One company designs the chips. One fabricates them. One builds the only machine capable of printing next-generation circuits. One engineers the custom silicon running inside the world’s largest AI systems. Together, Nvidia, TSMC, ASML, and Broadcom form what may be the most consequential supply chain in technology today, and understanding how their roles interconnect is the starting point for evaluating any investment thesis tied to AI semiconductor stocks.

Investor and analyst interest in the sector has intensified sharply through 2025 and into 2026, driven by record hyperscaler capital expenditure and an AI infrastructure buildout that shows no sign of plateauing. The scale is difficult to overstate: Nvidia reported full-year FY2026 revenue of $215.9 billion, while TSMC has guided for above 30% full-year revenue growth in 2026. What follows is a clear explanation of what each of these four companies does, why each role is considered structurally irreplaceable, what the financial evidence says about their current trajectories, and what the honest risks are. No prior knowledge of chip manufacturing is required.

Why the chip supply chain is more complex than most investors realise

The intuitive assumption is straightforward: AI companies make AI chips. The reality is considerably more layered. The semiconductor supply chain separates into three distinct, non-interchangeable functions, and no single company performs all three:

- Design: Architecting the chip’s logic, circuitry, and instruction sets (what the chip does)

- Fabrication: Manufacturing the physical chip at nanometre-scale precision (how the chip is built)

- Equipment: Producing the lithography machines that print circuits onto silicon wafers (what makes fabrication possible)

A bottleneck at any layer propagates across the entire ecosystem. If fabrication capacity is constrained, even the most advanced chip design cannot reach production. If the equipment needed to print leading-edge circuits is unavailable, fabrication cannot advance to the next process node.

Each of the four companies occupies a different layer, which is why they are complementary rather than competitive.

| Company | Supply Chain Layer | Primary Role | Key Advantage |

|---|---|---|---|

| Nvidia | Design | GPU architecture for AI training and inference | Dominant market position in AI accelerators |

| TSMC | Fabrication | Contract manufacturing at leading-edge nodes | ~72% global foundry market share |

| ASML | Equipment | EUV lithography systems | Sole global supplier of EUV machines |

| Broadcom | Design (Custom) | Application-specific AI chips (ASICs) for hyperscalers | Deep partnerships with Google, Meta |

TSMC holds approximately 72% of global foundry market share as of May 2026, with advanced nodes (7nm and below) representing 74% of its wafer revenue in Q1 2026. ASML remains the sole global supplier of extreme ultraviolet (EUV) lithography machines, the equipment required to print circuits at those leading-edge node sizes. Understanding this structure is the foundation for contextualising the financial figures that follow.

When big ASX news breaks, our subscribers know first

Nvidia and TSMC: the engine and the factory behind AI’s computing power

The journey from a chip concept to a physical product requires two distinct capabilities: one company to design the architecture, and another to manufacture it at scale. Nvidia and TSMC are the two protagonists of that story, and neither can function at its current scale without the other.

Nvidia: designing the GPUs that train the world’s AI models

Nvidia operates as a fabless chip designer. It architects the graphics processing unit (GPU) designs that power AI training and inference workloads, where training refers to building AI models and inference refers to running them, but it does not own any manufacturing facilities. Every chip Nvidia designs is physically produced by a contract manufacturer.

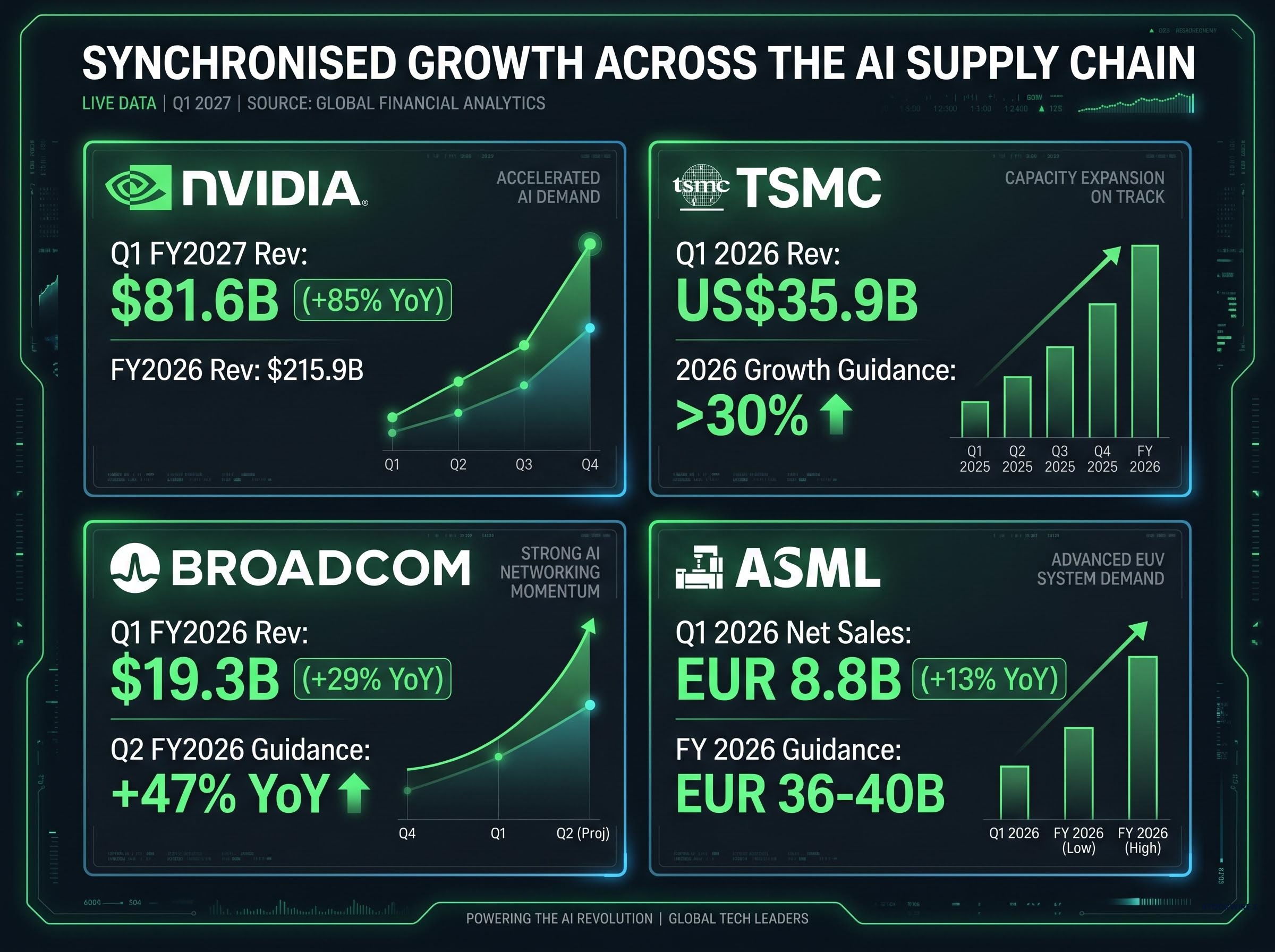

The financial trajectory reflects the intensity of AI-driven demand. Nvidia reported Q1 FY2027 revenue of $81.6 billion, up 85% year-over-year, with the Data Centre segment contributing $75.2 billion of that total. For the full fiscal year FY2026, revenue reached $215.9 billion, up 65% year-over-year, with gross margins of approximately 75%.

The current revenue cycle is driven by the ramp of the Blackwell GPU architecture, with Vera Rubin cited as the next generational step. Company executives have framed the long-term demand context in expansive terms.

Nvidia has framed its broader addressable market in terms of a $50-$80 trillion AI economic opportunity, with the Data Centre opportunity alone described as exceeding $500 billion.

TSMC: manufacturing the chips the AI era demands

TSMC (Taiwan Semiconductor Manufacturing Company) is the world’s dominant contract manufacturer, producing chips designed by Nvidia, Apple, AMD, and others at leading-edge process nodes. A process node refers to the size of the transistors etched onto a chip; smaller nodes allow more transistors per chip, which translates to greater computing power and energy efficiency.

TSMC reported Q1 2026 revenue of US$35.9 billion, with Q2 2026 guidance of US$39.0-$40.2 billion. Full-year 2026 growth guidance sits above 30%. The composition of that revenue is telling: High-Performance Computing (HPC) accounted for 61% of Q1 2026 revenue, directly linking AI infrastructure demand to foundry production volumes.

Advanced nodes (7nm and below) now represent 74% of wafer revenue, illustrating how dominant leading-edge production has become within TSMC’s business. The migration is not only AI-driven; it reflects a broader shift across the technology industry toward chips that require the most advanced fabrication capabilities available.

TSMC’s fabrication moat extends well beyond market share figures: at 3nm, TSMC is targeting approximately 180,000 wafers per month by end-2026, roughly eight times the estimated capacity at both Samsung and Intel, a gap that underpins the pricing power and customer lock-in visible in its revenue mix.

ASML and Broadcom: the invisible infrastructure of the AI chip ecosystem

Nvidia and TSMC command the most public attention, but two other companies occupy structural positions that are, in their own ways, equally difficult to replicate or replace. ASML and Broadcom operate in the less visible layers of the semiconductor ecosystem, yet both generate significant and growing AI-linked revenue.

ASML: the indispensable technology behind advanced chip manufacturing

ASML holds a position unlike any other in the semiconductor industry. It is the sole global supplier of EUV (extreme ultraviolet) lithography machines, the equipment required to print circuits at the most advanced node sizes. EUV lithography uses extremely short wavelengths of light to etch transistor patterns onto silicon wafers at a precision measured in nanometres.

This monopoly position was not acquired quickly. It represents decades of research and development and the construction of an industrial ecosystem involving hundreds of specialist suppliers. No competitor has replicated the capability.

The next step in that equipment roadmap is High NA EUV lithography, which raises the numerical aperture from 0.33 to 0.55 and enables single-exposure printing of features down to 8 nm, eliminating the multi-patterning steps that currently represent the largest cost and throughput constraint in advanced chip manufacturing.

ASML reported Q1 2026 net sales of EUR 8.8 billion, up 13% year-over-year. Full-year 2026 guidance sits at EUR 36-40 billion, with gross margin guidance of 51-53%. Demand has strengthened from non-China markets in particular, consistent with the company’s role as the sole supplier of equipment that every leading-edge fabrication facility requires.

Broadcom: the custom chip architect behind hyperscaler AI

Broadcom occupies a different design role from Nvidia. Rather than selling general-purpose GPUs, Broadcom engineers application-specific integrated circuits (ASICs) for hyperscalers including Google and Meta. ASICs are chips designed for a single, specific workload, allowing hyperscalers to build silicon tailored precisely to their AI training and inference requirements.

The distinction between the two models matters for understanding where AI compute demand flows:

- GPUs (Nvidia’s model) are versatile processors that can handle a broad range of AI workloads across many customers

- ASICs (Broadcom’s model) are purpose-built for a specific customer’s workload, offering potential efficiency advantages at the cost of flexibility

Broadcom reported Q1 FY2026 revenue of $19.3 billion, up 29% year-over-year, with Q2 FY2026 guidance of approximately $22.0 billion (up 47% year-over-year). AI semiconductor revenue reached $8.4 billion in Q1 FY2026, with the broader AI revenue trend described as approximately doubling in recent periods.

The structural demand forces that extend this story well beyond the current AI cycle

The financial results above are products of the current AI data centre buildout, but semiconductor demand does not depend on any single trend sustaining itself indefinitely. Multiple independent structural forces are converging simultaneously, which is what distinguishes this cycle from prior semiconductor booms where demand concentrated in one or two end markets.

Financial Times hyperscaler capital expenditure data published in April 2026 put the combined AI infrastructure spend of Amazon, Meta, Microsoft, and Alphabet at a projected $725 billion for 2026, a 77% increase over the $410 billion recorded in 2025, figures that contextualise why TSMC’s revenue guidance and Nvidia’s order book have remained robust despite broader macroeconomic uncertainty.

Six structural themes are driving chip demand across the industry:

- Artificial intelligence and data centres: The primary growth driver, with hyperscaler capital expenditure funding record chip orders

- Cloud computing: Ongoing migration of enterprise computing to cloud infrastructure, requiring sustained server and networking chip procurement

- Electric and autonomous vehicles: Modern EVs contain significantly more semiconductor content per vehicle than traditional cars, with autonomous driving adding further compute requirements

- Robotics and automation: Industrial and consumer robotics platforms require specialised processors for real-time decision-making

- Defence technology: Military modernisation programmes are increasingly dependent on advanced semiconductor capabilities

- Consumer electronics: Smartphones, wearables, and personal computing continue to demand smaller, more powerful chips at each product generation

Each of the four companies benefits from this broader set of drivers, not only AI. TSMC’s advanced node concentration (74% of wafer revenue from 7nm and below) reflects the reality that even non-AI demand is migrating toward leading-edge fabrication. Nvidia has framed its addressable market beyond the GPU business alone.

Nvidia executives have described the Data Centre opportunity as exceeding $500 billion, positioning current revenue as an early-stage capture of a much larger long-term market.

This multi-theme demand structure is the argument for why the semiconductor sector is considered a long-term thematic investment rather than a cyclical trade.

The next major ASX story will hit our subscribers first

Honest risks: what could challenge the AI semiconductor thesis

The structural case for these four companies is well supported by current financial evidence, but no sector investment thesis is complete without understanding its failure modes. Each company carries specific risks that are worth monitoring.

TSMC’s approximately 72% global foundry market share means its geopolitical concentration is a systemic risk for the entire semiconductor ecosystem, not merely a company-specific one. The vast majority of the world’s most advanced fabrication capacity sits in Taiwan, and any disruption to that capacity would propagate across every company that depends on leading-edge chip manufacturing.

The RAND Corporation analysis of Taiwan semiconductor concentration examined how the island’s dominance in high-end fabrication creates systemic vulnerabilities for the United States and its allies, framing the so-called silicon shield as both a deterrent and a single point of failure for the global technology supply chain.

Nvidia faces competitive risk from the very customers fuelling its growth. Hyperscalers including Google and Amazon are developing custom silicon as a potential alternative to purchasing GPUs at scale. This does not eliminate GPU demand, but it introduces a second channel that could redistribute market share over time.

The strategic paradox behind hyperscaler custom silicon is that the same capital expenditure wave funding Nvidia’s record order book is simultaneously bankrolling the Alphabet, Amazon, and Microsoft chip programmes designed to reduce their dependence on GPUs, particularly as inference, projected to represent approximately 80% of the AI accelerator market by 2030, becomes the dominant workload.

ASML carries exposure to export control regulations, particularly restrictions on EUV shipments to China, which affect near-term order visibility as flagged in Q1-Q2 2026 earnings commentary. Broadcom’s AI semiconductor revenue ($8.4 billion in Q1 FY2026) represented less than half of its total $19.3 billion quarterly revenue, meaning non-AI segments, which carry greater cyclicality risk, remain material to its overall financial profile.

| Company | Risk Category | Risk Description |

|---|---|---|

| Nvidia | Competition | Hyperscaler-developed custom silicon could reduce GPU procurement over time |

| TSMC | Geopolitical concentration | Advanced fabrication capacity concentrated in Taiwan; export control pressures |

| ASML | Export controls | Restrictions on EUV shipments to China affect order visibility |

| Broadcom | Cyclicality | Non-AI segments remain a material portion of revenue and carry greater cyclical risk |

These risks do not invalidate the structural case, but they define the variables an informed investor needs to watch.

The capex-to-revenue lag running through this cycle is a structural consideration that sits alongside the demand themes: hyperscalers have committed a combined approximately $725 billion in 2026 capital expenditure, but Morningstar analysts have identified an 18-24 month gap between that spending and the revenue it generates for end customers, a lag that has historically been the mechanism through which semiconductor cycles turn.

Four companies, one ecosystem: why the semiconductor supply chain is built to last

The four companies examined here do not merely participate in the same sector. They form an interdependent system. GPU design (Nvidia) requires advanced fabrication (TSMC), which requires leading-edge lithography equipment (ASML). Custom silicon design (Broadcom) adds a second channel through which hyperscalers access AI compute capability, running through the same fabrication and equipment layers.

The growth signals across these layers are synchronised. Nvidia reported revenue up 85% year-over-year in Q1 FY2027. TSMC is guiding above 30% full-year growth in 2026. Broadcom is guiding 47% year-over-year growth in Q2 FY2026. ASML has set full-year 2026 guidance at EUR 36-40 billion. TSMC’s HPC revenue share of 61% confirms that the fabrication layer is being pulled forward by the same demand forces driving chip design.

The structural demand themes identified earlier, AI, electric vehicles, robotics, defence, cloud computing, and consumer electronics, create demand across multiple layers simultaneously, not only at the GPU level. The system holds together because each layer needs the others.

- Nvidia designs the AI accelerators but depends on TSMC to manufacture them

- TSMC fabricates the world’s most advanced chips but depends on ASML for the lithography equipment to do so

- ASML supplies the machines that make leading-edge fabrication possible, with demand driven by the chips Nvidia and others design

- Broadcom provides an alternative path to AI compute through custom silicon, deepening the ecosystem’s reach into hyperscaler budgets

Understanding these individual roles and their interdependencies is the foundation for evaluating any investment vehicle that provides exposure to this sector, whether through direct equity positions, exchange-traded funds, or other instruments.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.