Metcash Maps Path to Margin Recovery as Food Growth Offsets Hardware Weakness

Metcash delivers resilient FY26 results as Food and Liquor offset Hardware headwinds

In its FY26 Full Year Results Presentation, Metcash outlined a year of resilient performance anchored by the strength of its Food and Liquor divisions, which successfully offset ongoing headwinds in the Trade hardware market. Group revenue reached $19.6 billion (+0.7%, or +3.8% excluding tobacco), while Group EBIT came in at $503.7 million (down 0.8%, but up 1.6% excluding one-off strategy and integration costs). Operating cashflow strength remained a standout feature, delivering $558 million (+3.5%), while the company declared a total dividend of 18.0 cents per share (fully franked), representing approximately 74% of underlying profit after tax. The debt leverage ratio stood at 1.0x, at the low end of the target range (1.0x–1.75x).

Management’s presentation framed the year as one of disciplined execution against a challenging backdrop. The resilience of the Food pillar, which grew earnings by 5.4% despite a $535 million decline in tobacco sales, demonstrated the strategic value of the supermarket franchise and the Foodservice & Convenience diversification. Liquor extended its market share gains for the seventh consecutive year, while Hardware & Tools showed improving sales momentum in the second half despite weak Trade conditions.

When big ASX news breaks, our subscribers know first

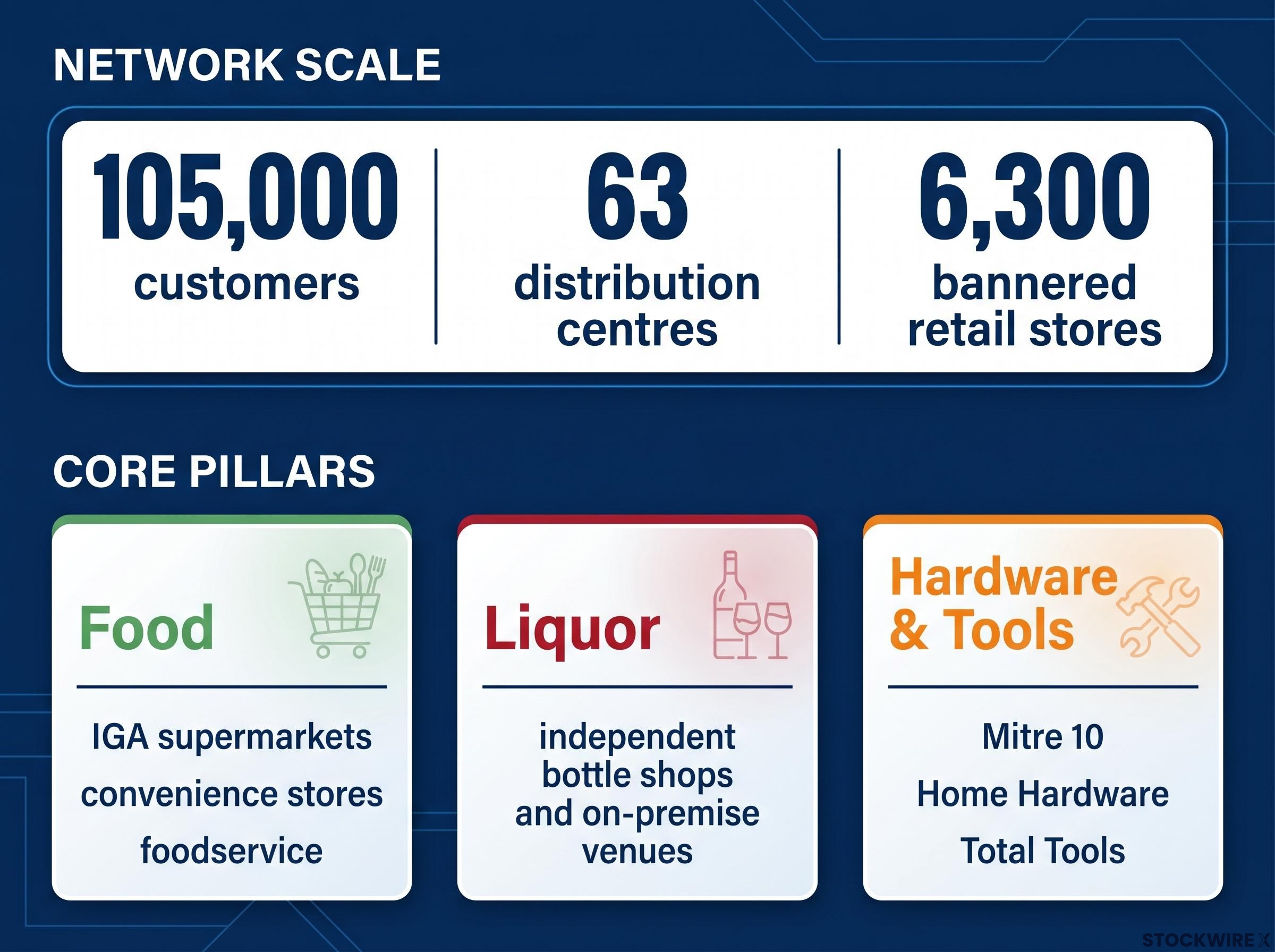

What is Metcash’s business model?

Metcash is Australia’s leading wholesaler and distributor to independent retailers across three core pillars: Food (IGA supermarkets, convenience stores, foodservice), Liquor (independent bottle shops and on-premise venues), and Hardware & Tools (Mitre 10, Home Hardware, Total Tools). The company serves approximately 105,000 customers, operates 63 distribution centres, and supplies around 6,300 bannered retail stores. The business operates on a “flywheel” model, providing procurement, logistics, marketing, digital solutions, and business services that independents could not achieve alone, creating scale and capability that individual retailers lack.

This wholesale-to-independent model creates a sustainable competitive moat. Metcash earns margins on distribution regardless of which independent ultimately wins the consumer sale, making the earnings base more resilient than pure retailers. The platform’s differentiated capabilities — from supply chain and inventory management to retail media and digital marketplaces — reinforce network strength and customer stickiness. The company’s strategy centres on delivering unique, differentiated value to independents, extending through the value chain for growth and resilience, and leveraging the platform for disciplined M&A.

Food pillar grows earnings 5.4% despite tobacco headwinds

The Food pillar increased EBIT to $261.8 million (+5.4%), with total Food revenue (including charge-through) reaching $10.54 billion. Excluding tobacco, Food revenue grew 5.4% (or 3.8% on an adjusted basis including Superior Foods for the full comparative period). The Foodservice & Convenience segment delivered EBIT of $54.5 million, up from just $12 million in FY22, underscoring the strategic value of this diversification.

The tobacco impact remained material but slowed in the second half. Sales declined 29% to $1.31 billion, driven by continued competition from illicit sources. However, the rate of decline improved markedly in Queensland, where regulatory enforcement strengthened, with sales growing approximately 3% in H2 compared to declines of around 30% in other states. The company acquired its first supermarkets in Q4 FY26 (Goolwa and Naracoorte in South Australia), with a long-term target to own 25–30% of IGA network revenue.

| Metric | FY26 | FY25 | Change |

|---|---|---|---|

| Food EBIT | $261.8m | $248.4m | +5.4% |

| Supermarkets EBIT | $207.3m | $194.2m | +6.7% |

| Foodservice & Convenience EBIT | $54.5m | $54.2m | +0.6% |

| Tobacco Sales | $1,308.7m | $1,844.0m | -29.0% |

The Food pillar’s earnings growth despite tobacco sales declining 29% to $1.31 billion demonstrates the resilience of the supermarket franchise and the strategic value of the Foodservice & Convenience diversification. Management highlighted that the Foodservice & Convenience business now represents 10.1% of group earnings, up from 3.2% in FY20, reflecting successful execution of the extension strategy through the value chain.

IGA pricing reaches most competitive position on record

The price gap between large IGA stores and chains narrowed to 2.1% (from 3.4% at end FY25), marking the most competitive position on record. Stores on the Extra Specials programme (121 stores, approximately 18% of revenue) are now just 1.2% above chain pricing, demonstrating the impact of targeted interventions in the most contested local markets. The improvement was driven by supplier support, enhanced promotional programmes, and retailer compliance. Approximately 390 top-selling private label products are now matched to chain equivalents.

Closing the price gap addresses the primary competitive disadvantage independents have historically faced against Coles and Woolworths. The narrowing differential supports network retention, drives sales growth, and strengthens the value proposition for IGA retailers operating in markets where price perception is a critical determinant of shopper choice. The presentation framed this as evidence that the IGA core network is “more price competitive than ever,” with the competitive positioning underpinning the resilience of supermarket earnings.

Liquor extends market share gains to 32.3%

The Liquor pillar delivered revenue of $5.37 billion (+1.0%), with EBIT of $100.1 million (down 3.8%). Management highlighted margin improvement in the second half, with the pillar returning to long-term average EBIT margins in H2. Market share reached 32.3% (up 1.3 percentage points year-on-year), extending a run of share gains since FY20 and reflecting the competitive strength of the independent liquor network and ALM’s distribution platform.

Key contract renewals representing over $500 million were secured, including Liquor Stax, ILR, Merivale, and Crown Casinos. Lion volume through ALM in Tasmania is targeted to commence in August 2026. The Liquor pillar’s multi-channel strategy — spanning retail bottle shops and on-premise venues — provides a hedge against shifts between retail and hospitality demand, while the platform’s scale and flexible supply chain support consistent share gains in a near-flat market.

Hardware & Tools shows sales momentum despite weak Trade market

Hardware & Tools revenue reached $3.71 billion (+4.3%), with EBIT of $177.3 million (down 6.3%). Normalised EBIT declined 2.7% excluding one-off costs. Sales momentum accelerated in H2 across both Hardware and Tools, with Total Tools retail sales growing 7.2%. Regional divergence was evident, with Queensland, South Australia, and Western Australia delivering Trade growth of +4.6% (like-for-like), while Victoria remained weak.

Management outlined a strategy reset targeting a return to mid-cycle margins: Hardware wholesale 2.7–3.0%, Hardware retail 3.0–4.0%, Tools retail 6.0–8.0%. The presentation detailed initiatives under four strategic pillars: Best Stores in Town (retail excellence and network formats), One Connected Network (shared scale and efficient support), Stronger Partnerships (exclusive brand growth and supplier alignment), and Trade’s Partner of Choice (improving Trade account loyalty through consistent, frictionless customer experience).

While earnings remain under pressure from the housing construction cycle, improving sales momentum and a clear strategy reset position the pillar for margin recovery as conditions normalise. The business added 17 Sapphire upgrades during the year, with like-for-like network sales accelerating in H2 (Hardware +6.3% vs +2.8% in H1, Tools +4.6% vs -0.9% in H1).

Technology investments position Metcash as AI-ready retailer

Program Horizon, the company’s ERP replacement initiative, has entered User Acceptance Testing, with first deployment planned for Q4 CY26. The Microsoft partnership includes over $3 million in co-investment, with the Microsoft Fabric AI platform targeted for deployment in end October 2026. Management highlighted the strategic value of transitioning to a modern, cloud-based ERP with embedded AI capability, positioning Metcash ahead of traditional wholesale competitors on technology.

“Our partnership with Metcash, built on the Horizon program initially, demonstrates what is possible when data and AI are embedded end-to-end across the full technology stack to drive enhanced customer experiences and operational impact. By scaling AI capabilities enterprise-wide, Metcash is accelerating decision-making and delivering measurable productivity gains throughout its business and retail network.”

— Judson Althoff, CEO of Microsoft’s Commercial Business

A modern, cloud-based ERP with embedded AI capability provides a platform for operational efficiency gains, including improved inventory health, reduction in Days Stock On Hand, better service levels, and AI-powered supply chain and operational intelligence. The evergreen cloud platform reduces legacy drag by avoiding major periodic upgrades, lowering future upgrade complexity and downtime risk. The initiative represents a foundational investment in competitive capability, enabling Metcash to leverage first-party data at scale and support the development of retail media and digital marketplace platforms.

Capital management supports growth and shareholder returns

Operating cashflow of $558 million supported a 3-year rolling cash realisation ratio of 104%, demonstrating strong cash conversion discipline. FY27 capex guidance of approximately $150 million (excluding M&A) represents a reduction from $175 million in FY26, reflecting moderated investment spend following prior-year M&A activity. The debt leverage ratio of 1.0x provides capacity for future M&A, while ROFE of approximately 20% reflects returns through the investment cycle. The dividend payout of 18.0 cents per share (fully franked) represents approximately 74% of underlying profit after tax, moderately above the target payout ratio of approximately 70%.

Strong cash conversion and a conservative balance sheet provide flexibility to pursue strategic acquisitions, including supermarket ownership, while maintaining consistent shareholder returns. The company retains undrawn debt facilities of approximately $967 million, with total committed debt facilities of $1.57 billion. Management noted that refinancing of syndicated facilities is underway, with strong lender demand. Average net debt during FY26 was $835 million, with weighted average cost of bank debt at 5.17% (inclusive of hedging), down from 5.65% in FY25.

The next major ASX story will hit our subscribers first

FY27 outlook shows steady start with June improvement

Group sales (excluding tobacco) are up 2.4% in the first seven weeks of FY27. Management noted May was subdued due to consumer sentiment weakness, but June trading recovered to FY26 growth levels. Hardware & Tools momentum is continuing, led by Total Tools growth of +9.5%. The Group’s cost-out programme is targeting approximately $25 million in annualised savings in FY27, supporting earnings resilience. The net earnings impact from completion of the accelerated tobacco excise programme is estimated at approximately $10 million.

Early FY27 trading suggests the resilience demonstrated in FY26 is continuing, with management initiatives supporting earnings despite macro headwinds. Food and Liquor experienced a subdued May as consumer sentiment softened in response to geopolitical uncertainty and cost-of-living pressures, but both pillars recovered in the first three weeks of June. Campbells & Convenience has cycled the Ampol contract win, with new tobacco contracts anticipated to benefit the balance of FY27. Hardware & Tools continues to deliver strong momentum, extending the improved H2 FY26 performance into early FY27, though market conditions are expected to remain challenging through the balance of FY27, with retail margins continuing to be under pressure.

Stay Ahead on Consumer Staples News

Join 20,000+ investors getting FREE breaking ASX news delivered to your inbox within minutes of release, complete with in-depth analysis. Click the “Free Alerts” button at StockWire X to receive real-time alerts the moment market-moving announcements drop across Consumer, Retail, and Food sectors.