Vinyl Group Snaps Up Time Out Australia and Pedestrian to Hit 55% of Aussies

Vinyl Group acquires Time Out Australia and Pedestrian Group for nominal consideration

Vinyl Group has acquired two prominent Australian media assets—Time Out Australia and Pedestrian Group—for nominal consideration, positioning itself as the preferred acquirer for international cultural brands and sub-scale publishers seeking local presence. The dual acquisition expands Vinyl’s de-duplicated online audience reach to 55% of Australians online (Ipsos iris, January 2026), placing the company alongside Australia’s largest media organisations in national scale.

Time Out Australia, one of the world’s most recognised urban culture brands, operates under a long-term franchise agreement with Time Out England and is currently profitable with an expected positive EBITDA contribution in FY27. Pedestrian Group, one of Australia’s most recognised youth media businesses acquired from Nine Digital Pty Ltd, is forecast to contribute $0.6m–$0.8m in EBITDA during FY27 whilst rebalancing Vinyl’s portfolio with original intellectual property.

The transactions demonstrate capital-efficient M&A execution, securing strategic assets through increasingly favourable valuations and structures whilst materially expanding advertiser relevance. The company noted an agentic AI-first strategy is under development, with a comprehensive update to accompany FY26 results.

When big ASX news breaks, our subscribers know first

What is de-duplicated audience reach and why does it matter?

De-duplicated audience reach measures unique individuals who engage with a media organisation’s content across multiple platforms, rather than counting total page views or impressions that may include the same person multiple times. A user who reads an article on a desktop browser, later views content on a smartphone app, and shares a post on social media registers as one unique person in de-duplicated metrics, not three separate “impressions.”

This metric matters for advertisers because it provides an accurate picture of actual human reach rather than inflated engagement counts. Traditional impression metrics can overstate audience size when the same individuals repeatedly interact with content across devices and channels. De-duplicated measurement reveals how many distinct Australians a media organisation can deliver to brands, making it the preferred evaluation metric for sophisticated marketing teams allocating budgets.

Vinyl’s ability to offer advertisers verified access to over half of Australians online—measured through Ipsos iris, the industry standard for digital audience measurement—creates competitive positioning against both legacy broadcasters and social platforms. This reach threshold positions the company alongside major Australian media organisations whilst maintaining niche targeting capabilities that mass-market broadcasters cannot replicate.

Audience scale rivals Australia’s largest media organisations

Vinyl’s combined portfolio now competes directly with established media conglomerates for advertiser budgets, a position achieved through strategic M&A rather than capital-intensive organic audience building. The company’s 55% de-duplicated reach across all content categories places it fifth among major Australian media organisations measured by Ipsos iris in January 2026.

| Organisation | All Categories Reach |

|---|---|

| News Corp Australia | 81% |

| Nine | 69% |

| ABC | 63% |

| Vinyl Media (combined) | 55% |

| Seven West Media | 50% |

The comparison draws on Ipsos iris data for Australians aged 14+ across PC/Laptop, Smartphone and Tablet devices. Vinyl Media figures represent a combined brand group audience including Vinyl Media, Val Morgan Digital, Time Out and Pedestrian entities.

The Val Morgan Digital completion in April 2026 marked the preceding step in this audience build-out, adding $10.7 million in CY25 revenue and novating brand licences for BuzzFeed, Fandom, LADbible Group, and Vox Media to Vinyl across Australia and New Zealand.

Within the news category specifically, Vinyl’s combined assets reach 54% of Australians online, trailing News Corp Australia (63%), Nine (55%), and ABC (55%). This dual positioning—competitive scale in news alongside cultural and entertainment verticals—enables the company to offer advertisers both mass reach and niche targeting within a single integrated offering.

The Adaptive Media thesis explained

Adaptive Media represents an integrated advertising model where cultural assets, technology and distribution channels work together to deliver meaningful brand connections at scale. The company defines this as a structural evolution beyond legacy broadcast media (which offers mass reach but fragmenting audiences and declining viewership among under-40 demographics) and social media platforms (which provide cheap awareness and microtargeting capabilities but rely on interruptive ad formats and face increasing regulatory constraints on data-driven targeting).

The value proposition centres on advertisers achieving three outcomes simultaneously: mass audience reach, niche demographic targeting, and meaningful brand connections embedded within cultural content rather than interrupting it. Legacy broadcast media cannot deliver niche targeting at scale; social platforms cannot deliver meaningful brand integration beyond standard ad units. Vinyl’s ecosystem of premium cultural assets—spanning music, urban culture, youth media, and entertainment—enables campaigns to reach specific audience segments through editorially integrated content, live events, creator collaborations, and technology-enabled distribution.

Why advertisers are shifting spend

The company delivered over 300 Adaptive Media campaigns in 2025, with brands increasingly allocating budgets to multi-channel activations that combine owned media properties, technology platforms, and cultural moments. Three factors drive this shift:

- Fragmenting traditional audiences force brands to either accept declining reach through legacy broadcast channels or fragment budgets across dozens of digital platforms, increasing complexity and reducing efficiency.

- Social platform limitations restrict meaningful brand storytelling to standard ad formats whilst regulatory changes constrain microtargeting capabilities that previously justified platform spend.

- Measurable ROI from integrated campaigns demonstrates superior outcomes compared to isolated channel spending, with brands achieving both awareness metrics and deeper engagement signals through culturally embedded activations.

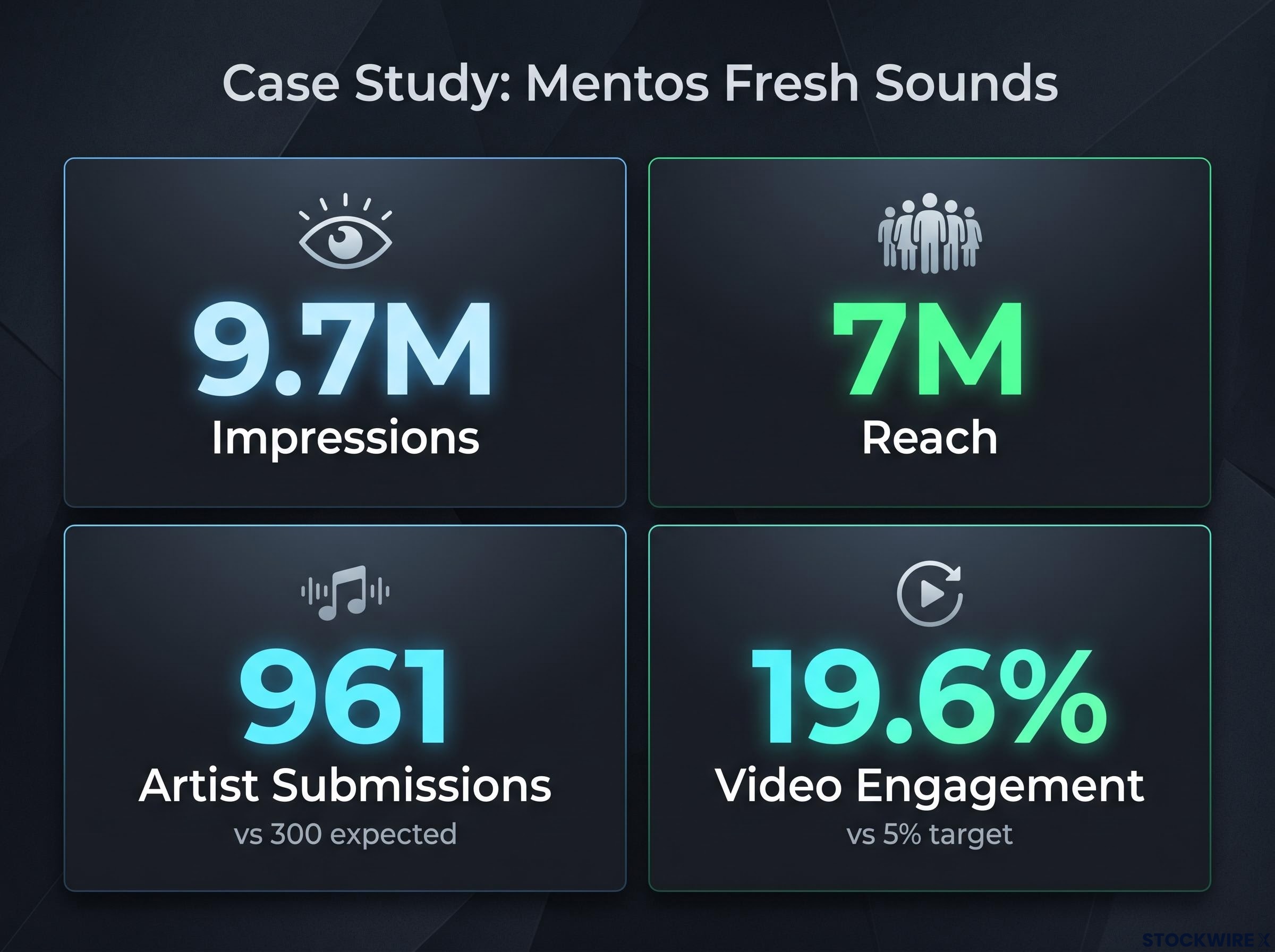

The Mentos Fresh Sounds campaign demonstrates the model’s commercial viability. The multi-layered discovery platform positioned Mentos as a champion of new Australian music through a combination of dedicated campaign website, weekly sponsorship integration, video series, editorial content, live event activation at SXSW, and content collaboration portals for emerging artists. The campaign delivered 9.7M impressions and 7M reach, exceeding booked benchmarks whilst driving 961 artist submissions compared to the 300 expected, demonstrating active audience participation rather than passive ad exposure. Video engagement reached 19.6% against a 5% target, materially outperforming standard social video benchmarks.

Portfolio strategy creates a self-reinforcing flywheel

The acquisition rationale for both assets reflects Vinyl’s positioning as the preferred exit partner for cultural media businesses that have reached scale constraints. Time Out Australia brings one of the world’s most recognised urban culture brands to the portfolio, currently profitable and operating under a long-term franchise agreement with Time Out England. The transaction confirms Vinyl as the preferred Australian partner for international cultural digital assets seeking local presence without the capital requirements and operational complexity of independent scaling.

Pedestrian Group, acquired from Nine Digital Pty Ltd, adds one of Australia’s most recognised youth media businesses whilst rebalancing the portfolio with original intellectual property distinct from licensed international brands. The transaction confirms Vinyl as the acquirer of choice for sub-scale publishers that have built audience trust and cultural relevance but lack the diversified revenue base and technology infrastructure required for standalone profitability.

The Pedestrian Group acquisition introduces wholly owned original IP into Vinyl’s portfolio, reducing the company’s reliance on licensed international brands and adding a monthly audience of 9.4 million across owned, social, and distributed platforms.

The portfolio additions strengthen the flywheel mechanics that underpin Vinyl’s strategic model:

- Time Out Australia (long-term franchise agreement with Time Out England)

- Pedestrian Group (acquired from Nine Digital Pty Ltd)

Growing audience scale attracts brands seeking efficient access to culturally engaged demographics. Successful Adaptive Media campaigns compound ecosystem value by demonstrating measurable ROI, encouraging repeat advertiser spend and larger integrated activations. Scale benefits enable further acquisitions at capital-efficient valuations, as sub-scale operators recognise Vinyl’s distribution infrastructure, technology capabilities, and advertiser relationships as force multipliers for their existing audiences. Each acquisition strengthens Vinyl’s negotiating position for future deals whilst expanding the revenue base that supports the pathway to profitability.

Pathway to first EBITDA-positive year in FY27

The company has forecast consolidated FY27 EBITDA of $3.5 million, representing its first EBITDA-positive year underpinned by scale benefits and a strategic focus on higher-margin revenue streams. Consolidated FY27 revenue is expected to reach $37–$40 million, representing approximately 100% revenue growth year-on-year, though the forecast assumes some revenue duplication from overlapping assets, products and customers to be worked through during the financial year.

Management acknowledged the advertising market remains soft due to geopolitical uncertainty and buyer hesitation, with the profitability pathway described as clear but not linear. Expected integration and market-related volatility, amplified by seasonal advertising spend patterns, may create quarter-to-quarter fluctuations in the trajectory toward sustained EBITDA-positive performance.

FY27 Profitability Guidance

The company’s forecast assumes Time Out Australia will contribute positive EBITDA whilst Pedestrian Group is expected to deliver $0.6m–$0.8m in EBITDA. The combined effect of these acquisitions, alongside existing portfolio optimisation and scale efficiencies, positions FY27 as an inflection point from growth-stage losses to structural profitability.

The transition from M&A-led revenue growth and diversification to operational optimisation and profitability represents a strategic shift in capital allocation. Whilst acquisitions remain a component of the growth model—particularly where assets can be secured at nominal consideration—the focus has shifted toward extracting margin improvement from the existing portfolio through technology investment, process alignment, and advertiser relationship deepening.

Near-term catalysts and integration timeline

The company outlined four key execution milestones for investors to track management delivery against stated objectives:

- Q4 FY26: Integration of Val Morgan Digital, Time Out and Pedestrian into unified technology infrastructure and commercial operations

- 1H FY27: Achieve EBITDA-positive run-rate across the combined business, demonstrating sustained profitability rather than single-quarter results

- FY27: Focused technology investment to enhance the flywheel, with the agentic AI-first strategy under development to receive comprehensive update alongside FY26 results

- FY27 and beyond: International growth through licensing, franchise and M&A opportunities, leveraging Vinyl’s Adaptive Media model and technology platform beyond Australian market constraints

The Q4 FY26 integration timeline for three significant acquisitions completed across a 12-month period represents the most operationally intensive near-term catalyst. Management’s ability to execute this integration will determine whether the EBITDA-positive run-rate milestone in 1H FY27 remains achievable.

The technology investment focus in FY27, particularly the agentic AI-first strategy, positions Vinyl to automate content production, personalise audience engagement, and optimise campaign delivery at scale. This capability becomes increasingly critical as the portfolio expands—manual editorial processes that supported 10-15 media properties cannot efficiently serve 30+ assets without technology-enabled workflow automation.

The next major ASX story will hit our subscribers first

Defensive moat through ecosystem complexity

The structural barriers to replicating Vinyl’s Adaptive Media business model create defensibility that compounds as the ecosystem scales. Five factors underpin this competitive positioning:

- Hard to replicate: Combining a large number of cultural assets into an integrated and immersive ecosystem requires capital, operational expertise, technology infrastructure, and sequential M&A execution over years. New entrants cannot shortcut this through organic audience building or single large acquisitions.

- Scale required for profitability: Delivering meaningful brand connections at competitive price points demands diversified revenue streams, shared technology infrastructure, and sufficient advertiser volume to justify dedicated sales resources. Sub-scale operators cannot achieve unit economics that support standalone profitability.

- Technology as core capability: Internally developed AI publishing suite aligns with current workflow requirements and enables rapid content production across dozens of properties. Off-the-shelf content management systems lack the integration depth and customisation required for Vinyl’s multi-property model.

- Dual content creation capability: Adaptive Media campaigns require both mass-distribution content (social media, programmatic advertising) and bespoke cultural activations (live events, creator collaborations, editorial integrations). Social platforms are a distribution component, not a direct competitor to the full-service model.

- Platform independence: The business model does not depend on any single social media platform, publisher, or algorithm for audience reach or revenue generation. Diversification across owned properties, licensed brands, and technology platforms insulates Vinyl from platform policy changes or algorithm updates that disrupt pure-play social publishers.

The self-reinforcing flywheel effect differentiates Adaptive Media from transaction-based advertising models. Consumers, creators, and brands all benefit as the ecosystem grows—audiences gain access to more cultural content and experiences, creators reach larger engaged communities through Vinyl’s distribution infrastructure, advertisers achieve better campaign outcomes through expanded inventory and integration options. Value compounds across campaign cycles rather than resetting with each transaction, creating structural advantages over pure-play social platforms and declining legacy broadcast media.

Don’t Miss the Next Tech Breakthrough

Join 20,000+ investors getting FREE breaking ASX news delivered to your inbox within minutes of release, complete with in-depth analysis. Click the “Free Alerts” button at StockWire X to start receiving real-time alerts the moment market-moving announcements hit the ASX.