BCA Research Says Warsh Has the AI Inflation Story Backwards

40 mins ago

A routine software update. No deliberate wrongdoing. A $205,350 penalty and nearly 15,000 affected trades. The Petra Capital case stands as one of the clearest recent illustrations of how technology risk and compliance oversight can diverge in ways firms never anticipate.

The Markets Disciplinary Panel (MDP) determination against Petra Capital Pty Ltd offers Australian finance professionals and sophisticated investors a detailed view of how market integrity regulation operates in practice. The case reveals the infrastructure underpinning every trade executed on ASX or Cboe Australia, and the consequences when that infrastructure fails silently. This analysis unpacks the penalty from root cause to regulatory implication, explains why client identifier accuracy sits at the heart of ASIC’s market surveillance capability, and distils the compliance obligations every market participant must meet to avoid a parallel outcome.

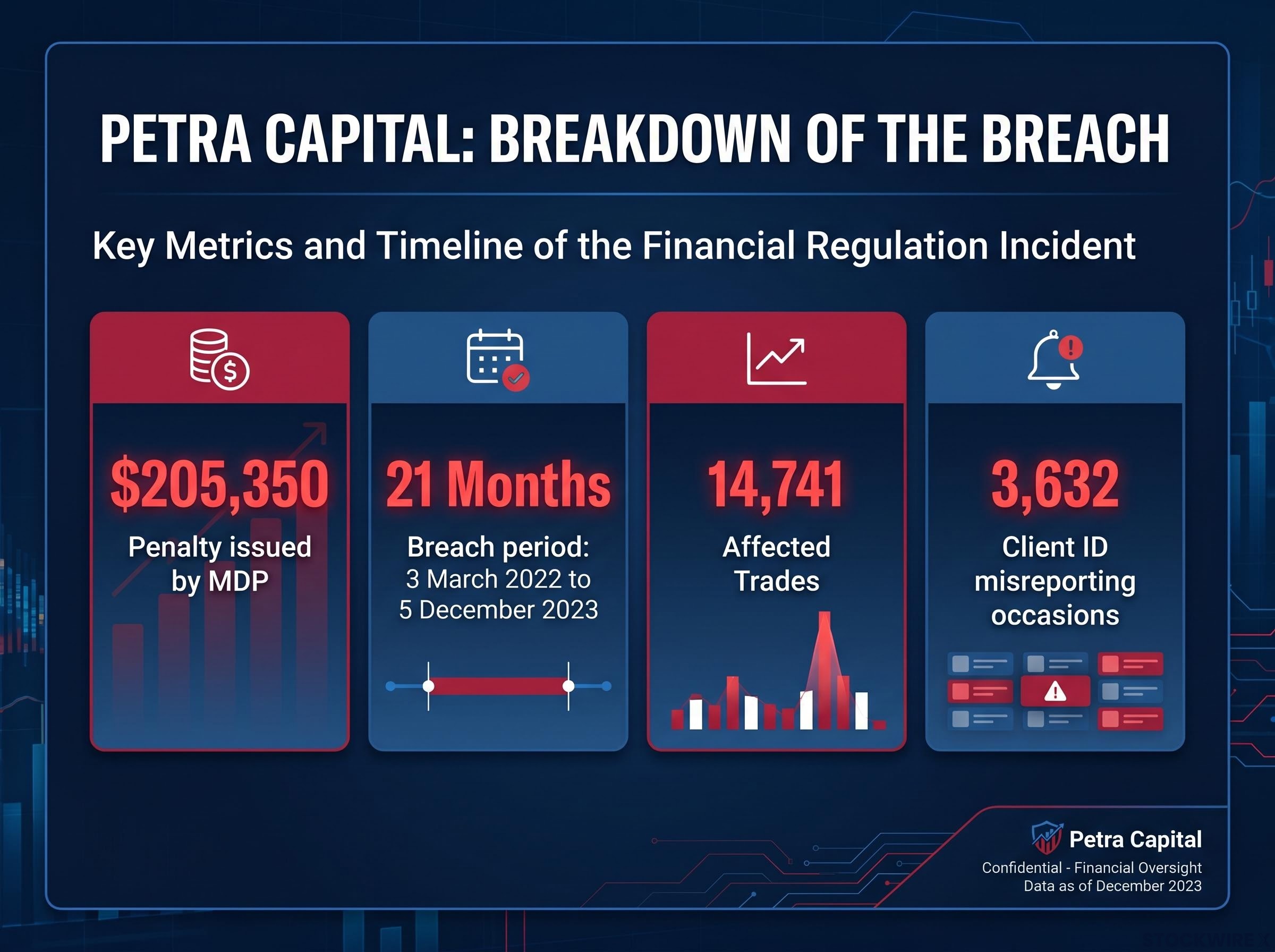

The numbers arrived before the explanation. The MDP issued Petra Capital an infringement notice carrying a $205,350 penalty for inaccurate regulatory data submissions spanning 3 March 2022 to 5 December 2023, a period of approximately 21 months. Across that window, a single client appeared as multiple distinct clients on 3,632 separate occasions, affecting 14,741 individual trades.

The key facts:

The root cause was a system update that corrupted how client identifiers were assigned or mapped within Petra Capital’s reporting platform. Not fraud. Not manipulation. A code-level change that went unverified.

The MDP classified the conduct as “careless,” determining the firm “should have proactively verified its reporting systems” and reviewed underlying coding assumptions. Compliance with the infringement notice does not constitute an admission of liability under the Corporations Act 2001.

Petra Capital holds market participant status on both ASX Limited and Cboe Australia Limited. The penalty was settled by payment.

A client reference identifier is a unique code that market participants must attach to orders and transactions when submitting regulatory trade data to ASIC. At the surface level, it is a piece of metadata. Below the surface, it is the mechanism that allows ASIC to link trading activity across accounts and over time.

Every trade executed on the ASX passes through layers of ASX trade infrastructure, including order matching, clearing, and settlement systems, before it reaches the regulatory reporting layer where client identifiers attach to the transaction record that ASIC receives.

That linkage forms the foundational dataset for detecting:

The MDP stated that supplying accurate regulatory data, including consistent client identifiers, represents a fundamental obligation for market participants. Without accurate identifiers, ASIC’s surveillance algorithms cannot connect the dots between trades that may, taken individually, appear unremarkable but collectively reveal a pattern of concern.

Corrupted identifier data fragments a client’s trading history into unlinked pseudonymous records. A single actor’s activity across many trades appears instead as a series of unrelated trades by unrelated parties.

In Petra Capital’s case, one client registered as multiple distinct entities on 3,632 occasions. ASIC’s ability to efficiently identify whether that client’s trading formed a pattern warranting investigation was directly impaired. The failure was not a paperwork error. It was a structural gap in the regulator’s surveillance capability.

The failure followed a sequence where each step made the next one foreseeable:

The MDP found that Petra Capital had not implemented sufficient periodic reviews of its reporting systems or the assumptions embedded in its reporting code. The system changed, but the oversight process designed to catch system-level errors did not activate. This was a governance failure layered on top of a technical one.

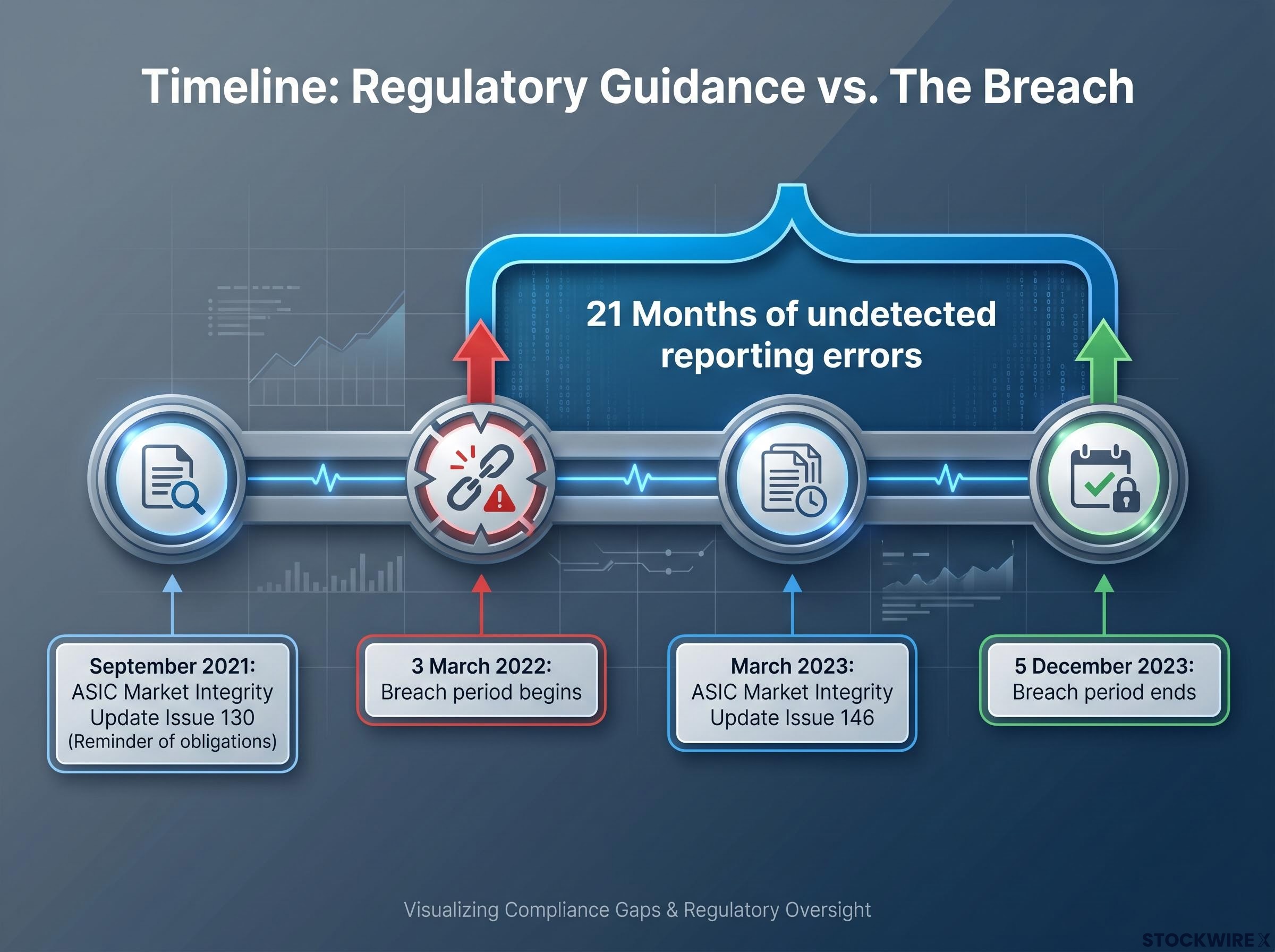

In September 2021, before the breach period began, ASIC had reminded market participants of their obligations to submit accurate and complete regulatory data through Market Integrity Update Issue 130, noting that infringement notices had already been issued for non-compliance at that time.

Market Integrity Update Issue 130, published by ASIC in September 2021, explicitly addressed regulatory data obligations and noted that infringement notices had already been issued for non-compliance, placing the market on formal notice of the enforcement risk well before Petra Capital’s breach period began.

The 21-month duration is the most instructive data point. An undetected reporting error compounded at scale, turning a single software change into thousands of regulatory violations. By the time the breach was resolved in December 2023, the damage was measured in five figures of affected trades and six figures in financial penalties.

ASIC and MDP guidance sets out minimum compliance obligations for market participant reporting systems. Three requirements stand out as directly relevant to the Petra Capital outcome:

The most recent identifiable ASIC guidance addressing these obligations was Market Integrity Update Issue 146, published in March 2023. ASIC’s earlier reminder in Market Integrity Update Issue 130 (September 2021) preceded the breach period entirely.

The gap between published guidance and Petra Capital’s conduct was direct:

| Compliance Obligation | What It Requires | Petra Capital’s Gap |

|---|---|---|

| Annual system testing | Review and test reporting systems at least once per year | No periodic review caught the identifier corruption across 21 months |

| Compliance staff involvement | Compliance personnel engaged in technical reporting functions | Post-update verification was not performed by compliance personnel |

| Third-party verification | Independent review even when external providers manage systems | Underlying coding assumptions went unreviewed after the system update |

Reliance on a third-party provider does not transfer the compliance obligation. Firms remain responsible for verifying their own regulatory reporting regardless of who builds or maintains their systems.

Continuous disclosure obligations sit alongside accurate regulatory data reporting as part of the broader compliance architecture ASIC enforces; the April 2026 Federal Court ruling against Electro Optic Systems confirmed that the obligation to disclose attaches at the point of internal awareness rather than board sign-off, and that personal liability for executives is now an active enforcement tool rather than a theoretical risk.

The $205,350 penalty against Petra Capital sits alongside a separate MDP infringement notice issued to CLSA Australia Pty Limited in August 2024, which carried a $144,300 penalty for incorrect regulatory data. Together, the two cases signal that data-accuracy enforcement is a consistent MDP priority, not an isolated action.

| Firm | Penalty | Date | Nature of Breach |

|---|---|---|---|

| Petra Capital Pty Ltd | $205,350 | Breach period: March 2022 to December 2023 | Incorrect client identifiers caused by system update |

| CLSA Australia Pty Limited | $144,300 | August 2024 | Incorrect regulatory data |

No comparable post-2024 case involving the specific system-update-to-client-identifier failure pattern has been publicly documented, positioning Petra Capital as a reference point without a close successor in this category.

An MDP infringement notice allows a firm to resolve an alleged breach by paying a penalty without the matter proceeding to court. Compliance with the notice does not constitute an admission of liability or a finding that subsection 798H(1) of the Corporations Act 2001 has been breached.

This distinction matters for how firms and investors interpret enforcement outcomes. A settled MDP notice is a regulatory cost and a deterrent signal. It is not a conviction. Firms assessing and communicating these events should frame them accordingly.

Technology changes faster than compliance reviews. The gap between a system update and the next scheduled verification is where regulatory risk accumulates, and the Petra Capital case quantifies that gap precisely: 21 months of undetected misreporting against a minimum annual review requirement. That represents at least two missed review cycles.

The MDP’s classification of the conduct as “careless” sends a clear signal. Regulators do not require intent to find a breach. A failure to take reasonable precautionary steps is sufficient. As trading systems become more automated and reliant on third-party infrastructure, the compliance obligation to independently verify reporting accuracy grows more important, not less.

ASIC’s enforcement posture has hardened considerably since the breach period opened for Petra Capital; the regulator established a dedicated insider trading team in late 2024, carried insider trading as a formal enforcement priority into both 2025 and 2026, and demonstrated through the Rodney Forrest prosecution that custodial sentences are the intended deterrent outcome for serious market conduct failures.

ASIC’s ongoing Market Integrity Update series remains the mechanism by which firms are expected to stay current on reporting obligations. The regulator had flagged these obligations before Petra’s breach period began.

Any compliance officer reading this case should be asking:

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The Petra Capital penalty was not a product of misfortune. It was the result of a governance gap that ASIC had publicly flagged before the breach period began. The MDP’s determination reinforces a straightforward standard: annual system testing, compliance staff involvement in technical reporting functions, and independent verification when third-party providers are used.

These three obligations form the practical framework that separates firms that catch system-level errors from firms that discover them 21 months later, measured in thousands of affected trades and six-figure penalties. Enforcement outcomes like this one define the standards that protect all market participants, including the investors whose trades depend on accurate surveillance data. The compliance challenge Petra Capital illustrates is not historical. It is structural, and it intensifies with every system update that goes unverified.

An MDP (Markets Disciplinary Panel) infringement notice allows a firm to resolve an alleged regulatory breach by paying a financial penalty without the matter proceeding to court, and compliance with the notice does not constitute an admission of liability under the Corporations Act 2001.

A software update corrupted how client identifiers were mapped within Petra Capital's regulatory reporting platform, causing one client to appear as multiple distinct clients across 3,632 occasions and 14,741 individual trades over approximately 21 months without detection.

Client reference identifiers allow ASIC to link trading activity across accounts and over time, forming the foundational dataset used to detect market manipulation and insider trading; corrupted identifiers fragment a client's trading history into unlinked records that undermine surveillance algorithms.

ASIC guidance requires market participants to test and review their reporting systems at least once per year, ensure compliance staff are meaningfully involved in technical reporting functions, and conduct independent verification even when third-party providers manage their systems.

The $205,350 penalty against Petra Capital is the largest in this category of recent data-accuracy cases, compared to a $144,300 infringement notice issued to CLSA Australia in August 2024 for incorrect regulatory data, signalling that data-accuracy enforcement is a consistent MDP priority.