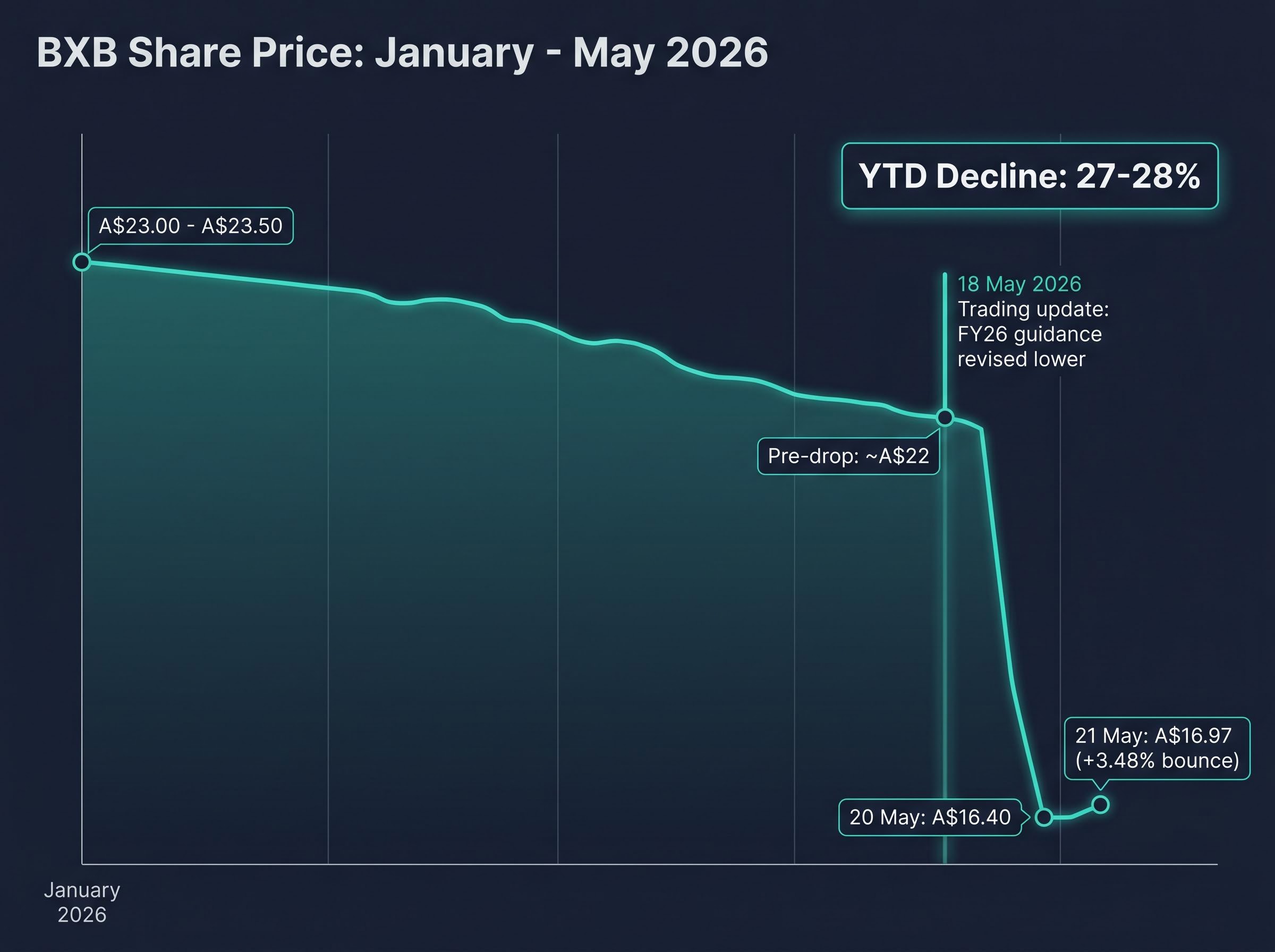

Brambles has shed roughly 27% of its share price value since January 2026. The stock opened the year near A$23.00-A$23.50, drifted lower through the first quarter, then collapsed from approximately A$22 to A$16.40 in a single session on 20 May after a formal guidance downgrade caught the market offside. By 21 May, a partial recovery had lifted the BXB share price to A$16.97, but the damage to sentiment was already locked in.

The selloff has repositioned Brambles from a premium-priced compounder to a stock trading closer to the broader industrials average. For Australian investors, the question is whether that reset reflects a genuine deterioration in the underlying business or simply a multiple compression on slower, but still solid, growth. What follows is a structured walkthrough of the catalyst, the business model, the financial metrics, the balance sheet, the peer comparison, and the valuation framing that investors need to form their own view.

What triggered the 27% slide in BXB shares in 2026

The 18 May 2026 trading update was the formal trigger: Brambles revised FY26 revenue and profit growth ranges downward, and the market responded by sending the stock from roughly A$22 to A$16.40 in a single move. By 21 May, a 3.48% bounce had brought the price back to A$16.97, but the YTD decline of approximately 27-28% was already the steepest drawdown in Brambles’ recent history.

The severity of the reaction, however, only makes sense in the context of what had been building underneath for months. Three distinct pressure layers converged to make the market acutely sensitive to any negative signal from management:

The operational mechanism behind the downgrade is more specific than the headline figures suggest: a US repair network bottleneck in the subcontracted service centre network has been estimated to cost Brambles approximately US$60 million in earnings, a detail that matters for assessing whether the guidance cut represents a one-off operational disruption or a symptom of deeper structural pressure.

- Guidance downgrade: The 18 May trading update formally revised FY26 revenue and profit growth expectations lower, shifting the narrative from “slower growth” to “growth ceiling confirmed.”

- Broker EPS downgrades: Several brokers had already trimmed FY25-26 earnings per share forecasts through early 2026, citing softer volume commentary and normalising pallet pricing. At least one major broker cut its rating from Buy to Hold.

- Macro rotation: Rising bond yields in Q1 2026 triggered a broader rotation out of defensive industrials and into cyclicals and resources, removing a pillar of support from Brambles’ valuation multiple.

“Limited upside to our target price after guidance reset and sector multiple compression.” , one major broker’s rationale for cutting Brambles from Buy to Hold

Each of these forces would have weighed on the stock individually. Together, they primed the market for a sharp re-rating the moment management confirmed what many had already suspected: that the double-digit earnings growth rates of 2022-2024 were not coming back.

When big ASX news breaks, our subscribers know first

How Brambles actually makes its money (and why the model is structurally resilient)

Brambles, through its CHEP brand, operates a pallet pooling business. Rather than selling pallets outright or carrying freight, the company owns a vast pool of standardised pallets that circulate continuously between manufacturers and retailers. At each transfer point, Brambles collects a daily hire fee. The revenue model is closer to a subscription or annuity than a traditional logistics operation.

The pallet pooling market structure differs fundamentally from conventional logistics in that revenue is generated through asset circulation and hire fees rather than freight movement, which is why pooling operators like CHEP sustain higher margins and more predictable cash flows than traditional transport businesses.

The business operates across three regions: Asia-Pacific, Americas, and EMEA. Demand is structurally embedded in the fast-moving consumer goods (FMCG) and retail supply chains that keep supermarket shelves stocked, which means volumes are tied to non-discretionary consumption rather than cyclical freight demand.

What makes pallet pooling different from standard logistics

The distinction matters for investors because it explains why the margins and returns on equity look the way they do. Three sources of competitive advantage keep large customers locked in:

- Network scale: CHEP’s pool of pallets and the infrastructure to manage their circulation across multiple continents is not easily replicated. New entrants face enormous upfront capital requirements.

- Contracted relationships: Management commentary highlights renewed and extended contracts with major FMCG and retail customers, with high retention rates and multi-year agreement structures.

- Digital integration: Ongoing investment in digital pallet tracking and network optimisation gives customers supply chain visibility that raises switching costs and reinforces the economic case for pooling over single-use pallet alternatives.

Brambles’ circular economy and sustainability positioning adds a further layer of differentiation, particularly as large retailers increasingly favour reusable supply chain solutions over disposable ones.

What the financials actually say about BXB’s performance

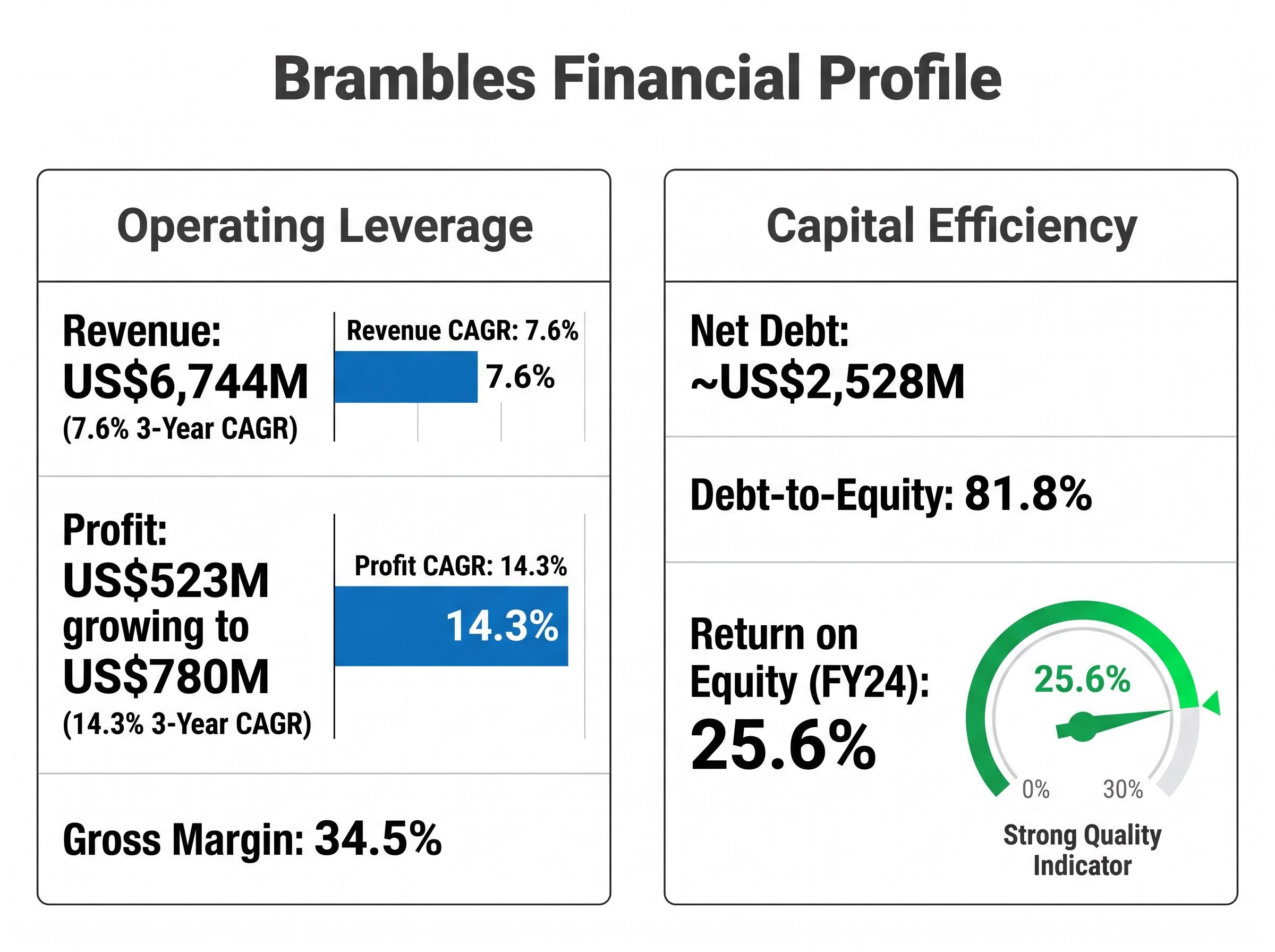

The headline revenue figure, US$6,744 million in the most recent annual result, tells only part of the story. Revenue has grown at a three-year compound annual growth rate (CAGR) of 7.6% per annum. That is respectable but not exceptional. The analytically interesting signal sits below the top line.

Profit has grown from US$523 million to US$780 million over the same period, a three-year CAGR of 14.3%. A gross margin of 34.5% supports the case that Brambles retains meaningful pricing power at the service level.

| Metric | Most Recent | Three Years Prior | Three-Year CAGR |

|---|---|---|---|

| Revenue | US$6,744M | — | 7.6% |

| Profit | US$780M | US$523M | 14.3% |

| Gross Margin | 34.5% | — | — |

Profit growing at 14.3% per annum while revenue grew at 7.6% signals operating leverage at work: Brambles has been compounding earnings through efficiency rather than volume.

That contrast is the core quality argument. Network efficiency, asset productivity initiatives, and residual pricing power from the inflation era have converted modest top-line growth into strong profit momentum.

The FY26 guidance revision complicates the picture. Revenue growth is now guided at the lower end of mid-single digits, with margin expansion characterised as “modest.” The market had been pricing in continuation of double-digit earnings growth. What it received was confirmation that mid-single digit growth is the operating reality, not a temporary soft patch. Whether the efficiency engine continues to outrun the top line at current run rates is the open question.

Balance sheet and capital efficiency: reading the debt and ROE picture

Brambles carries net debt of approximately US$2,528 million. For a business that owns and manages a global pool of physical assets, that figure needs to be read in context rather than in isolation.

| Capital Metric | Figure | Interpretive Note |

|---|---|---|

| Net Debt | ~US$2,528M | Supported by strong, predictable operating cash flows from annuity-style revenue |

| Debt-to-Equity Ratio | 81.8% | Equity exceeds total debt; moderate rather than aggressive for an asset-heavy industrial |

| Return on Equity | 25.6% (FY24) | Mid-20s ROE cited as a quality indicator by Livewire and broker commentary |

The 81.8% debt-to-equity ratio places Brambles in moderate territory. Equity still exceeds total debt obligations, and the predictability of CHEP’s cash flows, tied to non-discretionary FMCG consumption, distinguishes this balance sheet from a leveraged cyclical business where debt amplifies downside risk.

Why ROE matters more than debt in isolation for a pooling business

A pooling model is inherently asset-intensive. Pallets must be purchased, maintained, tracked, and replaced. The relevant question is not whether the business carries debt, but whether the capital deployed earns a return that justifies the leverage.

At 25.6%, Brambles’ return on equity indicates that borrowed capital is being deployed productively rather than simply sustaining the balance sheet. Livewire commentary and several broker notes cite the mid-20s ROE as one of the strongest quality indicators in the Brambles investment case. Investors who dismiss BXB on the basis of net debt alone risk misreading a business where leverage is a deliberate structural feature of the pooling model, not a vulnerability.

Reading debt and ROE together, rather than treating each in isolation, is the analytical discipline that separates a surface-level concern about Brambles’ US$2,528 million net debt position from a reasoned conclusion about whether the leverage is productive or dangerous for long-term holders.

How Brambles stacks up against ASX peers in 2026

The 27-28% YTD decline becomes more revealing when measured against the broader logistics and industrial cohort on the ASX.

| Company | 2026 YTD Return | Commentary |

|---|---|---|

| Brambles (BXB) | ~-27% to -28% | Guidance downgrade layered on top of macro headwinds |

| Goodman Group (GMG) | Low-to-mid single digit positive | Benefited from continued industrial property demand (AFR, April 2026) |

| Qube Holdings (QUB) | Flat to slightly positive | Logistics and ports exposure held steady |

| Lindsay Australia (LAU) | Modestly negative, single digits | Transport softness but no comparable guidance shock |

The divergence is stark. Goodman Group, Qube Holdings, and Lindsay Australia have all held up materially better in 2026. Brambles’ underperformance is not a sector-wide repricing; it is partially self-inflicted.

The 18 May guidance downgrade is a company-specific event. The same macro headwinds (rising bond yields, defensive industrial rotation) affected all four names, yet only BXB suffered a double-digit drawdown. That specificity cuts both ways for investors.

Bull case arguments:

- Structural economics of pallet pooling justify a premium to traditional industrials; BXB is now trading closer to the industrials average than the premium it commanded in 2022-2023.

- One broker maintains a Buy rating with a target of approximately A$16, arguing the quality of the business model has not changed.

Bear case arguments:

- A de-rated multiple may be “fair rather than cheap” given the mid-single digit growth profile, according to broker commentary.

- One major broker cut to Hold with a target of A$14-A$15, and Motley Fool Australia described Brambles as “good quality but not screamingly cheap.”

The implication: any positive catalyst from here is BXB-specific and not dependent on a broader sector recovery. That is both the opportunity and the risk.

Quality compounder or value trap? The case for and against BXB at current prices

The tension in the Brambles investment case is now sharply defined. On one side: a 25.6% ROE, a 14.3% profit CAGR, annuity-like revenue from non-discretionary supply chains, and a share price that has de-rated from a high-teens to low-20s forward PE at the start of 2026 to something closer to the broader industrials average. On the other: a mid-single digit revenue growth ceiling, a formal guidance downgrade as recently as 18 May 2026, and a broker consensus tilting toward Hold.

At approximately A$16.97 as of 21 May 2026, the stock sits between a A$14-A$15 target from the broker that cut to Hold and a A$16 target from the broker maintaining Buy. That range is tight, and it suggests the market has not yet decided whether the guidance reset is a floor or a waypoint to further downgrades.

Two steps separate a watchlist entry from a conviction position:

- Peer valuation comparison: Benchmark Brambles’ current PE and EV/EBITDA against logistics and industrials comparables at post-selloff prices. The pre-May premium has compressed, but “cheaper than before” is not the same as “cheap.”

- Guidance risk assessment: Determine whether the FY26 revision represents management resetting expectations conservatively (a floor) or the first acknowledgement of structural deceleration (further downside).

For BXB at current prices:

- Profit compounding through efficiency has been durable across multiple years.

- The pooling model generates cash flows that support both the debt load and continued investment.

Against BXB at current prices:

A shareholder class action adds a further layer of unquantified risk to the BXB investment case: the April 2026 Federal Court ruling marked the first successful class action trial on both liability and loss in Australian corporate history, and the financial exposure has not been incorporated into any of the broker price targets cited in current coverage.

- Mid-single digit revenue growth may not justify a re-rating back toward prior multiples.

- Broker consensus leans Hold, and the most recent formal disclosure is a downgrade, not a beat.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The selloff tells you a lot, but it does not tell you the whole story

The 27% YTD decline reflects both a legitimate reset in growth expectations and a sentiment overshoot that has brought Brambles to a more historically normal valuation starting point. The financial metrics reviewed here (profit CAGR, ROE, debt-to-equity, gross margin) are a starting point for evaluation, not a conclusion.

Any post-May broker note revisions will carry updated EPS and target price estimates calibrated to the guidance revision. Those numbers matter. The 18 May 2026 trading update is the most recent formal disclosure, and anything published before that date is working from outdated assumptions.

Brambles remains a quality business at a reset price. Whether “reset” equals “attractive” depends on the investor’s conviction about whether the guidance floor has been set or whether further revisions lie ahead. Investors should review the most recent ASX-lodged materials from Brambles and post-May 2026 analyst updates before drawing conclusions, then benchmark the current PE against logistics and industrials peers for a final valuation check.

For investors wanting a broader technical read on how the BXB selloff sits within the wider ASX selling environment, our full explainer on ASX confirmed downtrends covers the systematic scan methodology, the 33 names identified as of 20 May 2026, and the five macro forces driving simultaneous weakness across multiple sectors, providing the sector-wide context for the supply pressure visible in BXB’s May chart.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.