Hormuz Shipping Collapses 52% as US-Iran Clash Sends Oil Surging

5 hrs ago

Nufarm shares surged 13.6% on 28 May 2026, the company’s strongest single-session gain in at least a year, effectively erasing the damage from a 30% collapse that had rattled the stock roughly twelve months earlier. The catalyst was a first-half FY26 earnings release that landed at the top of management’s own guidance range, with underlying EBITDA up 18%, net profit after tax up 35%, and net debt down $135 million. Two of three major brokers covering the stock upgraded their ratings the same day, with all three now carrying price targets between $3.50 and $3.60. What follows unpacks what the numbers actually show, why the broker community responded so decisively, and what investors should watch as Nufarm presses toward its leverage target for the close of FY26.

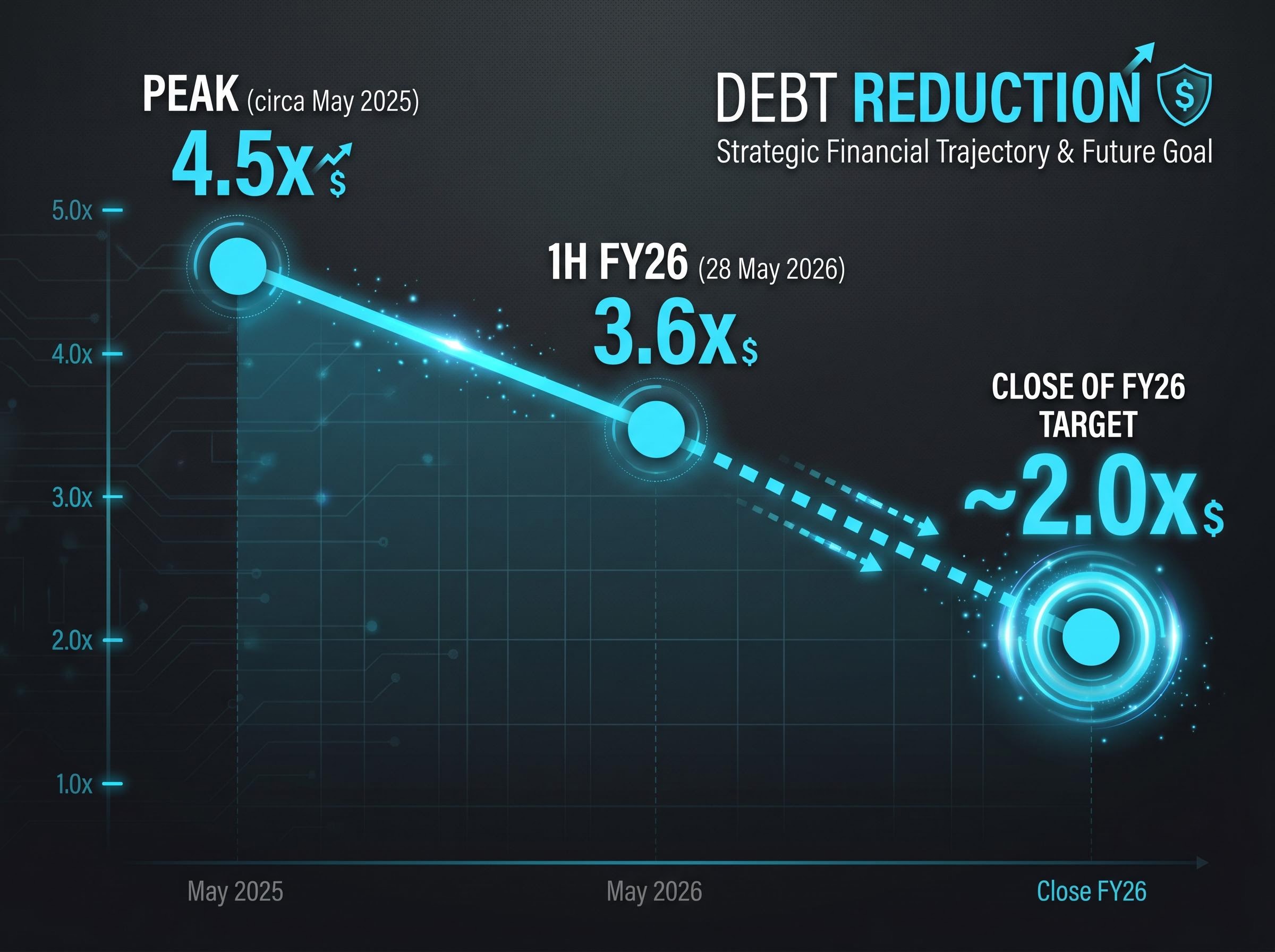

Roughly twelve months ago, Nufarm shareholders watched roughly 30% of the stock’s value disappear in a single session following a prior interim result. Leverage spiked to 4.5x, and the market punished the balance sheet risk with a valuation that lingered near multi-year lows for the better part of a year.

Today’s 13.6% rally is the market’s verdict on a very different set of numbers. The stock returned to its highest level since 21 May 2025, which means shareholders who held through the entire drawdown are now back near breakeven.

The same session that delivered Nufarm’s 13.6% gain also saw Select Harvests surged 14% on the back of a 33% jump in underlying profit, a reinstated dividend, and a board-endorsed buyback, reinforcing that the market was rewarding quality earnings delivery across the agricultural sector on 28 May 2026.

The key data points that frame the recovery:

A move of this magnitude only makes sense against the severity of what preceded it. Whether it marks a genuine re-rating or a technical bounce depends on the financial detail underneath.

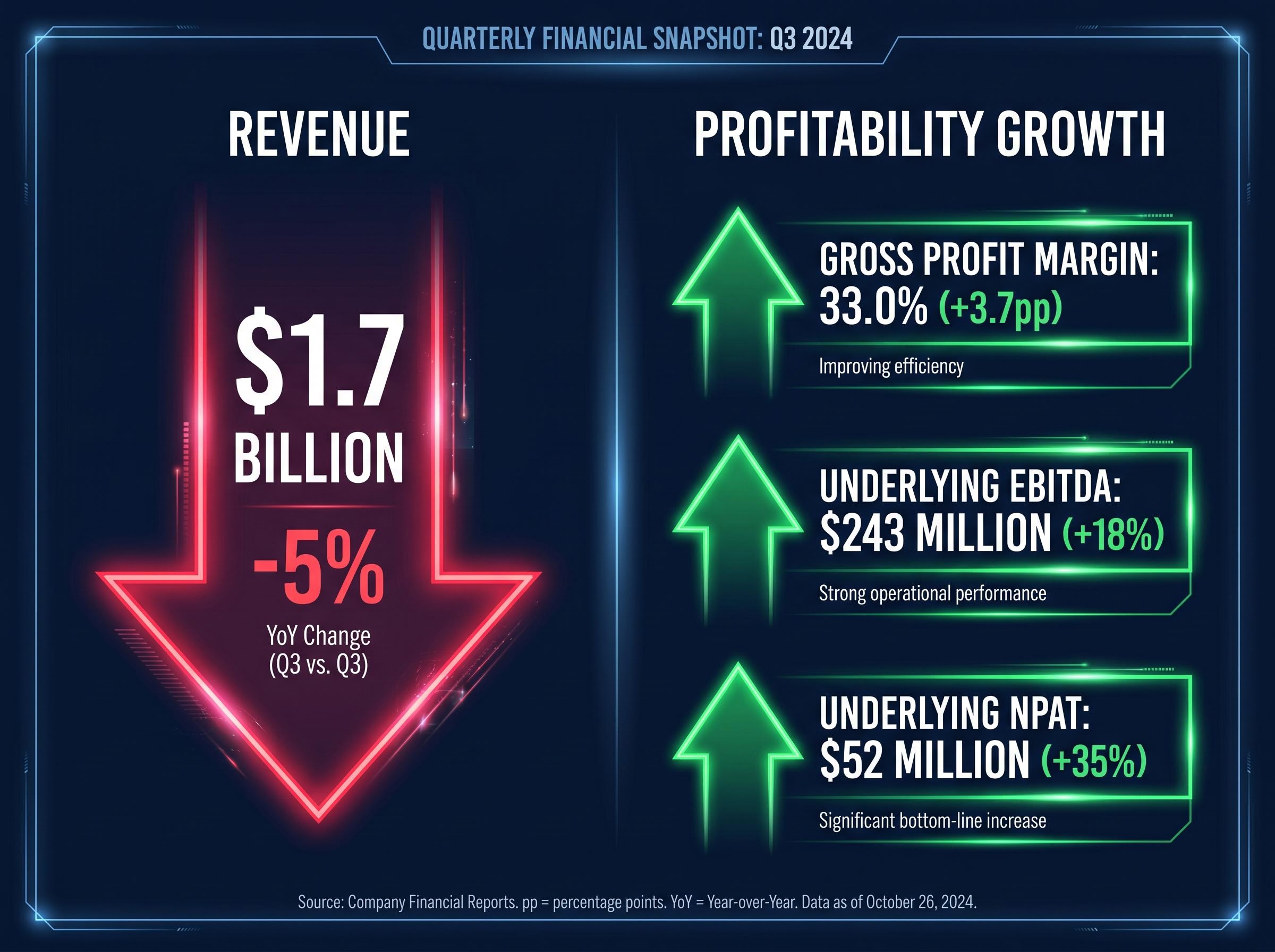

The counterintuitive story at the centre of this result is profitability improving while revenue shrank. Revenue fell 5% year-on-year to $1.7 billion, yet underlying gross profit margin expanded 3.7 percentage points to 33.0%. That margin expansion flowed directly through to earnings.

Standout metric: Gross profit margin expanded 3.7 percentage points to 33.0%, the clearest signal that profitability gains were driven by mix and cost discipline rather than volume.

Underlying EBITDA rose 18% to $243 million, finishing at the top of the guidance range of $239-$244 million. Underlying net profit after tax climbed 35% to $52 million.

The balance sheet moved faster than many had expected. Net debt fell $135 million to $1.23 billion, pulling leverage down from 4.5x at its peak to 3.6x, a reduction of approximately 20%.

| Metric | 1H FY25 (implied) | 1H FY26 | Change |

|---|---|---|---|

| Revenue | ~$1.79B | $1.7B | -5% |

| Gross profit margin | ~29.3% | 33.0% | +3.7pp |

| Underlying EBITDA | ~$206M | $243M | +18% |

| Underlying NPAT | ~$39M | $52M | +35% |

| Net debt | ~$1.37B | $1.23B | -$135M |

A company growing profit while shrinking revenue is executing a deliberate margin and efficiency strategy, not riding a revenue tailwind. That distinction matters for how durable the improvement is likely to be.

Nufarm is primarily a manufacturer and distributor of crop protection products, including herbicides, fungicides, and insecticides, as well as seeds. The company competes on formulation expertise and distribution reach rather than purely on volume.

Revenue can decline when commodity input pricing shifts or when the product mix changes. Margins can still improve if higher-value products take a larger share of the mix, or if input costs fall faster than selling prices adjust downward. That is what the 3.7 percentage point gross margin expansion reflects: the composition of what Nufarm sold improved even as the total amount sold declined.

The backdrop for Nufarm’s margin recovery sits within a broader agricultural sector dealing with global grain oversupply and compressed export margins, conditions that have weighed on commodity-exposed agri businesses throughout FY26 and made volume-driven revenue growth difficult across the supply chain.

The company operates across two broad revenue streams:

Both UBS and Bell Potter flagged the emerging platforms as performing ahead of expectations in this half, though specific revenue figures for those platforms were not disclosed in the available materials. The leverage reduction target of approximately 2.0x by the end of FY26 further indicates that cash generation is improving alongside margins, a signal that the improvement may be structural rather than cyclical.

Two of three major brokers upgraded Nufarm on the same day, and the third maintained its existing Buy rating at the same price target. The coordination is unusual. The reasoning behind each action is more revealing than the ratings themselves, because each analyst identified a different facet of the result as the decisive factor.

The ASX continuous disclosure obligations require listed companies to immediately notify the market of any information that a reasonable person would expect to have a material effect on share price, which is the framework under which Nufarm’s 1H FY26 earnings release and any associated broker-sensitive guidance updates are made available to all investors simultaneously.

| Broker | Previous rating | New rating | Previous target | New target |

|---|---|---|---|---|

| UBS | Neutral | Buy | $2.80 | $3.50 |

| RBC Capital Markets | Sector Perform | Outperform | $3.40 | $3.60 |

| Bell Potter | Buy | Buy (maintained) | $3.60 | $3.60 |

UBS centred its upgrade on sustainable crop protection margins, better-than-expected Omega-3 and hybrid seed platform performance, and an expectation that cost programmes will exceed inflation to support FY27-28 earnings growth. RBC Capital Markets took a different angle, emphasising the strategic shift toward capital efficiency over volume growth, credible progress on dual cost programmes, leverage trending toward approximately 2.0x, and improving return on invested capital.

Bell Potter characterised a “persistent valuation gap” relative to Nufarm’s strategic progress, suggesting that even the broker that did not upgrade sees further upside ahead.

When two brokers upgrade on the same day and a third maintains a Buy at the same target, the combined signal is unusually coherent. The multi-layered reasoning, spanning margins, cost discipline, capital efficiency, and platform growth, suggests the reassessment goes deeper than a single earnings beat.

The single most tangible forward commitment from management is the FY26 year-end leverage target of approximately 2.0x. The trajectory so far:

Both UBS and RBC cited the cost reduction programmes as central to their confidence in the FY27-28 earnings trajectory. UBS specifically noted that cost programmes are expected to exceed inflation, providing a structural tailwind to earnings growth beyond the current half. RBC emphasised improving return on invested capital as cost efficiency compounds through subsequent reporting periods.

Elders is running a parallel balance sheet repair programme in the same reporting season, targeting leverage toward a sub-2.0x target via the Killara feedlot divestment, with its own half-year result showing cash conversion surging to 176.6% and operating cash flow more than doubling, providing a live ASX agribusiness case study in how debt reduction and earnings growth can compound simultaneously.

It is worth noting that specific dollar targets and timelines for the cost programmes have not been publicly quantified in available materials. Platform-level revenue figures for Omega-3 and hybrid seeds from the 1H FY26 result were also not disclosed. These gaps mean the market is, to some degree, pricing in management execution on faith supported by directional broker commentary rather than granular disclosure.

Investors wanting to stress-test the risks that remain even after meaningful leverage reduction should consult our full explainer on Synlait Milk’s debt restructure, which examines how a company that halved its bank debt through a major asset sale still faced critical refinancing risk from facilities maturing within weeks of each other, a scenario that illustrates why reaching a leverage target is only one step in a full balance sheet recovery.

The leverage target is the clearest line management has drawn. Whether Nufarm reaches 2.0x by year-end will be the most closely watched metric in the second half of FY26.

The investment thesis around Nufarm has changed in a single session, not because of one day’s price action, but because the underlying financial evidence shifted. What was a highly leveraged, margin-pressured crop chemicals business twelve months ago is now demonstrating cost discipline, margin recovery, and a credible balance sheet repair trajectory.

The three-broker consensus (two upgrades, one maintained Buy, all at $3.50-$3.60 targets) establishes a near-term valuation anchor. The FY26 second-half result and leverage achievement will be the next major test.

Investors should watch three things from here:

For investors who sold or avoided the stock through the prior twelve months, this result resets the risk-reward calculation. For those already holding, it provides evidence that the worst may be behind the company. The road to 2.0x leverage and sustained platform growth is still being built, and the second half will determine whether today’s re-rating holds.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

Nufarm shares surged 13.6% after the company reported first-half FY26 results at the top of its own guidance range, with underlying EBITDA up 18% and net profit after tax up 35%, prompting two major broker upgrades on the same day.

Nufarm is targeting leverage of approximately 2.0x by the end of FY26, down from a peak of 4.5x following the prior interim result and 3.6x as of the 1H FY26 result reported on 28 May 2026.

Nufarm's gross profit margin expanded 3.7 percentage points to 33.0% even as revenue declined 5% to $1.7 billion, reflecting a shift toward higher-value product mix and cost discipline rather than volume-driven growth.

Following the 1H FY26 result, UBS set a target of $3.50 (upgraded to Buy), RBC Capital Markets set a target of $3.60 (upgraded to Outperform), and Bell Potter maintained its Buy rating with a $3.60 target.

Investors should monitor whether Nufarm achieves its approximately 2.0x leverage target by year-end, any further disclosure on Omega-3 and hybrid seed platform revenues, and whether cost programme savings continue to outpace inflation as UBS expects.