Vinyl Group secures Pedestrian Group for nominal consideration

Vinyl Group will acquire 100% of Pedestrian Group Pty Ltd from Nine Digital Pty Ltd for nominal consideration, with no material cash outlay, scrip issue, or ongoing royalties attached to the transaction. The capital-efficient acquisition is scheduled to complete on 15 June 2026 and is expected to contribute $0.6m-$0.8m in pro forma EBITDA during FY27.

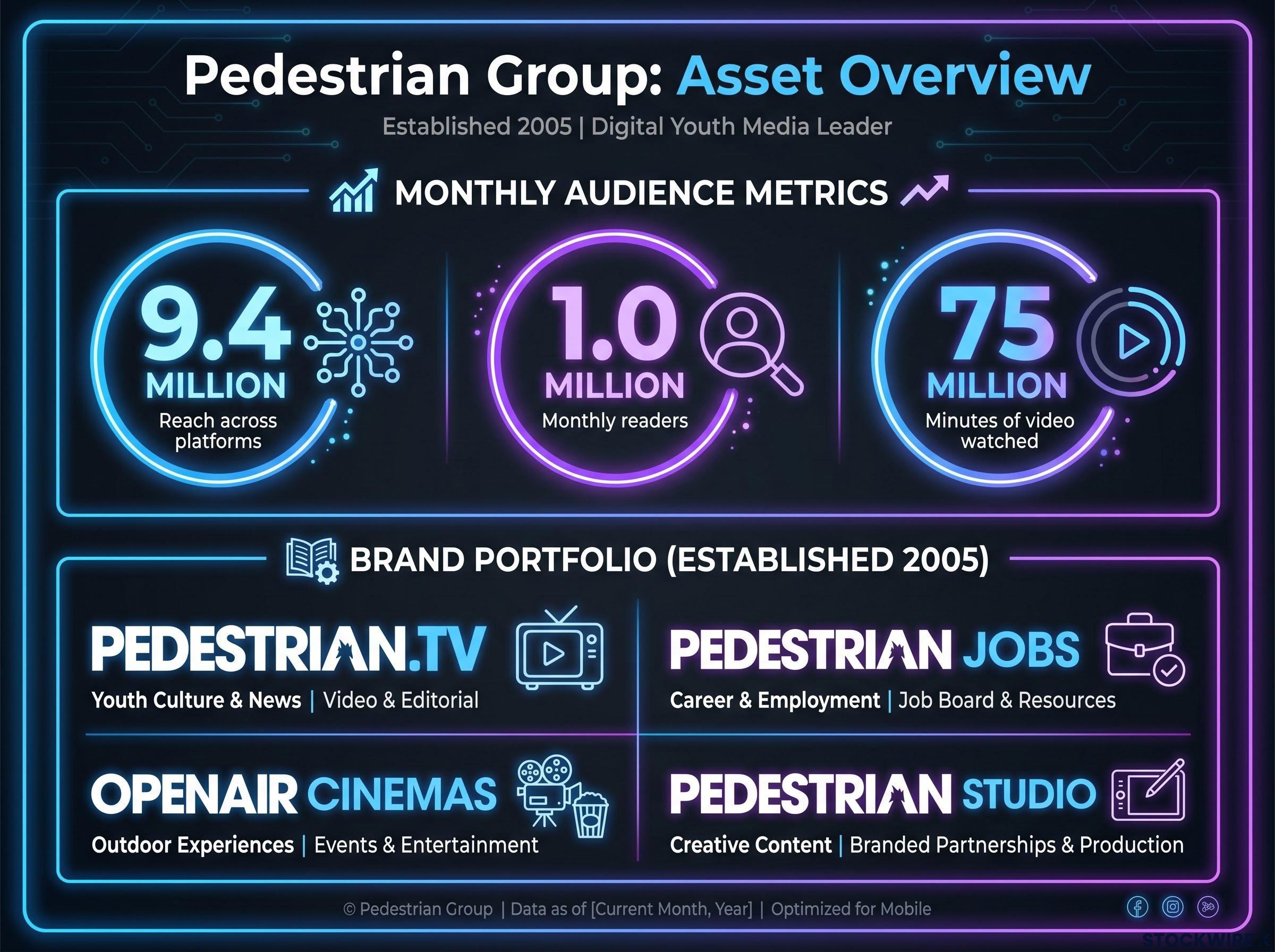

Pedestrian Group’s brand portfolio spans PEDESTRIAN.TV, Pedestrian Jobs, Openair Cinemas, and Pedestrian Studio. The acquisition increases Vinyl’s de-duplicated online audience reach from 51% to 53% of Australians online, measured on an Ipsos iris basis.

A nominal consideration acquisition that adds material EBITDA demonstrates disciplined capital allocation and validates management’s stated acquisition strategy of securing high-quality cultural assets through capital-efficient structures.

When big ASX news breaks, our subscribers know first

What the Pedestrian brand brings to Vinyl’s portfolio

Pedestrian Group operates as a recognised Gen Z and Millennial media brand, established in 2005, delivering content across web, social, video, newsletters, and experiential channels. The business generates revenue through multiple streams, including display advertising, native content, production, video, programmatic, BVOD, affiliate, and jobs-related activity.

Monthly audience metrics include:

- 9.4 million reach across owned, social, and distributed platforms

- 1.0 million monthly readers

- 75 million minutes of video content watched

- Active presence across Instagram, TikTok, Facebook, YouTube, LinkedIn, and newsletters

Diversified revenue streams reduce single-channel risk, while the established audience base offers immediate commercial value without customer acquisition costs. The scale of video engagement positions the asset for programmatic and BVOD monetisation opportunities.

What is de-duplicated audience reach?

De-duplicated audience measurement removes overlap when counting individuals who access multiple platforms or sites within a network. Ipsos iris tracks unique users across PC/laptop, smartphone, and tablet devices to provide an accurate count of distinct Australians reached, rather than inflated total impressions.

Advertisers value de-duplicated reach because it reveals the true size of an audience a brand can access through a media network. Reaching 53% of Australians online signals substantial scale and coverage, which increases pricing power when negotiating with advertisers seeking youth audience access. The metric matters for advertising revenue potential because brands pay premiums for networks that deliver broad, unduplicated reach across their target demographics.

The Pedestrian Group deal builds on momentum from the Val Morgan Digital acquisition completed in April 2026, which lifted Vinyl’s combined digital audience to approximately 51% of Australians online and added $2.5 million in annualised EBITDA.

Strategic rationale for the acquisition

Rebalancing licensed and owned IP

Vinyl Media’s current portfolio comprises licensed brands including Rolling Stone, Variety, LADbible, BuzzFeed, Refinery29, and POPSUGAR. Pedestrian Group introduces wholly owned original IP that reduces reliance on licensed arrangements, which typically carry revenue-sharing obligations or licensing fees.

Owned IP delivers higher margins and greater strategic flexibility than licensed brands. The acquisition creates opportunities to scale native content, social video, branded storytelling, events, newsletters, and jobs products across the broader group, leveraging Vinyl’s existing infrastructure.

Management noted the transaction rebalances the portfolio through a mix of licensed and wholly owned cultural assets, strengthening the company’s position in youth media.

Positioning as acquirer of choice

Vinyl Group’s stated strategy positions the company as the local partner of choice for international and sub-scale cultural assets. The company maintains executive leadership capability across editorial, commercial partnerships, production, technology, audience development, and operations, providing infrastructure for integrating acquired brands.

The capital structure of this transaction demonstrates management’s ability to negotiate favourable terms with vendors seeking strategic exits rather than financial returns.

Vinyl Group’s approach to capital-efficient media acquisitions has been consistent across recent transactions, with the Val Morgan Digital deal in early 2026 structured through a shareholder loan facility that preserved balance sheet flexibility while delivering immediate revenue accretion.

Josh Simons, CEO

“Pedestrian Group is one of Australia’s most recognisable youth media brands, with a distinctive voice, loyal audience and strong reputation in culture and entertainment. The addition of Pedestrian’s brand further rebalances Vinyl’s portfolio of cultural assets through a mix of licensed and wholly owned, original IP. The transaction also reflects the strength of Vinyl Group’s acquisition strategy. We are continuing to secure high-quality cultural assets through capital-efficient structures, validate our adaptive media flywheel, and build Vinyl into the acquirer of choice for subscale youth, culture and entertainment brands in Australia.”

Key transaction terms at a glance

| Term | Detail |

|---|---|

| Target | Pedestrian Group Pty Ltd (100% share capital) |

| Vendor | Nine Digital Pty Ltd |

| Consideration | Nominal (no material cash, no scrip, no royalties) |

| Expected completion | 15 June 2026 |

| FY27 EBITDA contribution | $0.6m-$0.8m (pro forma) |

The structure requires implementation of a restructure plan to achieve the stated EBITDA contribution range.

What this means for Vinyl Group’s investment case

The acquisition delivers several strategic benefits for shareholders:

-

Capital-efficient growth through nominal consideration structure: No material cash, scrip, or ongoing royalties preserves balance sheet capacity for future transactions.

-

Immediate EBITDA contribution ($0.6m-$0.8m in FY27): Pro forma earnings accretion within the first full financial year of ownership.

-

Increased advertiser relevance via expanded audience reach (53% of Australians online): Enhanced scale strengthens commercial positioning with brands seeking youth audience access.

-

Portfolio diversification through wholly owned youth media IP: Reduces reliance on licensed brands and introduces margin improvement potential.

-

Demonstrates execution capability on stated acquisition strategy: Validates management’s ability to secure strategic assets through disciplined valuation frameworks.

The transaction validates management’s “adaptive media flywheel” strategy, which aims to integrate cultural assets across a scaled platform whilst maintaining focus on sustainable profitability. The nominal consideration structure demonstrates execution of capital-efficient M&A rather than growth at any price.

Next steps and integration

Completion is scheduled for 15 June 2026, with Vinyl Group assuming operational control from that date. The company has an executive leadership team in place across editorial, commercial partnerships, production, technology, audience development, and operations to support integration.

Management has outlined a restructure plan that will be implemented post-completion to achieve the targeted $0.6m-$0.8m pro forma EBITDA contribution in FY27. Near-term completion and existing integration capability reduce execution risk associated with the transaction.

Want the Next Media Breakout in Your Inbox?

Join 20,000+ investors getting FREE breaking ASX news delivered within minutes of release, complete with in-depth analysis. Click the “Free Alerts” button at StockWire X to receive real-time coverage of capital-efficient deals, strategic acquisitions, and market-moving announcements the moment they break.