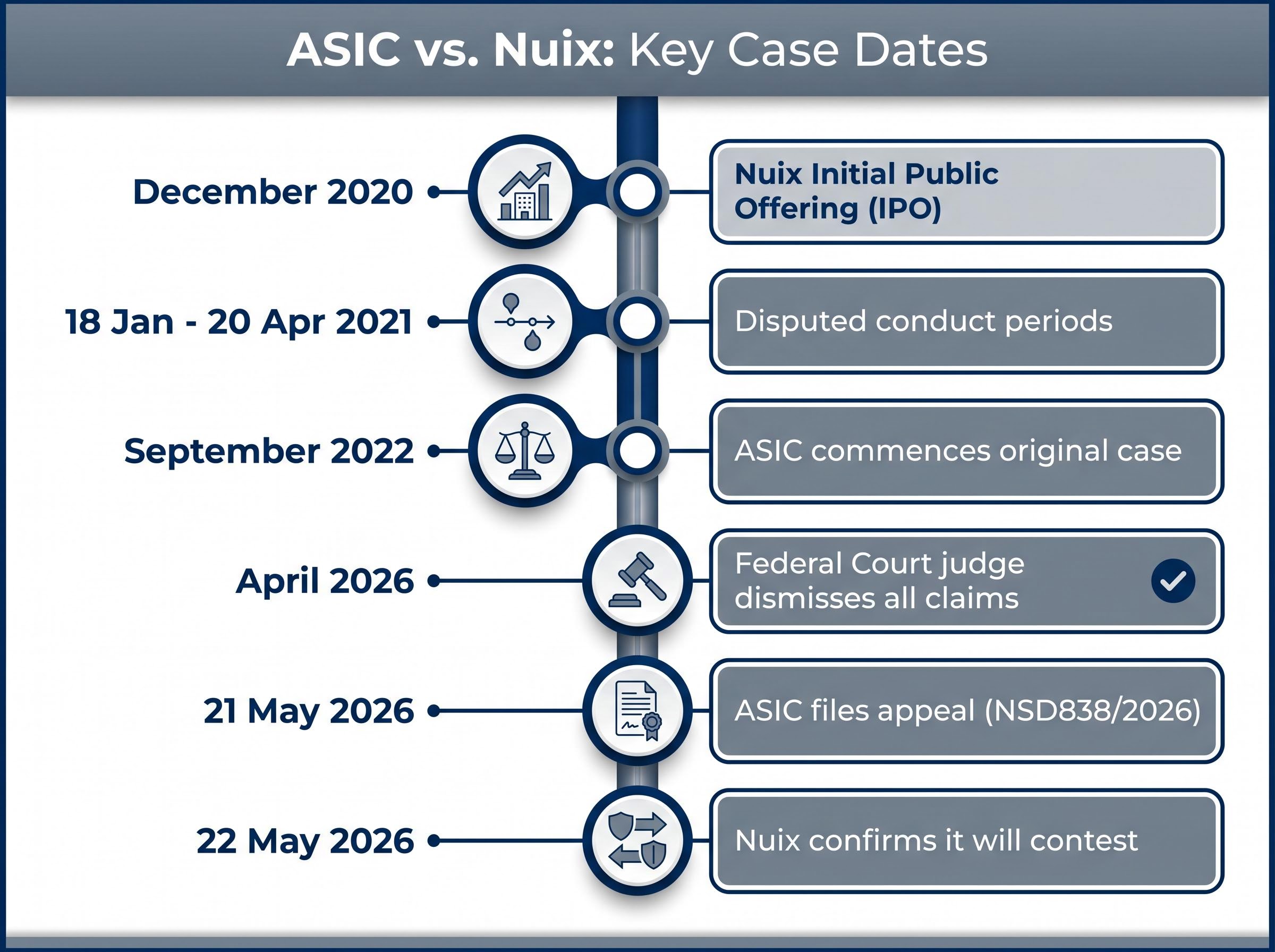

Australia’s corporate regulator is refusing to let a Federal Court loss stand. The Australian Securities and Investments Commission (ASIC) filed an appeal on 21 May 2026 challenging the judgment that cleared Nuix Limited (ASX: NXL) of misleading investors about its revenue performance after a high-profile December 2020 initial public offering. The original case, which commenced in September 2022, centred on whether Nuix properly disclosed a shortfall against the revenue forecast in its prospectus. A Federal Court judge dismissed all of ASIC’s claims in April 2026, describing part of the regulator’s case as “contrary to commercial reality.” ASIC responded in less than a month by lodging proceedings in the Full Federal Court, targeting what it calls specific errors in the primary judge’s findings. What follows covers the precise grounds of the appeal, why the original judgment went against ASIC, and what the Full Federal Court outcome could mean for every ASX-listed company navigating continuous disclosure obligations.

ASIC files appeal, targeting two specific legs of the original case

ASIC’s decision to appeal came with a pointed signal. Media release 26-103MR, published on 21 May 2026, confirmed the filing in proceedings NSD838/2026 and stated the regulator is concerned “there were errors in the primary judge’s findings.”

ASIC filed the appeal because it is concerned “there were errors in the primary judge’s findings.”

The appeal is not a broad rehearing. It targets two specific legal grounds across two defined conduct periods:

- Misleading or deceptive conduct under the Corporations Act and the ASIC Act, relating to the period from 18 January to 25 February 2021 and from 26 February to 20 April 2021, including the 8 March 2021 ASX announcement

- Continuous disclosure breaches under ASX Listing Rule 3.1 and s 674 of the Corporations Act, covering the same two periods

ASIC explicitly chose not to appeal the dismissal of claims against the five individual director defendants. The challenge is directed entirely at Nuix as the corporate entity. A Full Federal Court hearing date is yet to be determined.

When big ASX news breaks, our subscribers know first

What the Federal Court actually decided in April 2026

The April 2026 judgment gave Nuix a comprehensive win, and the reasoning explains why ASIC found the outcome unacceptable.

At its core, the court found that Nuix’s realised revenue falling approximately 9.6% below its prospectus forecast did not constitute misleading conduct or trigger continuous disclosure obligations. After accounting for headwinds the company had already disclosed to the market, the shortfall narrowed to approximately 4.7%.

The judge went further than a numerical finding. ASIC’s misleading conduct case was characterised as “contrary to commercial reality,” a phrase that signalled the court viewed the regulator’s position as disconnected from how listed companies actually manage and communicate forecast variances.

Three categories of claim were dismissed in full:

- Misleading or deceptive conduct

- Continuous disclosure breach

- Directors’ duty breaches (against all five individual defendants)

The directors’ exoneration is now settled. ASIC is not contesting it. The judgment’s treatment of the revenue variance, however, set a commercially pragmatic benchmark that ASIC is now asking a higher court to revisit.

ACV and the metrics at the heart of the disclosure dispute

The case did not hinge on statutory revenue figures alone. A non-statutory metric, Annualised Contract Value (ACV), became the focal point of the regulatory dispute, and it remains central to the appeal.

Annualised Contract Value (ACV) represents the total contracted revenue on an annualised basis, captured at a point in time. Nuix featured ACV prominently in its prospectus as a growth indicator, though it is not required under statutory reporting standards.

ASIC’s contention is that for companies like Nuix, where statutory revenue recognition may lag underlying performance, ACV functions as a meaningful signal of growth trajectory for investors. How the primary judge treated ACV disclosures and prospectus representations in assessing materiality is now directly in play in the appeal.

Legal commentary published after the judgment flagged three implications for listed companies:

- Companies using non-statutory metrics in prospectuses face heightened scrutiny on whether those metrics carry ongoing disclosure obligations

- The distinction between internal management information and market-sensitive disclosable information requires clearer documentation

- Forecasting processes need to be robust enough to withstand regulatory challenge, particularly where non-statutory metrics underpin investor expectations

Both Clayton Utz (11 May 2026) and Ashurst (29 April 2026) identified the treatment of ACV as particularly significant for ASX-listed technology companies that routinely use operational metrics beyond statutory accounts in their investor communications.

What continuous disclosure law says and why this case tests it

Continuous disclosure is the obligation that underpins informed trading on the ASX. ASX Listing Rule 3.1 and s 674 of the Corporations Act require listed companies to immediately disclose information that a reasonable person would expect to have a material effect on the price or value of their securities.

Continuous disclosure obligations attach at the point a company becomes aware of material information, not at the point of board sign-off or formal announcement preparation, a distinction the Electro Optic Systems penalty confirmed with a $4 million finding against a company that waited 14 weeks to disclose a $48 million revenue shortfall.

The test a company must apply involves two steps:

ASX Guidance Note 8 sets out the materiality framework that listed companies must apply when assessing whether information requires immediate disclosure under Listing Rule 3.1, including the 5% threshold that featured directly in the primary judge’s reasoning on the Nuix revenue variance.

- Identify the information: Determine whether the company is aware of information that has not been disclosed to the market

- Assess materiality: Determine whether a reasonable person would expect that information to have a material effect on the price or value of the company’s securities, guided by ASX Guidance Note 8

The Nuix judgment engaged directly with the question of where the materiality line falls for revenue forecast variances. The primary judge addressed the 5% materiality threshold discussed in ASX Guidance Note 8 and distinguished the case from the precedent set in Southernwood v Brambles.

Clayton Utz noted on 11 May 2026 that the judgment provides helpful clarification on continuous disclosure obligations. The distinction the court drew between internal management information and market-sensitive disclosable information sits at the centre of ASIC’s appeal grounds.

| Internal management information (not disclosable) | Market-sensitive information (disclosable) |

|---|---|

| Preliminary internal revenue tracking against forecast | Confirmed revenue shortfall material enough to affect share price |

| Management discussions about adjusting operational targets | Board decision to revise a publicly stated forecast |

| Internal ACV reports used for operational planning | ACV performance data that contradicts prospectus representations to the market |

The Full Federal Court will now determine whether the primary judge drew this line in the right place.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Nuix’s market position and the commercial stakes of the appeal outcome

Nuix responded to the appeal filing with a brief ASX announcement on 22 May 2026, confirming it had received notice.

Nuix stated it will contest the appeal.

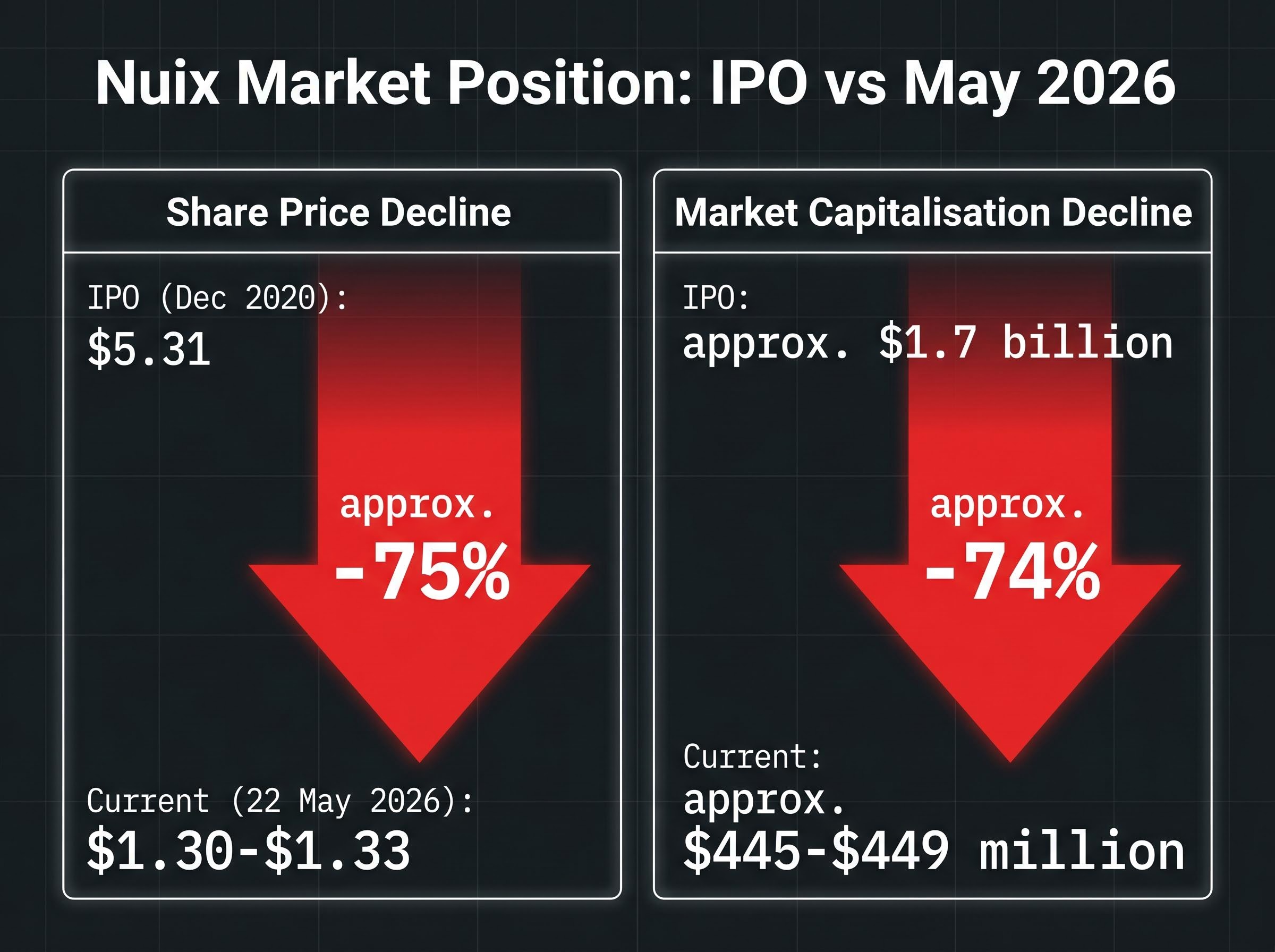

The company’s share price trajectory since its IPO frames what is at stake for investors who bought in at listing and those watching the stock today.

IPO structural risks are particularly acute for retail investors who buy at or after listing, when the first-day premium is already baked in and insiders who entered at much lower prices are positioned to exit, a dynamic that contextualises why the gap between Nuix’s $5.31 IPO price and its current trading range carries different significance for different investor cohorts.

| Metric | IPO (December 2020)* | Current (22 May 2026) | Change |

|---|---|---|---|

| Share price | $5.31 | $1.30-$1.33 | approximately -75% |

| Market capitalisation | approximately $1.7 billion | approximately $445-$449 million | approximately -74% |

IPO price and market capitalisation figures are sourced from secondary reporting and have not been independently verified.

With no Full Federal Court hearing date yet scheduled, regulatory uncertainty will remain attached to the stock for an extended period. For the broader market, the outcome will set a precedent on what regulators can demand from companies that issue revenue forecasts at the IPO stage.

What the Full Federal Court will now decide, and why it matters beyond Nuix

The Full Federal Court will assess whether the primary judge correctly interpreted the continuous disclosure obligations and misleading conduct provisions of the Corporations Act. Legal commentators from both Ashurst (29 April 2026) and Clayton Utz (11 May 2026) expect the materiality assessment for revenue forecast variances, specifically the approximately 9.6% shortfall figure, to be the central contested question.

The outcome carries implications well beyond Nuix:

- Materiality standards: A Full Federal Court ruling will establish whether a shortfall of this magnitude triggers continuous disclosure, creating a reference point for every ASX-listed company that issues prospectus forecasts

- Class action proceedings: Related class action cases are likely to be influenced by the appeal’s determination on materiality and misleading conduct

- Non-statutory metric disclosure: The treatment of ACV will guide how listed companies, particularly in the technology sector, use operational metrics in prospectuses and ongoing investor communications

Both Ashurst and Clayton Utz described the primary judgment as commercially pragmatic and likely to be influential. ASIC’s appeal ensures that characterisation will now be tested at a higher level. Until the Full Federal Court delivers its ruling, the legal standards for continuous disclosure of forecast variances remain in a state of regulatory contest.

Past performance does not guarantee future results. Forward-looking statements regarding the appeal’s outcome and its implications are speculative and subject to change based on legal proceedings and regulatory developments.

The appeal keeps ASIC’s enforcement signal alive for listed companies

ASIC’s decision to appeal, rather than accept the Federal Court outcome, signals that the regulator views the primary judgment’s commercial pragmatism as a benchmark worth challenging. The contest over where the materiality line falls for revenue forecast variances is now a live question before the Full Federal Court rather than a settled one.

ASIC enforcement posture in 2026 extends well beyond the Nuix proceedings, with the $35 million Macquarie Securities penalty for short sale misreporting and the $4 million EOS ruling together signalling that the regulator is prepared to pursue systemic failures and disclosure lapses across different corners of the market in the same enforcement cycle.

Two practical takeaways apply for ASX-listed companies in the interim. First, maintain documented forecasting processes capable of withstanding regulatory scrutiny. Second, treat non-statutory metrics used in prospectuses as carrying ongoing disclosure obligations until the courts determine otherwise.

Investors and market participants should monitor proceedings NSD838/2026 for a hearing date. The Full Federal Court’s ruling, whenever it arrives, will settle one of the more consequential questions in Australian continuous disclosure law.