What Berkshire’s Insurance Float Actually Does to Returns

2 hrs ago

Eli Lilly’s stock has staged one of the most dramatic runs in large-cap pharmaceutical history. The share price reflects a company that has already won. And yet, by most estimates, GLP-1 drugs have reached only about 2% of the global obese population. Something cannot be both over and early at the same time.

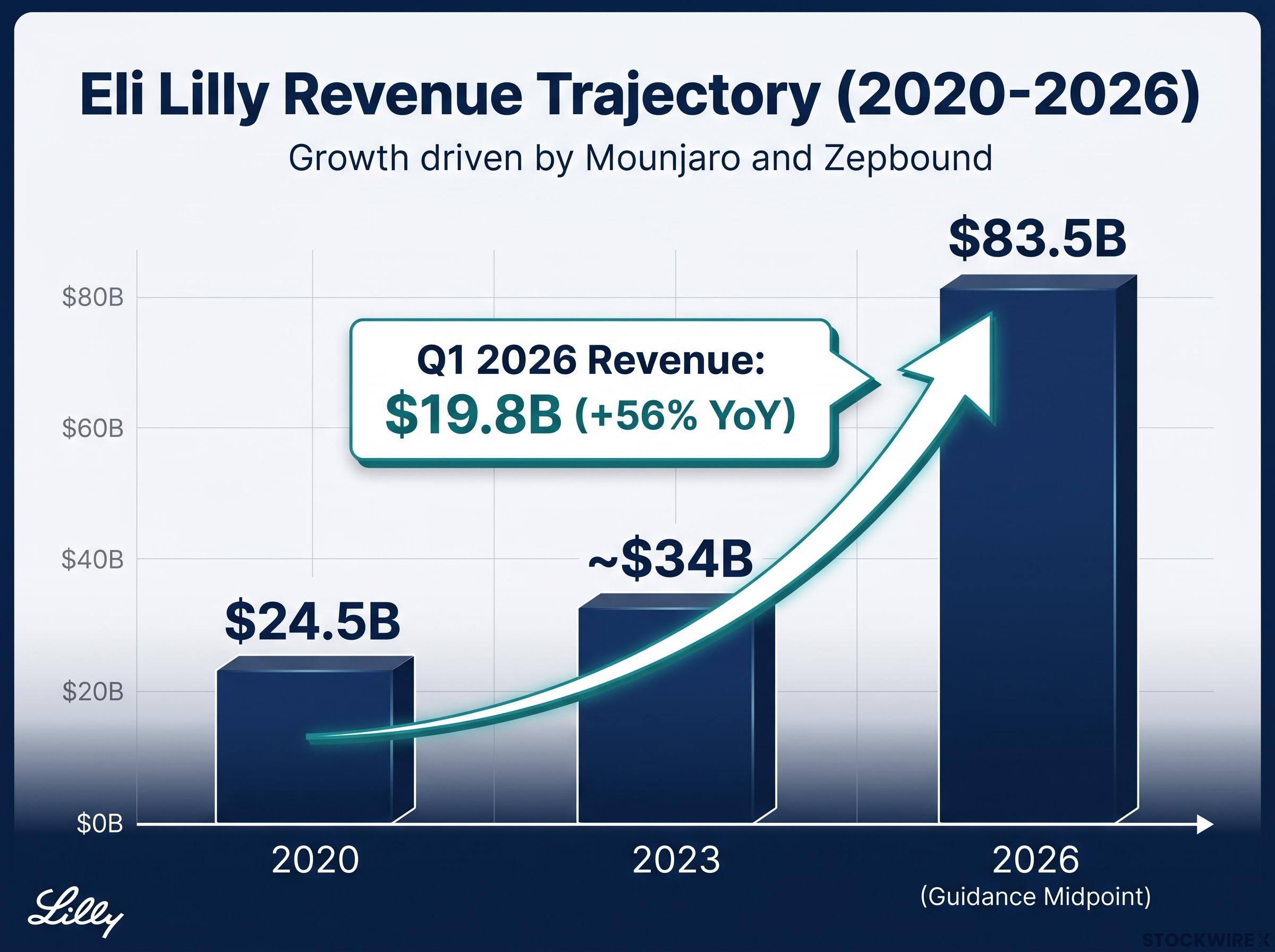

That tension sits at the centre of every conversation about Eli Lilly in mid-2026. The company updated its Q1 guidance to a full-year revenue range of $82-$85 billion, up from $24.5 billion in 2020. It is one of the most searched and debated healthcare names in the market, and investors who missed the initial move are asking a version of the same question: have they permanently missed the trade, or is a multi-decade megatrend still accessible at this price?

Here is the case for and against investing at current levels, and the specific conditions that would need to hold for either scenario to play out. The goal is not to hand you a verdict but to give you the questions worth asking before you make a call.

This analysis is for informational purposes only and does not constitute financial, investment, or tax advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Start with the baseline. Eli Lilly generated $24.5 billion in revenue in 2020. By the midpoint of its 2026 guidance, that figure reaches $83.5 billion. Nearly all of that acceleration comes from two products: Mounjaro (tirzepatide, approved for diabetes) and Zepbound (tirzepatide, approved for obesity). They are the same molecule with different regulatory labels, and together they have turned a mid-tier pharmaceutical company into one of the highest-revenue drug makers on the planet.

The FDA approval of Zepbound confirmed that tirzepatide, already marketed as Mounjaro for type 2 diabetes, received a separate regulatory label for chronic weight management, a dual-indication structure that gives Lilly two distinct commercial pathways from a single molecule.

The most recent quarterly print puts the growth rate in perspective.

Eli Lilly reported approximately $19.8 billion in Q1 2026 revenue, up 56% year over year.

A 56% year-over-year growth rate at a $19+ billion quarterly run rate is not how mature pharmaceutical businesses behave. Conventional valuation tools, built for companies growing at 5-10% annually, struggle to capture a trajectory this steep. That matters because it shapes how you should read every earnings print and analyst revision going forward: the question is not whether Lilly is growing, but whether the rate of growth can persist long enough to justify the price the market is charging today.

One nuance worth noting: volume growth has been exceptional, but realised prices have started compressing due to payer pressure. Both things are true simultaneously. Revenue is surging because demand is overwhelming the price headwind, but the price headwind exists, and it will feature in every forward estimate.

| Year | Revenue (USD billions) | Key Driver |

|---|---|---|

| 2020 | $24.5B | Legacy portfolio (pre-GLP-1 ramp) |

| 2023 | ~$34B | Mounjaro launch and early scaling |

| 2026 (guidance midpoint) | $83.5B | Mounjaro + Zepbound at scale |

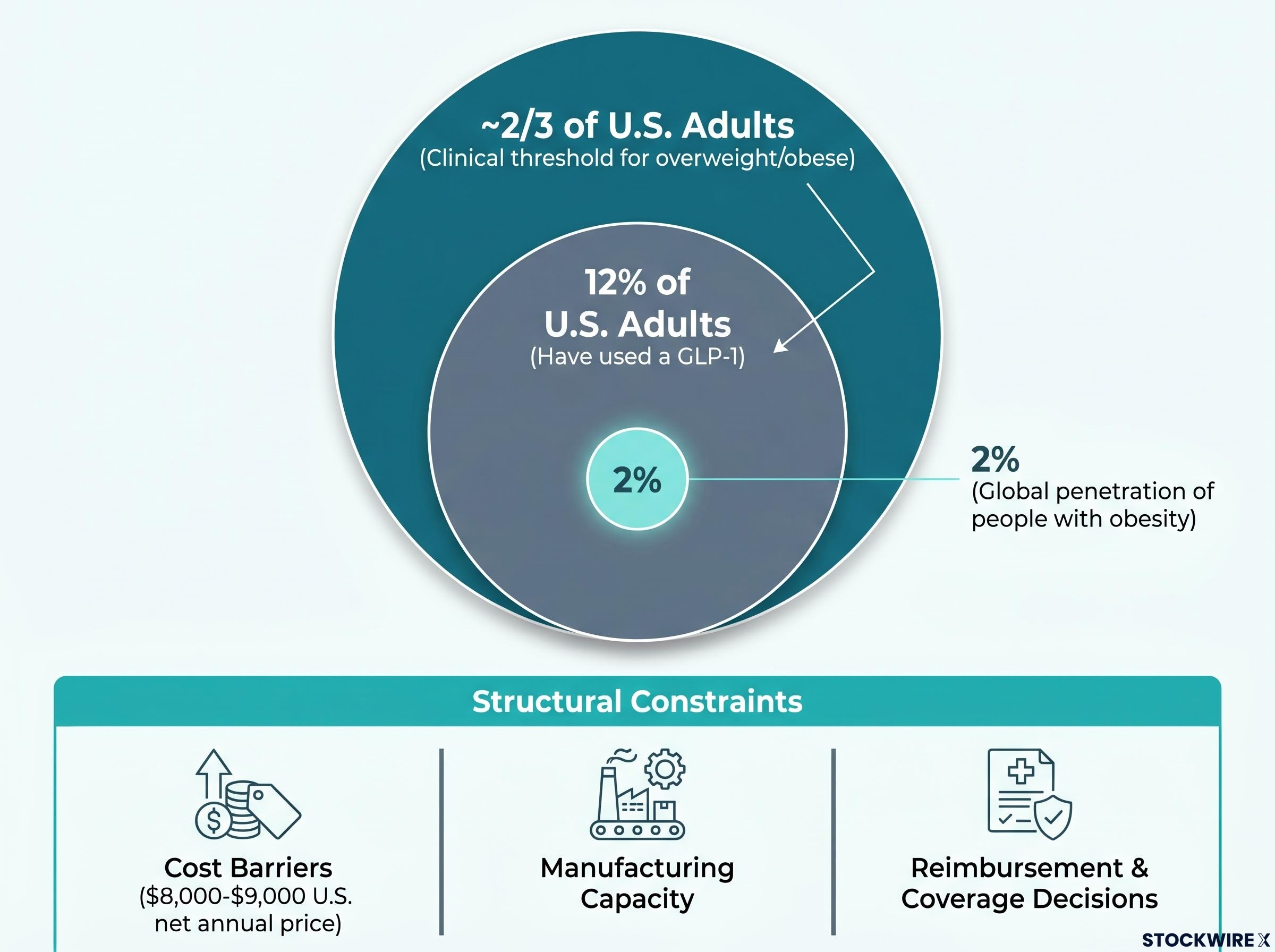

Despite the media saturation and the stock’s performance, the adoption numbers tell a different story about where the GLP-1 category actually sits on its growth curve. According to the Kaiser Family Foundation, roughly 12% of U.S. adults have used a GLP-1 medication, including drugs such as Ozempic or Wegovy. Globally, one widely cited bank estimate puts GLP-1 penetration at roughly 2% of people with obesity, though that figure has not been independently verified.

Set those numbers against the addressable population. U.S. health data consistently shows that around two in three adults in the country meet the clinical threshold for overweight or obese status. The gap between 2% global penetration and a two-thirds domestic prevalence rate is the single most important number in the GLP-1 bull case. It is the difference between a trade that is mostly done and a market that has barely started.

The GLP-1 weight management market is attracting capital across the healthcare ecosystem, not only at the drug-maker level: in May 2026, Doctor Care Anywhere acquired a direct-to-consumer GLP-1 prescribing business for approximately A$1.7 million, representing a 0.16x EV/Sales multiple on trailing revenue and illustrating how the demand signal is reaching even the delivery and prescribing layer of the category.

But the gap does not close automatically. Three structural constraints explain why penetration remains low despite overwhelming demand.

What this tells you is straightforward: the market opportunity is enormous, but the speed at which Lilly can convert it into revenue depends on variables that extend well beyond clinical efficacy. Understanding those variables is the difference between a considered position and a bet on momentum.

The investment case shifts meaningfully when you look past Mounjaro and Zepbound to what is coming next. Lilly is not betting on a single product. It is building a sequenced pipeline where each new asset solves a problem the current products cannot.

Lilly’s licensing activity extends well beyond its own branded pipeline: in early 2026 the company secured exclusive rights to clazakizumab from CSL for a $100 million upfront payment plus milestone exposure, a move that signals the company is actively deploying capital into immuno-inflammatory indications that sit outside the GLP-1 and Alzheimer’s categories entirely.

| Asset | Mechanism | Stage | Strategic Role |

|---|---|---|---|

| Orforglipron | Oral small-molecule GLP-1 | Phase 3 complete | Expands addressable population via oral delivery |

| Retatrutide | Triple agonist (GLP-1/GIP/glucagon) | Phase 3 data available | Next-generation efficacy beyond dual agonists |

| Kisunla | Anti-amyloid (Alzheimer’s) | Approved | Revenue diversification beyond obesity/diabetes |

If orforglipron and retatrutide both reach market and gain meaningful coverage, Lilly’s revenue runway extends well beyond current products. That optionality is a key part of what justifies the premium multiple the stock carries today. Without it, you are paying a growth-company price for a traditional pharma asset, and the maths becomes harder to defend.

Eli Lilly’s market capitalisation sits in the range of approximately $900 billion to $1 trillion as of mid-2026, with the stock trading at approximately 40 times earnings. That is not a pharmaceutical multiple. It is a growth-company multiple, and it comes with growth-company expectations baked into the price.

For the investment to generate strong returns from current levels, five conditions likely need to hold simultaneously:

Section 232 pharmaceutical tariffs introduce a tiered rate structure with a 100% default rate for non-qualifying manufacturers, and while generic drugs and biosimilars currently carry a temporary exemption, that exemption faces reassessment as early as April 2027, adding another layer of policy uncertainty to net price realisations across the category.

That is a lot of things that need to go right at the same time. And each one individually is plausible. The question is whether all five remain true across the investment horizon.

The bear case does not require catastrophe. It requires that some of those assumptions are delayed or underwhelming.

In a stock already priced for excellence, even a “good but not great” outcome can trigger a sharp compression in the earnings multiple.

For investors working through whether a 40x earnings multiple on a $900 billion to $1 trillion market cap is defensible, our dedicated guide to intrinsic value and margin of safety walks through discounted cash flow construction, terminal value sensitivity, and the practical discount thresholds value practitioners apply before committing capital, with worked examples relevant to high-growth businesses.

Consider three specific scenarios. Orforglipron’s regulatory submission is delayed by six to twelve months, pushing meaningful oral GLP-1 revenue into 2028 or later. U.S. pricing reform materialises faster than models assume, compressing net realisations by 10-15% before volume fully compensates. Novo Nordisk regains market share with its own next-generation pipeline, eroding the assumption that Lilly’s competitive position is durable.

None of those scenarios is implausible. None requires a product failure. Each simply represents a world where Lilly delivers good results that fall short of the very high expectations the current multiple demands. Pullbacks driven by pricing news, supply disruptions, or trial data are historically common for high-multiple growth stocks regardless of long-term trajectory.

“What am I being paid for the risk I’m taking, and does that match my investment profile?”

That is the better question. “Is it too late?” assumes there is a single answer. There is not.

The answer depends on who you are as an investor. A long-horizon, high-conviction investor with a 5-10+ year view who believes GLP-1 therapies will become a multi-decade standard of care can rationally own Lilly at a premium multiple. The thesis is that category growth, pipeline sequencing, and global expansion will generate enough earnings growth to justify today’s price over time.

A shorter-term or more conservative investor faces a less attractive trade-off. Much of the optimistic scenario is already priced in. The asymmetry is unfavourable: the upside requires near-perfect execution, while the downside only requires delay.

| Dimension | Long-Horizon Investor (5-10+ years) | Shorter-Term / Conservative Investor |

|---|---|---|

| Time horizon | Multi-decade megatrend exposure | Needs returns within 1-3 years |

| Valuation sensitivity | Willing to pay premium for category leadership | Premium pricing limits margin of safety |

| Recommended framing | Core growth holding, sized appropriately | Wait for a pullback or size very small |

In both cases, the most practical risk management tool is position sizing. Treat Lilly as a high-quality but higher-risk growth holding rather than an oversized core position. This approach allows participation in the GLP-1 upside while keeping portfolio-level risk manageable if the story proves less perfect than the current price implies. One perspective from the original source discussion is worth noting: investment trends typically persist longer than investors expect, and tracking a company like Lilly over time, through earnings reports and pipeline milestones, has value as a learning exercise regardless of position size.

Three catalyst categories will test the bull case in the months ahead, and each provides a specific signal worth monitoring:

KFF analysis of Medicare drug price negotiation under the Inflation Reduction Act confirms that GLP-1 drugs including Ozempic and Wegovy have been selected for negotiated pricing, with new rates scheduled to take effect in 2027, a policy timeline that directly shapes the net realisation assumptions built into Lilly’s forward revenue models.

Manufacturing capacity remains an ongoing watch item. Supply constraints have periodically created access gaps, and the pace of capacity expansion will influence both revenue and competitive dynamics against Novo Nordisk, which is scaling its own manufacturing programme.

The synthesis is this: the GLP-1 opportunity is probably not over. A 2% global penetration rate, a massive addressable population, and a sequenced pipeline argue that the category has years of growth ahead. But with a market capitalisation approaching $1 trillion and an earnings multiple of approximately 40 times, the stock is not cheap. Investors who understand both of those realities simultaneously, that it is both early and expensive, are in a better position to make an informed decision than those anchored to either “I missed it” or “it can only go up.”

Past performance does not guarantee future results. Financial projections referenced in this article are subject to market conditions, regulatory outcomes, and various risk factors. This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

GLP-1 drugs are a class of medications that mimic a gut hormone to regulate blood sugar and appetite, and they are the primary driver of Eli Lilly's revenue surge, with Mounjaro and Zepbound, both based on the molecule tirzepatide, pushing annual revenue guidance to a midpoint of $83.5 billion in 2026, up from $24.5 billion in 2020.

One widely cited bank estimate puts global GLP-1 penetration at roughly 2% of people with obesity, a figure that underpins the bull case that the category has barely started converting its addressable population despite the media saturation and Lilly's dramatic stock performance.

Trading at approximately 40 times earnings with a market cap approaching $1 trillion, Lilly's stock requires five conditions to hold simultaneously: sustained GLP-1 category growth, maintained market share against Novo Nordisk, adequate manufacturing capacity, regulatory approval and reimbursement of orforglipron and retatrutide, and no severe U.S. drug-pricing policy changes compressing margins.

Lilly's next-generation pipeline includes orforglipron, an oral GLP-1 pill that completed Phase 3 with statistically significant A1C reductions; retatrutide, a triple agonist that met primary endpoints in Phase 3 obesity trials with a stronger weight-loss signal than current products; and Kisunla, an approved anti-amyloid therapy for early Alzheimer's disease that diversifies revenue beyond the obesity and diabetes categories.

The article recommends treating Lilly as a high-quality but higher-risk growth holding rather than an oversized core position, with long-horizon investors able to rationally hold at a premium multiple over a 5-10 year view, while shorter-term or conservative investors face unfavourable asymmetry because the upside requires near-perfect execution and the downside only requires delay.