Eli Lilly at 40x Earnings: Expensive Stock, Underpenetrated Market

1 hr ago

Barclays is formally underweight UK equities. Its strategists do not think the index deserves a full allocation heading into the second half of 2026. And yet, the same team has identified specific pockets of the UK market it considers worth buying, with tactical overweight positions established in banks, homebuilders, and real estate.

That tension sits at the centre of the UK stock market outlook right now. The Bank of England held rates at 3.75% in June 2026. A projected 20% earnings-per-share growth headline for UK equities looks strong on the surface. But the global market remains dominated by AI and technology narratives from which the UK is structurally excluded, and the fine print beneath that earnings number tells a less comfortable story.

This piece separates the index-level case from the sector-level case. After reading it, you will have a practical framework for understanding which parts of the UK market deserve attention, which deserve scepticism, and how Barclays’ apparently contradictory positioning actually holds together as a single, coherent investment view.

The verdict came first. Emmanuel Cau and the Barclays equity strategy team entered the second half of 2026 with a formal underweight on UK equities, paired with a stated preference for eurozone stocks as their core European allocation. This is not a reaction to a single data point or a quarterly miss. It is a structural positioning call.

Two problems underpin it, and they compound each other. The first is composition: the UK index has negligible allocation to the technology sector that has driven global equity returns for the past several years. The second is earnings quality: the headline growth number for UK equities looks strong, but its foundations are narrow and increasingly fragile.

According to Barclays, the eurozone offers more cyclical tilt than the defensively positioned UK market, making it the preferred European allocation for H2 2026.

The backdrop to Barclays’ eurozone preference involves a period of European equity consolidation that has left the STOXX Europe 600 roughly 9% behind the S&P 500 over the same three-month window, with the same US-Iran diplomatic dynamic that is pressuring UK energy earnings identified as the single catalyst most capable of triggering a sharp sector rotation across consumer, banking, and luxury names.

What this tells you is that the underweight is unlikely to reverse on sentiment alone. It is rooted in what UK indices are made of, and that composition does not change quarter to quarter. Understanding these two structural pillars is the prerequisite to evaluating whether the sector-level opportunities Barclays identifies are worth pursuing.

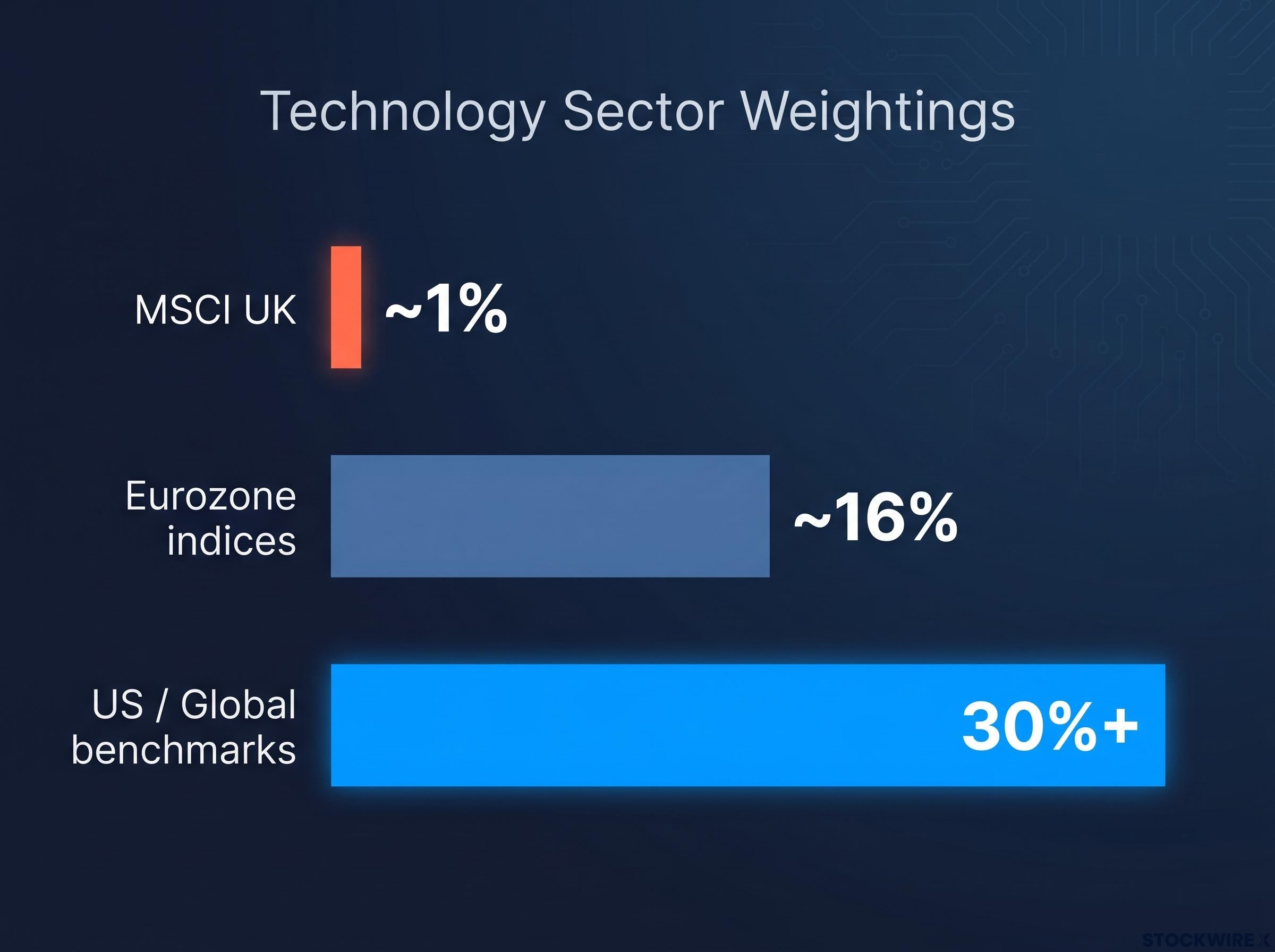

Start with one number: approximately 1%. That is the MSCI UK index’s weighting in Information Technology. Now compare it.

| Index | Technology weighting | Structural implication |

|---|---|---|

| MSCI UK | ~1% | Near-zero participation in tech-led earnings growth |

| US / Global benchmarks | 30%+ | Fully exposed to the AI and mega-cap growth engine |

| Eurozone indices | ~16% | Partial participation; meaningfully above UK |

In an AI- and tech-led bull market, an index with near-zero tech exposure simply cannot participate in the primary driver of global earnings growth. The gap between 1% and 30% is not a rounding error. It is a structural explanation for why the UK has persistently lagged global benchmarks, and it is not something that changes with a single listing or IPO cycle.

If you already hold US tech-heavy funds or global index ETFs, the UK’s composition gap is not only an explanation for past underperformance. It is a practical reason why adding targeted UK exposure could reduce concentration risk in your existing portfolio, precisely because the UK does not track the same driver.

The same composition that drags in a tech boom becomes a buffer in a tech-led correction. The UK’s defensive, value-oriented market structure holds up better when expensive growth names sell off, because it never participated in the rally that inflated them.

According to Barclays, both UK and European equities carry value as portfolio diversifiers for investors with concentrated exposure to AI and mega-cap technology names. If the AI trade stumbles, the UK could outperform on a relative basis; not because its fundamentals improve, but because its exposure profile means it has less to lose from that specific reversal.

The valuation logic underpinning a potential market leadership rotation is directly relevant here: MSCI EAFE trades at roughly a 50-55% forward P/E discount to the S&P 500 IT sector, a spread near multi-decade extremes that has historically preceded extended periods of underperformance by the dominant cohort.

The headline is eye-catching. UK equities carry a projected earnings-per-share growth rate of approximately 20% for 2026. At face value, that looks like a market you want to own.

Then you look at what is driving it.

Barclays characterises this growth as reliant on sectors that are themselves under pressure. The US-Iran nuclear agreement has contributed to a decline in oil prices, and that decline is eroding the energy earnings support that the 20% headline depends on.

The relationship between oil prices and rate expectations runs deeper than a single earnings line: a sustained oil shock adds roughly one percentage point to CPI readings, creating a policy dilemma for the Bank of England between tightening into a supply shock and holding at the risk of losing inflation credibility, a dynamic that has material consequences for the bank sector thesis as well as the energy earnings base underpinning the 20% headline.

Barclays identifies the UK’s projected EPS growth as narrowly sourced from energy and commodities, leaving the headline number exposed to commodity price swings and masking the relative weakness of earnings across the rest of the index.

A 20% growth figure that depends on a single volatile sector is not broad-based earnings health. It is concentration risk wearing the appearance of index-level strength, and you should treat it with the same scepticism you would apply to any undiversified position. The analytical discipline here applies well beyond this single call: whenever an earnings headline looks strong, the first question is always what is driving it, not just what the number is.

The structural critique is the index-level story. The sector-level story is different, and it is where Barclays finds genuine opportunity. Three sectors carry tactical overweight calls, each with a distinct investment thesis rather than a shared “buy UK” argument.

| Sector | Core thesis | Key support factor | Primary risk |

|---|---|---|---|

| UK banks | Rate-supported margin expansion | Bank Rate held at 3.75% | Faster-than-expected rate cuts |

| Homebuilders | Mispriced risk premium | Persistent housing supply constraints | Consumer confidence deterioration |

| Real estate / REITs | Yield plus optionality | Post-repricing valuation compression | Economic slowdown hitting rents and occupancy |

The common thread across all three is that markets appear to be pricing in worse conditions than Barclays’ fundamental analysis supports. In each case, the opportunity is a valuation gap rather than a growth story, and that distinction matters for how you size any position.

The Bank of England held the Bank Rate at 3.75% in June 2026, and that level remains supportive for net interest margins, the spread between what banks earn on loans and what they pay on deposits. UK banks still trade at a discount to many European peers, offering what Barclays sees as a positive earnings trajectory at modest valuations.

The Bank of England June 2026 rate decision confirmed the Monetary Policy Committee voted to hold Bank Rate at 3.75%, a level that continues to support net interest margin expansion for UK lenders and underpins the core of Barclays’ constructive thesis on the sector.

The risk is straightforward: faster-than-expected rate cuts would compress those margins, and a sharper UK economic slowdown would hit credit quality and loan demand simultaneously. If rates stay supportive and the economy avoids a hard landing, this is a growth-at-a-reasonable-price thesis.

Barclays sees mispriced risk in homebuilders. Current valuations embed a risk premium that appears excessive relative to what the sector’s yield profile and housing supply dynamics would support. Persistent UK housing supply constraints provide structural support that does not disappear with short-term sentiment shifts.

The potential catalyst is mortgage affordability. As rates gradually normalise, demand could recover. The risk side is consumer confidence and any renewed spike in financing costs. But the core Barclays argument is that markets are pricing in worse conditions than the reality, creating a gap between sentiment and fundamentals that patient investors can exploit.

For income-focused investors, the real estate sector offers yield plus optionality. After a painful repricing driven by higher interest rates, UK REIT and property valuations have compressed meaningfully, and with rate expectations beginning to normalise, entry points look more attractive than they have in several years.

The risk set here is broader: an economic slowdown that hits rents and occupancy, and structural questions in commercial real estate, particularly around offices and hybrid working patterns. But for investors willing to accept those risks, the current risk premium relative to the sector’s yield profile is larger than Barclays believes conditions warrant.

The Barclays positioning logic translates into a specific portfolio discipline. UK equities are a diversifier and a source of selective sector exposure. They are not a core growth engine meant to replace global or eurozone allocations.

The distinction between index-level positioning and sector-level positioning is the most practically important takeaway from this analysis. Holding a broad UK index tracker alongside a global equity fund may be doing less work at the index level than you expect, while the sector-level opportunities Barclays identifies require more targeted exposure to capture.

Barclays’ framework implies three practical steps:

The eurozone remains Barclays’ preferred European cyclical allocation. The UK’s role is supplementary and selective, not foundational.

The quantitative case for European diversification rests on a 31% valuation discount to the S&P 500 on forward earnings multiples, a gap that persisted even after European markets rallied in early 2026, meaning the relative value argument does not depend on a precise market-timing call.

The Barclays underweight is conditional, not permanent. Three specific variables would alter the picture, and monitoring them is more useful than waiting for a blanket upgrade.

None of these are predictions. They are monitoring signals. The enduring tension in Barclays’ view is that the UK is not broken; it is composed differently. That composition will eventually work in its favour under specific market conditions, but those conditions are not yet in place.

The UK equity index carries real structural weaknesses: a near-absent technology sector, earnings growth concentrated in a single volatile commodity complex, and a composition that lags in the current market regime. Those weaknesses are genuine, and they justify the underweight at the index level.

But they do not apply uniformly. Banks, homebuilders, and real estate each carry valuation gaps that Barclays’ analysis suggests are wider than fundamentals warrant. The framework is clear: underweight the index, selectively constructive on specific sectors, and useful as a diversifier against tech concentration.

The most actionable distinction this analysis offers is a simple one. What the UK index is doing and what specific sectors within it are doing are two different investments, requiring two different analytical frameworks. Treating them as one decision is where allocation mistakes are made.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and company performance.

Barclays is formally underweight UK equities at the index level for H2 2026, citing near-zero technology sector exposure and earnings growth concentrated in volatile energy and commodities. Despite this, the firm holds tactical overweights in UK banks, homebuilders, and real estate, where it sees valuations pricing in worse conditions than fundamentals support.

The MSCI UK index allocates approximately 1% to Information Technology, compared to over 30% in US and global benchmarks. In an AI and tech-driven bull market, that near-zero exposure means the UK index simply cannot participate in the primary engine of global earnings growth.

Barclays treats it with caution: the headline 20% earnings-per-share growth figure is disproportionately driven by energy and commodities, and the US-Iran nuclear agreement has contributed to falling oil prices that are already eroding that earnings base. Strip out energy and commodities, and the underlying UK earnings picture is considerably weaker.

Barclays holds tactical overweight positions in UK banks, homebuilders, and real estate. UK banks benefit from the Bank of England holding rates at 3.75%, supporting net interest margins; homebuilders carry what Barclays sees as an excessive risk premium relative to housing supply dynamics; and real estate offers yield plus valuation optionality after a significant post-rate-rise repricing.

Three signals would shift the picture: a sharp correction in AI and mega-cap technology names (which would favour the UK's defensive composition), a stabilisation or recovery in oil prices (which would firm up the energy earnings underpinning the 20% EPS headline), and a slower, shallower Bank of England rate-cutting path (which would sustain bank margin expansion for longer).