Tasmea Ltd Forecasts Over 70% Earnings Growth in Record FY27 Guidance

Tasmea forecasts more than 70% earnings growth in record FY27 guidance

Tasmea Limited (ASX: TEA) has issued earnings guidance for the financial year ending 30 June 2027, forecasting more than 70% year-on-year earnings growth in what represents record forward guidance for the specialist trade skills services group.

The company expects Underlying EBITA of A$202–A$208 million and Underlying NPATA of A$128–A$132 million for FY27, following completion of its FY27 budgeting process.

Management attributes the guidance to a record order book at the commencement of FY27, more than 120 Master Services Agreements, and a number of programmatic acquisitions during Q4 FY26. The figures reflect continued execution of Tasmea’s twin-pillar growth strategy of organic growth and programmatic acquisitions.

Tasmea also reconfirmed its FY26 guidance, as previously announced to the ASX on 24 June 2026. For investors, the guidance provides forward earnings visibility into the next financial year before it has even begun.

When big ASX news breaks, our subscribers know first

The numbers behind the guidance

The FY27 guidance sets out clear ranges across the group’s core profitability metrics, alongside an organic growth assumption for its base businesses.

| Metric | FY27 Guidance Range | Notes |

|---|---|---|

| Underlying EBITA | A$202–A$208m | More than 70% YoY growth |

| Underlying NPATA | A$128–A$132m | Before amortisation of acquired customer contracts |

| Organic growth (base businesses) | 10–15% | FY27 vs FY26, excludes acquisitions |

Underlying EBITA and Underlying NPATA exclude the impact of non-underlying items and are stated before the non-cash profit and loss impact from amortisation of acquired customer contracts expense resulting from the company’s announced programmatic acquisitions.

The guidance incorporates specific acquisition assumptions. The Maxim Group acquisition, now unconditional, is expected to settle on 1 July 2026, with a full 12-month contribution assumed.

The Maxim Group acquisition, structured across upfront cash, scrip, and a performance-linked earn-out of up to A$70 million across FY27-FY29, is forecast to deliver approximately 31% pro forma EPS accretion and lift the combined group’s Electrical segment EBIT to approximately A$100 million.

The JPS Group acquisition is expected to settle on or around 1 August 2026, contributing 11 months of earnings. JPS remains subject to the satisfaction of customary conditions precedent, including obtaining ACCC approval to proceed under Australia’s new mandatory merger control regime.

The JPS Group acquisition adds a recurring LNG services platform with Tier-1 clients including Chevron, Shell, and Woodside, bringing more than 10 long-term MSAs and revenue visibility exceeding 80% for FY27 from Australia’s producing LNG facilities.

Consistent with prior practice, the FY27 guidance excludes any contribution from potential new acquisitions other than those already announced during FY26 to date.

The twin-pillar growth strategy explained

Tasmea owns and operates 28 individual brands that provide outsourced specialist maintenance and labour hire to fixed plant for essential industry asset owners. These businesses focus on shutdown, programmed maintenance, emergency breakdown, and brownfield upgrade services across Australia’s key industries.

Two terms are central to understanding the company’s earnings visibility. An order book represents the contracted and expected work the company has lined up. A Master Services Agreement (MSA) is a long-term contract that governs the ongoing provision of services to a customer, generating recurring revenue rather than one-off project income.

Recurring, contracted revenue matters to investors because it provides earnings predictability. The company’s twin-pillar strategy combines this organic base with acquisitions, and the FY27 guidance is driven by several factors:

-

Growth in high-quality, recurring revenues, with now more than 120 MSAs, Facilities Management Agreements and long-term contracts following recent acquisitions and organic customer growth.

-

Increasing revenue synergies across the national portfolio, which the company describes as having the widest breadth of self-perform specialist capabilities in the market.

-

Strong industry tailwinds across mining and resources, data centres and infrastructure, oil and gas, electrification, power and renewables, waste and water, telecommunications, defence, and retail.

-

The first full-year contribution from recently acquired WorkPac, plus the maiden contribution from the Maxim Group and JPS Group acquisitions.

-

Continued organic growth of 10–15% from the existing base businesses in FY27 versus FY26.

Record order book and strengthening revenue pipeline

Tasmea’s contracted order book has reached record levels, which the company states provides strong forward earnings visibility and reinforces its ability to deliver sustained organic earnings growth.

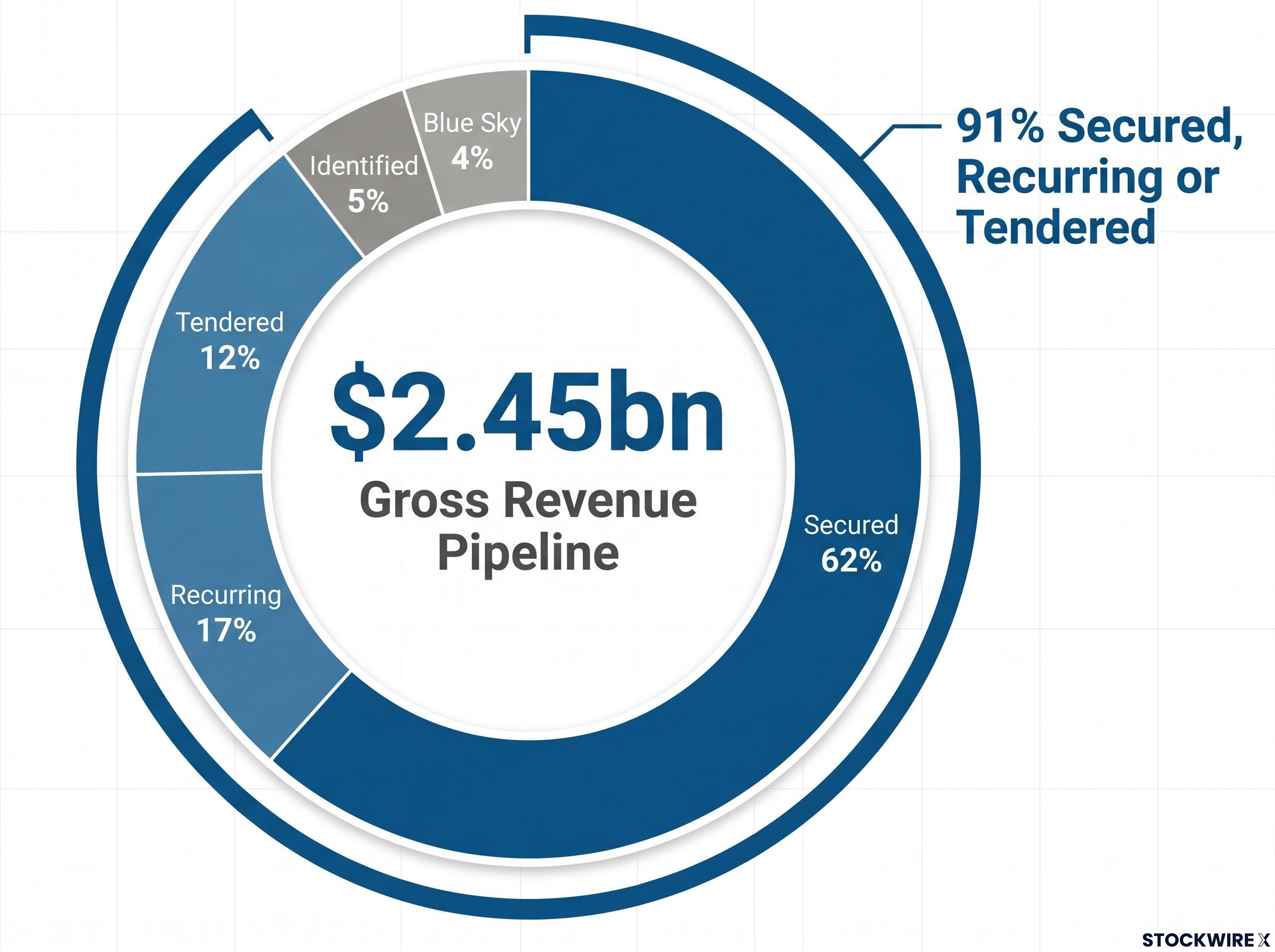

At the commencement of FY27, the revenue pipeline stood at $1,436m on a net revenue basis for the current group, including WorkPac. Of this, 85% is secured, recurring and tendered.

On a gross revenue basis, the full revenue pipeline is approximately $2.45bn, with 91% classified as secured, recurring or tendered. The FY27 gross revenue profile breaks down as follows:

-

Secured: 62%

-

Recurring: 17%

-

Tendered: 12%

-

Identified: 5%

-

Blue Sky: 4%

A record contracted order book underpins forward earnings visibility and helps de-risk the guidance, with the majority of FY27 revenue already secured or recurring rather than speculative.

A track record of compounding growth

Tasmea has consistently delivered compounding earnings growth since its IPO, recording a multi-year EBIT and NPAT CAGR of more than 50% from FY24 to forecast FY27. The revenue pipeline has also strengthened each year from the commencement of FY24 through to the commencement of FY27.

Director alignment reinforces the picture. Executive Directors Stephen Young, Mark, Jason and Trent have collectively reinvested over $50 million in Tasmea since IPO.

For investors, sustained insider reinvestment of this scale signals management confidence in the company’s outlook and alignment with shareholders.

Managing Director’s outlook

Founder and Managing Director Stephen Young pointed to the momentum behind the FY27 guidance and the contribution of the company’s workforce.

Stephen Young, Founder and Managing Director

“We are proud to be providing FY27 earnings guidance that reflects the continued strength and momentum of our business. These results are only possible thanks to the outstanding efforts of our people across the country. I want to sincerely thank all Tasmea employees for their unwavering commitment to safety and operational excellence — the foundation of everything we do. Tasmea’s Executive Directors, Mark, Jason, Trent and I have together reinvested over $50 million in Tasmea since IPO—reflecting our continued confidence in the Company’s outlook, our strategy, and the strength of the team that’s driving it with our core purpose, to Deliver Value. Always!”

The announcement was authorised for release by Stephen Young, Managing Director, on behalf of the Board of Tasmea Limited.

The next major ASX story will hit our subscribers first

What it means for investors

The FY27 guidance positions Tasmea for forecast earnings growth of more than 70% year-on-year, with Underlying EBITA of A$202–A$208 million and Underlying NPATA of A$128–A$132 million. That visibility is anchored by a record contracted order book, more than 120 long-term agreements, and diversified exposure to structurally supported industry sectors.

The guidance combines organic momentum of 10–15% from the base businesses with maiden and full-year contributions from recent acquisitions.

Two near-term catalysts remain on the timeline: the Maxim Group settlement expected on 1 July 2026, and the JPS Group settlement expected on or around 1 August 2026, the latter pending ACCC approval. Both will determine the pace at which the forecast contributions flow through to the group’s earnings.

Don’t Miss the Next Industrials Breakout on the ASX

Big News Blast delivers FREE breaking ASX news and in-depth analysis directly to your inbox within minutes of release. Over 20,000 active subscribers are already getting the edge on market-moving announcements the moment they hit. Click the “Free Alerts” button at StockWire X to make sure you never miss the next major move.