Why a BoJ Rate Hike Hasn’t Stopped the Yen Carry Trade

4 hrs ago

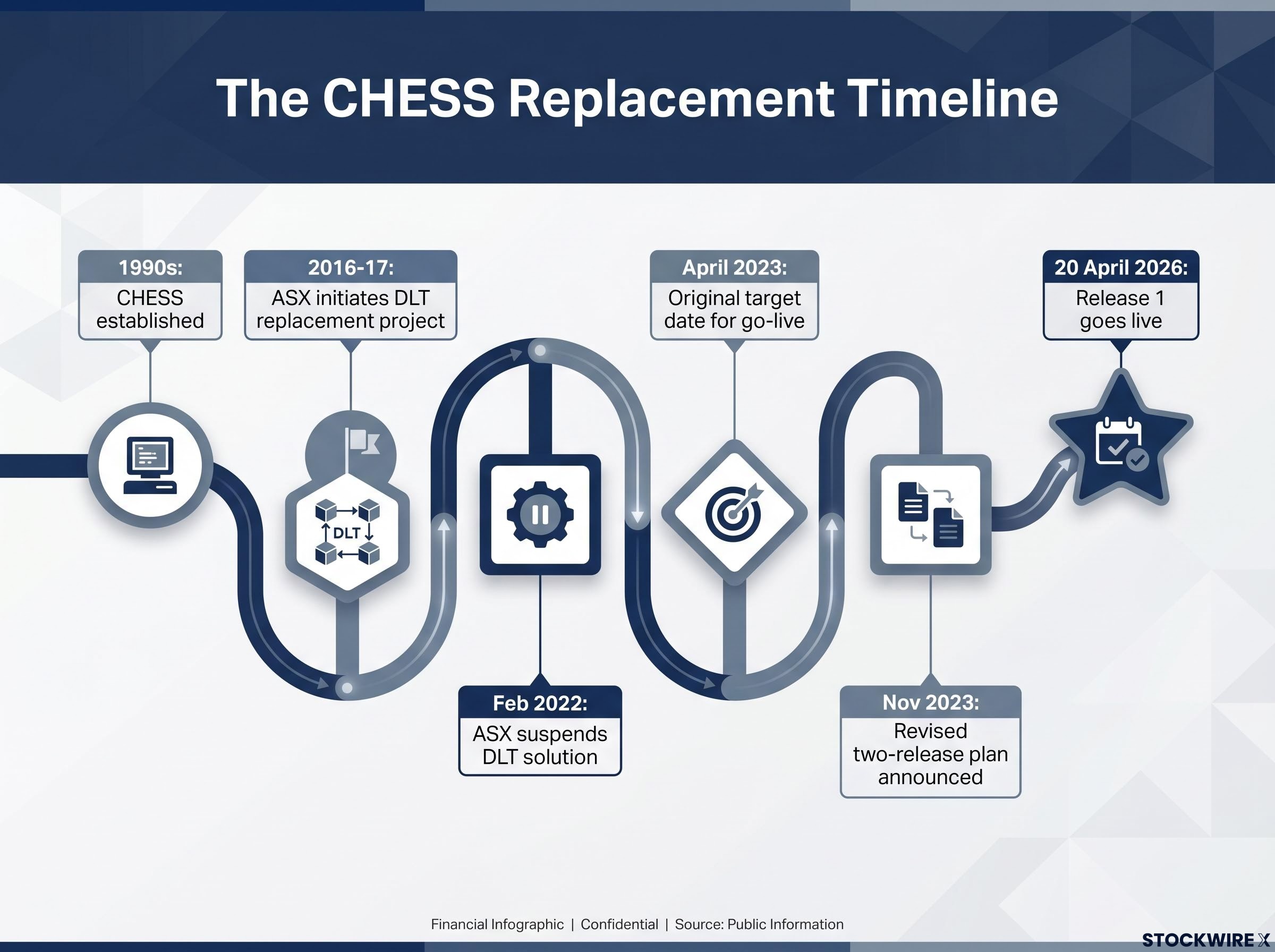

In February 2022, ASX suspended a technology programme that had consumed years of planning and hundreds of millions of dollars in industry preparation costs. The project was meant to replace the system through which every equity trade on the Australian market clears and settles. When the regulator responded, the focus extended well beyond a late delivery. The question was what ASX had told the market while the project was deteriorating, and whether those disclosures met the standard demanded of an entity whose operations sit at the centre of the financial system.

That question has now been answered, at least in part. Release 1 of the replacement system went live on 20 April 2026, but the disclosures made in the years before that milestone had already prompted formal regulatory action, governance commitments, and a public statement from ASIC Chair Sarah Court about the accuracy of information ASX provided during the project’s decline. What follows is an examination of the ASX disclosure obligations that apply to operators of systemically important infrastructure: why they differ from ordinary continuous disclosure, how a failure in those obligations cascades through the market, and how investors can apply those lessons when reading future communications from any operator of core market systems.

CHESS, the Clearing House Electronic Subregister System, is the system that clears and settles equity trades on ASX and maintains the official electronic subregister of ownership for listed securities. It sits at the centre of every equity transaction completed on the exchange, handling the transfer of legal title and the corresponding cash movements for millions of investors. Established in the 1990s, it is not a peripheral back-office tool. It is the circulatory system of the Australian equities market.

That distinction matters because replacing CHESS was never a matter of one organisation upgrading its own software. Brokers, custodians, registries, fund managers, and listed entities all connect to CHESS directly or indirectly. Any replacement forces the entire ecosystem to plan, build, test, and cut over in lockstep. Execution risk multiplies beyond what any single participant controls, and every public statement about the project’s timeline becomes a planning input for hundreds of separate organisations.

The replacement programme moved through a series of decisions, reversals, and restructurings over nearly a decade:

Release 2, covering settlement and subregister functions, remains to be delivered. The programme is not yet complete.

Under the Corporations Act, listed companies carry a continuous disclosure obligation: they must promptly disclose information that a reasonable person would expect to have a material effect on the price or value of their securities. The primary audience for this obligation is the company’s own shareholders and potential investors.

Investors looking to understand the legal framework that underpins these standards before examining the CHESS-specific obligations will find our dedicated guide to continuous disclosure obligations useful; it walks through the Corporations Act provisions, the point at which the obligation attaches, and the personal liability exposure that now applies to individual executives alongside the corporate entity.

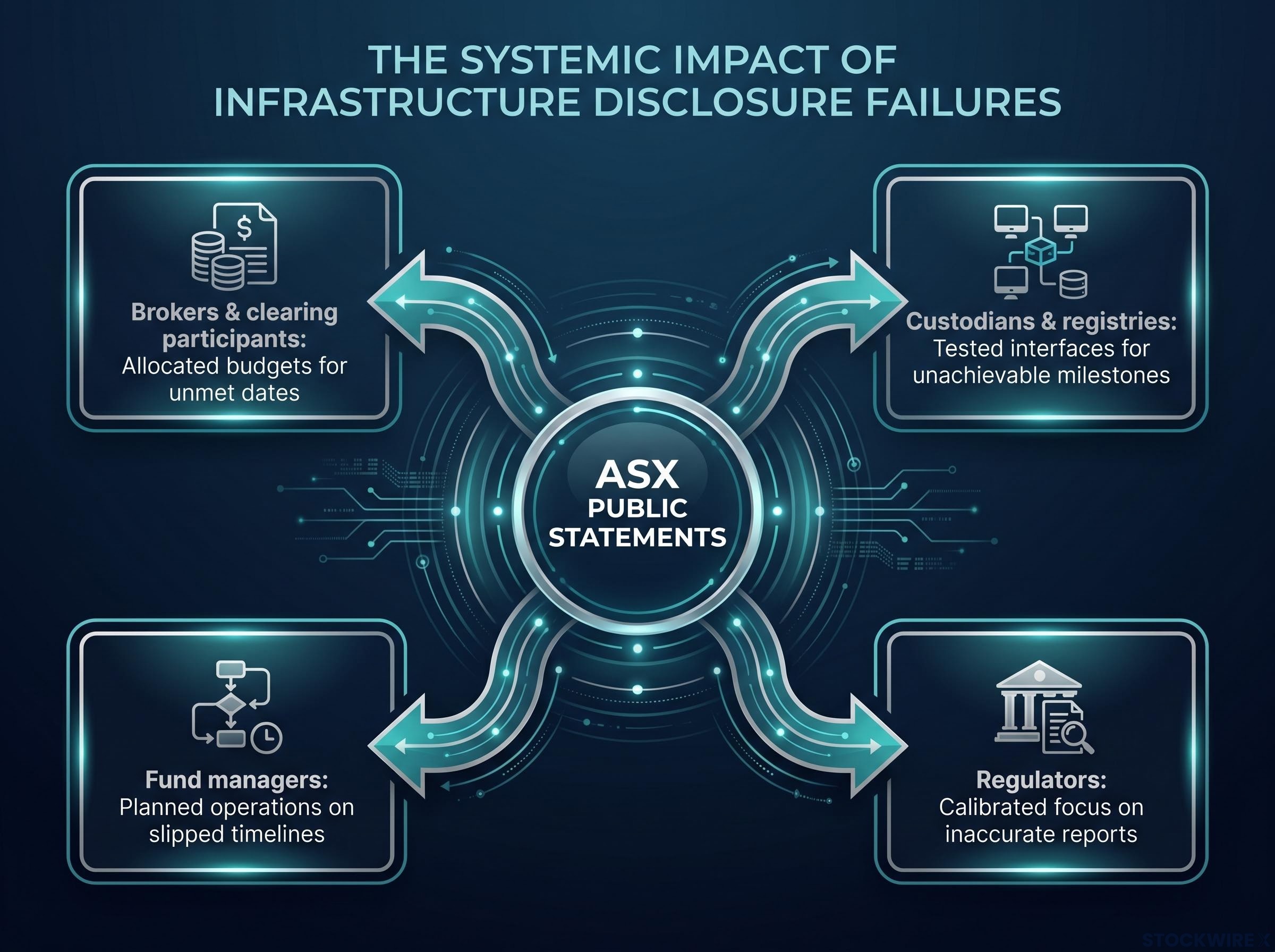

For entities operating systemically important financial market infrastructure, that framework is structurally insufficient. Their disclosures serve not only shareholders but every participant who operationally depends on their systems. When ASX publishes a timeline for CHESS replacement, it is not just informing equity investors. It is providing a planning input to every broker, custodian, registry, and fund manager that must build, test, and budget around that timeline.

ASX’s core clearing and settlement entities are explicitly recognised as systemically important financial market infrastructures under Australian law. They are jointly supervised by ASIC and the Reserve Bank of Australia (RBA) under the international Principles for Financial Market Infrastructures (PFMI), a framework that places explicit weight on transparency about risk, governance, and major projects so that participants and authorities can assess an infrastructure’s safety and efficiency.

ASIC has stated that entities operating critical market infrastructure carry a heightened obligation to provide timely and accurate public disclosures, a standard that goes beyond the ordinary continuous disclosure framework applied to listed companies.

| Dimension | Ordinary listed company | Critical market infrastructure operator |

|---|---|---|

| Primary audience served by disclosures | Shareholders and potential investors | Shareholders, clearing participants, custodians, registries, fund managers, regulators |

| Regulatory framework governing disclosure | Corporations Act continuous disclosure provisions | Corporations Act plus PFMI framework, jointly supervised by ASIC and RBA |

| Scope of harm from non-disclosure | Mispricing of the company’s own securities | Degraded planning across the financial ecosystem; systemic coordination failure |

| Examples | Most ASX-listed companies | ASX clearing and settlement entities; other recognised financial market infrastructures |

This two-tier structure is the conceptual foundation for understanding everything that followed in the CHESS saga. The standard that applies to ASX as an infrastructure operator is different in kind, not merely in degree.

ASIC’s financial market infrastructure reforms, which entered a consultation phase in April 2026, expanded the regulator’s licensing, supervisory, and enforcement powers over systemically important operators, giving formal regulatory weight to the heightened disclosure standard that the CHESS episode had already made visible in practice.

The regulatory concern was specific. ASIC identified that the information ASX provided to the market in the period leading up to the February 2022 suspension was misleading about the project’s actual status. ASX admitted its conduct regarding certain CHESS replacement disclosures was misleading. The problem was not merely that the project was late. It was that the market’s picture of the project’s health did not reflect what was happening inside it.

The CHESS settlement proceedings concluded with ASX agreeing to pay $20.5 million in penalties plus $3 million in ASIC legal costs, with ASX admitting to one contravention, the ‘progressing well’ representation, while ASIC dropped the remaining allegations.

That disconnect radiated outward through four categories of market participants, each of whom was making real operational decisions on the basis of ASX’s public statements:

ASIC Chair Sarah Court publicly stated that the admissions “relate to the accuracy of information provided to the market about a significant and complex project with real consequences for confidence, planning, and investment across the financial system.”

Capital and effort were sunk into integrations that could never be deployed on time. Necessary contingencies were delayed because stakeholders relied on overly optimistic or incomplete information. In this way, misleading disclosure by an infrastructure operator functions as a systemic coordination problem, not just a single-issuer breach. The harm is not limited to mispriced shares; it degrades the entire decision-making environment across the market.

Rather than pursuing immediate court-based enforcement, ASIC and the RBA obtained a package of governance and oversight commitments from ASX. This was a tailored supervisory response to identified structural weaknesses in how the CHESS replacement programme was governed and communicated.

These commitments typically involve four components:

The existence of such commitments signals that regulators identified specific structural deficiencies requiring remediation, not merely a generic need for improvement. They are not backward-looking penalties. They are active, operative constraints that reshape the framework within which future communications occur.

Any future statement from ASX about CHESS Release 2 must be interpreted against the existence of these commitments. If disclosures appear to lack the risk granularity that the commitments require, or if known challenges are absent from otherwise positive updates, that discrepancy itself is informative.

Release 1’s successful go-live on 20 April 2026 demonstrates that the revised governance framework can deliver a working system in live market conditions. That is a meaningful operational achievement. It does not, however, dissolve the heightened scrutiny applicable to Release 2, which covers the more participant-facing settlement and subregister functions. Regulators have stated that supervision of the CHESS replacement programme, including interoperability and operational resilience, will remain a focus.

The CEO transition at ASX, structured to follow the CHESS Release 1 go-live and precede the arrival of incoming CEO Anthony Attia in September 2026, adds an organisational dimension to the governance reset that investors should factor into their reading of future CHESS Release 2 communications.

The CHESS episode provides a template for evaluating disclosure from any operator of systemically important infrastructure. The following five questions target specific failure modes identified in the CHESS case. Infrastructure disclosures must pass two tests: the standard price-sensitivity test for shareholders, and a separate operational-planning test for the broader ecosystem. These questions address both.

Australia’s financial markets rely on a small number of infrastructures for which there are limited short-term substitutes. The stability and fairness of those markets depend on operators being forthright about project risks, delays, and failures, even when doing so is uncomfortable.

The CHESS saga reinforces a principle that extends well beyond a single programme.

The more systemically important an entity’s function, the higher the effective standard for accuracy, completeness, and timeliness of its disclosures, and the more consequential the gap when that standard is not met.

Release 1’s successful go-live on 20 April 2026 is a meaningful milestone that demonstrates the revised governance framework can deliver. It is not, however, a full resolution. CHESS Release 2, covering settlement and subregister functions, remains to be delivered. ASIC and RBA supervision of the programme, including interoperability and resilience, remains active.

ASX’s FY27 cost guidance, which prompted a 13.2% single-day share price fall on 26 May 2026, illustrated a direct financial consequence of the prolonged programme: a mandatory ASIC-driven spend cycle with capex set at A$180-200 million for FY27 alone, and Release 2 covering settlement functionality not targeted until 2029.

Investors and market participants should carry this framework into any future engagement with disclosures from operators of systemically important infrastructure, not just ASX, and not just clearing and settlement. The standard is commensurate with the trust and dependence the system places on them.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

ASX's clearing and settlement entities are jointly supervised by ASIC and the Reserve Bank of Australia under the Principles for Financial Market Infrastructures, which requires timely and accurate disclosures that go beyond the ordinary continuous disclosure framework applied to listed companies, serving not just shareholders but every broker, custodian, registry, and fund manager that depends operationally on ASX systems.

ASIC's proceedings concluded with ASX agreeing to pay $20.5 million in penalties plus $3 million in ASIC legal costs, with ASX admitting to one contravention relating to a 'progressing well' representation while ASIC dropped the remaining allegations.

CHESS (Clearing House Electronic Subregister System) is the system that clears and settles every equity trade on ASX and maintains the official electronic record of share ownership; replacing it affects every broker, custodian, registry, and fund manager in the Australian market, making any disclosure about the project's progress a critical planning input across the entire financial ecosystem.

Investors should check whether disclosures distinguish milestone achievements from overall project health, note what risks or challenges are absent from otherwise positive updates, confirm whether independent reviews have been commissioned and their findings shared, and assess whether the information provided would allow brokers and custodians to realistically plan their own operations.

Release 1 (the clearing component with FIX messaging for trade registration) went live on 20 April 2026, demonstrating the revised governance framework can deliver a working system, but Release 2 covering settlement and subregister functions remains to be delivered and is not targeted until 2029, with ASIC and RBA supervision of the programme still active.