Why 2026 Market Volatility Feels Worse Than the Data Shows

25 mins ago

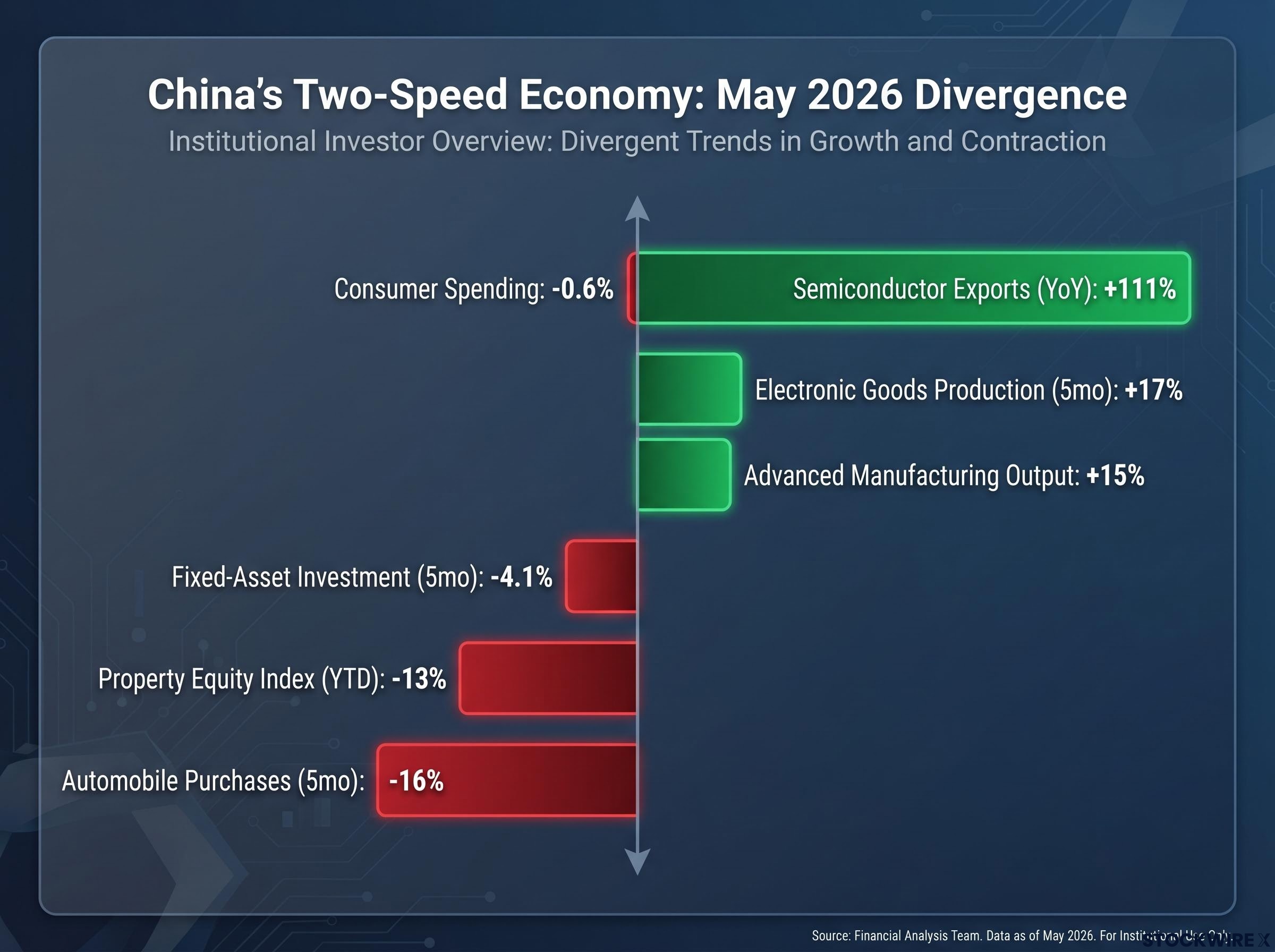

China’s semiconductor exports surged 111% year-on-year in May 2026, reaching approximately $36 billion. In the same month, domestic consumer spending contracted 0.6%, the first negative reading since pandemic restrictions ended in late 2022. These two data points belong to the same economy, but they describe different countries.

The divergence is not a temporary cyclical mismatch. As China’s property crisis enters its fifth consecutive year, Beijing has made a deliberate structural choice: channel capital toward advanced manufacturing, artificial intelligence, and electric vehicles rather than deploy traditional real estate bailouts. The result is a two-speed economy where headline export strength obscures a deepening domestic consumption freeze. For global investors, the implications extend well beyond Chinese equities. What follows is a framework to decompose Chinese market exposure by sector, identify the value traps embedded in property-linked assets, and map the capital rotation strategies that major institutions are deploying heading into the second half of 2026.

The numbers tell two stories that refuse to merge.

On the export side, semiconductor shipments contributed roughly half of China’s overall export growth in May, according to Chinese customs data reported via Bloomberg. Manufacturing output expanded to 4.5%, up from 4.1%, driven by a 15% increase in advanced manufacturing. Electronic goods production rose 17% over the first five months of the year. These are not marginal improvements; they represent a structural acceleration.

The domestic economy tells a different story entirely. Fixed-asset investment fell 4.1% over the same five-month period, with non-government investment dropping a steeper 7.1%. Automobile purchases declined 16%. Appliance and building material sales posted double-digit percentage declines. The consumers and private enterprises that once powered China’s internal demand are pulling back.

This divergence is not an accident. Beijing’s “new quality productive forces” agenda actively redirects state capital toward high-technology sectors while allowing the property and construction complex to contract. The policy logic is coherent, but the economic consequence is an economy where aggregate figures are increasingly meaningless as an investment signal.

| Sector | Key Metric | May 2026 Performance | Institutional Sentiment |

|---|---|---|---|

| Semiconductors | Export value (YoY) | +111% | Selective overweight (JPMorgan) |

| Advanced manufacturing | Output growth | +15% | Positive, hedged for geopolitical risk |

| Property | Sector equity index (YTD) | -13% | Underweight (consensus) |

| Consumer spending | Annual growth | -0.6% | Cautious (Citi, BofA) |

Broad China index investing, in this environment, blends a booming export sector with a contracting domestic market into a single misleading number. Sector decomposition is no longer optional.

The divergence between China’s technology export boom and its domestic consumption contraction is one expression of a broader regime shift: mercantilist capital flows directed by state policy rather than market signals are reshaping which sectors accumulate capital across the US, EU, China, and India simultaneously, demanding a fundamental rethink of how portfolios are constructed around country-level macro assumptions.

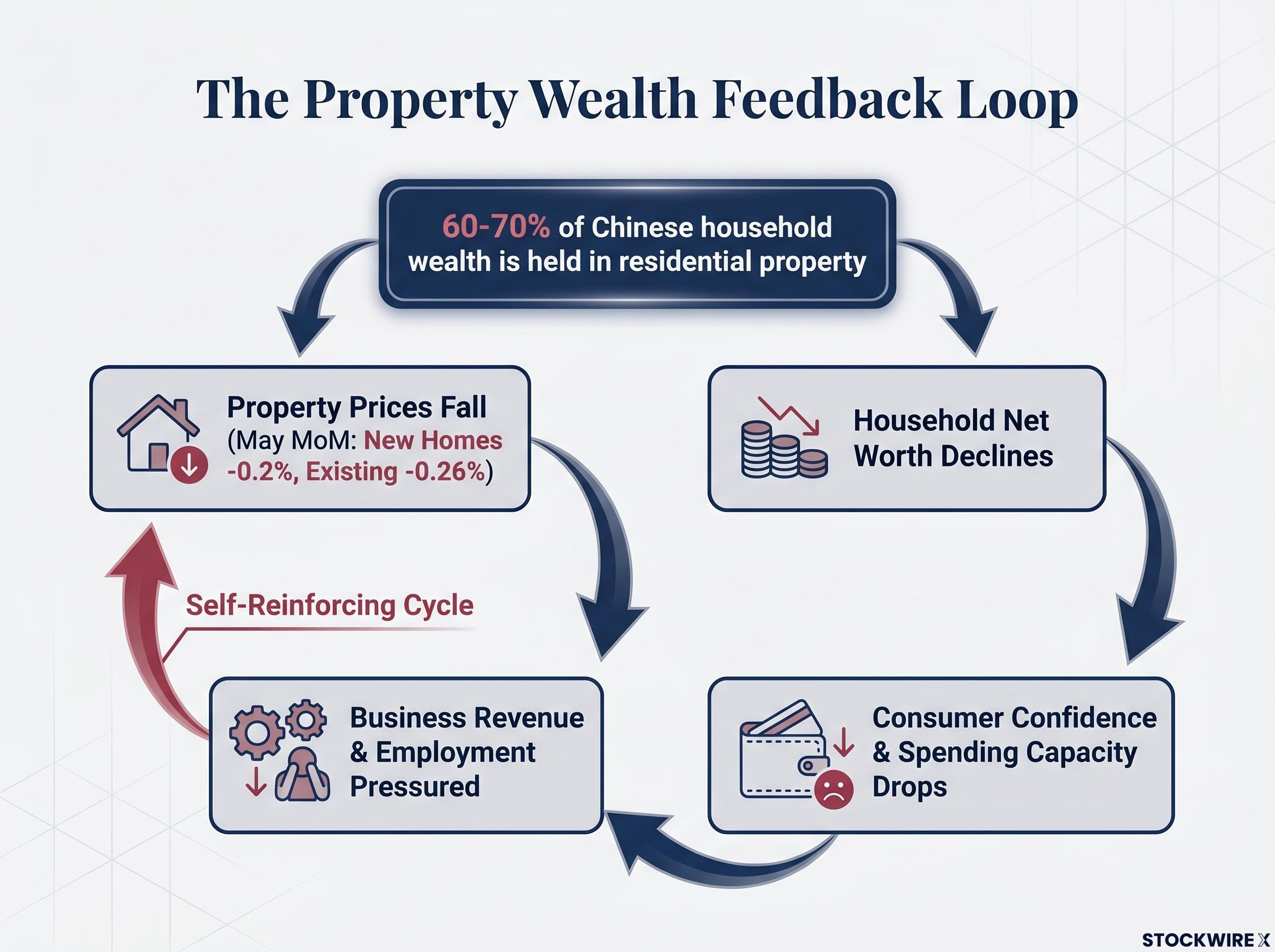

Understanding why targeted stimulus keeps failing requires understanding where Chinese household wealth actually sits.

Various surveys by Chinese researchers and international institutions estimate that 60-70% of Chinese household assets are concentrated in residential property. This figure is substantially higher than comparable economies; in the United States, for instance, equities and pension assets carry a much larger share of household balance sheets.

Key statistic: An estimated 60-70% of Chinese household wealth is held in property, making home prices the single most powerful determinant of consumer spending capacity across the economy.

The mechanics of the resulting feedback loop are straightforward. When home prices fall, household net worth declines. Declining net worth suppresses consumer confidence and spending capacity. Reduced spending pressures business revenue and employment, which feeds back into further downward price pressure on property. The cycle is self-reinforcing.

Official data from the National Bureau of Statistics (NBS), reported via Bloomberg, confirms the cycle remains intact. New home prices across 70 cities fell 0.2% month-on-month in May, accelerating from a 0.19% decline previously. Existing home prices dropped 0.26% over the same period.

The National Bureau of Statistics official May 2026 release confirms the fixed-asset investment contraction and new home price declines cited across this analysis, providing the primary source data that underpins the two-speed divergence thesis.

This is why the September 2024 stimulus package and subsequent interventions failed to produce durable recovery. Developer equities rallied briefly on policy announcements, then gave back the gains entirely as underlying price data continued to deteriorate. Mainland real estate equities have now completely reversed the valuation gains generated by the autumn 2024 government intervention measures, with the property sector index posting a 13% year-to-date decline. The pattern, repeated across multiple intervention episodes, suggests that short-term policy-driven rallies in property equities represent well-documented value traps rather than recovery signals.

Beijing is not waiting for property to recover. Capital is being redirected, and the destination is clear.

Electronic goods production rose 17% over the first five months of 2026. The export surge is concentrated in two categories: AI compute hardware and electric vehicles. Traditional export segments including clothing, toys, and low-end consumer goods are underperforming. The economy is not broadly strong; a narrow band of state-backed, capital-intensive sectors is carrying the headline numbers.

The drivers of the semiconductor export surge include base effects from prior-year weakness, domestic capacity expansion accelerated by Western sanctions, and China’s established scale in mature-node chip manufacturing. Sanctions pressure, paradoxically, has intensified the domestic investment cycle: restricted from purchasing advanced foreign equipment, Chinese manufacturers have doubled down on expanding capacity in the chip segments they can produce at scale.

There is a critical distinction here that separates informed positioning from headline-driven allocation. The $36 billion May semiconductor export figure does not signal that China has closed the gap with leading-edge producers.

China has meaningful scale in mature-node logic and memory chips, the segments that dominate current export volumes and serve the bulk of global demand for automotive, industrial, and consumer electronics applications. In advanced EUV-class nodes (sub-5nm), China does not have comparable capability.

The distinction between mature-node and advanced-logic production also clarifies where Chinese capacity expansion intersects with the AI chip supply chain: NVIDIA, TSMC, ASML, and Broadcom each occupy non-interchangeable layers of that chain, and Chinese foundry scale in legacy nodes pressures certain of those layers directly while leaving others structurally insulated.

For investors, the mature-node distinction matters more than the cutting-edge gap. Chinese foundries are building pricing power in legacy chip markets where global demand is large and persistent. Non-Chinese foundries with heavy revenue exposure to these same segments face direct competitive pressure. The investment opportunity, and the competitive threat, sits in the mature-node market share story rather than the advanced logic race.

The structural limitation, however, is employment. Advanced manufacturing is capital-intensive rather than labour-intensive. A semiconductor fabrication facility employs a fraction of the workforce that a comparable-value construction project supports. Strong technology export performance therefore does not generate the jobs or household income needed to replace what the contracting property sector has destroyed. This is why the two-speed economy is likely to persist rather than self-correct.

China’s domestic restructuring is repricing assets well beyond Chinese exchanges. Three specific transmission channels are already visible.

Non-Chinese hardware manufacturers face a compounding constraint beyond pricing competition: rare earth supply chain dependencies concentrate approximately 93% of global permanent magnet production and an estimated 99% of heavy rare earth processing within China, creating a structural cost-of-entry barrier that pricing pressure in mature-node chips does not fully capture.

These spillover channels mean that the Chinese economic transition is directly actionable intelligence for investors holding zero direct China exposure. A European automaker, an Australian iron ore producer, or a Taiwanese foundry with legacy-node revenue are all, in effect, trading on the same two-speed divergence playing out in Chinese macroeconomic data.

Major global institutions are no longer treating China as a single allocation decision. The decomposition is already happening in real portfolios.

Citi’s commentary highlights that strong technology and export performance is not translating into broad income growth or household consumption recovery, consistent with the capital-intensity argument that underpins the two-speed thesis. BofA has flagged credit-quality concerns in consumer-facing and construction-linked corporates, reflecting the downstream effects of property weakness. JPMorgan maintains selective overweight or neutral positioning on certain China technology names while underweighting property and old-economy segments.

Four dominant rotation themes emerge from institutional allocation commentary:

The disparity between state-led investment and the private sector contraction is the clearest signal that policy support is flowing to technology, not to the broader economy. Portfolio positioning that follows the capital, rather than the headlines, reflects this reality.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

China can no longer be traded as a unified macroeconomic entity. The property-linked old economy and the technology export economy have divergent fundamental trajectories, different policy support profiles, and different risk factors. Aggregate indices obscure more than they reveal.

The weight of institutional evidence points toward underweighting property-linked assets while maintaining selective, hedged exposure to advanced manufacturing and AI. The hedging is not optional: geopolitical risk premiums on Chinese technology exports remain elevated heading into the second half of 2026, and sanctions dynamics could shift the competitive calculus in either direction.

Geopolitical risk premiums on Chinese technology exports remain difficult to model precisely because the confirmed trade deal commitments from the May 2026 Beijing summit left AI chip export controls, Taiwan policy, and semiconductor supply chain restrictions entirely unresolved, meaning the sanctions trajectory that has driven Chinese domestic capacity investment remains the operative baseline for the second half of 2026.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors. Forward-looking statements regarding China’s economic trajectory are speculative and subject to change based on policy developments, geopolitical conditions, and market performance.

China's two-speed economy refers to the simultaneous boom in technology exports and advanced manufacturing alongside a contraction in domestic consumer spending and property markets. For investors, this divergence means aggregate China index exposure blends fundamentally opposite trajectories, making sector decomposition essential.

An estimated 60-70% of Chinese household wealth is held in residential property, creating a self-reinforcing feedback loop where falling home prices suppress consumer confidence and spending, which feeds further price declines. Policy-driven developer equity rallies in late 2024 fully reversed, with the property sector index posting a 13% year-to-date decline by May 2026.

Chinese domestic foundry capacity has scaled significantly in mature-node chip segments, creating volume and margin compression for non-Chinese chipmakers with legacy-node revenue exposure. The competitive threat sits in the mature-node market share story rather than cutting-edge advanced logic, where China does not yet have comparable capability.

As of mid-2026, institutions including JPMorgan, Citi, and BofA are underweighting property and old-economy segments while maintaining selective, hedged positioning in AI, semiconductors, and advanced manufacturing. Premium consumer names are also drawing selective attention given a K-shaped spending pattern favouring high-end retail over mass-market.

China's shift away from property and construction is reducing demand for iron ore, coking coal, and steel inputs, while driving growth in copper, lithium, and rare earths linked to EVs and renewables. Commodity exporters should be assessed against which demand basket their revenue aligns with rather than relying on aggregate China demand assumptions.