Marvell Technology Surges 22% on Nvidia CEO’s Trillion-Dollar Call

7 hrs ago

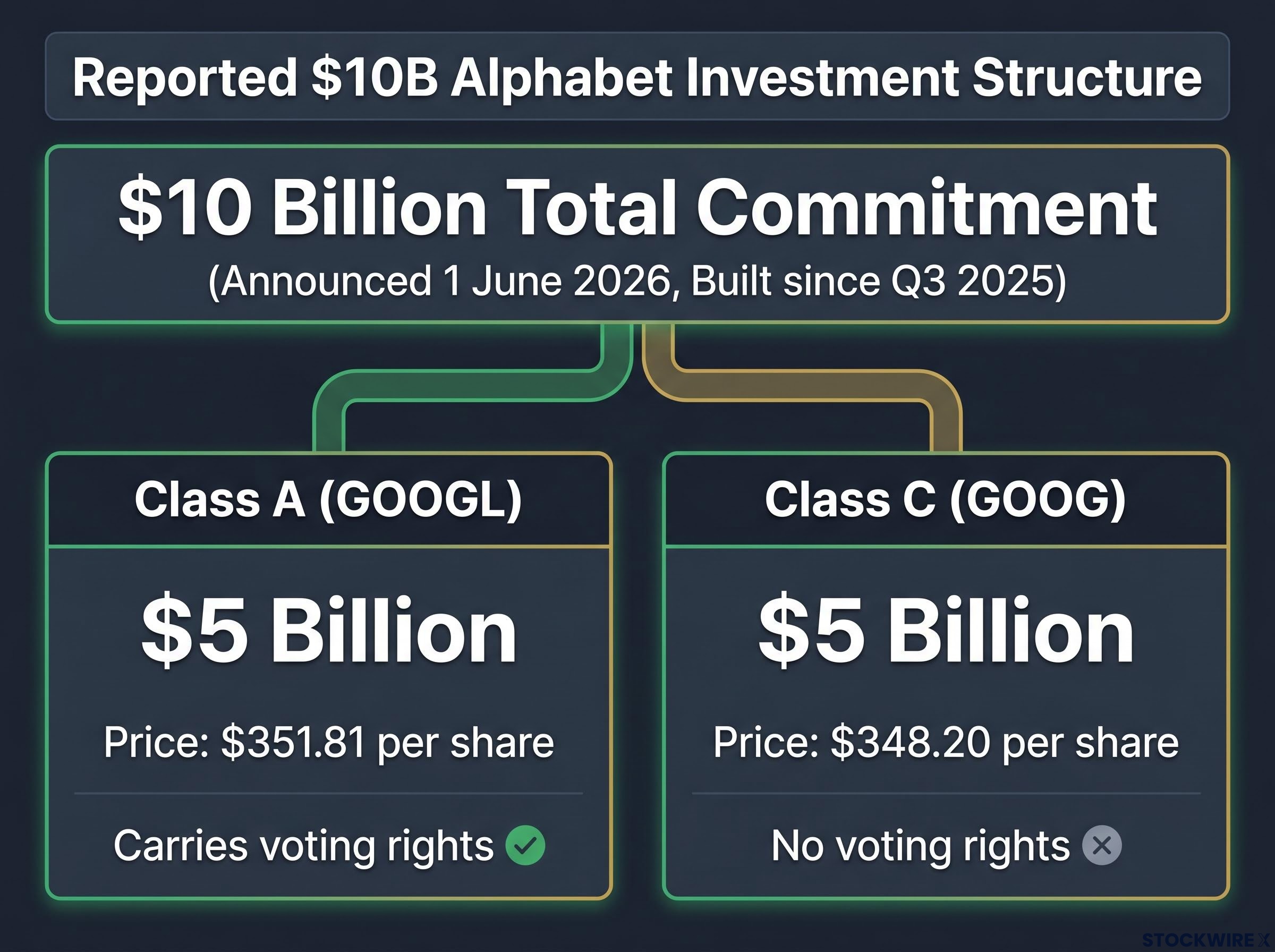

Berkshire Hathaway has reportedly committed $10 billion to Alphabet Inc. through a private placement split across two share classes, a move attributed to reporting by Investing.com citing Alphabet and announced on 1 June 2026. The scale alone would make this one of the largest single technology investments in Warren Buffett’s career. It arrives after decades of documented caution toward fast-changing technology businesses, and in the middle of an institutional cycle that has channelled enormous capital into AI-hyperscaler equities. The transaction details have not yet been independently confirmed through regulatory filings or major financial newswires, a sourcing context this article addresses directly. What follows covers the reported deal structure, the Google Cloud metrics that appear to underpin the thesis, Buffett’s documented evolution as a technology investor, and what the institutional signal means for investors weighing Alphabet exposure.

The reported deal structure is specific. Berkshire Hathaway is said to have committed $10 billion to Alphabet, split evenly between two share classes: $5 billion into Class A shares (GOOGL) at $351.81 per share, and $5 billion into Class C shares (GOOG) at $348.20 per share.

Reported total commitment: $10 billion, split across GOOGL and GOOG in a private placement announced 1 June 2026.

The distinction between the two classes matters. Class A shares carry voting rights; Class C shares do not. The even split suggests a position sized for economic exposure rather than governance influence, though the specific terms of the private placement, including any lock-up periods, board representation, or governance provisions, have not been disclosed.

| Share Class | Ticker | Amount Invested | Price Per Share |

|---|---|---|---|

| Class A | GOOGL | $5 billion | $351.81 |

| Class C | GOOG | $5 billion | $348.20 |

According to the same reporting, Berkshire began building its Alphabet position during Q3 2025, making the 1 June 2026 announcement the formalisation of a longer accumulation strategy. All deal details are attributed to Alphabet Inc. via Investing.com. At time of publication, no independent SEC filing or confirmation from a major financial newswire had been identified. Readers should treat this as a sourcing status to monitor rather than a factual dispute; the verification pathway is addressed in this article’s closing section.

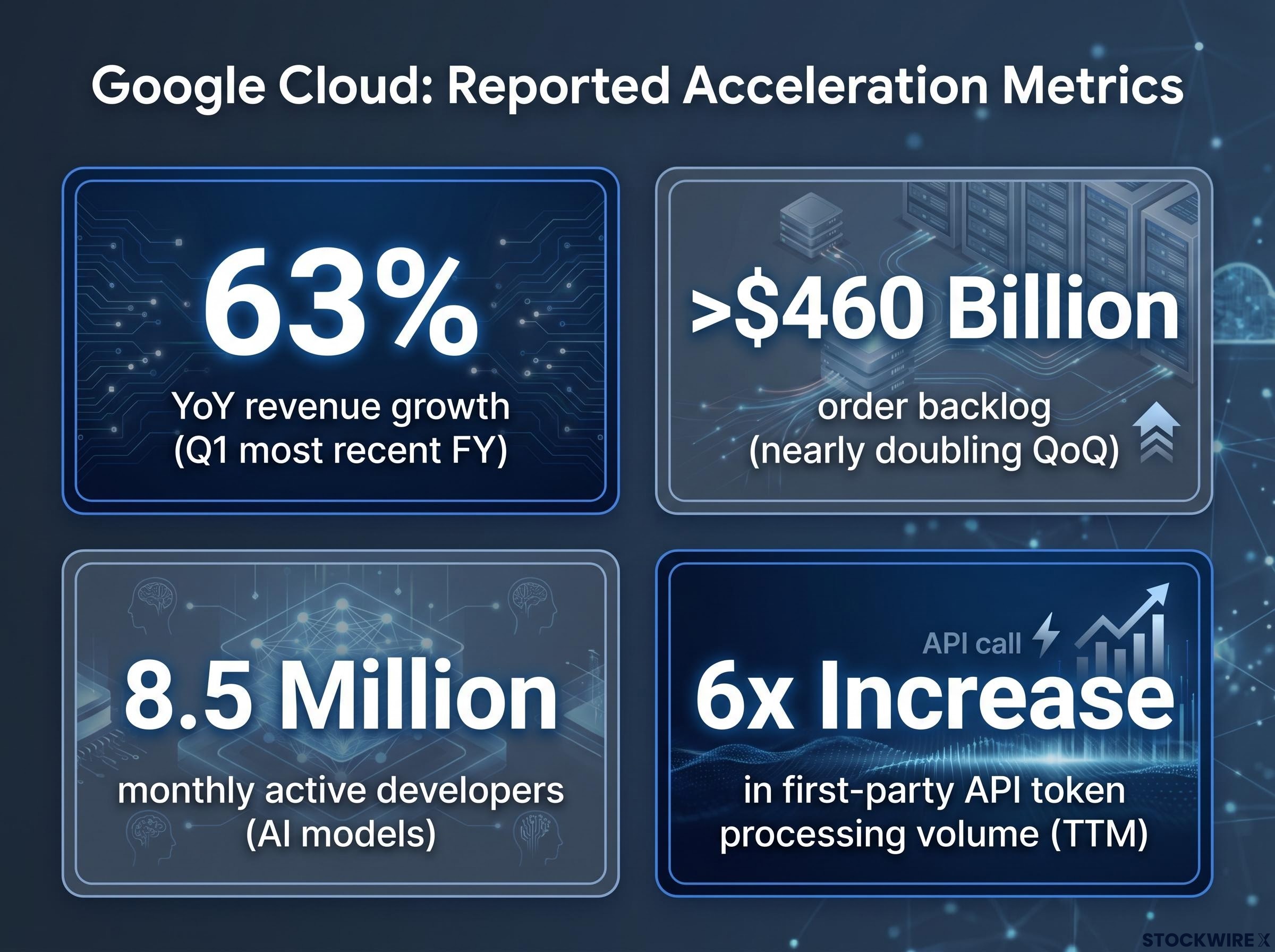

The business metrics attributed to Google Cloud in the same reporting paint a picture of acceleration across several dimensions:

Each of these figures is sourced from reporting attributed to Alphabet and Investing.com and has not been independently confirmed at time of publication.

Through a value-investor lens, the order backlog figure stands out. Berkshire has historically favoured businesses with durable, compounding cash flows and strong competitive moats. A cloud platform with a rapidly growing backlog of contracted enterprise commitments fits that template more closely than a speculative AI bet.

Cloud order backlog represents contracted but not-yet-recognised revenue. When enterprise customers sign multi-year cloud infrastructure agreements, those commitments enter the backlog and convert to recognised revenue over the life of the contract. The figure gives investors visibility into future spending that has already been committed, reducing reliance on quarterly booking momentum alone.

A near-doubling in a single quarter, if confirmed, would indicate an acceleration in enterprise AI adoption at Alphabet’s infrastructure layer. For readers who follow equities but may not track cloud-specific accounting metrics, the backlog is best understood as a forward-looking measure of demand already locked in, distinct from current-quarter revenue.

Buffett’s caution toward technology is not a myth. It is a documented, decades-long philosophical position rooted in his preference for businesses whose economics he can understand over long time horizons. Coca-Cola, railroads, and insurance operations share a quality that early-stage technology companies do not: predictability measured in decades, not product cycles.

The evolution came in stages:

Documented 2024 commentary characterised Buffett’s evolved stance as viewing dominant tech franchises as “consumer businesses with technology under the hood” rather than speculative technology plays.

The TSMC episode deserves acknowledgement. Berkshire built and then reduced a position in Taiwan Semiconductor Manufacturing Company, an episode commentators cited as evidence of continued selectivity rather than a wholesale embrace of technology-sector exposure. Buffett’s pattern is not a pivot toward technology as a category. It is a selective expansion of what counts as understandable, anchored always to cash-flow durability.

Large Berkshire investment moves carry documented weight as institutional quality signals. The Apple stake generated commentary across 2023 and 2024 framing Buffett’s involvement as validation of a company’s economic moat, influencing sentiment among long-only managers and retail investors alike.

The reported Alphabet placement, if confirmed, would carry a similar signalling function. A $10 billion commitment from the world’s most scrutinised value investor would almost certainly prompt reassessment among portfolio managers already evaluating Alphabet’s AI positioning.

That signal has limits. It is a quality endorsement, not a price target.

Google Cloud Platform (GCP) is the third-ranked cloud provider behind Amazon Web Services (AWS) and Microsoft Azure by revenue, a verified market structure that has held across several recent reporting periods. GCP has been growing faster than AWS in percentage terms, making market share gains plausible even from a trailing position. BigQuery and Vertex AI have been identified by analysts and outlets including the Financial Times as Google Cloud’s documented competitive strengths in data analytics and AI tooling.

Investors evaluating Alphabet independently of the Berkshire signal should consider several questions the reported deal terms do not answer:

These are questions the institutional endorsement does not resolve. The Berkshire signal speaks to quality; the investment decision still requires independent assessment of valuation, execution, and competitive dynamics.

If confirmed, the reported transaction represents a coherent extension of Buffett’s documented evolution as a technology investor: a dominant franchise, strong cash generation, a durable competitive moat, and AI as the growth catalyst rather than the speculative premise. The Google Cloud metrics attributed to the original reporting, particularly the order backlog and developer engagement figures, describe a business with the operational characteristics Berkshire has historically favoured.

The sourcing context remains material. All transaction details derive from reporting attributed to Alphabet Inc. and Investing.com. Independent regulatory confirmation had not been identified at time of publication. Readers monitoring this story should watch for:

If independently confirmed, a $10 billion Berkshire placement into Alphabet would generate regulatory filings, analyst reassessments, and sustained institutional attention that would further validate or complicate the investment thesis.

The reported scale and structure are compelling regardless of one’s view on AI-era equities. Independent verification remains the threshold for treating this as a settled investment fact. Until that threshold is crossed, the story is best understood as a high-profile signal worth monitoring closely, with specific filings to watch for.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements regarding potential market impacts are speculative and subject to change based on market developments and company performance.

A private placement is a direct investment negotiated between a company and an investor, bypassing the public stock exchange. In this reported case, Berkshire Hathaway would have agreed terms directly with Alphabet rather than purchasing GOOGL or GOOG shares through a stock exchange.

Berkshire Hathaway has reportedly committed $10 billion to Alphabet, split evenly between $5 billion into Class A shares (GOOGL) at $351.81 per share and $5 billion into Class C shares (GOOG) at $348.20 per share, announced on 1 June 2026.

A cloud order backlog represents contracted but not-yet-recognised revenue from enterprise customers who have signed multi-year agreements. Google Cloud's reported backlog of more than $460 billion signals strong forward revenue visibility, as these commitments convert to recognised revenue over the life of each contract.

Buffett historically avoided technology stocks due to their unpredictability, but evolved his view by reframing dominant platforms like Apple as cash-flow businesses rather than technology speculations. The reported Alphabet investment appears to extend this same logic to a second dominant franchise with strong cash generation and AI as a growth catalyst.

Investors should monitor Alphabet's Form 8-K filings on SEC EDGAR, which would disclose a material private placement, and Berkshire Hathaway's next 13F filing, which would reveal the position if held at the reporting date. Coverage from major financial wires such as Reuters, Bloomberg, or the Financial Times would also typically confirm a transaction of this scale.