Acrow Launches $70M Raise to Fund Dual Acquisitions and Cut Leverage to 1.5x

Acrow launches dual acquisitions with $70 million equity raising to accelerate growth strategy

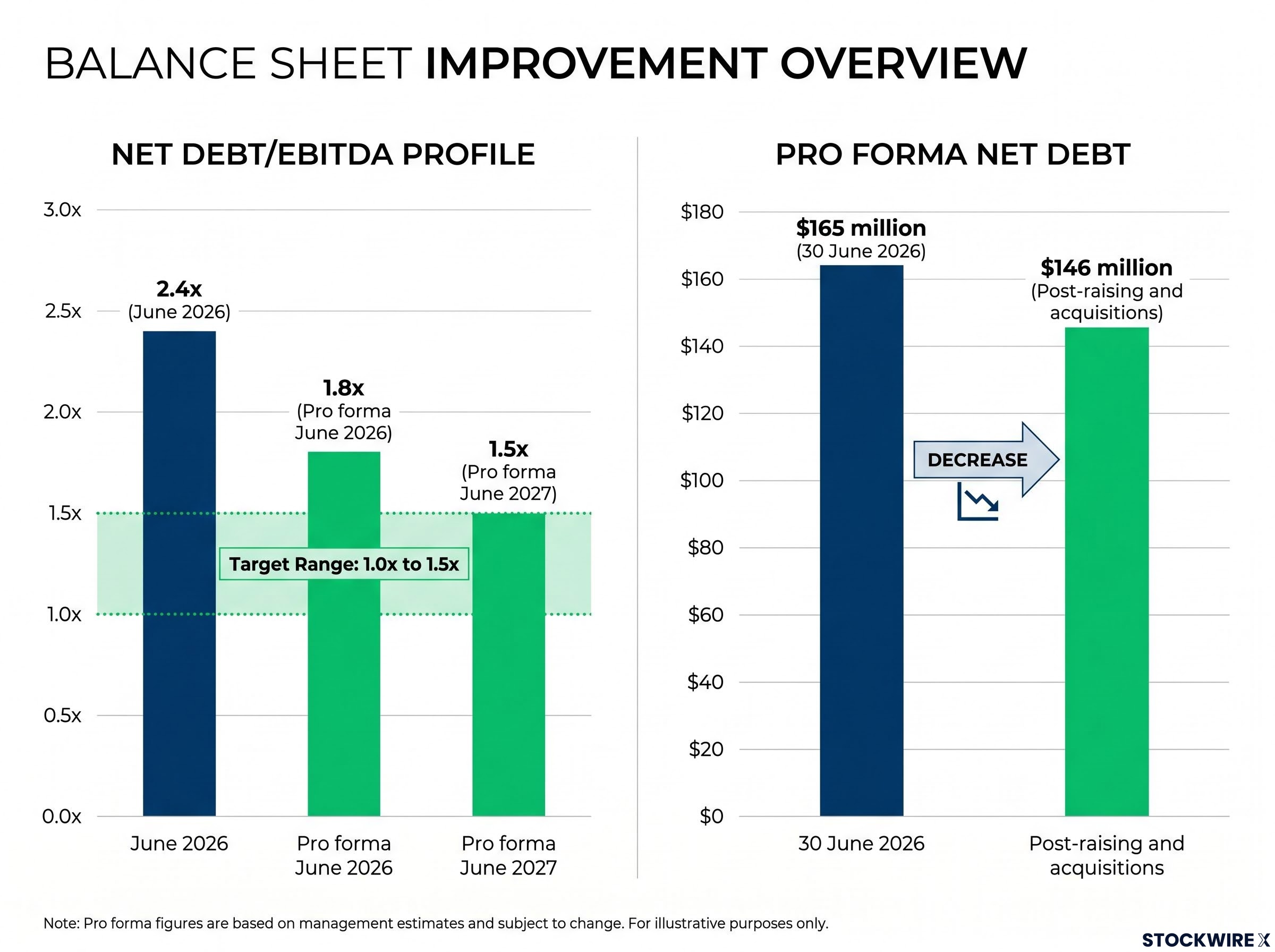

Acrow has entered binding agreements to acquire Ausgroup Industrial Services (AGIS) and the Preston SuperDeck® business for a combined enterprise value of $54.5 million. The acquisitions will be funded through a fully underwritten $70 million two-tranche placement at $0.85 per share, plus a Share Purchase Plan (SPP) to raise up to $10 million. The transactions expand both Acrow’s Industrial Access and Construction Services divisions while reducing pro forma net debt/EBITDA from 2.4x to 1.5x by FY27.

The AGIS acquisition is subject to approval from the Australian Competition and Consumer Commission (ACCC) under mandatory notification rules introduced 1 January 2026. Following the acquisitions, Acrow has increased FY27 revenue guidance to $405-425 million (up 21% on previous guidance midpoint) and EBITDA to $102-112 million (up 15%).

When big ASX news breaks, our subscribers know first

What the acquisitions bring to Acrow’s portfolio

Ausgroup Industrial Services (AGIS)

AGIS is a Queensland-based integrated industrial services provider servicing mining, ports, and energy sectors. The acquisition carries an enterprise value of $27.0 million plus $2.5 million capital expenditure, representing 4.1x EV/EBITDA based on estimated FY26 earnings, pre-synergies.

The consideration structure comprises $22.79 million upfront cash (77.1% of upfront consideration) plus $6.75 million scrip consideration via the issue of 7.9 million ACF shares at $0.8568, representing a 7% discount to the 15-day VWAP prior to announcement.

AGIS holds blue-chip client relationships including Anglo American, Glencore, BHP/BMA, and Dalrymple Bay Coal Terminal (a relationship maintained since 2006). The business is expected to contribute $40.0 million revenue and $6.5 million EBITDA in FY26. Management anticipates $1.25 million in synergies over 12 months, with an annualised uplift of $1.75 million from new capital expenditure returns and depot consolidation.

Preston SuperDeck®

Preston SuperDeck® is a market-leading retractable loading platform provider with 70%+ market share and approximately 900 decks (average lifespan 25 years). The acquisition carries an upfront cash consideration of $25.0 million, representing 4.0x EV/EBITDA based on estimated FY26 earnings, pre-synergies.

The business is expected to contribute $11.0 million revenue and $6.3 million EBITDA in FY26. Anticipated synergies of $1.25 million over 12 months are expected to arise from forward order book integration and depot consolidation. Loading platforms fill one of the few remaining product gaps in Acrow’s integrated construction services platform, enhancing the “one-stop-shop” value proposition to clients.

| Metric | AGIS | Preston SuperDeck® |

|---|---|---|

| Enterprise Value | $27.0m + $2.5m capex | $25.0m |

| EV/EBITDA Multiple | 4.1x | 4.0x |

| FY26 Revenue (est.) | $40.0m | $11.0m |

| FY26 EBITDA (est.) | $6.5m | $6.3m |

| 12-Month Synergies | $1.25m | $1.25m |

Understanding loading platforms and industrial access services

Retractable loading platforms are specialised platforms attached to buildings under construction that enable safe loading and unloading of materials at height. Preston SuperDeck®’s 70%+ market share positions the product as the industry benchmark, with 30+ years of expertise creating barriers to entry for competitors.

Industrial access services encompass scaffolding, engineering, protective coatings, and rigging solutions that support maintenance and shutdown activities in mining and energy infrastructure. These are not commodity services. They require specialised engineering, safety compliance, and long-term customer relationships.

Both acquisitions bring recurring revenue characteristics. Preston SuperDeck® operates a long-life installed base requiring ongoing hire and maintenance, while AGIS has entrenched relationships with blue-chip resources clients on multi-year contracts. This provides Acrow with visibility over revenue streams in both divisions.

Equity raising structure and use of proceeds

The $70 million fully underwritten two-tranche institutional placement is priced at $0.85 per share, representing a 6.6% discount to the last close of $0.91.

The tranches are structured as follows:

- Tranche 1: Approximately 39.0 million shares to raise $33.1 million (unconditional, using existing placement capacity under ASX Listing Rule 7.1).

- Tranche 2: Approximately 43.4 million shares to raise $36.9 million (conditional on shareholder approval at an EGM on or around Tuesday, 28 July 2026).

The SPP offers eligible shareholders the opportunity to subscribe for up to $30,000 per shareholder to raise up to $10 million. All SPP shares will be issued at the placement price, free of brokerage.

Funds raised will be allocated as follows: $47.79 million for acquisition consideration, $19.5 million for debt reduction and balance sheet flexibility, and $2.8 million for transaction costs.

ACCC Contingency

If the AGIS acquisition is not approved by the ACCC, excess funds raised will be allocated to further debt reduction. On a pro forma basis, net debt/EBITDA would reduce to 1.4x, within Acrow’s target range of 1.0x to 1.5x.

The funding structure positions Acrow to capture expected market growth from the civil infrastructure cycle and Olympic-related construction requirements in South-East Queensland.

Balance sheet transformation and FY27 outlook

Pro forma net debt decreases from $165 million (30 June 2026) to $146 million post-raising and acquisitions. Net debt/EBITDA reduces from 2.4x (June 2026) to 1.8x (pro forma June 2026) to 1.5x (pro forma June 2027), within Acrow’s target range of 1.0x to 1.5x.

Acrow has revised FY26 guidance: revenue $330-335 million, EBITDA $80-81 million (EBITDA now expected towards the lower end of the previous range). FY27 upgraded guidance (post-acquisitions): revenue $405-425 million, EBITDA $102-112 million.

Acrow’s hire revenue pipeline stood at $256 million as of late March 2026, up 34% on the prior corresponding period, a record level that framed the pre-acquisition FY27 baseline before the AGIS and Preston SuperDeck contributions were layered on top.

The company has confirmed a dividend policy targeting a payout ratio of 25% to 40% of underlying NPAT going forward. The acquisitions are expected to deliver mid single digit EPS accretion on a pro-forma basis.

Key FY27 metrics include:

- FY27 revenue uplift: 21% on previous guidance midpoint

- FY27 EBITDA uplift: 15% on previous guidance midpoint

- Acquisition contribution to FY27: $50 million revenue, $14 million EBITDA

The combination of earnings-accretive acquisitions and balance sheet deleveraging creates operational flexibility to pursue further growth opportunities in an expected infrastructure upcycle.

Acrow’s acquisition integration track record

Acrow has demonstrated a repeatable playbook for acquiring, integrating, and growing bolt-on businesses. Recent acquisitions and their revenue lift outcomes include:

- Natform (Aug 2018) – Screens – 300% revenue lift

- Uni-Span (Nov 2019) – Civil/Industrial Access – 250% revenue lift

- MI Scaffolding (Nov 2023) – Industrial Access – 25% revenue lift

- Benchmark (Feb 2024) – Industrial Access – 20% revenue lift

- Above Scaffold (May 2025) – Industrial Access – 28% revenue lift

- Brand (May 2025) – Industrial Access – 10% revenue lift

Acquisition metrics for AGIS and Preston SuperDeck® (4.0-4.1x EV/EBITDA) are in line with Acrow’s targeted approach and previous acquisition history. This consistency provides investors with confidence in the company’s execution capability and reduces integration risk.

Acrow’s acquisition integration track record has compounded across a multi-year program of bolt-on deals, with the company delivering 22% group revenue growth in H1 FY26 as earlier acquisitions including Above Scaffolding and Brand Australia performed ahead of initial expectations.

Key dates and shareholder participation

Key dates for the equity raising are as follows:

- Placement bookbuild: Thursday, 18 June 2026

- Tranche 1 allotment: Friday, 26 June 2026

- SPP opens: Monday, 29 June 2026

- SPP closes: Thursday, 16 July 2026

- EGM for Tranche 2 approval: Tuesday, 28 July 2026

- Tranche 2 allotment: Tuesday, 4 August 2026

SPP eligibility is determined by shareholders with a registered address in Australia and New Zealand as at the record date (Wednesday, 17 June 2026). Eligible shareholders may subscribe for up to $30,000 per shareholder at the offer price of $0.85, free of brokerage.

The next major ASX story will hit our subscribers first

Investment thesis: Positioning for the infrastructure cycle

The transaction package delivers a dual benefit: earnings accretion from acquisitions plus balance sheet capacity to capture organic growth. Acrow is positioned to capitalise on market tailwinds including civil infrastructure cycle uplift and Brisbane 2032 Olympics-related construction activity in South-East Queensland.

Following the transaction, Acrow’s shares on issue increase from 312.2 million to 402.4 million. Pro forma market capitalisation stands at $342.1 million (at offer price), with pro forma enterprise value of $487.6 million.

Strategic Balance Sheet

The strengthened balance sheet and expanded service offering position Acrow to capitalise on the expected infrastructure investment cycle. With pro forma net debt/EBITDA of 1.5x by FY27, the company maintains capacity to pursue further growth opportunities while delivering earnings accretion from the AGIS and Preston SuperDeck® acquisitions.

Want the Next Industrial Sector Breakout in Your Inbox?

Join 20,000+ investors receiving FREE breaking ASX news within minutes of release, complete with in-depth analysis. Click the “Free Alerts” button at Big News Blast to get industrial sector updates the moment market-moving announcements drop.