How the US Government Became Intel’s Investor and Deal Broker

54 mins ago

On 12 May 2026, the Australian Government announced it would scrap the 50% capital gains tax discount from 1 July 2027, replacing it with cost-base indexation and a 30% minimum tax on net capital gains. The reform addresses a concession that the Grattan Institute, ACOSS, the Tax Institute, and independent economists have spent years calling too blunt, too generous, and poorly targeted. On the direction of travel, there is broad consensus. On the design, there is a question worth pressing: the problem with Australia’s CGT discount may not be its size but its shape. A flat concession that treats a 13-month speculative flip identically to a 30-year business builder is structurally odd regardless of the percentage involved. What follows is an examination of that structural flaw, detailed modelling of a tapered alternative, and a comparison against the government’s chosen reform path, with a focus on what the design choice means for long-term productive investment.

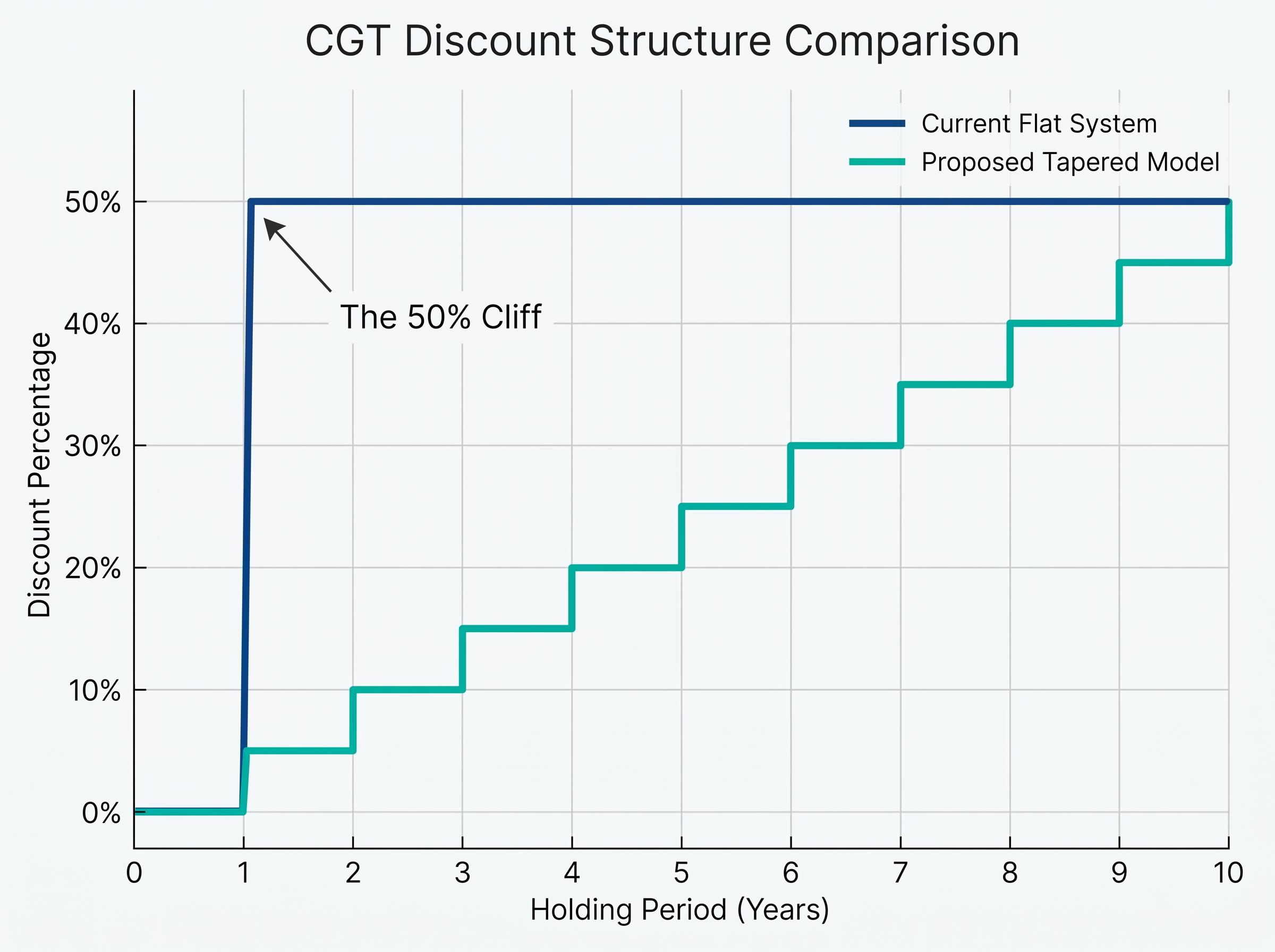

The 50% CGT discount applies identically from the first day after 12 months of ownership. An investor who sells a property at 13 months receives the same concession as one who held a business for three decades. There is no second threshold, no graduation, no additional reward for patience. The system is binary: hold for less than a year, pay full tax; hold for one day longer, and half the gain disappears from the tax base permanently.

A 13-month holder and a 13-year holder face identical tax treatment under the current system. The discount rewards crossing a single threshold, not building long-term value.

The behavioural consequences follow logically. As the Australian Financial Review noted in August 2024, the flat discount creates a cliff that encourages investors to time disposals just past the 12-month mark, secure the concession, then recycle capital into the next position. The Grattan Institute has linked this dynamic to speculative property investment rather than productive long-term capital formation. Three distortions stand out:

The flaw is structural, not arithmetical. Even a 25% flat discount would share the same cliff problem.

The alternative is straightforward in concept: replace the binary cliff with a gradient. Under the tapered model examined here, an investor receives a 5% discount on the capital gain for each full year of ownership, reaching the existing 50% cap at year 10 and remaining there indefinitely. The incentive shifts from crossing a single threshold to accumulating duration.

The modelling uses inputs from Stockspot founder Chris Brycki: a $100,000 starting portfolio, 10% annual nominal return, 2.5% annual inflation, and a 47% marginal tax rate. These assumptions reflect a productive growth asset consistent with long-run Australian equities returns of approximately 6-7% real, rather than a speculative short-term trade.

| Holding Period (Years) | Taper Discount | Portfolio Value | Tax (Tapered Model) | Tax (Flat 50% Discount) |

|---|---|---|---|---|

| 1 | 5% | $110,000 | $4,465 | $2,350 |

| 2 | 10% | $121,000 | $8,883 | $4,935 |

| 3 | 15% | $133,100 | $13,218 | $7,779 |

| 4 | 20% | $146,410 | $17,438 | $10,905 |

| 5 | 25% | $161,051 | $21,508 | $14,347 |

| 6 | 30% | $177,156 | $25,392 | $18,131 |

| 7 | 35% | $194,872 | $29,049 | $22,291 |

| 8 | 40% | $214,359 | $32,236 | $26,862 |

| 9 | 45% | $235,795 | $35,113 | $31,884 |

| 10 | 50% | $259,374 | $37,453 | $37,453 |

| 15 | 50% | $417,725 | $74,663 | $74,663 |

| 20 | 50% | $672,750 | $134,596 | $134,596 |

The crossover point arrives at year 10, where both models converge. For every disposal before that point, the tapered model collects more tax than the flat system, penalising short-duration holders while progressively rewarding patience.

The 50% CGT discount was introduced on 21 September 1999, replacing the Keating-era system under which investors could index their cost base to inflation before calculating a taxable gain. The replacement was blunt by design. Rather than requiring taxpayers to track inflation-adjusted cost bases annually, the discount offered a single, administratively simple concession.

The original reform rested on three objectives:

As the Tax Institute noted in August 2024, the discount was “theoretically a rough proxy for inflation compensation.” For a time, that proxy held. In the 1990s, average annual labour productivity growth ran at approximately 1.8%, and the economic environment that produced the 1999 design looked materially different from today’s. The Productivity Commission’s 2024 Bulletin reported that average annual labour productivity growth over the past decade had fallen to approximately 0.9%. The economy the discount was designed for has changed. The discount has not.

Per-asset-class indexation outcomes diverge significantly depending on when an asset was acquired and how rapidly it appreciated: property held through the high-inflation period of 2022-2024 receives proportionally more indexation relief than shares purchased in a low-inflation environment and held for a decade, meaning the effective tax difference between the old discount and the new regime is not uniform across investor portfolios.

The budget announcement replaces the flat discount with cost-base indexation (restoring the pre-1999 mechanism) plus a 30% minimum tax on net capital gains for assets held more than 12 months. Transitional rules, confirmed by Baker McKenzie and the ATO, preserve the 50% discount for gains accrued before 1 July 2027.

The CGT reform does not operate in isolation: the broader budget tax package includes a ring-fencing of negative gearing on established properties purchased after 12 May 2026 and a 30% minimum tax on discretionary trust distributions from 1 July 2028, creating a combined policy environment that reshapes the after-tax calculus for investors across property, equities, and family trust structures simultaneously.

The ATO’s 2026 CGT reform legislation detail confirms that the 50% discount will be replaced by cost-base indexation and a 30% minimum tax on net capital gains from 1 July 2027, with transitional rules preserving the existing discount for gains accrued on assets held before that date.

Both the government’s approach and the tapered model reduce the concession for short-term holders. Where they diverge is in the treatment of long-duration, above-inflation returns, precisely the category of investment Australia’s productivity performance most needs to encourage.

| Holding Period (Years) | Tax (Tapered Model) | Tax (Indexation + 30% Floor) | Difference |

|---|---|---|---|

| 1 | $4,465 | $3,525 | +$940 |

| 2 | $8,883 | $8,309 | +$574 |

| 3 | $13,218 | $13,341 | -$123 |

| 4 | $17,438 | $18,478 | -$1,040 |

| 5 | $21,508 | $22,505 | -$997 |

| 6 | $25,392 | $27,298 | -$1,906 |

| 7 | $29,049 | $33,016 | -$3,967 |

| 8 | $32,236 | $39,547 | -$7,311 |

| 9 | $35,113 | $46,982 | -$11,869 |

| 10 | $37,453 | $61,742 | -$24,289 |

| 15 | $74,663 | $131,014 | -$56,351 |

| 20 | $134,596 | $239,177 | -$104,581 |

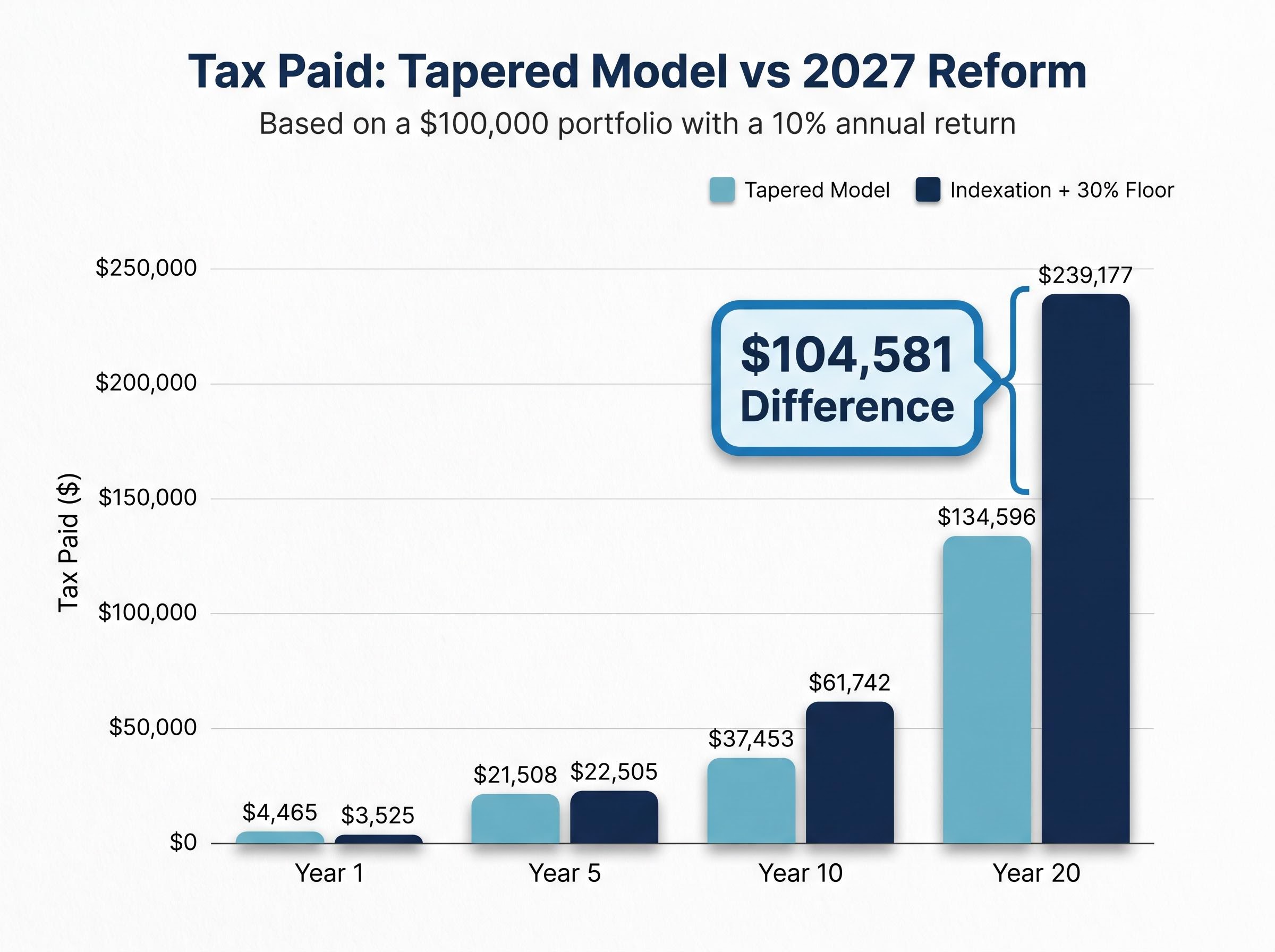

At year 1, inflation indexation is $940 cheaper for the investor. By year 5, the tapered model is $997 cheaper. By year 20, the gap reaches $104,581 on a $100,000 starting portfolio.

On a $100,000 portfolio earning 10% annually, the difference between the tapered model and the government’s indexation-plus-floor approach reaches $104,581 over 20 years. The design choice is not abstract.

The nominal return threshold at which the tapered model outperforms indexation sits at approximately 4.5% per year (assuming 2.5% inflation), a level historically exceeded by productive growth assets including Australian equities.

The transitional rules announced alongside the reform preserve the 50% discount for gains accrued before 1 July 2027. In practice, this means established portfolios, disproportionately held by older, higher-wealth Australians, are largely insulated from the change.

ABS Household Income and Wealth data from 2021-22 confirms that investment property and shares are key drivers of net wealth for higher-income, older households. ACOSS has linked the current CGT discount to “excessive investor demand” that drives housing unaffordability disproportionately affecting younger Australians.

The grandfathering arrangement creates two distinct regimes:

As Chris Brycki of Stockspot has argued, the grandfathering structure creates winners and losers based on when an individual began investing rather than on investment behaviour. A tapered model would have been generationally neutral: the same rules applied to all future investments, with the reward structure tied to holding duration rather than birth year.

For investors who have relied on timing asset disposals in low-income years, including the year of retirement, to reduce their effective CGT rate below 30%, our full explainer on income-timing strategies under the new CGT floor details precisely which disposal structures are eliminated by the minimum tax, the income brackets most materially affected, and the planning alternatives that remain available before 1 July 2027.

Both the current flat discount and the government’s indexation-plus-floor approach share a common gap: neither creates a graduated reward for patient, productive capital commitment. The flat system offers full reward at 12 months and nothing more after. The indexation model compensates for inflation but imposes a 30% floor that grows heavier in absolute terms as real returns compound, meaning the tax burden on genuinely productive long-term holdings increases faster than the concession offsets it.

The tapered model addresses the structural critique raised by the Grattan Institute and ACOSS. For any disposal before year 10, it collects more tax than the current flat system, satisfying both the revenue and equity objectives of reform. For disposals after year 10, it collects less than the government’s 2027 approach, protecting the long-duration investors whose capital formation underpins productivity growth.

The tapered model collects more tax from short-term speculation than the current system while collecting less than the government’s 2027 approach from long-term productive investment. It addresses the direction of reform without penalising the behaviour Australia most needs to encourage.

Australia’s market sector labour productivity growth has averaged approximately 0.9% per year over the past decade, according to the Productivity Commission’s 2024 Bulletin, down from 1.8% in the 1990s. At June 2024, ABS data recorded 2,783,744 actively trading businesses, with an entry rate of 14.7% and an exit rate of 12.6%. Tax settings that channel capital toward long-term productive deployment, rather than optimising short-term revenue collection, are one lever available to policymakers seeking to reverse that productivity trajectory.

Replacing a flat discount with indexation-plus-floor addresses the size of the CGT concession but not the shape. The shape is what creates the behavioural distortions: the cliff at 12 months, the identical treatment of speculation and patience, the absence of any graduated incentive to hold productive assets through a full business cycle and beyond.

The 2027 reform will generate additional revenue and will reduce the most generous short-term speculation benefits. These are legitimate objectives, and the direction of travel has broad support across the policy spectrum. The question is whether the same objectives could be achieved with less collateral damage to long-term investment incentives, and the modelling suggests they can.

Over 20 years, on a $100,000 portfolio at 10% annual return, the tapered model produces a tax bill more than $100,000 lower than the indexation-plus-floor approach. The difference is not marginal. It is the difference between a system that rewards productive patience and one that taxes it.

Investors with long-duration holdings should model the impact of the transitional rules on their specific portfolios before 1 July 2027. The three-year lead time before the new regime takes effect remains an opportunity, for both policymakers and market participants, to consider whether a tapered structure could achieve the same revenue and equity outcomes with a design that actually rewards the behaviour Australia needs most.

Investors holding assets across the 1 July 2027 transition date face a practical compliance challenge that the policy design creates but does not resolve: dual-calculation record-keeping will require documented original cost bases, inflation-indexed adjusted bases, and a methodology for splitting accrued gains at the commencement date, a set of requirements that the old 50% discount system made entirely unnecessary.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections referenced in this article are based on specific modelling assumptions and are subject to market conditions and various risk factors. Past performance does not guarantee future results.

—

On 12 May 2026, the Australian Government announced it would scrap the 50% capital gains tax discount from 1 July 2027, replacing it with cost-base indexation and a 30% minimum tax on net capital gains for assets held more than 12 months.

Long-term investors face a heavier tax burden under the indexation-plus-30%-floor approach than they would under the current flat discount; modelling shows the difference reaches over $104,000 on a $100,000 portfolio earning 10% annually over 20 years.

A tapered CGT discount gradually increases the concession by 5% for each full year of ownership, reaching the 50% cap at year 10, instead of applying the full 50% discount from the moment an asset is held for just over 12 months.

Yes, transitional rules confirmed by Baker McKenzie and the ATO preserve the 50% discount for gains accrued on assets held before 1 July 2027, meaning existing portfolios are largely insulated from the change.

Investors should model the impact of the transitional rules on their specific portfolios before 1 July 2027, ensure they have documented original cost bases for all assets, and consider consulting a financial professional about disposal timing strategies that may be eliminated by the new 30% minimum tax.