Microba Targets Final Capital Raise to Fund Cashflow Breakeven by End of CY2027

Microba targets cashflow break-even by end of CY2027

In its June 2026 investor presentation, Microba Life Sciences outlined plans to raise approximately $4 million via a non-underwritten placement, plus up to $1 million through a share purchase plan (SPP), to fund the company to cashflow break-even on a run rate basis by the end of CY2027. The placement involves issuing 80 million fully paid ordinary shares at $0.05 per share, with the SPP targeting up to $1 million on identical terms (maximum $30,000 per eligible shareholder). Each share issued will include one free attaching unlisted option, exercisable at $0.0625 and expiring three years from issue.

The offer price represents a 20.6% discount to the last close price of $0.063 on 2 June 2026, a 25.3% discount to the 5-day VWAP, and a 25.9% discount to the 10-day VWAP. The company’s cash balance as at 31 March 2026 stood at $7.28 million. Management positioned this capital raise as the final funding round required to reach operational self-sustainability.

When big ASX news breaks, our subscribers know first

What does cashflow break-even mean for investors?

Cashflow break-even refers to the point where cash inflows from operations equal cash outflows, eliminating the need for additional external funding to sustain the business. For Microba, this milestone would validate the commercial model the company has been building through years of investment in product development, clinical accreditation, and market expansion.

Break-even on a “run rate basis” means monthly cash inflows are expected to match monthly outflows by the end of CY2027, not necessarily cumulative profitability for the full year. The presentation highlighted that Microba has been deploying capital into infrastructure, clinical accreditation, and product development. Reaching break-even would shift the company from growth-stage cash consumption to self-sustaining operations — a transition that typically changes how the market values development-stage healthcare companies and reduces the risk of further shareholder dilution.

11 consecutive quarters of core testing sales growth

The presentation highlighted consistent commercial traction in the Diagnostics division, with 11 consecutive quarters of quarter-on-quarter core testing sales growth. The division has achieved 9x cumulative growth from Q4 FY2023 to Q3 FY2026, and 106% growth over the last 12 months (latest four quarters versus prior four). The annualised test run rate reached 23,000+ in Q3 FY26, reflecting 99% year-on-year core testing revenue growth for the quarter.

Management detailed a pipeline of signed enterprise-style contracts delivering 22,000+ tests per annum in incremental volume potential, signed between Q2 and Q4. The company has identified over 130 key account targets in Australia with estimated ordering potential exceeding 60,000 tests per annum. The presentation framed organic growth momentum as spanning both core markets: Australia, where adoption has moved beyond innovators into early adopters via enterprise clinic contracts, and the United Kingdom, where the testing market has outperformed Australia at the equivalent post-launch stage.

| Growth Metric | Figure |

|---|---|

| Consecutive quarters of growth | 11 |

| Cumulative growth (Q4 FY23 to Q3 FY26) | 9x |

| Year-on-year growth (last 12 months) | 106% |

| Q3 FY26 core testing revenue growth (YoY) | 99% |

| Annualised test run rate (Q3 FY26) | 23,000+ |

| Volume potential from new enterprise accounts (Q2-Q4) | 22,000+ tests p.a. |

| Key account pipeline (Australia) | 130+ targets |

| Estimated ordering potential (Australian pipeline) | 60,000+ tests p.a. |

GI Navigator launch set for Q3 CY26

Management outlined the upcoming launch of GI Navigator, described as a world-first complete microbiome and GI test designed to support the 40% of people living with unresolved GI disorders. The product is positioned to make result interpretation accessible for all healthcare professionals, not just specialists, powered by Microba’s Clinical Intelligence and advanced clinical decision support system.

The launch is scheduled for Q3 CY26 and will be supported by distribution partners Sonic and SYNLAB. The presentation positioned GI Navigator as the next major growth catalyst to drive adoption with mainstream medical professionals. The product targets a broader clinician base than existing offerings, potentially accelerating the company’s path to break-even by expanding market reach beyond early adopter practices.

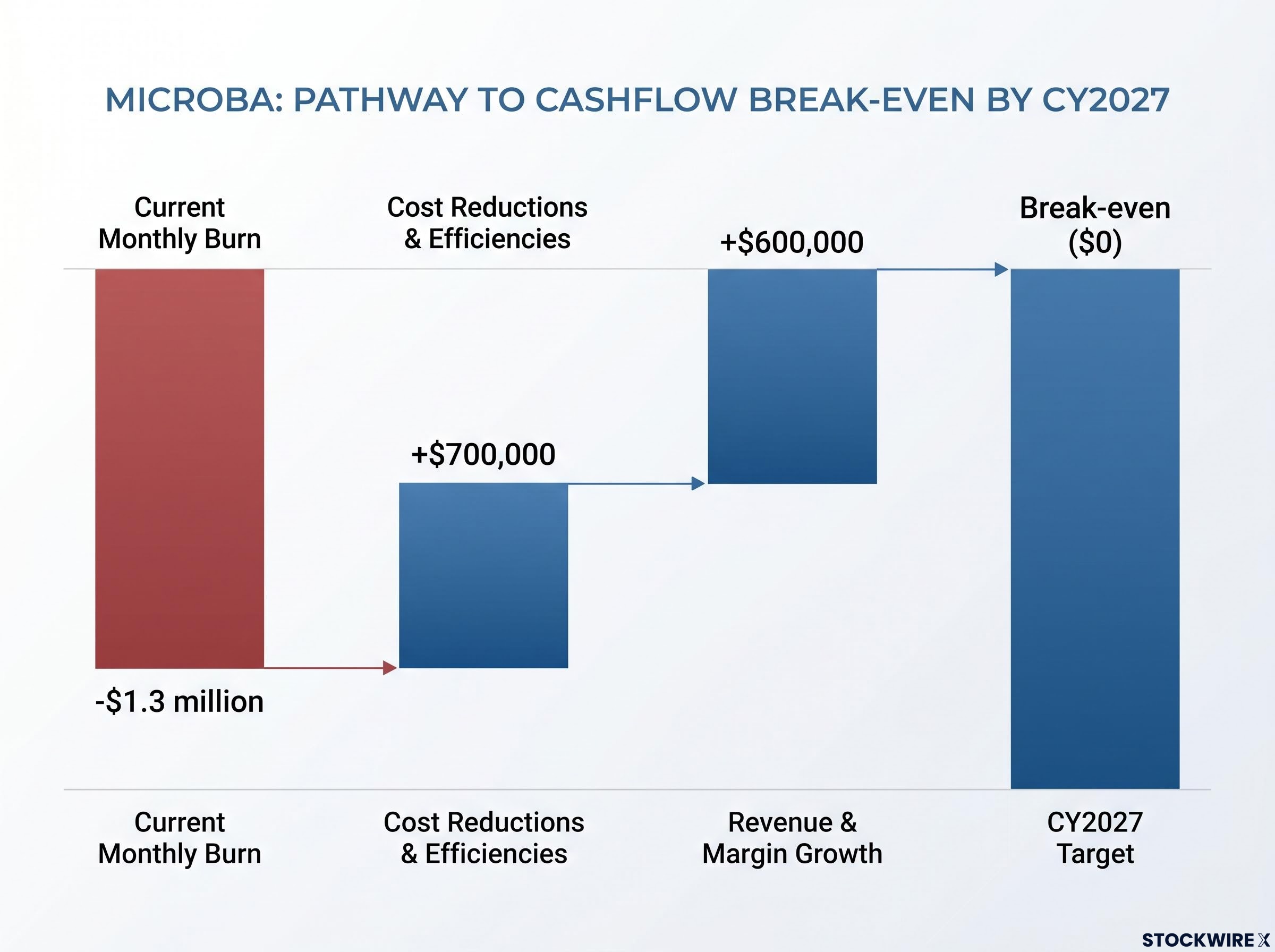

How Microba plans to close the gap to break-even

The presentation detailed four operational levers to move from the current monthly burn of $1.3 million to break-even by CY2027, built on infrastructure already in place:

-

Sales and marketing efficiencies: AI-supported customer targeting and marketing, unified global brand, automated lifecycle marketing, and self-serve signup systems designed to reduce customer acquisition cost.

-

Cost reductions and operational efficiencies: AI automation across customer support, HR, legal, and finance functions to structurally lower cost-to-serve as the company scales.

-

Engineering, science and product efficiency: Major new product build nearing completion, with AI-supported product, evidence, and software development systems designed to cut engineering and product cost per release.

-

Sales growth and margin expansion: Rising volume on a fixed cost base, with margin expansion anticipated from pricing power, scaling economics, and operational efficiency.

Management quantified the pathway: approximately $700,000 in monthly cost reductions and efficiencies, plus approximately $600,000 in monthly growth from revenue and contribution margin on the fixed cost base, bridging the gap from $1.3 million burn to break-even. The company emphasised that this pathway relies on operating leverage over existing infrastructure rather than aggressive new capital deployment.

$25 billion addressable market in gastrointestinal disorders

The presentation detailed market sizing across multiple layers. The Total Addressable Market (TAM) is estimated at $25 billion representing 82 million tests per annum across seven major markets (Australia, UK, US, France, Germany, Spain, Italy) addressing GI disorders. The Serviceable Addressable Market (SAM) — the near-term target slice — is estimated at 18.6 million tests per annum across the top five focus markets.

The Serviceable Obtainable Market (SOM), representing expected capture in a cash-pay environment, is estimated at 2 million tests per annum. Management stated the company “only needs to capture a small amount to impact at scale,” highlighting that current penetration is minimal relative to the SOM. The market sizing methodology incorporated primary, secondary, and tertiary research, including detailed analysis of US Medicare claims data, clinician penetration modelling, and prevalence studies.

Therapeutics division active in partnering process

The presentation disclosed that Microba’s Therapeutics division is active in a partnering process with a Boston-based specialist advisory firm. Management included an explicit caveat: no partnering agreement has been entered into as at the date of the presentation.

Partnering Status

For the avoidance of doubt, no partnering agreement has been entered into as at the date of this presentation.

The update followed multiple positive clinical trial readouts across the microbiome therapeutics sector between November 2025 and February 2026, including results from Siolta Therapeutics (allergic disease), MaaT Pharma (graft-versus-host disease), EnteroBiotix (irritable bowel syndrome), and Microbiotica (inflammatory bowel disease). The presentation cited over $100 million investment for the sector, validating sector appetite for these assets.

Microba’s lead therapeutic asset is MAP 315, a Phase 2-ready oral-capsule Live Biotherapeutic Product for mild-to-moderate ulcerative colitis, targeting a US$10 billion+ market where 30% to 60% of patients are under-served. A fast-follow programme involves MAP 315 in Phase 1b for immunotherapy-induced colitis. The company has identified therapeutic leads across 18 diseases.

Recent corporate interest validates company value

Management disclosed that a UK-based Private Equity fund approached Microba regarding potential divestment of the Diagnostics and Supplements businesses. Terms were agreed on an in-principle basis, subject to conditions precedent including shareholder approval. The consideration would have exceeded Microba’s market capitalisation at the time ($44 million on 28 April 2026).

The transaction did not proceed; management stated the final deal structure was no longer in the best interest of shareholders. The presentation framed this as external validation of the company’s asset value rather than a failed transaction. Third-party interest at a premium to market capitalisation suggests the market may be undervaluing Microba’s assets, providing a reference point for investors assessing intrinsic value.

Key dates for investors

The timetable for the equity raise includes:

- Settlement of placement shares: 17 June 2026

- Issue of placement shares: 18 June 2026

- Prospectus lodgement and SPP opens: 19 June 2026

- SPP closes: 22 July 2026

- Extraordinary General Meeting (EGM) to approve attaching options and SPP shares: 24 July 2026

- Issue of SPP shares and all attaching options: 29 July 2026

- SPP shares commence trading: 30 July 2026

Investors considering participation should note the SPP record date was 11 June 2026 and the SPP closes 22 July 2026. The placement is non-underwritten and will be conducted under the company’s existing capacity under ASX Listing Rule 7.1. All attaching options under both the placement and SPP are subject to shareholder approval at the EGM.

The next major ASX story will hit our subscribers first

Major shareholders and capital structure

As at 9 June 2026, Microba had 608.96 million shares on issue with a market capitalisation of $38.36 million. The 52-week trading range was $0.063 to $0.135.

Major shareholders as at the most recent substantial shareholder notices (pre-raise):

- Sonic Healthcare: 21.68%

- Perennial: 12.02%

- Mercer Investments (Australia): 6.37%

- Thorney Investment Group: 5.88%

- SA Microba Holdings: 5.50%

Strategic shareholders including Sonic Healthcare hold over 20%, providing alignment between commercial partners and the share register. The cash balance as at 31 March 2026 was $7.28 million.

Don’t Miss the Next Healthcare Breakthrough

Join 20,000+ investors getting FREE breaking ASX news delivered to your inbox within minutes of release, complete with in-depth analysis. Click the “Free Alerts” button at StockWire X to receive real-time alerts the moment market-moving announcements hit in Healthcare, Tech, Finance and beyond.