Kip McGrath revises FY26 guidance as softer trading prompts strategic reset

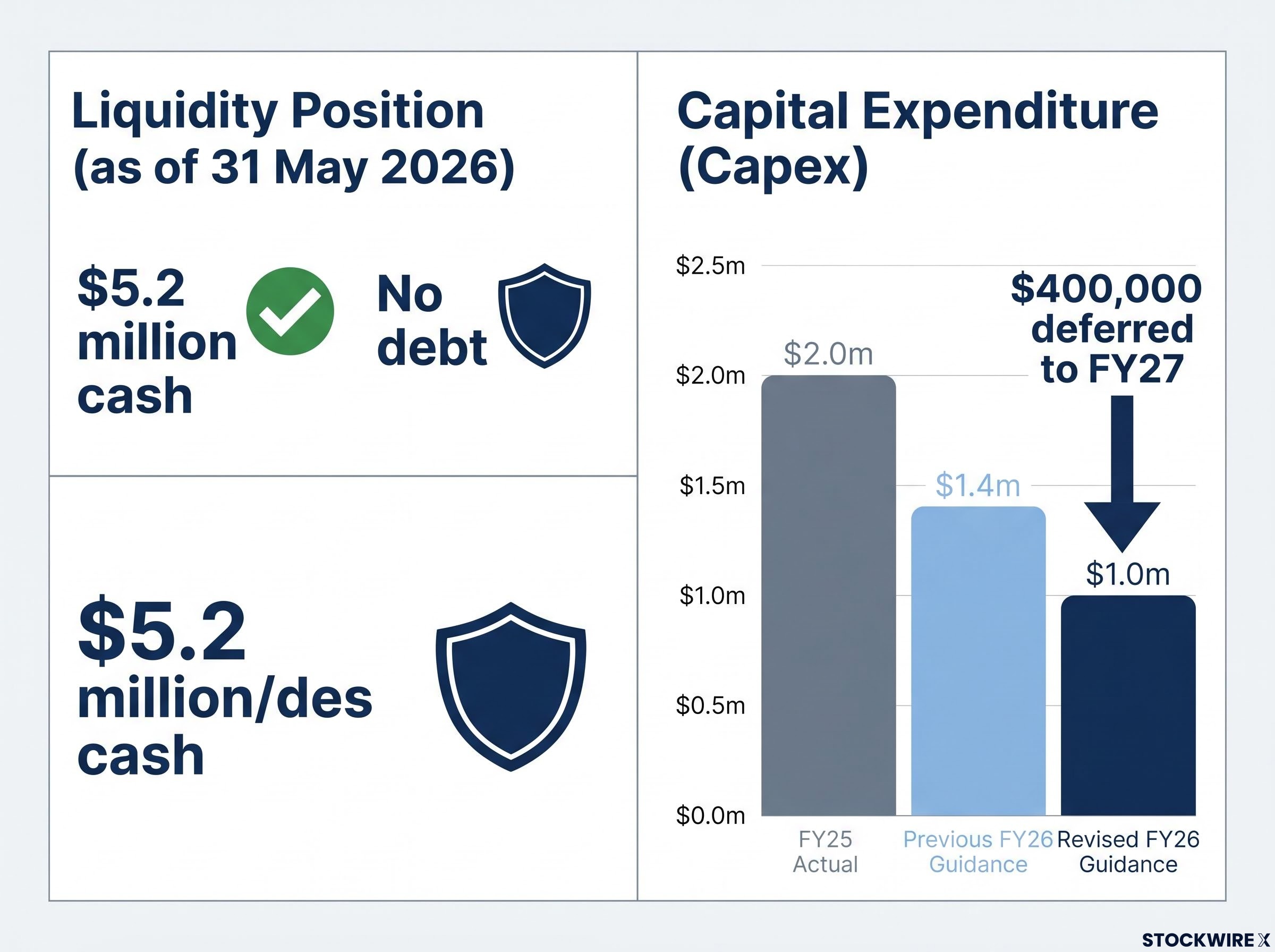

Kip McGrath Education Centres has revised its FY26 guidance downward following a trading review to end of May 2026, with revenue performance softer than anticipated in the second half. The education franchisor reported that increased lesson prices have not fully offset lower lesson volumes during H2, prompting management to adjust expectations for the full year. Despite the near-term headwinds, the company maintains a strong balance sheet with $5.2 million cash at 31 May 2026 and no debt, positioning it to navigate the softer trading environment whilst investing in strategic initiatives targeting franchisee experience and network health.

The company has deferred $400,000 of capital investment to FY27 as part of a disciplined approach to cash management. Management is using this period to reset the franchisee network and implement a range of operational improvements informed by feedback from franchisees, signalling a focus on long-term sustainability over short-term metrics.

When big ASX news breaks, our subscribers know first

What the revised guidance means for FY26

The guidance revision reflects both operational headwinds and currency translation impacts, with a strong Australian dollar compressing reported earnings from UK and New Zealand operations. Revenue from continuing operations is now expected to decline mid-single digits in Australian dollar terms, down from the previous guidance of flat performance. On a constant currency basis, the decline moderates to low-single digits, highlighting the material impact of foreign exchange movements on reported results.

| Metric | FY25 Actual | Previous Guidance | Revised Guidance |

|---|---|---|---|

| Revenue from continuing operations (AUD) | **$31,414k** | Flat | Mid-single digit decrease |

| Total expenses (AUD) | **$28,403k** | Low-single digit decrease | Mid-single digit decrease |

| NPAT (AUD) | **$2,287k** | Not provided | Low-single digit decrease |

| NPAT Underlying (AUD) | **$2,812k** | Early-double digit increase | Low-double digit decrease |

| Capex | **$2.0m** | **$1.4m** | **$1.0m** |

Underlying NPAT has shifted from an anticipated early-double digit increase (AUD) or mid-single digit increase (constant currency) to a low-double digit decrease (AUD) or mid-single digit decrease (constant currency), reinforcing the significant role currency translation has played in the earnings revision. Total expenses are now expected to decline mid-single digits, demonstrating management’s focus on cost discipline to partially cushion the earnings impact. The $1.0 million reduction in planned capex preserves cash for operational flexibility whilst deferring non-critical investments to FY27.

KME’s H1 FY26 results had shown the franchise model delivering meaningful operating leverage, with underlying NPAT growing 15.4% against modest revenue growth and the franchise fee percentage improving to 18.1%, making the H2 deterioration in lesson volumes a sharper reversal than the first-half trajectory suggested.

Understanding education franchise economics

Education franchise businesses generate revenue primarily through franchisee royalties tied to both lesson volumes and pricing. Lesson numbers drive franchisee profitability and, by extension, the franchisor’s royalty income stream. When lesson volumes decline, franchisees earn less, which directly reduces the royalty payments flowing to the franchisor.

Price increases can offset volume declines to a degree, but pricing power has limits in discretionary education services. Families reduce tutoring spend when household budgets tighten, making lesson volumes a lead indicator of network health. The price versus volume dynamic is particularly sensitive in periods of reduced consumer confidence, where demand elasticity increases.

Currency exposure adds a further layer of complexity for KME. International operations in the UK and New Zealand create foreign exchange translation risk when the Australian dollar strengthens, as overseas earnings translate to fewer Australian dollars when reported. Investors evaluating KME should monitor lesson numbers as the primary indicator of network health, with pricing power as a secondary lever that can support revenue but cannot fully compensate for sustained volume weakness.

Network stabilisation offers a forward signal

Centre count movements during the five months to 31 May 2026 suggest the network is stabilising following a period of rationalisation. The company reported 6 new centres opened, 7 centres resold or transferred, and 8 centres closed as management resets the franchisee network.

- 6 new centres opened

- 7 centres resold or transferred

- 8 centres closed (network reset)

The net outcome indicates centre numbers have stabilised in H2, with closures representing intentional pruning of underperforming locations rather than widespread franchisee distress. Management framed the closures as part of a deliberate network reset, suggesting a focus on quality over quantity.

A stabilising centre count is a positive signal for investors. It suggests the worst of the network rationalisation may be behind the company, creating a cleaner base from which to rebuild franchisee confidence and lesson volumes in FY27. New centre openings and resales demonstrate that some franchisees remain willing to invest in the network, indicating pockets of confidence despite the challenging macro environment.

Strategic initiatives targeting franchisee experience

CEO Melinda Smith has restructured the business during H2, with initiatives informed by direct feedback from the franchisee network. The focus areas include enhancing the franchisee experience, supporting network performance, and strengthening the operating model. Management has prioritised these investments despite the softer trading environment, using tightly controlled operating expenses to fund the initiatives whilst maintaining profitability.

Melinda Smith, CEO, Kip McGrath

“I am optimistic about the future of the business. The improvements we are making to enhance the franchisee experience, support network performance and strengthen our operating model are laying the foundations for sustainable long-term growth. We remain focused on delivering strong educational outcomes for our students and families while creating value for our franchisees and shareholders.”

Franchisee satisfaction is a leading indicator for network growth. Dissatisfied franchisees exit the system or reduce investment, whilst satisfied franchisees expand their operations and attract new entrants through positive word-of-mouth. The restructuring signals management’s recognition that franchisee support is critical to reversing the lesson volume declines experienced in H2.

Macro headwinds behind the demand softness

Reduced consumer confidence, driven by ongoing economic uncertainty and global events, has impacted demand for tutoring services during the second half. This macro headwind specifically affected lesson numbers, which declined versus the prior corresponding period despite price increases. The company noted that consumer discretionary spending has tightened, with families reducing non-essential education services when household budgets come under pressure.

Tutoring demand is discretionary and tends to recover as consumer confidence improves. Unlike structural threats such as new competitors or technology disruption, the current weakness reflects a cyclical demand issue tied to broader economic conditions. Lesson numbers can rebound when household finances stabilise and parents regain confidence in their ability to fund supplementary education. This is a macro timing issue rather than a competitive threat to KME’s market position.

Investment outlook and what to watch

Kip McGrath maintains a strong balance sheet with $5.2 million cash and no debt, providing flexibility to navigate the softer trading environment whilst continuing to invest in strategic initiatives. The company has demonstrated cost discipline by reducing expected capex from the previously guided $1.4 million to $1.0 million, preserving cash for operational priorities and deferring non-critical investments to FY27.

FY27 will be the critical year for investors to assess whether the strategic initiatives implemented during H2 FY26 are delivering results. Evidence of lesson volume stabilisation, franchisee confidence returning, and operating leverage as the network scales will be key indicators of success. Investors should monitor the following metrics:

- Lesson number trends — lead indicator of network demand

- Centre count stability — signal of franchisee confidence

- FY27 capex deployment — evidence of reinvestment when conditions improve

- Currency movements — AUD strength/weakness impacts reported earnings

The company is preserving optionality through cost discipline whilst investing in network fundamentals. This defensive posture positions KME for recovery when macro conditions ease, with the debt-free balance sheet providing runway to execute the franchisee experience improvements without financial pressure. The revised guidance reflects a realistic assessment of near-term headwinds, whilst management’s continued investment in strategic initiatives signals confidence in the long-term structural opportunity.

Don’t Miss the Next Consumer Discretionary Mover

Join 20,000+ investors receiving FREE breaking ASX news within minutes of release, complete with in-depth analysis. Get real-time alerts covering Tech, Healthcare, Finance, Consumer, and more sectors. Click the “Free Alerts” button at Big News Blast to start receiving expert coverage the moment market-moving announcements drop.