Why 2026 Market Volatility Feels Worse Than the Data Shows

1 hr ago

AI may prove one of the most consequential technologies in a generation. The companies building its foundations, however, could end up earning less from it than airlines earn from flying. That is the provocation at the centre of a research note published on 15 June 2026 by BCA Research Chief Global Strategist Peter Berezin, arriving at a moment when AI capital expenditure commitments have reached historic scale and per-token pricing is sliding. The timing sharpens the warning. What follows is a structured analytical lens for evaluating AI investment risks across the value chain, grounded in Berezin’s specific framework: where the airline analogy holds, where it breaks down, and what early signals investors can track in real time.

Berezin’s comparison is not casual. Airlines are capital-intensive businesses that sell a commoditised product, and most passengers default to price when choosing between carriers. Those two characteristics, extreme capex and interchangeable output, are what make the analogy precise rather than decorative.

The mechanism connecting it to AI model providers is the absence of social lock-in. Berezin draws a distinction that deserves quoting directly.

A platform like Instagram is used largely because others use it. That is a network effect. A model like ChatGPT is used because it is good. If something better or cheaper arrives, users switch.

That single observation reframes the competitive position of standalone model providers. There is no social graph binding users to a specific large language model. There is no content library they would lose by leaving. The switching cost is functionally zero.

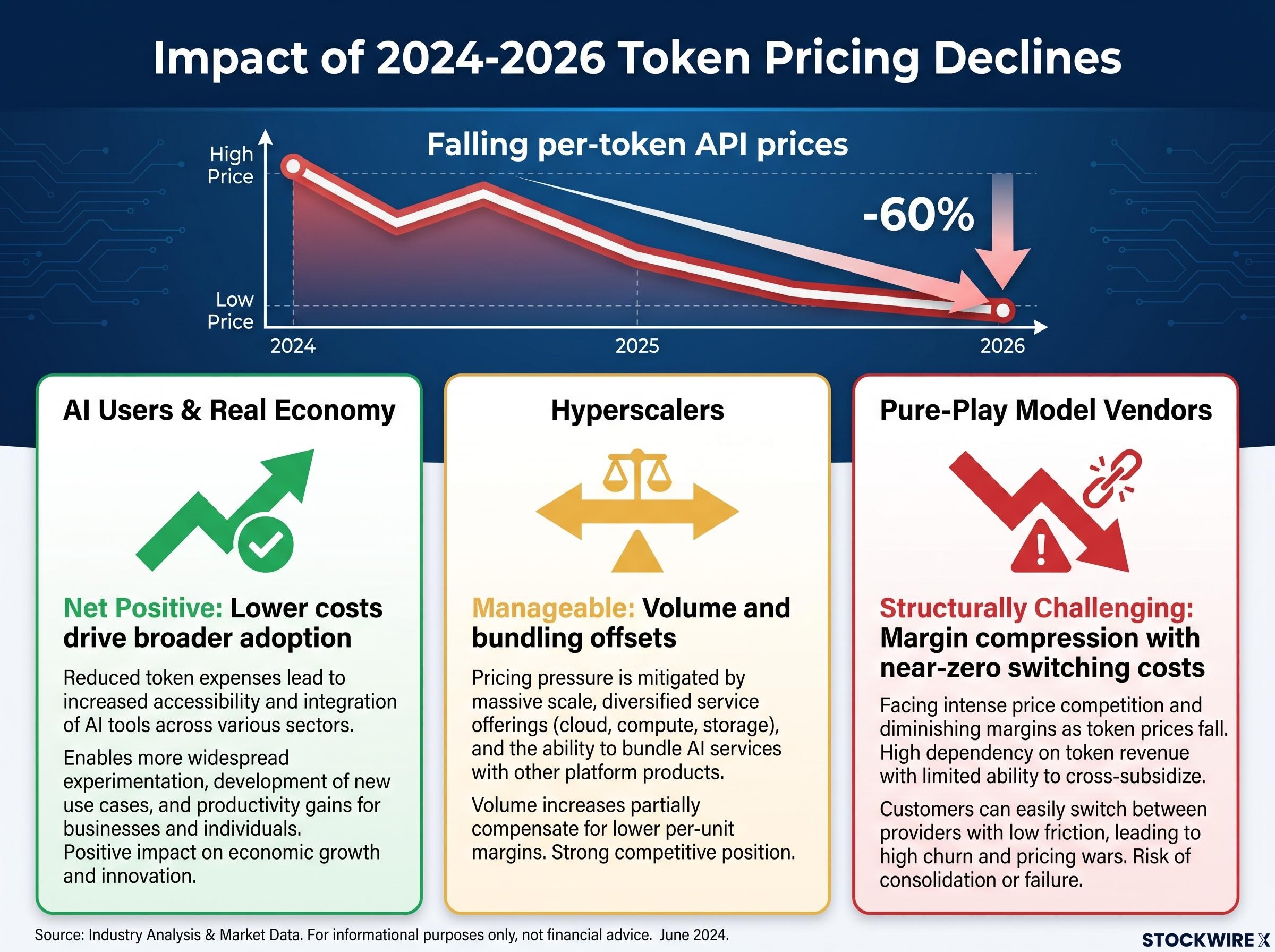

BCA’s 15 June 2026 note goes further, describing first-mover advantage in AI infrastructure as a “false premise.” Being first to build does not confer lasting pricing power if the product commoditises. Token prices had declined in the weeks preceding the note, with cost-sensitive users migrating away from premium frontier models. The pattern Berezin identified is not hypothetical; it is already visible.

The airline comparison is a precise instrument, but it cuts some layers of the AI value chain cleanly and leaves others untouched. Investors who apply it too broadly risk misclassifying defensible businesses as structurally challenged, or assuming hyperscaler bundling protects every AI investment regardless of economics.

| AI Stack Layer | Example Categories | Airline Analogy Strength | Key Moat Source | BCA Risk Assessment |

|---|---|---|---|---|

| Infrastructure (chips, data centres) | Semiconductor designers, fabricators | Moderate | Economies of scale, IP | Capital-intensive but scale advantages persist |

| Foundation model providers | Standalone API model vendors | Strong | Weak; output is interchangeable | Most exposed to commoditisation |

| Cloud and platform bundlers | Hyperscalers with integrated services | Weak | Migration costs, security, bundling | Volume offsets unit price compression |

| Application and workflow layer | Enterprise software with embedded AI | Very weak | Network effects, proprietary data, integration | Structurally defensible economics |

At the foundation model layer, the parallels are direct. Capital intensity is enormous. The output, a response to a prompt, is increasingly interchangeable to cost-conscious buyers. BCA has repeatedly warned that this layer faces overbuild-cycle dynamics, drawing explicit parallels to telecom fibre and dot-com infrastructure spending where the underlying technology proved valuable but early investors bore severe losses.

Airlines face large, inescapable marginal costs: fuel, crew, landing fees. AI inference costs, by contrast, can fall sharply as hardware and models improve. Software-like scalability means a trained model can serve orders of magnitude more queries without proportional cost increases.

BCA itself stresses that durable AI profits will accrue to companies with economies of scale, network effects, and proprietary technology. A dominant enterprise platform that weaves AI into mission-critical workflows and holds proprietary behavioural data has moat sources that airlines simply do not possess. The analogy, correctly applied, is a scalpel for the model layer, not a verdict on the entire stack.

Enterprise software pricing regimes are shifting faster than valuations reflect: AI-native entrants are undercutting incumbent SaaS costs by 80-90% through consumption-based models, and concrete enterprise case studies show companies cutting analytical software headcount from 20 seats to 3, a dynamic that reinforces why the application layer’s moat depends on workflow depth and proprietary data rather than seat counts or brand recognition.

Token pricing is not an abstraction. It is a publicly observable data series, and Berezin has identified it as an early warning indicator of monetisation pressure in the 15 June 2026 note. The pattern through 2024-2026 tells the story empirically: major providers have repeatedly cut API prices, and open-weight models have steadily eroded the pricing premium that closed models once commanded.

The mechanism is straightforward. As per-token prices fall, the revenue curve flattens while the capex curve remains steep. The widening gap between the two is where investor impatience accumulates.

What falling token prices mean, however, depends entirely on where an investor sits:

Berezin warned specifically that a continuation of the token pricing slide could reignite investor concern about the monetisation of large AI capital expenditures.

The AI business model fragility Berezin identifies is already visible in concrete corporate structures: Oracle’s record $638 billion backlog rests nearly half on a single OpenAI contract whose implied $60 billion annual compute obligation requires OpenAI’s current revenue to more than double, a counterparty dependency that Moody’s has flagged as a material risk and that open-source benchmark convergence makes structurally harder to sustain.

That warning gives investors a concrete surveillance tool. Token price trends do not require proprietary research access to track; they are visible in public API pricing pages and competitive benchmarking data.

BCA’s “Metaverse Moment” is not a prediction that AI technology fails. It is a named framework for a specific type of valuation event: the point at which investors punish companies for escalating capex before cash flows catch up, regardless of the underlying technology’s long-run utility.

The pattern has repeated across multiple infrastructure cycles. Telecom fibre buildouts in the late 1990s created genuine long-term economic value, yet early infrastructure investors absorbed catastrophic equity losses as valuations compressed years before utilisation caught up. BCA invokes these parallels deliberately, noting that the AI capex cycle, like all other capex cycles, will “end in tears.”

The metaverse-adjacent investment wave offered a more recent echo. Narrative outran monetisation, sentiment reversed, and companies that had committed billions saw sharp multiple contraction without the technology itself being disproven.

The scale of current AI infrastructure spending is historically unusual. BCA has observed that the AI boom has exerted less tangible real-economy impact than widely assumed, creating a gap between narrative and evidence that investor impatience could widen into a valuation event.

The conditions that BCA implies must align for a Metaverse Moment to materialise follow a specific sequence:

An AI company can be right about long-run economics and still suffer severe multiple contraction if its capex trajectory runs ahead of demonstrable cash flow.

For investors who want to pressure-test the Metaverse Moment thesis against multiple independent analytical lenses, our deep-dive into AI capex bubble frameworks examines how the Minsky financing stage model, Kindleberger’s speculative cycle, Sharma’s four O’s, and the Shiller CAPE ratio at 40.11 each reach different verdicts on whether current AI infrastructure spending has crossed into genuinely dangerous speculative territory.

BCA’s analysis translates into four investor-facing questions, each designed to interrogate a specific risk dimension rather than treat “AI exposure” as a monolithic category.

| Question | What to Look For | Red Flag Signal | Green Flag Signal |

|---|---|---|---|

| Durability of differentiation | Network effects, proprietary data, workflow integration | Standalone API with no switching costs | Deep integration into mission-critical enterprise workflows |

| Capex payback vs. Metaverse Moment timing | Ratio of AI capex to current AI-attributed revenue | Escalating capex with no visible cash flow inflection | Demonstrable revenue scaling alongside spend |

| Position in the AI stack | Layer-specific risk profile | Undifferentiated model provision layer | Application layer with proprietary data and network effects |

| Scenario humility | Range of outcomes considered in valuation | Single high-conviction point forecast | Explicit scenario analysis across bull and bear cases |

BCA’s analysis identifies three moat sources as the locus of durable AI profits:

Economic moat ratings provide a systematic way to operationalise the distinctions BCA’s framework implies: Morningstar’s mid-2026 analysis assigns wide moat status to Nvidia and Broadcom on the basis of CUDA switching costs and custom silicon lock-in respectively, while flagging Micron and Ciena as overvalued on thematic AI association alone, a classification that maps cleanly onto the foundation model layer versus infrastructure layer split Berezin draws.

McKinsey’s analysis of AI and network effects finds that capabilities embedded into core enterprise systems, combined with proprietary data feedback loops, generate switching costs that compound over time, precisely the moat dynamics BCA identifies as separating structurally defensible application-layer businesses from commoditised model providers.

Berezin has also acknowledged that BCA’s own MacroQuant model may be poorly suited to the current environment, described in the context of rapid policy shifts and potential structural breaks. If AI constitutes a genuine structural break from historical norms, the historical correlations underpinning quantitative macro frameworks may no longer serve as dependable predictive guides. That admission argues for scenario analysis over high-conviction point forecasts.

The airline analogy is not a verdict on AI’s future. It is a structural filter, and the question it poses is the one BCA has been building toward across months of research.

The question for investors is not whether AI is transformative. It is whether the companies building AI’s model layer will capture the value that transformation creates.

BCA’s position is that AI may drive significant productivity improvements and real income growth while the main equity beneficiaries are not today’s undifferentiated model providers. That is not a contradiction; it is a historical pattern that has played out across every major infrastructure cycle.

The conditions under which investors should have higher confidence in AI equity returns are specific: strong moats from network effects or proprietary data, deep workflow integration that raises switching costs, and capex profiles that are disciplined relative to demonstrable cash flow. Where those conditions are absent, the airline analogy applies with full force.

Token prices remain the canary Berezin has identified. If they continue declining without a volume or margin offset from bundled services, the warning has a clear empirical test. Investors who internalise this framework not as a prediction but as a filter will be better positioned to distinguish companies building durable economic franchises from those accumulating the conditions for a Metaverse Moment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The airline analogy, used by BCA Research's Peter Berezin, compares AI model providers to airlines because both are capital-intensive businesses selling a commoditised product with minimal customer switching costs; it matters because it suggests standalone model providers may struggle to earn lasting profits even as the underlying technology proves transformative.

Falling token prices signal that per-unit AI revenue is compressing while capital expenditure remains high, widening the gap between spending and returns; Berezin identifies continued token price declines as a key trigger that could reignite investor concern about the monetisation of large AI capital expenditures.

Foundation model providers offering standalone API access are most exposed, as their output is increasingly interchangeable and users face functionally zero switching costs, while application-layer businesses with proprietary data and deep enterprise workflow integration are considered structurally more defensible.

The Metaverse Moment, as defined by BCA Research, is the point at which investors punish AI companies for escalating capital expenditure before cash flows catch up, drawing parallels to the dot-com fibre overbuild and the metaverse investment wave where narrative outran monetisation and valuations compressed sharply.

BCA's framework suggests investors ask four questions: whether the company has durable differentiation through network effects or proprietary data; whether its capex is justified by demonstrable revenue scaling; which layer of the AI stack it occupies; and whether its valuation reflects a range of scenarios rather than a single high-conviction forecast.