Citi Splits on Big Four: Buy ANZ, Sell CBA in Sector Downgrade

6 hrs ago

Three capital-market events landed in the same direction during the week of 9-10 June 2026: a $7 billion equity raise from Super Micro Computer, a guidance miss from Broadcom, and an $80 billion capital raise from Alphabet. Each event, taken alone, would have moved its stock. Together, they are forcing a harder question about the AI stock selloff now rippling across indices and semiconductor names: who funds the artificial intelligence buildout, and when does it pay back? The Philadelphia Semiconductor Index had already dropped 10.26% in a single session on 5 June. The VIX spiked above 20 for the first time since April. What follows is an assessment of whether the AI investment thesis has entered a structural repricing phase or is cycling through a painful but recoverable correction, and what the distinction means for portfolio positioning.

The damage on 10 June 2026 was broad, simultaneous, and skewed toward the names most identified with the AI trade:

The VIX above 20 is not merely a volatility reading. It is a positioning signal: the AI trade had become crowded enough that its own repricing generated systemic stress.

The Philadelphia Semiconductor Index decline on 5 June erased more than $1 trillion in market capitalisation from chip stocks in a single session, a scale of destruction that reflects how thoroughly AI-linked equities had become the load-bearing weight of the broader technology trade.

According to Vital Knowledge analysts, technology sector deterioration was considered more consequential to the S&P 500 than escalating Middle East geopolitical tensions, as the sector extended its Friday losses.

That framing matters. When analysts treat chip-stock weakness as more market-moving than active conflict, the AI trade is no longer a sector bet. It is the index itself, repricing.

Index-level concentration risk compounds the repricing dynamic: Goldman Sachs identified in May 2026 that low volatility across AI-heavy benchmarks was masking dangerous distributional divergence, where large opposing moves by individual winners and losers cancel each other out, leaving passive investors exposed to single-stock risk they believe they have diversified away.

On 9 June 2026, Super Micro Computer (SMCI) announced a $7 billion equity and equity-linked financing package: $5 billion in underwritten offerings (common stock and convertible preferred depositary shares) plus a $2 billion at-the-market programme commencing no earlier than Q3 2026. The stated purpose was purchasing components to fulfil outstanding AI server orders.

The company disclosed approximately $39 billion in AI server orders from more than 20 customers. SMCI shares fell approximately 15% at the open on 10 June.

The stock reaction was not punishment for a bad business. It was repricing of the capital model the business now requires. Three structural implications follow:

For investors who had modelled AI hardware names as operating-leverage plays, the adjustment is material. Valuation frameworks must now incorporate dilution paths and recurring capital raises, not assume a single spending phase followed by harvest.

The AI infrastructure stack operates in three layers, each with a distinct capital function. Understanding this structure is what separates noise from signal when multiple data points arrive in the same week.

| Layer | Representative Company | Signal This Week | What It Indicates |

|---|---|---|---|

| Hyperscalers | Alphabet | $80 billion equity raise | AI capex outstripping self-funding capacity |

| Chip Designers | Broadcom | $1.2 billion guidance shortfall | Demand not converting to linear earnings beats |

| Server Assemblers | Super Micro | $7 billion equity issuance | Suppliers equity-hungry at scale |

Hyperscalers commission infrastructure. Chip designers supply custom silicon and networking components. Server assemblers integrate and deliver. Broadcom sits between hyperscalers and foundries, designing custom accelerators, ASICs for AI inference, and networking silicon for high-performance data centres. Its order book functions as a high-frequency signal on how aggressively the top layer is scaling AI capacity.

When signals at multiple layers of the same stack point in the same direction simultaneously, the analytical weight is multiplicative, not additive. A supplier miss alone could be idiosyncratic. A hyperscaler equity raise alone could reflect balance-sheet prudence. A server assembler dilution alone could be opportunistic.

All three in the same week compress the probability that any single event is noise. Combined with crowded positioning in AI-linked equities, even modest earnings friction gets amplified into violent price moves, exactly the pattern the SOX index demonstrated on 5 June.

Broadcom (AVGO) delivered its Q3 fiscal 2026 AI semiconductor revenue guidance at $16 billion, against a consensus estimate of $17.2 billion, a $1.2 billion shortfall. The stock fell approximately 12% around 3-4 June 2026, even as management maintained strong AI demand language.

The miss is best understood not as a demand failure but as an earnings-linearity problem. Strong demand accompanied by a guidance shortfall signals that converting orders into smooth beat-and-raise results is harder than the prior narrative assumed. Non-AI segment drag, pricing pressure, and order lumpiness all introduce friction that linear growth models cannot absorb.

A Morningstar-identified capex-to-revenue lag of 18-24 months sits at the centre of the semiconductor valuation debate, meaning the earnings-linearity problem visible in Broadcom’s guidance miss may persist across the sector well into 2027 before AI infrastructure spending converts to measurable revenue at scale.

Alphabet (GOOGL) announced plans to raise $80 billion in equity offerings around 1-2 June 2026, including a $10 billion private placement to Berkshire Hathaway in Class A and Class C shares, to fund AI compute infrastructure.

Vital Knowledge analysts noted that the raise prompted questions about whether even the largest technology firms can adequately fund the data centre buildout required to support advanced AI development.

A hyperscaler accessing capital markets hits sentiment harder than a supplier doing the same because it questions the funding assumptions investors had relied on most:

The combination removes the two most common counterarguments to AI capex concern: that hyperscalers are flush enough to self-fund and that AI demand reliably converts to earnings beats.

| Dimension | Correction Case | Structural Warning Case |

|---|---|---|

| Demand Signals | Secular AI adoption drivers remain intact; $39 billion in SMCI orders signals sustained multi-year demand | Broadcom’s miss suggests hyperscaler demand may be transitioning from explosive to managed |

| Earnings Linearity | Prior semiconductor cycles have seen violent drawdowns inside longer uptrends when positioning was crowded | Strong demand paired with guidance misses signals volatile conversion, not smooth beat-and-raise |

| Funding Model | SMCI’s willingness to dilute at current prices implies management confidence in demand sustainability | Hyperscalers and suppliers both relying on capital markets creates pro-cyclical risk |

| Historical Analogy | Valuation and positioning reset within a secular growth cycle | Telecom-era build-out: extreme capital intensity with still-developing monetisation |

The pro-cyclical funding dynamic deserves particular attention. When falling equity prices and rising credit spreads coincide with revised growth assumptions, capex cuts can follow, which then validate the lower assumptions. The system feeds on itself.

At this stage, the data support heightened scepticism and higher risk premia, not a definitive end-of-cycle call. The burden of proof, however, has shifted to management teams. Invoking “AI” will no longer justify aggressive multiples without hard evidence of earnings and cash-flow traction.

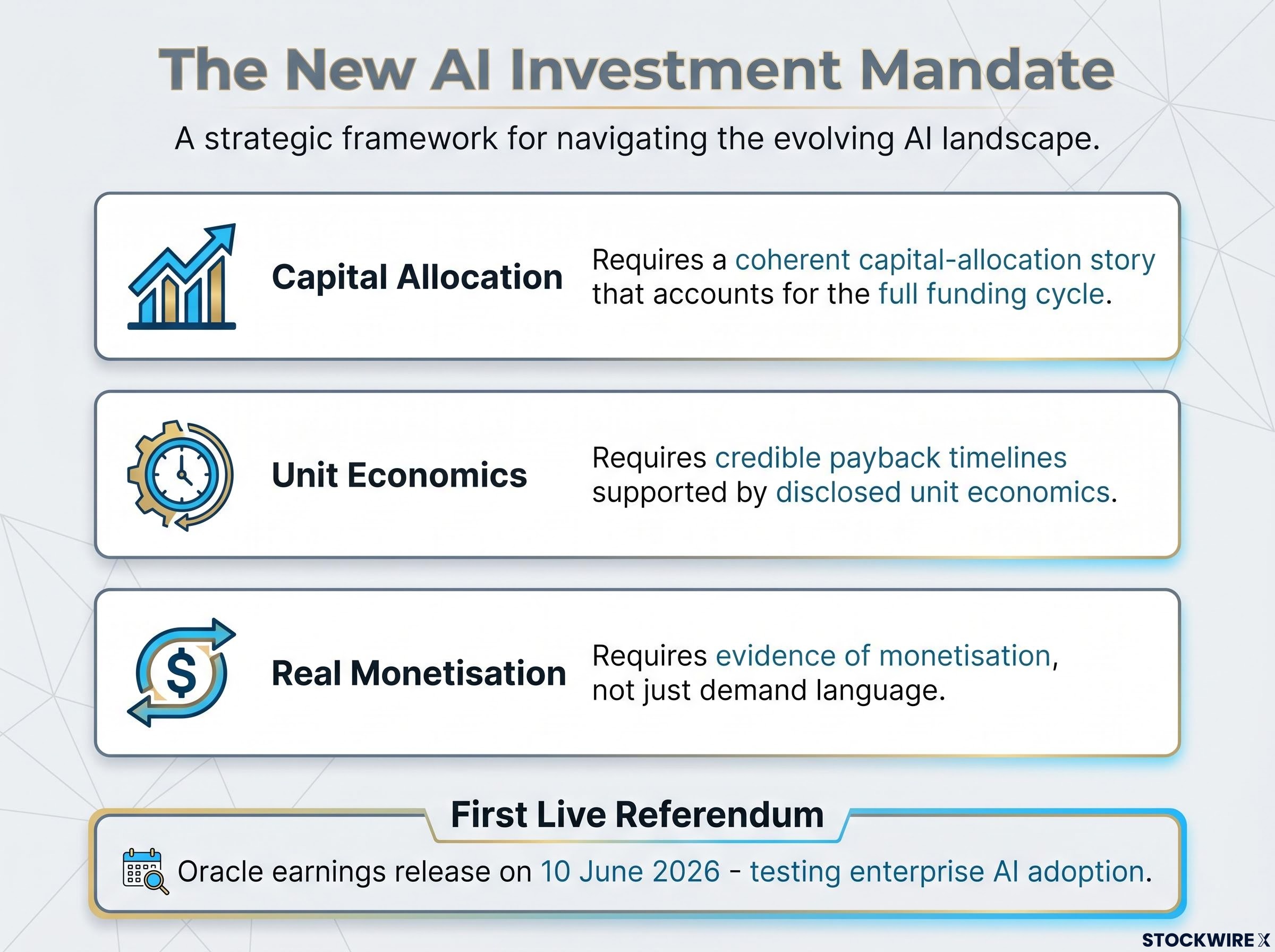

Oracle’s earnings release, scheduled after the close on 10 June 2026, functions as the immediate test case. Oracle has positioned itself as a cloud and AI infrastructure beneficiary; its results and AI-workload guidance will provide the first post-selloff data point on enterprise AI adoption.

Strong AI-driven cloud growth would support the correction view. Weak AI signals or cautious guidance would reinforce structural concerns. The result will not resolve the debate, but it will weight one side of it.

The selloff argues for re-underwriting, not abandoning, AI exposure. The investment case has not collapsed. The analytical framework, however, must shift from total addressable market optimism to return on invested capital and capital-structure discipline.

The three-part test for any AI-linked holding is now:

Five forward indicators will determine whether the current repricing stabilises or deepens:

Enterprise software monetisation is the missing variable in the AI investment equation: more than 75% of software application companies in the Morningstar US Technology Index are in negative territory year-to-date in 2026, yet the spread between the top and bottom deciles of US technology stocks has reached a record 133 percentage points, suggesting the market is making sharp distinctions rather than selling technology indiscriminately.

For infrastructure names specifically, model return on invested capital across the full AI capex and working capital cycle, not next-quarter earnings per share. Favour businesses that self-fund AI investments from diversified cash flow and still return capital to shareholders. Apply a discount to models requiring frequent equity issuance or high leverage to sustain their AI roadmap.

The three concurrent events of early June 2026 are best understood as regime confirmation, not isolated noise. They mark the transition from a narrative-driven AI trade, where the direction of AI adoption was sufficient to justify positioning, to a capital-discipline and earnings-proof trade, where the cost of funding and the timeline to returns determine which names merit ownership.

The investors who navigate this phase well will be those who demanded coherent capital-allocation stories, credible paybacks, and evidence of monetisation when the market was still willing to reward stories alone. The AI thesis is not broken. The free version of it is.

For readers wanting to apply a more rigorous analytical structure to the repricing question, our dedicated guide to AI bubble frameworks examines the Shiller CAPE ratio at 40.11, Minsky’s financing stages, and three additional valuation lenses, with specific attention to where the current AI cycle sits relative to the speculative financing threshold that historically precedes the most severe drawdowns.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections referenced in this article are subject to market conditions and various risk factors.

For deeper coverage of the individual names most affected, refer to related StockWire X analysis on semiconductor sector valuations and hyperscaler capex trends.

The AI stock selloff refers to the broad decline in AI-linked equities that accelerated in early June 2026, triggered by three concurrent events: Super Micro Computer's $7 billion equity raise, a $1.2 billion guidance shortfall from Broadcom, and an $80 billion capital raise by Alphabet, which collectively raised questions about the sustainability of AI infrastructure funding and earnings linearity.

The Philadelphia Semiconductor Index fell 10.26% in a single session on 5 June 2026, erasing more than $1 trillion in market capitalisation from chip stocks, because AI-linked equities had become so heavily weighted in technology indices that crowded positioning amplified even modest earnings friction into violent price moves.

Super Micro's $7 billion raise signals that AI hardware suppliers can no longer finance their order cycles from internal cash flow alone, meaning investors must now model recurring dilution risk and longer capital payback periods similar to telecom or infrastructure build-outs rather than assuming a software-style operating leverage story.

Broadcom's Q3 fiscal 2026 AI revenue guidance came in $1.2 billion below consensus estimates, highlighting an earnings-linearity problem where strong underlying demand does not convert to smooth beat-and-raise results; analysts at Morningstar identify an 18-24 month capex-to-revenue lag that could persist across the sector well into 2027.

Investors should monitor Oracle's AI-workload commentary, hyperscaler capex disclosures from Microsoft, Alphabet, Amazon, and Meta for any shift toward ROI discipline, Philadelphia Semiconductor Index technical levels, additional equity raises across the AI supply chain, and enterprise software AI monetisation data from Salesforce, ServiceNow, and SAP.