Morgan Stanley Rules Out Fed Hikes, Names Two Numbers to Watch

11 mins ago

OpenAI has confidentially filed its S-1 with the Securities and Exchange Commission (SEC) and is targeting a public valuation of approximately $1 trillion, yet leadership is now reportedly leaning toward a 2027 debut rather than listing later this year. The filing landed around 22 May 2026, confirming that the process is already in motion even as the timeline stretches.

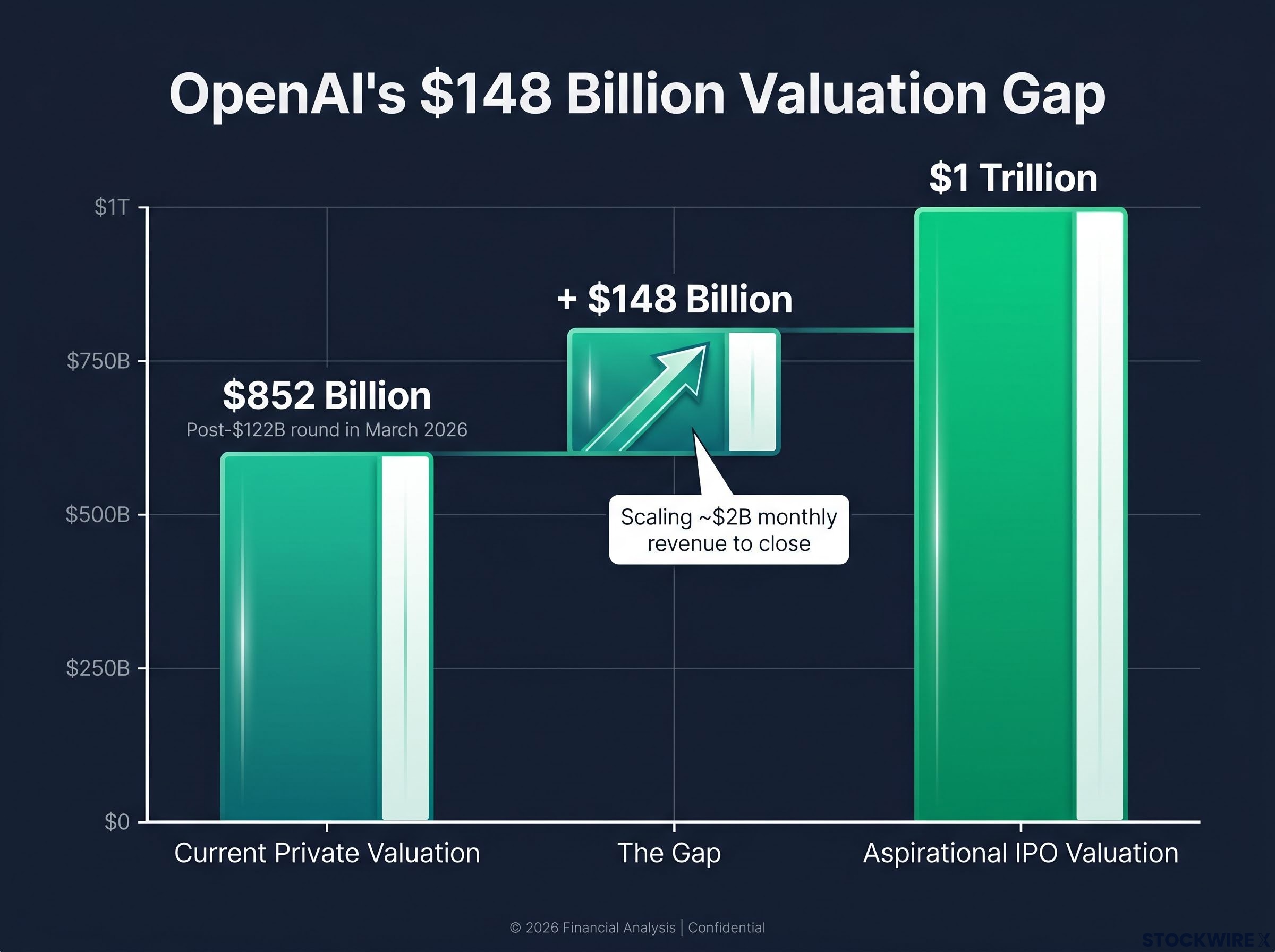

The gap between where the company sits today, a private-market valuation of roughly $852 billion following its $122 billion funding round in March 2026, and where it wants to arrive tells you what the timing debate is really about. OpenAI is generating approximately $2 billion in monthly revenue, a figure large enough to anchor a serious IPO thesis but not yet large enough to make a trillion-dollar ask feel inevitable to public-market investors.

If you hold AI-related equities or broad U.S. index funds, the when and the how of this listing carry direct portfolio implications. Here is what the filing, the valuation gap, and the delay signal about the company’s confidence in its own growth trajectory.

The confidential S-1 filing removes any ambiguity about intent. OpenAI is not floating the idea of going public; it has started the formal process, with the paperwork reaching the SEC around 22 May 2026.

The confidential IPO prospectus filed around 22 May 2026 confirms Goldman Sachs and Morgan Stanley as lead underwriters, with OpenAI’s Public Benefit Corporation structure meaning public shareholders would not hold traditional governance control, a structural distinction with no clean precedent among large-cap listings.

What the filing does not resolve is timing. The most likely listing window spans late 2026 to 2027, with recent reporting indicating that leadership is leaning toward the later end of that range. The company aims to raise at least $60 billion in the offering and wants to arrive in public markets at or above $1 trillion.

| Metric | Figure |

|---|---|

| Aspirational IPO valuation | ~$1 trillion |

| Current private valuation | ~$852 billion |

| March 2026 funding round | $122 billion |

| Monthly revenue | ~$2 billion |

| IPO raise target | $60 billion+ |

| S-1 filing date | ~22 May 2026 |

| Likely listing window | Late 2026 – 2027 |

The distance between $852 billion and $1 trillion is not trivial. That $148 billion gap tells you OpenAI is not waiting passively for a window to open; it is buying time to close a very specific financial argument before facing the scrutiny of public-market investors.

A delay to 2027 reads as calculated patience, not hesitation. Three strategic pressures point in the same direction:

According to The New York Times, CEO Sam Altman has reportedly expressed a preference for the $1 trillion valuation target, indicating that internal deliberations are oriented around arriving at that specific number rather than listing at whatever the market will bear today.

For investors evaluating pre-IPO AI funds or adjacent listed companies, Altman’s willingness to wait rather than rush is a signal. Management believes the growth curve has not yet peaked. Whether that reassures you or gives you pause depends on your view of how quickly enterprise AI adoption converts into durable, margin-accretive revenue.

AI valuation frameworks including the Shiller CAPE ratio at 40.11, Minsky’s financing stage analysis, and behavioural sentiment indicators each produce different verdicts on whether current AI sector multiples reflect durable monetisation or speculative excess, with the Magnificent Seven now representing approximately 34-35% of S&P 500 weight.

OpenAI is not the only company choosing patience over speed. Well-capitalised private companies at a late stage of development routinely hold off on a public listing when they judge that another year or two of growth could support a substantially higher valuation at debut. The reasoning is straightforward: so long as private capital markets continue to provide adequate funding, the cost of waiting is low and the potential upside of a stronger financial narrative at listing is significant.

The current cycle has intensified this pattern. A broader 2026-2027 IPO wave includes several prominent names:

Whichever company lists first at scale among the major AI platforms will set the valuation benchmark for the entire sector. If OpenAI arrives at $1 trillion and the market validates that number through sustained trading, analysts and fund managers will use that multiple as the reference point when pricing comparable companies across the AI stack, from infrastructure providers to application-layer firms to chip suppliers. A disappointing trajectory, conversely, would compress valuations across all three layers. That makes the OpenAI IPO a forward indicator for anyone holding AI-adjacent positions, not just a standalone corporate event.

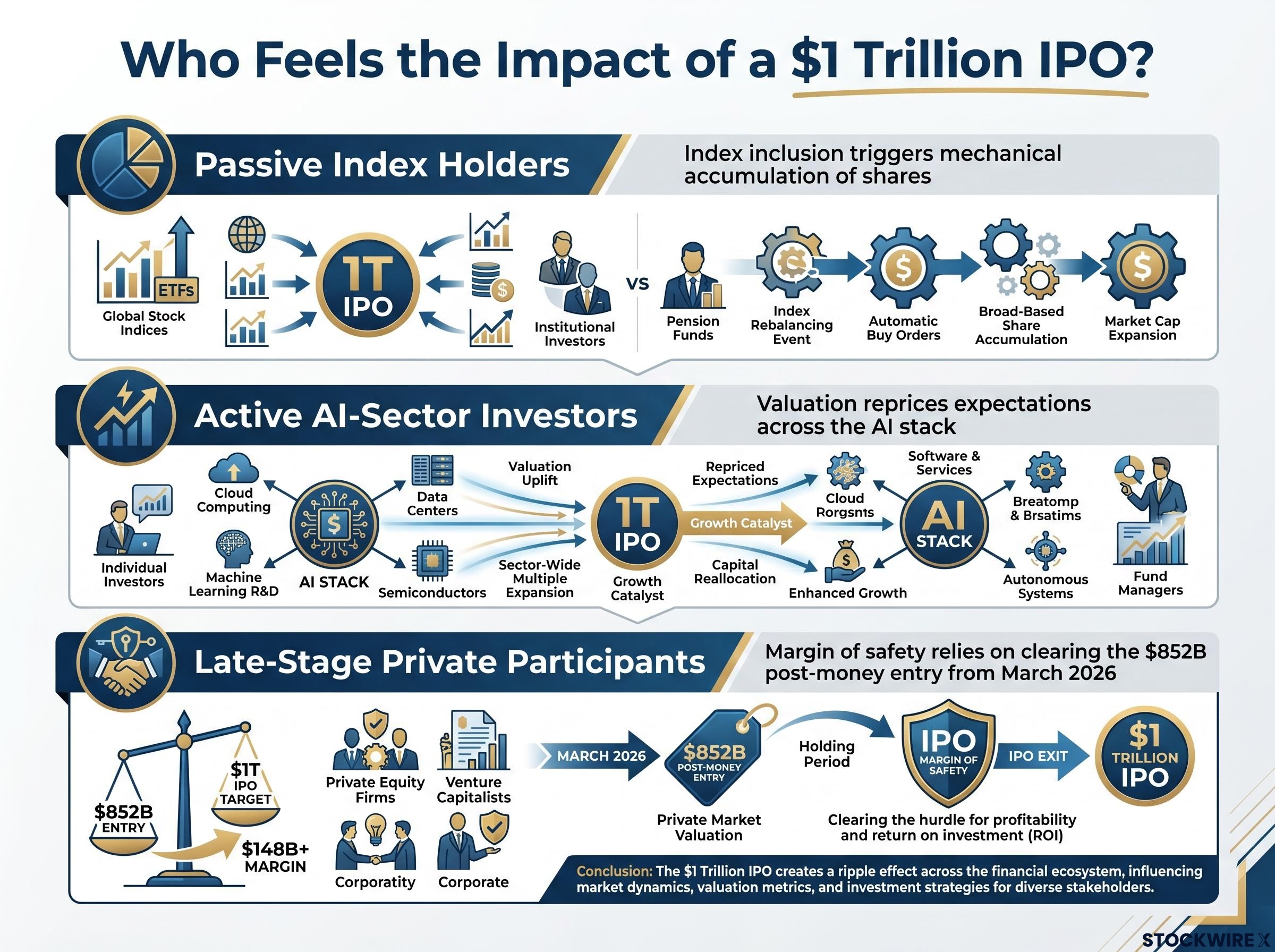

The trillion-dollar figure is easy to abstract. The mechanics behind it are concrete, and they reach further than just the investors who buy the offering.

Three distinct groups would feel the impact:

Index concentration risk compounds the passive exposure dynamic, with the top five US companies already controlling roughly 30% of total US market capitalisation and the top ten S&P 500 constituents representing approximately 40% of index weight, meaning a trillion-dollar OpenAI addition would deepen a skew that passive holders have already accumulated without active choice.

If you hold broad U.S. equity products, you will accumulate OpenAI exposure automatically upon listing, regardless of whether you actively choose to invest. The IPO is relevant to far more investors than just those tracking AI equities.

The S-1 is filed and the strategic logic points to 2027, but several variables could reshape the outcome between now and a potential listing:

If you are building a thesis on the OpenAI IPO as a sector-defining catalyst, hold that view with enough flexibility to reprice it. Any of these four variables shifting materially before 2027 could change the timeline, the valuation, or both.

The gap between $852 billion and $1 trillion is not a problem to be solved. It is a gap to be earned, and management’s willingness to wait rather than rush into public markets is itself an indicator of confidence in the revenue curve ahead. OpenAI is telling you, through its actions, that it believes enterprise AI monetisation has not yet reached the inflection point that would make a trillion-dollar valuation self-evident to public-market sceptics.

The metrics to monitor between now and a potential 2027 listing are monthly revenue growth, the pace and size of enterprise contract announcements, and any shifts in the competitive or regulatory landscape flagged above. Those will tell you whether the trillion-dollar moment is approaching or receding.

For investors building a position thesis on the OpenAI listing, our full explainer on IPO timing and retail underperformance covers Jay Ritter’s longitudinal dataset showing consistent S&P 500 underperformance across three and five year horizons, and why clusters of marquee filings historically signal that insiders believe valuations are near peak.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and company performance.

The OpenAI IPO refers to OpenAI's planned listing on U.S. public markets, for which the company filed a confidential S-1 with the SEC around 22 May 2026. Leadership is currently leaning toward a 2027 debut rather than listing in late 2026, with a target valuation of approximately $1 trillion.

OpenAI is generating approximately $2 billion in monthly revenue and was valued at roughly $852 billion following its $122 billion funding round in March 2026. Management is waiting until revenue growth closes the $148 billion gap to $1 trillion so the valuation ask feels credible and inevitable to public-market investors, rather than listing at whatever the market will bear today.

A $1 trillion debut would place OpenAI immediately among the largest U.S. companies by market capitalisation, triggering mandatory index inclusion; this means index funds underpinning most retirement accounts would be required to accumulate OpenAI shares mechanically, regardless of any active investment view.

Goldman Sachs and Morgan Stanley are confirmed as lead underwriters on the OpenAI IPO, as disclosed through the confidential S-1 prospectus filed around 22 May 2026.

Four main variables could shift the outcome: competitive pressure from Anthropic and Google DeepMind eroding OpenAI's valuation narrative, changes in interest rates affecting what investors will pay for long-duration AI growth stocks, regulatory moves around large AI models, and OpenAI's own execution on revenue growth and compute cost discipline.