Passive Income Investing in Australia: What Actually Works

1 hr ago

Canadian retail margin debt hit $47.3 billion in January 2026, a 23% year-over-year increase that placed the figure within $1 million of its November 2025 peak. The number is large enough to suggest margin is no longer a niche tool for day traders and momentum speculators. Yet most public discussion of margin still treats it that way, as if borrowing against a portfolio is inherently aggressive regardless of the amount, the purpose, or the plan behind it.

A growing subset of income-focused investors in Canada are using margin in small, deliberate quantities. The purpose is not to amplify speculative bets. It is to bridge temporary income gaps, supplement yield during life transitions such as parental leave or career changes, and avoid selling core dividend-generating holdings at inopportune moments. This approach rarely makes headlines precisely because it is quiet and incremental.

What follows unpacks what a conservative margin strategy actually looks like in practice for income investors: what the numbers mean, what the only publicly verifiable Canadian benchmark says, how a real investor is applying it, and what guardrails separate a defensible position from one that quietly becomes dangerous.

The instinct to keep margin away from an income portfolio is understandable. Margin amplifies risk. Income investing is built on stability and predictable cash flow. The two appear structurally incompatible.

That framing holds when margin is used aggressively, when an investor borrows to increase position size in pursuit of capital gains, pushing utilisation toward brokerage maximums with no defined exit. It does not hold as neatly when the borrowing is modest, time-limited, and backed by a portfolio of dividend-generating securities that continues to produce yield on the underlying holdings regardless of the margin balance.

The distinction matters because the two use cases carry fundamentally different risk profiles:

Whether leverage builds or destroys wealth over time hinges on a single condition: the cost of the borrowed capital must be reliably lower than the after-tax return generated by the assets it funds, a hurdle that becomes structurally harder to clear as interest rates rise and dividend yields compress.

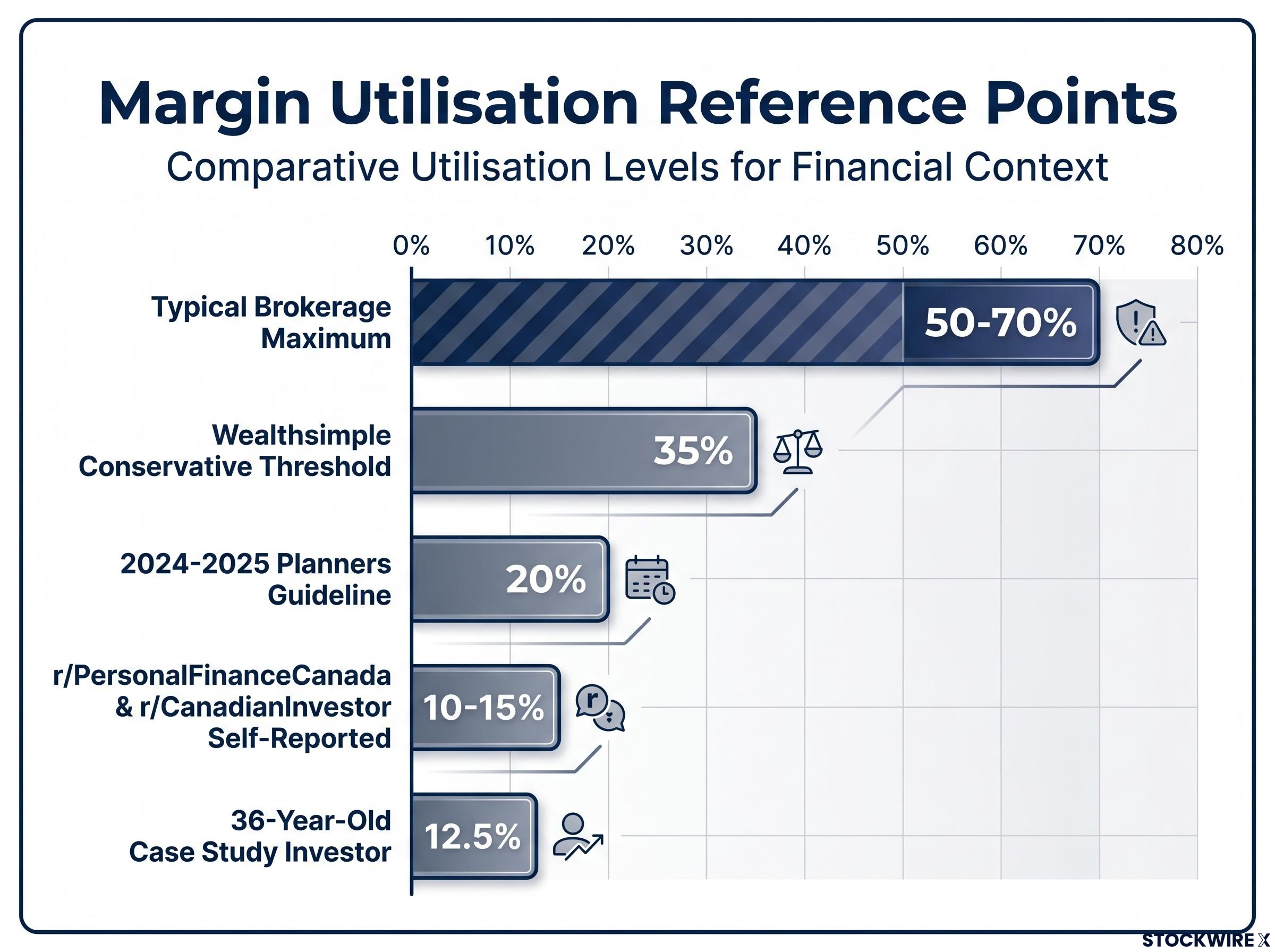

The $47.3 billion in Canadian margin debt reported by CIRO (the Canadian Investment Regulatory Organization) in January 2026 confirms that margin use is widespread. What it does not confirm is how much of that borrowing falls into each category. Major Canadian brokerages publish security-level margin requirements but do not classify overall account utilisation levels as conservative or aggressive, a gap that leaves income investors without a clear benchmark.

The CIRO monthly client margin debt statistics track aggregate retail borrowing across Canadian brokerages, providing the only official national data series that contextualises whether individual utilisation levels sit above or below the broader market trend.

Search for an official definition of conservative margin utilisation at any of Canada’s major brokerages and the result is the same: nothing.

Questrade, TD Direct Investing, RBC Direct Investing, and Interactive Brokers Canada all publish detailed margin requirements at the individual security level, consistent with CIRO rules. A given stock might carry a 30% margin requirement; another might sit at 50% or higher depending on volatility. These are security-level classifications. None of these institutions publishes a client-level utilisation band labelled conservative, moderate, or aggressive.

The exception is Wealthsimple. Its portfolio line of credit is the only identified Canadian retail platform that attaches a specific numeric threshold to the word “conservative.”

Wealthsimple’s portfolio line of credit documentation characterises borrowing up to 35% of eligible portfolio value as conservative by design, intended to provide a buffer against market swings.

That 35% figure is not a regulatory standard. It is a single platform’s product design choice. But it is the only publicly verifiable Canadian benchmark where the word “conservative” meets a specific number, and that makes it a useful reference point in a space where most guidance remains qualitative.

Knowing what threshold one platform calls conservative is a starting point. Knowing whether a specific margin position is financially defensible requires a calculation.

The concept is the yield spread: the gap between what a portfolio earns in after-tax dividend yield and what the margin balance costs in after-tax interest. If the spread is positive, the position has positive carry, meaning portfolio income exceeds the cost of borrowing. If it is negative, the investor is paying for the privilege of holding risk.

Commentary in the Financial Post and Globe and Mail during 2024-2025 noted that margin borrowing has become “considerably more expensive than during the ultra-low-rate era,” with the spread between dividend yield and margin interest narrowing materially relative to earlier periods.

That narrower spread makes the calculation more demanding, and the stress test that follows it more important. A yield spread that looks comfortable today can evaporate if rates rise or dividends are cut.

The yield spread under stress narrows faster than most investors model: in a scenario where variable margin rates exceed 10% per annum and a portfolio’s dividend yield holds at 5-6%, the positive carry that justified the position disappears entirely, leaving the investor funding interest from salary or other liquid reserves rather than portfolio income.

The stress test follows three steps:

The critical point: relying solely on portfolio yield to service margin interest violates the conservative framing entirely. Dividend cuts and margin calls can arrive simultaneously during a downturn, precisely when the investor is least able to cover the gap. Canadian financial advisors writing in MoneySense and Globe and Mail columns during 2024-2025 consistently stressed that conservative margin use assumes the investor can cover a margin call from external resources, not from forced asset sales.

A 36-year-old Canadian income investor provides a concrete example of this strategy in action. The investor manages a portfolio generating sufficient income to support family expenses and introduced margin deliberately to supplement yield during an extended period of family leave following the birth of a fourth child.

The margin was not introduced on impulse. It was a response to a defined life event with a foreseeable end point: parental leave, after which employment income would resume. Current margin utilisation sits at approximately 12.5% of the full portfolio value, a figure that is being actively reduced over time.

That 12.5% sits well below Wealthsimple’s stated 35% conservative threshold, roughly one-third of it. It also aligns with the range most commonly reported by self-described income investors in Canadian forums. Threads on r/PersonalFinanceCanada and r/CanadianInvestor during 2024-2025 documented investors using small margin balances against blue-chip dividend ETFs, with self-reported utilisation commonly falling in the 10-15% range for similar bridging purposes.

| Reference Point | Utilisation Level | Characterisation |

|---|---|---|

| Typical brokerage maximum | 50-70% (varies by security) | Regulatory / house maximum; no qualitative label |

| Wealthsimple conservative threshold | 35% | Explicitly labelled conservative by design |

| Case study investor | 12.5% | Actively declining; approximately one-third of labelled conservative threshold |

The investor does not apply margin to high-yield ETF positions themselves. This is a deliberate design choice. If yields on those positions were cut, the investor would not face a double failure: an income drop from the very holdings that were supposed to service the margin interest.

Instead, interest is serviced from salary and dividends generated across the broader portfolio. The margin balance exists as a separate supplementary tool, not as a lever attached to the portfolio’s highest-yielding components. Additional margin would only be considered in response to a specific external opportunity, and any increase would be kept minimal.

The yield spread calculation tells an investor whether a position is defensible today. Guardrails determine whether it stays defensible over time. Most margin blowups in income portfolios are not mathematical failures at the point of entry. They are discipline failures that accumulate quietly.

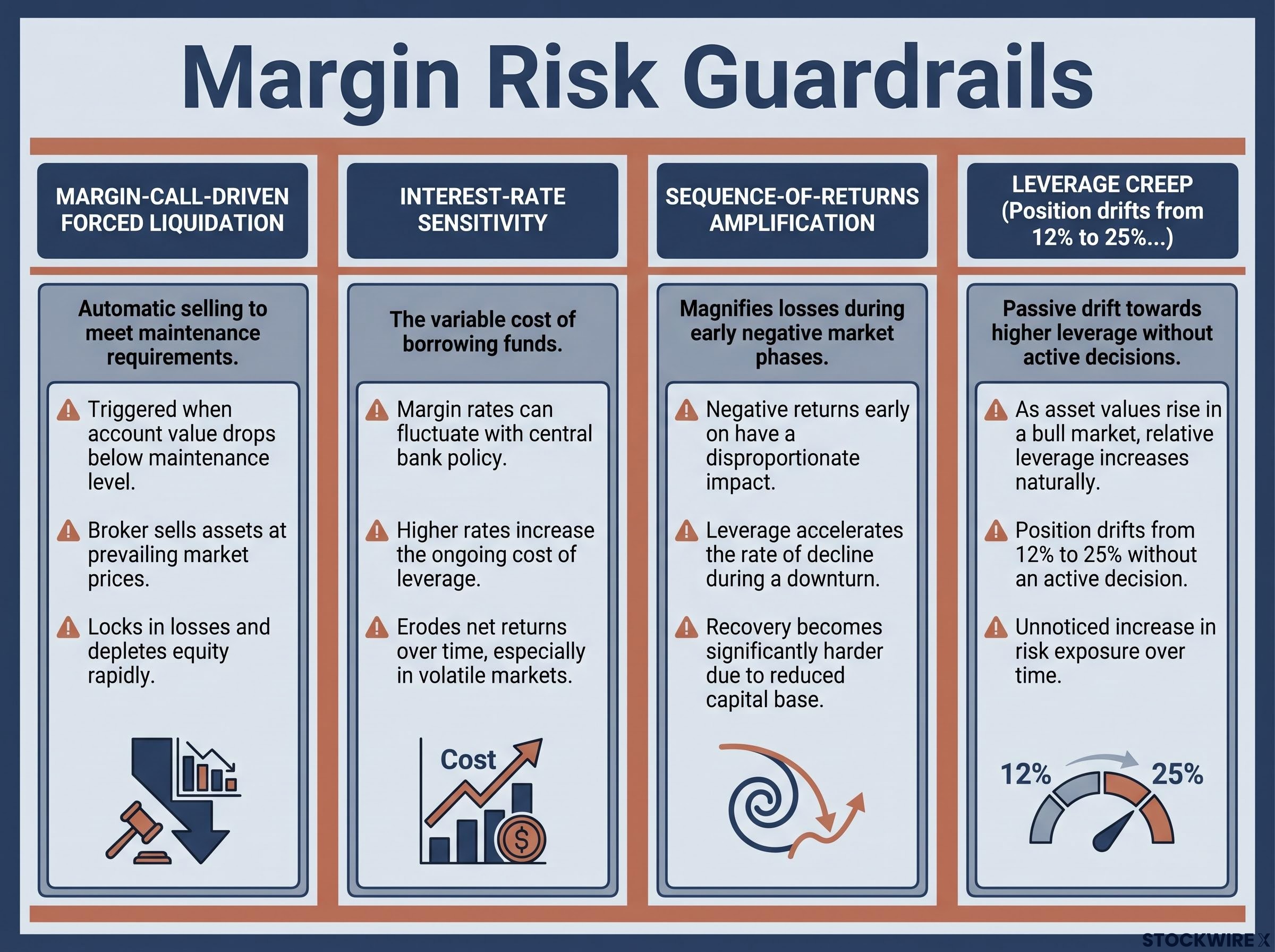

Four risk categories demand specific attention from income investors using margin:

The loan-to-value mechanics that govern margin call triggers operate the same way across jurisdictions: when falling asset prices push the outstanding balance above the lender’s maintenance threshold, the borrower faces a call that must be met within 24 hours, often regardless of whether the decline reflects temporary volatility or a sustained correction.

Leverage creep is particularly insidious because it is structurally invisible until it is too late. The investor makes no aggressive decision. The market simply rises, comfort increases, and the margin balance that once looked small relative to the portfolio begins to represent a materially different risk profile.

Canadian financial planners and bloggers writing during 2024-2025 cited informal personal guidelines: keeping investment leverage under 20% of investable assets, with very cautious investors staying in the single-digit to low-teens percent range. These are opinions, not formal thresholds, but they align with the utilisation ranges observed in real-world cases.

The antidote to leverage creep is a written personal leverage policy, a document that removes future decision-making from the moment when discipline is most likely to fail. Three elements belong in any such policy:

The tone here is practical, not prescriptive. The specific numbers depend on individual circumstances. What matters is that the policy exists in writing before it is needed, not as a mental note revisited under stress.

The income investors using margin well share a consistent profile. The borrowing is temporary, tied to a defined life event with a foreseeable end. Utilisation is modest, well below any labelled conservative benchmark and typically in the 10-15% range. Interest is serviced from external income rather than solely from portfolio yield. An active reduction plan is in place and being executed.

What conservative margin use is not: a permanent yield-enhancement mechanism, a substitute for adequate savings, or a strategy for investors who lack external income to service interest. If the margin balance becomes part of the portfolio’s baseline rather than a temporary supplement, the conservative label no longer applies regardless of the utilisation percentage.

“A conservative, time-limited use of margin, not a long-term lifestyle subsidy.”

That framing, drawn from Canadian dividend blog commentary during 2024-2025, captures the distinction more precisely than any single number can. Wealthsimple’s 35% threshold marks the outer boundary of what one Canadian platform explicitly calls conservative. Real-world income investors cluster well below it, in the 10-15% range, with declining balances and defined exit conditions.

The analytical question for any income investor considering or already using margin is specific: does your situation, your income sources, your utilisation rate, your yield spread under stress, and your written leverage policy, match the profile described throughout this article? If so, the tool may be appropriate for the defined purpose it serves. If not, the framework above identifies exactly where the mismatch sits.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

A conservative margin strategy involves borrowing a small, deliberate amount against a portfolio, typically well below 15% of total portfolio value, to supplement cash flow during defined life events rather than to amplify speculative bets, with interest serviced from external income sources.

Wealthsimple's portfolio line of credit is the only identified Canadian retail platform that attaches a specific number to the word conservative, characterising borrowing up to 35% of eligible portfolio value as conservative by design to provide a buffer against market swings.

You calculate the yield spread by subtracting your after-tax margin interest cost from your after-tax portfolio dividend yield, then stress-test the result by assuming margin rates rise 1-2 percentage points and by applying a meaningful partial dividend cut to confirm the spread remains positive under both scenarios.

Leverage creep occurs when a margin position that starts at a low utilisation level, such as 12%, drifts higher during a bull market without any single active decision, because rising portfolio values increase comfort and the original conservative posture quietly dissolves into a materially higher risk profile.

Investors should write a personal leverage policy that defines a maximum portfolio percentage threshold, specifies a reduction trigger if loan-to-value rises above a set level, and establishes an explicit prohibition on adding margin during market drawdowns.