip.

The key price data points:

The instinctive reading is that gold failed as a hedge. The more precise reading is that the specific macro conditions required for gold to function as an effective inflation hedge were absent.

A metal that briefly broke below $4,000 while the dollar was near a one-year peak is not malfunctioning. It is functioning exactly as the macro mechanics predict under a strong-dollar, rising-real-yield regime. That distinction matters enormously for how you respond. The problem is not that gold is broken. The problem is that a single-instrument hedge is always exposed to the specific conditions that instrument requires to work.

The AI trade has been dominant for the better part of two years. So why is the inflection point arriving in mid-2026 rather than earlier?

The answer is structural, not sentimental. The largest technology platforms have transitioned from asset-light, high-margin business models into a capital-intensive infrastructure investment race. That shift changes the earnings maths fundamentally.

The largest hyperscalers raised over USD 100 billion in debt in 2025 alone to fund AI-related capital expenditure (T. Rowe Price).

When the largest technology companies are raising nine figures in debt to fund infrastructure bets with uncertain payoff timelines, the question is no longer whether AI is transformative. It is whether current stock prices already assume the best-case scenario for revenue capture.

Multiple strategists have converged on this reading:

Micron’s robust forward guidance and Apple’s decision to push through higher prices on its products together highlight the widening gap in outcomes emerging across the sector. The valuation anxiety is not about whether AI matters. It is about who gets paid and when, which is precisely what this dispersion is beginning to reveal.

The rotation underway is not a de-risking of the whole market. It is a broadening of market leadership, and the distinction is critical.

De-risking would show up as a move to cash and short-duration bonds across the board. What the data shows instead is capital probing different parts of the equity market for better risk-reward. T. Rowe Price frames this as value migrating from software platforms to physical supply chains, potentially the most significant equity regime change since the global financial crisis. BlackRock argues the new environment rewards active management, factor diversification, and the flexibility to rotate across size, style, and geography. Citi points to long-cycle themes of supply-chain rewiring and energy independence as the durable underpinnings for broader equity leadership.

When BlackRock, Citi, and T. Rowe Price are converging on the same rotation themes independently, that is a signal worth taking seriously, not as a guarantee, but as a directional read on where institutional capital is already moving.

| Theme / Sector | Strategist Advocate | Key Rationale |

|---|---|---|

| Industrials / Manufacturing | T. Rowe Price, Citi | Supply-chain rewiring creating tangible capex demand with near-term earnings visibility |

| Energy / Power infrastructure | BlackRock, T. Rowe Price | AI data-centre buildout shifting value from platforms to physical power delivery |

| Small caps | Kavout, BlackRock, Citi | Broader market participation as concentration in mega-caps unwinds |

| Non-US developed markets | Citi, BlackRock | Regional diversification as US tech premium compresses |

| Value equities | Kavout, BlackRock | Capital efficiency and cash-flow visibility favoured over long-duration growth stories |

If your equity exposure is still concentrated in a narrow set of AI mega-caps, you may be positioned for a thesis that multiple major strategists are actively moving away from. That carries portfolio construction consequences regardless of your view on AI’s long-term significance.

Distributional volatility within AI-heavy indices is masking single-stock risk that aggregate measures obscure: large opposing moves by individual winners and losers cancel at the index level, leaving investors exposed to position-level danger they believe diversification has already resolved.

Gold’s Q2 performance forces a more conditional view of when and how the metal earns its place in a portfolio. The World Gold Council’s 2026 outlook provides the conceptual anchor.

The World Gold Council frames gold’s performance as highly path-dependent on the success or failure of policy responses, positioning it as a tail-risk hedge rather than a universal inflation hedge.

That distinction matters. Gold works as a hedge in scenarios of policy error or severe economic downturn. It faces structural headwinds in strong-dollar, rising-real-yield regimes, precisely the conditions prevailing now. Distinguishing between these conditions is the investor’s job.

A more durable approach treats hedging as a layered toolkit rather than a single-instrument bet:

The cost of conventional hedging is rarely made explicit in portfolio construction discussions: the traditional 60/40 portfolio lagged the S&P 500 by approximately 14 percentage points in 2024, and low-volatility equity funds underperformed by a similar margin, illustrating that every hedge has an opportunity cost that must be weighed against the protection it provides.

The World Gold Council notes that an AI expectations reset could become an additional drag on broader equity indices, given the weight of AI names, which connects the two asset narratives back together for hedging purposes. Longer-term forecasts still see potentially attractive gold levels by late 2026-2027, contingent on policy outcomes and central bank demand.

The lesson of Q2 2026 for gold holders is not that gold is broken. It is that a single-instrument hedge is always exposed to the specific macro conditions that instrument requires to work. That is a portfolio construction problem, not a gold problem.

Two time horizons need to be held simultaneously here, and the error most investors make is collapsing them into one.

Tactically, Q3-Q4 2026 is characterised by elevated volatility, widening dispersion, and continued sensitivity to Fed data surprises. The specific variables that could change the near-term picture quickly:

Structurally, the regime change underway is expected by multiple strategists to persist well beyond near-term noise. AI capex scrutiny, value migration toward physical infrastructure, and more diffuse equity leadership are not quarter-to-quarter trades. T. Rowe Price identifies capital efficiency and returns on incremental AI capex as the alpha-differentiating variable within the sector. BlackRock urges staying engaged with AI but demanding specificity about which companies monetise versus which absorb costs.

| Asset / Theme | Tactical View (Q3-Q4 2026) | Structural View (Late 2026-2027) | Key Risk to the View |

|---|---|---|---|

| AI mega-caps | Continued multiple compression; high sensitivity to rate data | Dispersion widens; winners separate from capex absorbers | Faster-than-expected AI monetisation validates current multiples |

| AI enablers (memory, power, industrials) | Near-term earnings visibility improving; beneficiaries of capex spend | Structural beneficiaries of physical infrastructure buildout | Capex cycle slows if hyperscaler returns disappoint |

| Gold | Pressured while dollar strength and rate hike expectations persist | Potentially attractive by late 2026-2027 if policy outcomes shift | Sustained disinflation or dovish pivot reverses dollar headwind |

| Small caps / Value | Broadening beneficiaries; rotation may pause but thesis intact | Structural shift toward diffuse equity leadership favours the category | Recession risk undermines small-cap earnings disproportionately |

| Non-US developed markets | Reassessment opportunity as US tech premium compresses | Regional diversification rewarded as concentration unwinds | Dollar strength persists, eroding non-US returns for USD investors |

Investors who can hold both the near-term sensitivity and the structural regime shift in mind simultaneously are better positioned to avoid the two most common errors: chasing momentum back into crowded trades, or abandoning credible long-cycle themes because of short-term noise.

For investors exploring the non-US developed market opportunity in more depth, our full explainer on the international equity rotation examines the specific valuation gap driving the outperformance, with the Emerging Markets ex-China ETF delivering approximately 31.5% year-to-date versus 9.3% for the S&P 500 as of late May 2026.

The simultaneous repricing of AI mega-caps and gold is not a coincidence or two separate risks. It is one macro regime expressing itself across asset classes, and the investor who understands that mechanism is better equipped to navigate the second half of 2026.

Two frameworks from this analysis carry forward. First, the conditional hedging lens: gold works under specific conditions, and building a layered toolkit beats relying on any single instrument. Second, the capital-efficiency filter: within technology, the question is no longer whether AI matters but which companies convert capex into earnings and which absorb the cost.

BlackRock describes the current environment as one of “reversal, rotation and recalibration.” That framing captures the regime precisely.

The structural shift underway, value migrating from platforms to physical supply chains, from concentrated mega-cap leadership to broader market participation, is expected by multiple major strategists to outlast this quarter’s volatility. Portfolio construction decisions made now are being made in that context.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

Market rotation is the shift of capital from one sector or asset class to another, and in mid-2026 it is being driven by rising real rate expectations and dollar strength that compress high-multiple AI mega-caps while simultaneously pressuring non-yielding assets like gold, pushing institutional money toward industrials, energy infrastructure, small caps, and value equities.

Gold dropped roughly 13% in Q2 2026, its steepest quarterly decline since 2013, because a strong US dollar (near a one-year peak at 101.33 on 29 June 2026) and rising real yield expectations made the non-yielding metal more expensive for non-US buyers and less attractive relative to yield-bearing alternatives.

The largest hyperscalers raised over USD 100 billion in debt in 2025 alone to fund AI infrastructure, shifting these businesses from asset-light models to capital-intensive ones; higher discount rates from Fed rate hike expectations are compressing multiples on these long-duration growth stocks precisely when investors are questioning whether current prices already assume the best-case revenue outcome.

BlackRock, Citi, T. Rowe Price, and Kavout are independently pointing to industrials, manufacturing, energy and power infrastructure, small caps, value equities, and non-US developed markets as the primary beneficiaries, with the common thread being capital efficiency and near-term earnings visibility over long-duration growth stories.

The World Gold Council frames gold as a tail-risk hedge that is path-dependent on specific macro conditions, not a universal inflation hedge; in a strong-dollar, rising-real-yield environment it faces structural headwinds, so a layered toolkit combining quality equities, shorter-duration bonds, and inflation-linked instruments is more durable than relying on gold alone.