Most competitive advantages in investment analysis are framed around technology, brand recognition, or regulatory licences. For a listed funds manager, the most underappreciated form of protection may be something far more concrete: contractually guaranteed access to the raw material of the business itself. Asset managers live or die on their ability to source investable opportunities. In real-asset funds management, where assets are sourced deal-by-deal in competitive processes, supply-side constraints represent a persistent structural vulnerability. Long-term exclusive pipeline agreements address this vulnerability directly, yet they rarely feature in standard moat analysis frameworks. This article explains what pipeline exclusivity is, how it functions as a sustainable competitive advantage, what makes it difficult to replicate, and how equity markets can interpret these arrangements when assessing a listed fund manager’s competitive position. Aland Equity Group (ASX: AEG) and its 10+10 year pipeline arrangement serve as a concrete illustrative case throughout.

Why asset supply is the raw material that funds management runs on

The commercial engine of any funds management business operates across three stages. First, the manager raises capital from investors. Second, that capital is deployed into assets. Third, the manager earns management and performance fees over the life of those assets.

Every stage is contingent on a reliable, repeatable supply of suitable investments. Without credible access to assets, there are no new funds to launch, no fee base to grow, and no performance upside to target. Asset sourcing is not a background operational function; it is the foundational input of the entire business model.

Most managers, particularly in private markets and real assets, source this input in direct competition with other capital. Each development, acquisition, or co-investment must be found, underwritten, and won through a competitive process. That introduces a set of structural vulnerabilities that persist across market cycles.

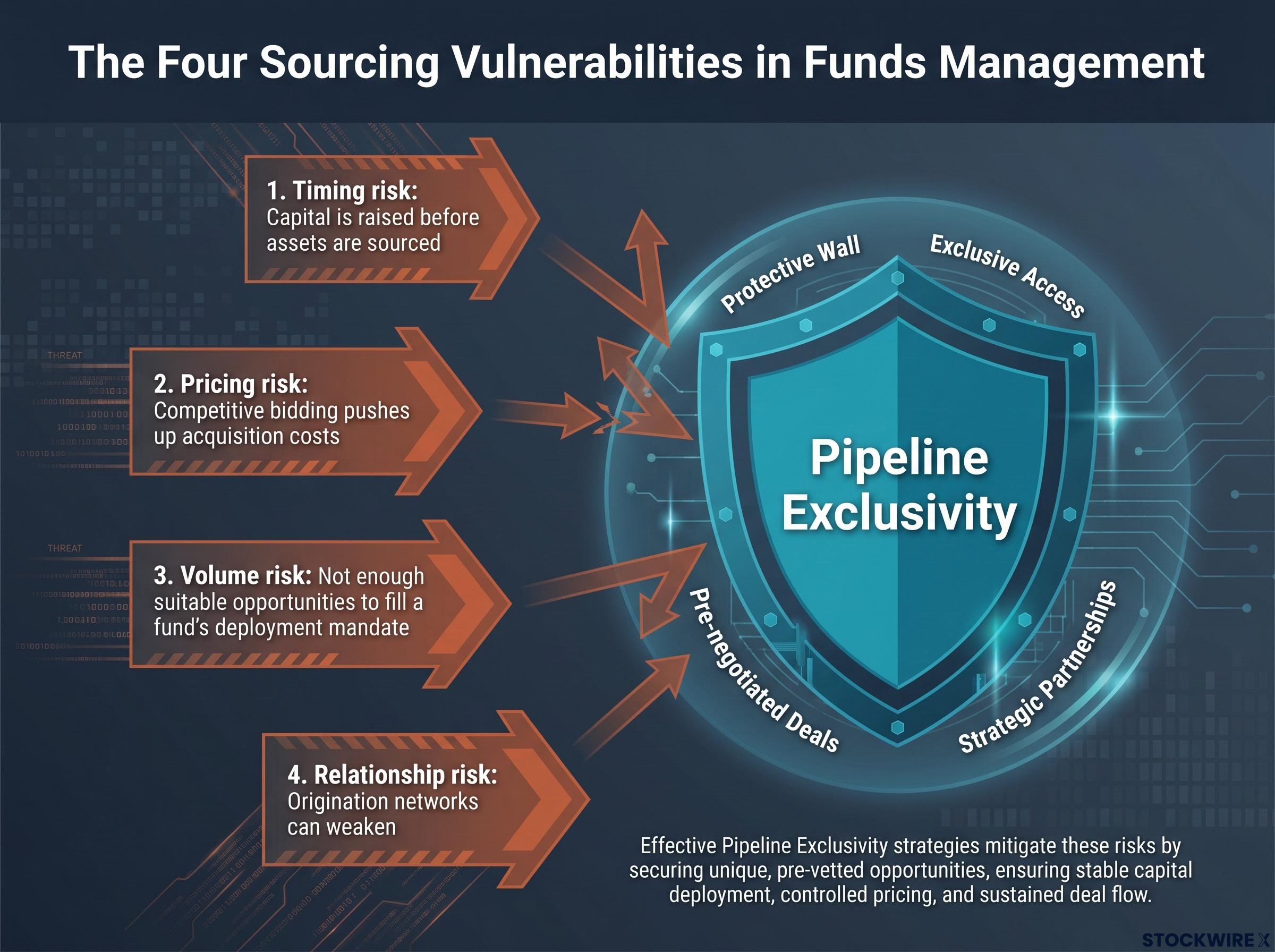

The four sourcing vulnerabilities competitive deal flow creates

- Timing risk: Capital is raised before assets are sourced, creating schedule pressure to deploy that can compress returns and erode investor confidence.

- Pricing risk: Competitive bidding pushes up acquisition costs and compresses the fee-generating economics of each deal.

- Volume risk: In thinner markets, there may not be enough suitable opportunities to fill a fund’s deployment mandate.

- Relationship risk: Origination networks can weaken or be outcompeted over time, leaving a manager exposed to deal flow erosion.

These are not one-off problems. They drive volatility in fund launch timing, assets under management (AUM) growth, and fee revenue across the cycle. Pipeline exclusivity directly targets this structural vulnerability by pre-securing the asset supply before competitive processes can intervene.

When big ASX news breaks, our subscribers know first

What a sustainable competitive advantage actually requires

A meaningful distinction exists between advantages that improve a firm’s odds in a competitive process and advantages that remove the competitive process entirely. Most advantages in asset management are relative: better sourcing networks, a lower cost of capital, or a stronger brand. These improve the probability of winning deals but do not prevent other managers from competing for the same assets.

Pipeline exclusivity sits in a different category. Under a Buffett-style moat framework, a genuine competitive advantage prevents competitors from accessing the same economic opportunity, not merely lets a firm compete more effectively for it. Where a manager holds contractual exclusivity over a defined set of assets, competing managers are not disadvantaged; they are categorically excluded for the term of the agreement.

The analytical dividing line: exclusivity removes the competitive process rather than improving the manager’s odds within it. For assets within its scope, there is no competitive process to win or lose.

The standard moat taxonomy identifies protection through technology, brand, network effects, and regulatory licences. Pipeline exclusivity sits alongside these as a structurally distinct category: a quasi-licence over the future supply of investable assets in specific markets. The table below illustrates the difference between relative advantages and categorical exclusivity across several dimensions.

The economic moat framework that underpins this analysis was developed by Morningstar to identify companies capable of sustaining excess returns on invested capital for 20 years or more, a threshold fewer than 20% of covered companies typically meet; pipeline exclusivity, as a supply-side protection over asset access rather than over customers or technology, represents a distinct structural category that the standard taxonomy does not explicitly address.

| Dimension | Relative advantage | Categorical exclusivity |

|---|---|---|

| Mechanism | Improves probability of winning deals | Removes the competitive process entirely |

| Competitor access | Competitors can still bid for the same assets | Competitors are contractually excluded |

| Durability | Erodes as competitors improve their own position | Persists for the contractual term regardless of competitor actions |

| Replicability | Can be matched with capital and talent | Requires pipeline rarity, developer trust, and time to replicate |

This framework gives analysts a reusable test for evaluating exclusivity claims in any asset management context. The question is not whether the arrangement improves competitive position, but whether it removes a category of competition entirely.

How long-term exclusive pipeline rights work in practice

The structural anatomy of a pipeline exclusivity arrangement has several defining features: the asset types and geographies covered, the duration of the commitment, and what exclusivity means operationally for both the manager and the development partner.

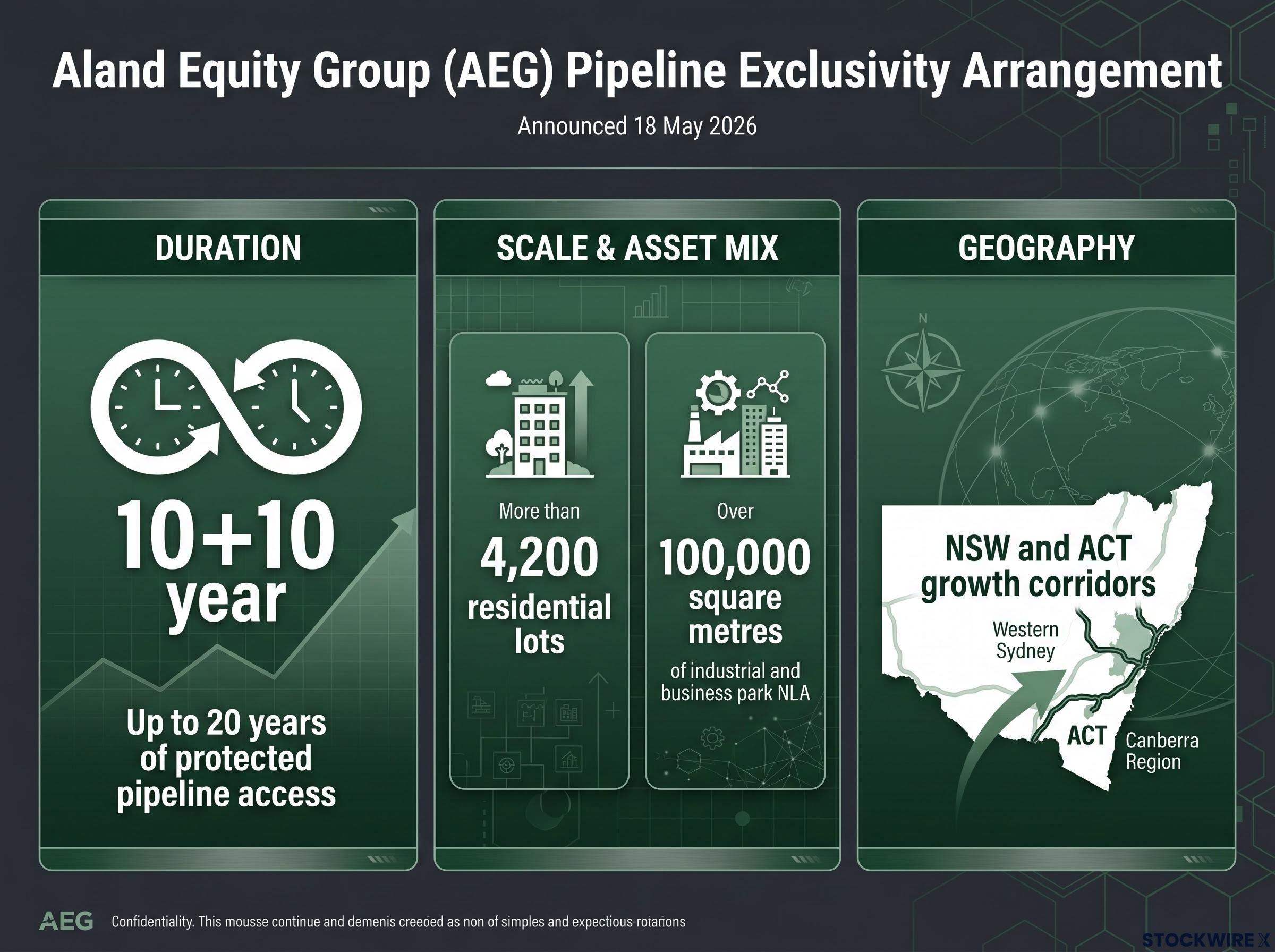

AEG’s arrangement, announced via ASX on 18 May 2026, illustrates how the concept is implemented at scale in a listed Australian context. The key structural features include:

- Scale: Exclusivity over more than 4,200 residential lots and over 100,000 square metres of industrial and business park net lettable area (NLA)

- Geography: Assets located in NSW and ACT growth corridors, where population growth and infrastructure investment underpin demand

- Duration: A 10-year initial exclusivity term with an option to extend for a further 10 years, providing up to 20 years of protected pipeline access

- Asset mix: Both residential and industrial asset classes, providing sector diversification within the pre-secured pipeline

The dual asset-class composition carries its own strategic significance. Residential and industrial property respond differently to economic, policy, and credit cycle conditions. Having both classes within a pre-secured exclusive pipeline provides sequencing optionality: the manager can structure and time fund launches according to prevailing market conditions, a flexibility unavailable to managers dependent on opportunistic deal flow.

Why the duration of an exclusivity agreement changes its strategic weight

Duration is what separates a tactical arrangement from a franchise-level feature. A 10-20 year window spans multiple fund cycles and at least one full property cycle. That means the exclusivity is not a one-off transaction advantage; it is a structural component of the business model that persists across changing market conditions.

A short-term preferred access agreement, by contrast, provides a temporary head start. It can be outcompeted, renegotiated, or allowed to lapse. A multi-decade exclusivity arrangement embeds itself into the manager’s forward planning horizon, capital raising narrative, and competitive identity in a way that short-term access cannot.

Why replicating a pipeline exclusivity position is structurally costly

For pipeline exclusivity to constitute a genuine moat, it must be difficult to replicate. Four overlapping barriers apply in practice, each reinforcing the others.

- Pipeline rarity. A competitor would need to identify a development partner controlling a similar scale of residential and industrial assets in high-demand growth corridors, willing to commit them on an exclusive basis. That combination of scale, location quality, and developer control over future pipeline is uncommon in any market.

- Developer trust and incentive alignment. A developer agreeing to exclusivity is surrendering the option to shop projects to multiple capital sources. Developers do so only where they receive something in return: funding certainty, a tested multi-project relationship, or a structure that aligns incentives over many years. Recreating that depth of relationship and integration is time-consuming, uncertain, and cannot be shortcut with capital alone.

NBER research on vertical integration and long-term contracting establishes that exclusive supply agreements create durable barriers to entry by combining contractual lock-in with the relationship-specific investments required to sustain them, precisely the dynamic that makes pipeline exclusivity difficult to replicate through capital deployment alone.

- Geographic land constraints. Land in growth corridors is finite. Zoning approvals, infrastructure access, and demand dynamics are location-specific. A competitor cannot substitute an alternative geography and claim equivalence; the investment case is partly embedded in the specific corridors and the finite land supply within them.

- Development-stage operational capability. Many listed fund managers focus on acquiring completed or near-complete assets. Exclusivity over development-stage assets requires comfort with construction risk, development-stage underwriting, and direct partnering with developers through the project lifecycle. That operational integration is demanding and not easily acquired by a manager without the relevant track record and internal capability.

The barrier is not legal impenetrability. It is the compounding of time, trust, operational capability, and corridor-specific land control required to assemble an equivalent position. The exclusivity window of up to 20 years means any replication attempt must begin immediately to have any prospect of mattering before the arrangement potentially renews.

The result: rivals cannot quickly assemble an equivalent position even with abundant capital. Each barrier is meaningful on its own, but their overlap is what makes replication slow and costly by design.

How exclusive pipeline access shapes fund formation and earnings predictability

Pre-secured pipeline access changes the earnings and risk profile of a listed funds manager across several connected dimensions.

Knowing the scale, type, and geography of available assets over the next decade allows a manager to plan a sequence of funds with defined themes, target sizes, and deployment schedules. Capital raising becomes a conversation about deploying into a known, exclusive pipeline rather than a generic promise to find assets in an uncertain market. That specificity strengthens the capital raising proposition directly.

One of the most damaging risks for any manager is raising capital and then failing to deploy it on schedule. Idle capital drags on fund-level returns, can trigger fee concessions, and erodes limited partner (LP) confidence. With an exclusive pipeline, the manager holds a pre-defined inventory to deploy into, materially reducing deployment timing risk.

A long-duration pipeline spanning multiple asset classes also gives the manager optionality to sequence projects according to prevailing conditions. That can smooth AUM growth and fee revenue across market cycles rather than leaving both as a function of sporadic deal flow. The table below compares the profile of a manager with exclusive pipeline access against one relying on opportunistic sourcing.

| Dimension | Exclusive pipeline access | Opportunistic sourcing |

|---|---|---|

| Fund formation predictability | High; pipeline scale and timing are known in advance | Low; dependent on deal flow availability at time of raising |

| Deployment timing risk | Reduced; pre-identified assets minimise idle capital | Elevated; capital may sit undeployed while assets are sourced |

| AUM growth visibility | Stronger; multi-cycle pipeline supports forward forecasts | Weaker; dependent on competitive market conditions |

| Earnings dispersion | Narrower; fewer downside scenarios from supply failure | Wider; sourcing uncertainty introduces additional downside paths |

From earnings visibility to valuation: what analysts should consider

These features support greater confidence in medium-term AUM and fee forecasts, and a narrower dispersion of outcomes in scenario analysis. Both can support a higher multiple on management fee earnings relative to a manager reliant on deal-by-deal sourcing.

Higher confidence in AUM growth supports more reliable fee revenue forecasts. Reduced capital deployment slippage risk narrows the downside scenario. Structural, durable pipeline access may warrant a premium to peers without equivalent supply-side protection. Pipeline exclusivity may merit explicit treatment in scenario analysis and valuation frameworks rather than being subsumed into generic qualitative commentary on management quality.

For investors wanting to contextualise how the pipeline visibility argument connects to listed market valuations, our full explainer on alternative asset manager re-ratings examines how KKR’s 23% fee-related earnings growth and Macquarie’s 49% profit surge in 2025 illustrate the operating leverage mechanics that make AUM growth predictability so valuable to listed fund manager multiples.

The analytical questions that separate genuine exclusivity from preferred access

Not all exclusivity claims carry equal weight. A disciplined approach requires probing both the strength of the protection and the risks concentrated within it. Five questions provide a practical framework.

- Is this true exclusivity or preferred access? Strong origination networks are valuable but are not the same as contractually binding exclusive rights. Exclusivity removes a category of competitive risk entirely; preferred access merely reduces it. The distinction is material to valuation.

- What are the key terms and termination conditions? Analytical value depends on enforceability, clarity around the assets covered, scope of the exclusivity, and the conditions under which the arrangement can be altered or terminated, including change-of-control provisions, performance thresholds, or counterparty default triggers.

- How deliverable is the underlying pipeline? Exclusivity has value only if the development partner can actually bring projects through to fundable stages. This requires scrutiny of the partner’s execution track record, balance sheet strength, access to construction finance, and operational capacity across the pipeline horizon.

- What is the quality and positioning of the pipeline? Headline metrics such as 4,200 lots and 100,000 square metres are a starting point, not a conclusion. Analysts need to consider corridor-level demand, zoning and planning risk, infrastructure access and timing, and likely exit markets.

- How concentrated is the exposure? While exclusivity strengthens the moat, it can simultaneously concentrate risk in specific geographies and a single development relationship. That concentration should be weighed explicitly against the diversification benefit of the dual asset-class structure and the manager’s overall strategic positioning.

The core analytical dividing line: exclusivity is a distinct category of competitive advantage, not a sub-type of strong origination. Treating it as such changes the weight assigned to it in valuation frameworks.

These questions convert the conceptual discussion into a reusable framework applicable to any listed funds manager claiming a pipeline advantage, making the analysis generalisable beyond the specific AEG case study.

Pipeline exclusivity as a supply-side moat in the competitive landscape of funds management

In listed real-asset funds management, long-term pipeline exclusivity functions as a supply-side moat: a quasi-licence over the future supply of investable assets in specific, attractive markets. It is durable, structural, and difficult to replicate.

Supply-side moat: A competitive advantage that protects access to the core input of the business, is durable when structured over long time horizons, is structural rather than dependent on continuing to outcompete rivals, and is difficult to copy given the relationship depth, pipeline scale, and geographic specificity required.

AEG’s 10+10 year exclusivity over 4,200-plus residential lots and 100,000-plus square metres of industrial NLA in NSW and ACT growth corridors provides a live listed-market example of how this can be embedded into a business model at scale. Whether or not an investor holds the stock, the structure itself is instructive: it demonstrates how a commercial arrangement around asset supply can translate into a sustainable competitive advantage that equity markets can identify, analyse, and over time, price. As listed real-asset managers grow in number and complexity, supply-side moats of this kind are likely to become a more explicitly recognised category in competitive position assessments.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. All specific AEG pipeline figures and exclusivity terms derive from the company’s ASX announcement dated 18 May 2026.

—