Reliance Worldwide Targets US$9M Earnings Boost Closing Melbourne Brass Plants

Reliance Worldwide Corporation (ASX: RWC) has announced plans to close brass casting, forging and machining operations at its Moorabbin and Braeside facilities in Melbourne, along with additional smaller sites, targeting an annual earnings uplift of approximately US$9 million by the end of FY27. The closures follow a sustained decline in brass production volumes at the Melbourne facilities, rendering continued operations economically unviable.

The restructuring forms part of RWC’s ongoing optimisation of its global manufacturing footprint rather than reactive cost cutting. Approximately 85 employees are expected to be affected, with consultation underway and anticipated to complete during July 2026.

RWC targets US$9 million annual earnings uplift through Australian manufacturing consolidation

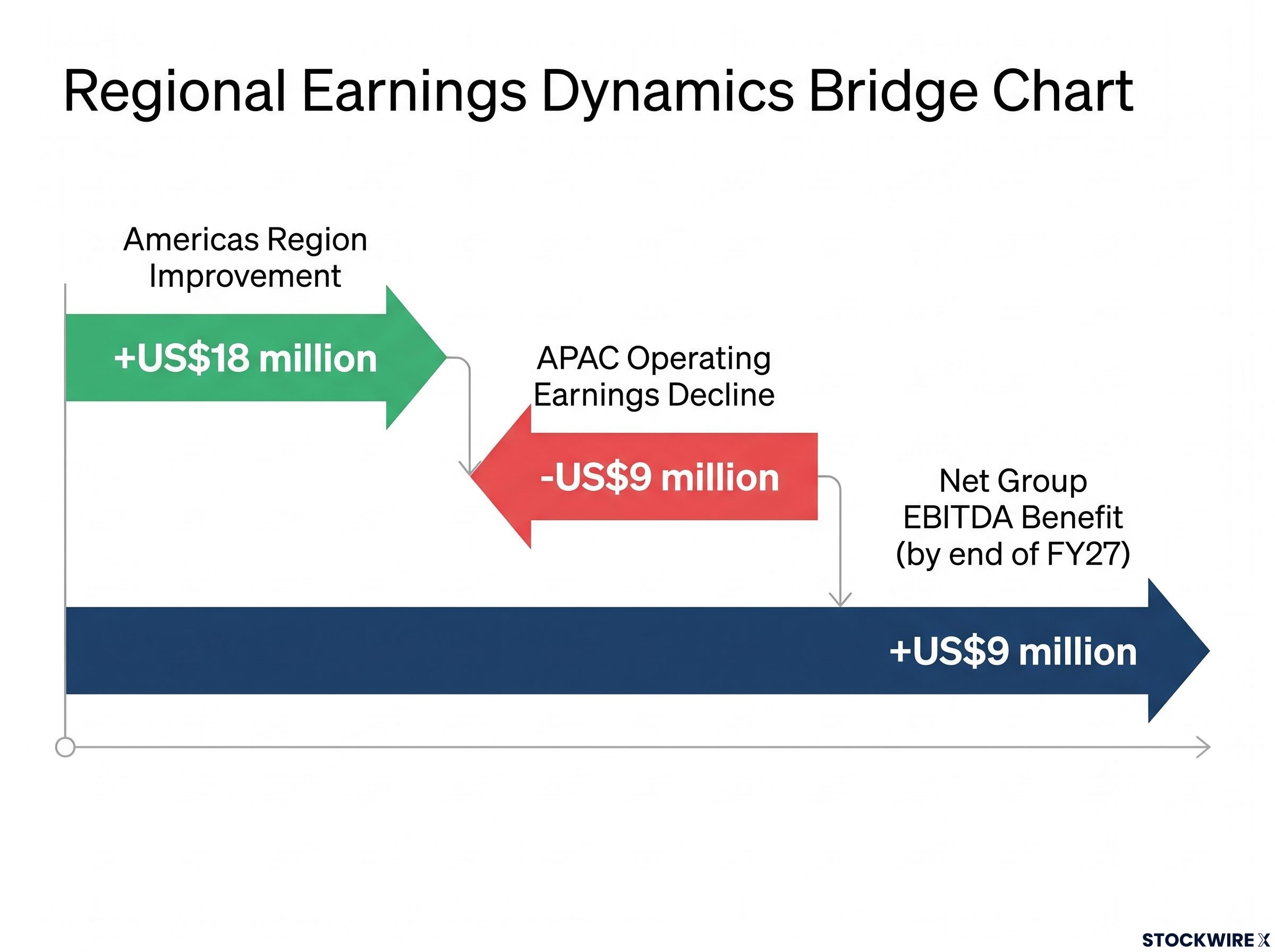

The decision to close Melbourne brass operations reflects a strategic shift towards third-party sourcing in Asia and automated production closer to North American end markets. RWC expects the changes to deliver a net US$9 million annual EBITDA benefit by the end of FY27, despite an estimated adverse US$9 million operating earnings impact on the APAC region.

The company will recognise a one-off net charge of US$100 million to US$110 million in FY26, which will be excluded from operating earnings. Approximately US$5 million represents the expected net cash outcome, with the remainder comprising non-cash write-downs and impairments.

From FY27, production will shift away from APAC, resulting in the region’s intercompany revenue declining substantially from approximately US$38 million recorded in FY25. These impacts are expected to be more than offset by lower costs in the Americas region, which anticipates an expected net annual benefit of US$18 million.

When big ASX news breaks, our subscribers know first

What is manufacturing footprint rationalisation?

Manufacturing footprint rationalisation involves consolidating production facilities to improve efficiency and reduce costs when production volumes at certain sites fall below economically viable levels. Companies typically undertake this process when shifting production closer to end markets or to lower-cost suppliers delivers superior economics.

In RWC’s case, the Melbourne brass operations have experienced sustained volume declines, making third-party sourcing and US-based production more cost-effective alternatives. The company has invested in automating assembly at its Alabama facility whilst transitioning APAC brass component sourcing to third-party vendors in Asia.

For shareholders, successful rationalisation means improved margins and earnings without requiring revenue growth. The strategy extracts more profit from existing operations by eliminating uneconomic capacity and optimising the geographic distribution of production.

Three factors driving the shift away from Australian brass production

The decline in brass volumes at Melbourne facilities reflects three structural drivers:

-

Alabama automation investment — RWC has automated assembly of SharkBite Max brass push-to-connect fittings in the USA, enabling production closer to North American end markets and significantly reducing volumes sourced from Australia.

-

Design efficiency gains — The SharkBite Max design achieves a 20% reduction in the amount of brass per fitting compared to previous designs.

-

APAC sourcing transition — In 2025, RWC transitioned from manufacturing brass SharkBite PTC components in Melbourne for the APAC region to sourcing from third-party vendors in Asia.

Looking ahead, RWC expects its overall brass requirements to decline further as it progresses its strategy to replace brass with stainless steel across key product ranges.

Financial impact breakdown

The restructuring will result in a one-off charge in FY26 and recurring annual benefits from FY27 onwards. The FY26 charge will be excluded from operating earnings, preserving the company’s reported underlying performance.

| Item | Amount (US$) | Cash/Non-cash | Timing |

|---|---|---|---|

| Redundancies & property exit costs | ~$5 million | FY26 | |

| Net tangible asset write-down (including inventory) | ~$25 million | Non-cash | FY26 |

| Intangible asset impairment (including goodwill) | $70 million-$80 million | Non-cash | FY26 |

| Total one-off charge | $100 million-$110 million | ~$5 million net cash | FY26 |

The ongoing impact from FY27 includes:

- APAC intercompany revenue decline: From approximately US$38 million in FY25 to substantially lower levels

- APAC operating earnings impact: Estimated adverse US$9 million

- Americas region benefit: Expected US$18 million annual improvement

- Net group EBITDA benefit: Approximately US$9 million annually by end of FY27

Regional earnings dynamics explained

The US$9 million net benefit reflects a US$18 million improvement in the Americas region, partially offset by a US$9 million decline in APAC operating earnings. The Americas benefits reflect more favourable economics of third-party sourcing plus reduced US tariff exposure under the revised supply chain.

This represents a deliberate rebalancing of where earnings are generated within the group. Production closer to end markets in North America reduces logistics costs and currency translation complexity whilst improving the company’s competitive positioning.

For investors, the restructuring addresses US tariff exposure, a relevant consideration given ongoing trade policy considerations. The shift towards third-party sourcing in Asia for APAC markets and automated domestic production in North America for that region optimises the cost base whilst reducing exposure to cross-border trade friction.

The RWC FY26 tariff outlook has improved alongside this restructuring, with tariff costs now tracking at the lower end of the previously flagged US$25-30 million range after nine months of trading to March 2026.

Employee consultation underway

Approximately 85 employees are expected to be affected by the closure of brass manufacturing operations in Australia. RWC has commenced consultation with impacted employees and anticipates this process to be completed during July 2026.

The next major ASX story will hit our subscribers first

Strategic context for investors

The announcement positions within RWC’s broader manufacturing evolution involving both geographic transition (Melbourne to Alabama and Asia) and material transition (brass to stainless steel across key product ranges). The dual transition delivers structural margin improvement without requiring top-line growth.

Key Financial Outcome

Net annual EBITDA benefit of approximately US$9 million expected by end of FY27

The US$9 million annual EBITDA uplift represents recurring margin improvement that compounds over time. Mostly non-cash one-off charges preserve balance sheet cash position, with only approximately US$5 million net cash outcome required to execute the restructuring.

Reduced US tariff exposure strengthens competitive positioning in the key North American market, whilst the shift to third-party sourcing in Asia for APAC markets optimises the cost base for that region. The restructuring extracts more profit from existing operations by eliminating uneconomic capacity and aligning production geography with end market demand.

Don’t Miss the Next Manufacturing Breakthrough

Join 20,000+ investors getting FREE breaking ASX news delivered to your inbox within minutes of release, complete with in-depth analysis. Click the “Free Alerts” button at StockWire X to receive market-moving announcements the moment they drop, analysed and ready to act on.