On 17 May 2026, the 10-year Treasury yield climbed to 4.595% while WTI crude surged past $101 per barrel, producing the kind of simultaneous spike that historically accelerates a bond selloff. Alpine Macro is doing the opposite of panicking.

With U.S.-Iran negotiations at a knife-edge and the Strait of Hormuz partially constrained, markets are pricing in persistent energy inflation. Most bond investors are stepping back. Alpine Macro’s Dan Alamariu is stepping in, making a 3-6 month contrarian case for long-duration bonds based on an oil price thesis that markets have not yet fully discounted.

What follows unpacks Alpine Macro’s thesis in full: the geopolitical scenario underpinning it, the mechanical link between falling oil and bond yields, the equity positioning implications, and the specific risks that could invalidate the call. The bond market outlook hinges on a binary geopolitical event, and the framework below offers investors a structured lens to evaluate the opportunity for their own fixed-income and equity allocations.

The 50/50 bet at the heart of Alpine Macro’s trade

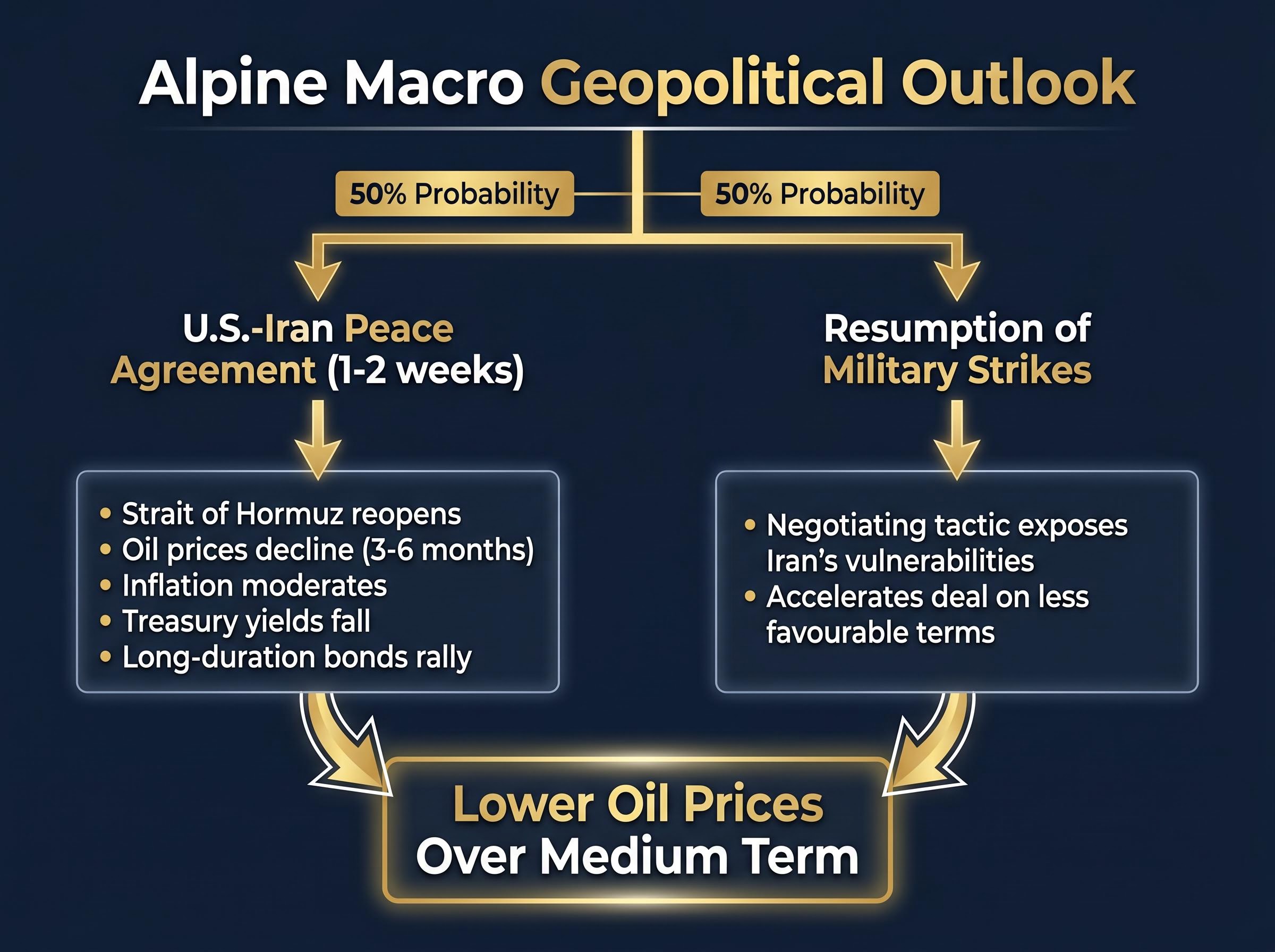

Alamariu assigns exactly 50% probability to a U.S.-Iran peace agreement within 1-2 weeks, and 50% to a resumption of military strikes. That sounds like a coin flip. In pricing terms, it is not.

The bond-positive scenario, a peace deal, is the one markets appear underweighted toward. Current yield levels and the oil spike reflect positioning for persistent conflict, not resolution. A coin-flip outcome where one side is mispriced creates an asymmetric entry point.

Alpine Macro’s two scenarios and their projected market implications break down as follows:

- Peace deal within 1-2 weeks: Strait of Hormuz reopens, oil prices decline over 3-6 months, inflation expectations moderate, Treasury yields fall, and long-duration bonds rally

- Resumed military strikes: Framed not as a bearish endpoint but as a negotiating tactic designed to expose Iran’s structural vulnerabilities and accelerate a deal on less favourable terms for Tehran

According to Alpine Macro’s Alamariu, as reported by Investing.com, the odds of a deal versus renewed strikes sit at roughly 50/50, but both scenarios ultimately converge toward lower oil prices over the medium term.

The second scenario is where the thesis gains its contrarian edge. Even under the hawkish outcome, Alpine Macro frames conflict escalation as a pressure mechanism that shortens the path to eventual resolution rather than extending it indefinitely.

When big ASX news breaks, our subscribers know first

How the Strait of Hormuz connects oil prices to your bond portfolio

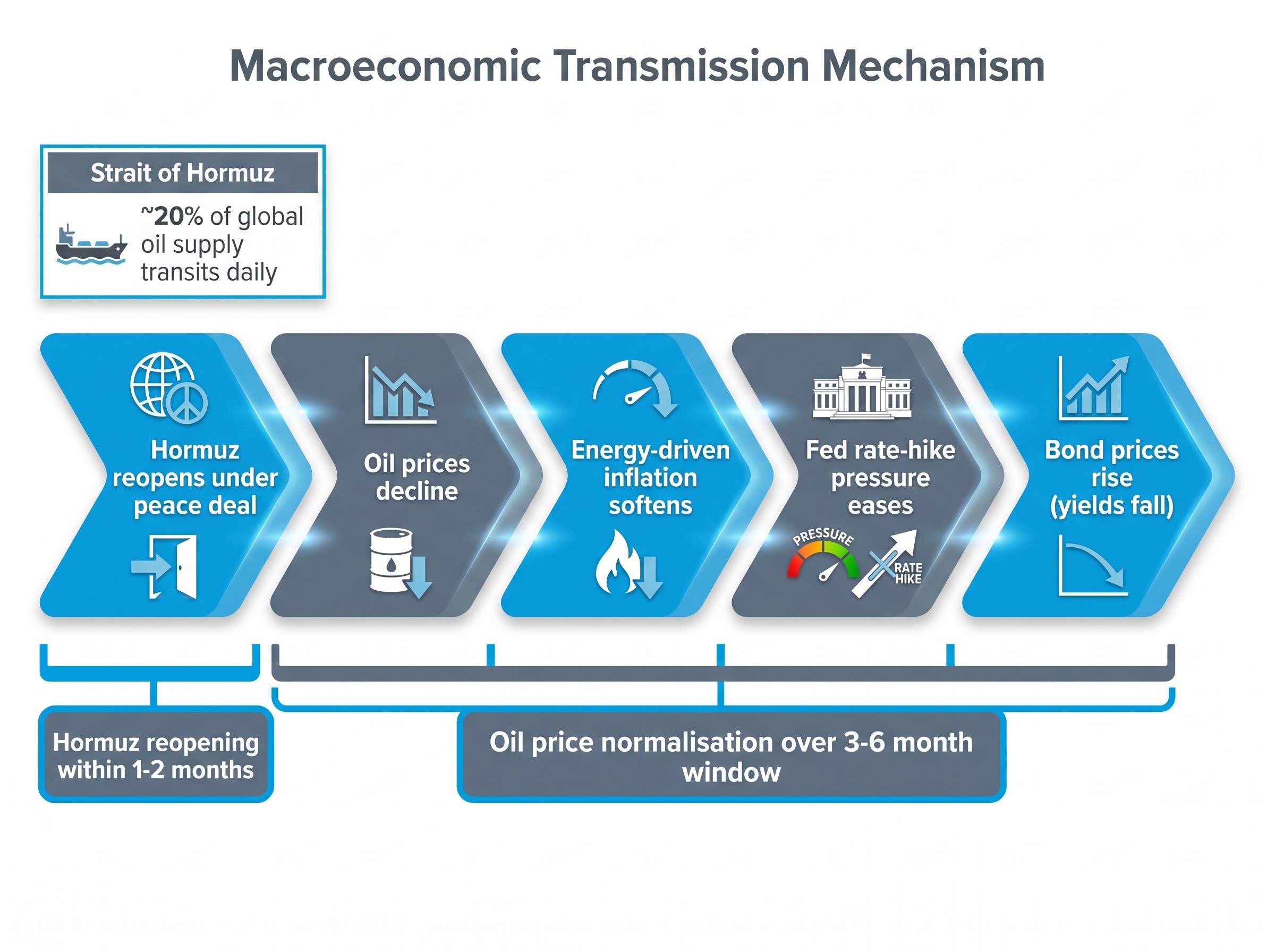

The Strait of Hormuz is the narrow waterway between Iran and the Arabian Peninsula through which roughly one-fifth of global oil supply transits daily. When that chokepoint is constrained, the supply disruption embeds a risk premium into energy prices, which flows directly into inflation expectations and, by extension, Treasury yields.

The transmission chain from Hormuz to bond prices follows a specific sequence:

- Hormuz reopens under a peace deal, removing the physical supply bottleneck

- Oil prices decline as the geopolitical risk premium unwinds and supply normalises

- Energy-driven inflation softens, pulling headline CPI readings lower

- Federal Reserve rate-hike pressure eases, as the inflation impulse fades from the data

- Bond prices rise (and yields fall) as markets reprice the forward rate path downward

Alpine Macro projects that a deal would include Hormuz reopening within 1-2 months, with oil price normalisation expected over a 3-6 month window.

Broad energy complex elevation reinforces how embedded the current premium is. Natural gas futures closed at $2.96, up 2.28% on 17 May 2026, while the 30-year Treasury yield reached 5.128%, up 0.115 percentage points (+2.29%) on the same date.

What the yield curve is signalling right now

The 10-2 year Treasury yield spread widened to 31.32 basis points on 17 May 2026, a single-day steepening of 4.15 basis points (+15.27%). That steepening reflects a market repricing growth expectations relative to inflation expectations: the long end is selling off faster than the short end, consistent with investors demanding more compensation for holding duration during an energy shock.

Thirty-year yields above 5.1% represent historically elevated entry points for long-duration positioning. If the geopolitical premium dissipates, these levels could mark a near-term ceiling rather than a new floor.

The 30-year yield threshold above 5% carries structural consequences beyond bond pricing alone: at that level, fixed mortgage rates push above 8%, corporate borrowing costs reset materially higher, and the federal government’s debt service burden compounds against a deficit already running near 7.2% of GDP, a feedback loop that makes the entry-point argument for long-duration bonds dependent on how quickly the geopolitical premium dissipates.

Why Alpine Macro says this bond selloff is almost over

The core of Alpine Macro’s fixed-income argument rests on a distinction between transitory and structural inflation drivers. Corporate pricing pressures from tariffs and energy costs, in the firm’s assessment, fall into the former category. The primary risks to bonds are policy-driven rather than rooted in macro fundamentals.

Current yield levels reflect a geopolitical premium that, under the peace-deal scenario, dissipates within weeks. That framing repositions today’s prices as a potential entry point for long-duration bonds rather than a warning to stay out.

The following table summarises Treasury yield levels and single-day moves across three maturities as of 17 May 2026:

| Maturity | Yield (%) | Change (pp) | Change (%) |

|---|---|---|---|

| 5-Year | 4.258 | +0.137 | +3.32 |

| 10-Year | 4.595 | +0.136 | +3.05 |

| 30-Year | 5.128 | +0.115 | +2.29 |

Single-day moves of this magnitude across the curve are uncommon outside of crisis repricing events. The uniform direction, every maturity selling off simultaneously, suggests a common driver rather than maturity-specific dynamics.

Alpine Macro advises investors to disregard near-term inflation noise, according to Investing.com reporting. The firm expects both bond and equity prices to be materially higher within 3-6 months.

When a credible macro research firm with a named geopolitical thesis identifies specific yield levels as a potential bottom, investors gain a defined analytical framework against which to test their own duration assumptions.

For investors who want to model the specific magnitude of the yield decline before sizing a long-duration position, our dedicated guide to the yield reversal ceiling applies Wolfe Research’s sign-restriction decomposition to the 40-basis-point Iran-linked surge, finding that only 10-15 basis points are attributable to the reversible geopolitical premium, with the remainder driven by growth repricing and structural factors that a peace deal will not unwind.

The equity side of the barbell: what falling oil means for stocks

The Alpine Macro thesis does not stop at bonds. The same oil price trajectory that supports fixed income creates distinct winners and losers in equities, and the firm’s recommended positioning reflects both sides of that trade.

Alpine Macro’s barbell equity strategy pairs two legs:

- AI and technology sector leaders: Lower energy costs reduce operating expenses for data centre-intensive businesses, supporting margin expansion in a sector already benefiting from secular demand growth

- Energy-intensive cyclicals: Manufacturers, transporters, and industrials with high fuel input costs see direct margin improvement as oil normalises, providing a catalyst that is currently underpriced

On 17 May 2026, the divergence was already visible. The S&P 500 fell 92.74 points (-1.24%) to 7,408.50, while the S&P 500 Energy sector index rose 2.32%. The NASDAQ Composite dropped 410.08 points (-1.54%) to 26,225.15. The VIX climbed to 18.43, up 1.17 points (+6.78%).

Three factors have insulated equities from the full force of the geopolitical shock so far: strong Q1 2026 earnings, no Fed rate hikes in a stable-growth environment, and market expectations for oil price mean reversion. That insulation has limits, but it explains why equities have not repriced as aggressively as bonds.

Oil shock equity performance across the 2008, 2011, and 2022 episodes produced S&P 500 returns well below the index’s long-run average over the following 12 months, yet Morgan Stanley and JPMorgan both recommend maintaining existing positions rather than reactive selling, citing historical S&P 500 gains averaging approximately 12% in the first year following major supply disruptions as the energy premium unwinds.

When energy producers stop outperforming energy consumers

The current outperformance of energy-producing equities, up 2.32% on a day when the broader market fell more than 1%, is consistent with an active supply disruption. Under the Alpine Macro thesis, that relative performance reverses as oil normalises.

The expected rotation from energy producers to energy consumers is projected to materialise between May 2026 and year-end. Investors positioned in the barbell framework would hold both legs through the transition, capturing the initial energy strength and the subsequent shift toward technology and industrial beneficiaries.

The two risks that could unwind the entire thesis

Alpine Macro identifies the primary threats to its thesis as policy decisions, not macroeconomic fundamentals. Two risk categories stand out:

- Federal Reserve missteps and fiscal stimulus: If energy prices remain elevated, the Trump administration may pursue fiscal stimulus ahead of the 3 November midterm elections, adding to deficit pressure and keeping yields elevated. A Fed forced into rate hikes by persistent energy-driven inflation would undercut the entire duration thesis.

- Diplomatic collapse and sustained conflict: If renewed military escalation extends beyond a negotiating tactic into sustained conflict, the oil and inflation premium persists. The 3-6 month normalisation window closes, and the geopolitical risk premium becomes a structural feature rather than a temporary distortion.

Fed rate hike probability has shifted from a tail risk to a near-majority market forecast, with Kalshi prediction markets placing the odds of a hike before July 2027 at 60%, driven by 76 consecutive days of effective Hormuz closure transmitting a supply-side shock into US energy, food, freight, and petrochemical prices that rate policy cannot directly resolve, and by Kevin Warsh’s confirmation as Fed chair under political conditions that draw explicit comparisons to the Burns-era accommodation of the 1973 oil shock.

Alpine Macro frames policy decisions, not macro fundamentals, as the primary risk to bonds, according to Investing.com reporting. The distinction matters: macro conditions are trending supportive, but political miscalculation could override them.

The U.S. Dollar Index at 99.21, up 0.480 points (+0.49%) on 17 May 2026, offers an additional signal. Dollar strength in this context reflects risk-off positioning, and a sustained move higher would suggest markets are pricing in prolonged uncertainty rather than near-term resolution.

Any contrarian trade requires clearly defined invalidation signals. Monitoring Fed commentary for hawkish shifts, tracking congressional fiscal proposals ahead of the midterms, and watching Iran negotiation headlines for signs of breakdown are the specific criteria that would signal the thesis is failing.

The next major ASX story will hit our subscribers first

What investors should be watching in the days ahead

The Alpine Macro thesis narrows the monitoring task to three leading indicators that will signal whether the trade is working:

- Iran negotiation headlines: Progress toward a deal within Alamariu’s 1-2 week window is the primary catalyst. A bullish-for-bonds signal is any formal framework agreement; a bearish signal is a declared breakdown or military escalation beyond tactical positioning.

- Hormuz shipping status: Reports of resumed tanker traffic through the strait or reduced insurance premiums on Hormuz-transiting vessels would confirm the physical supply bottleneck is easing. Continued diversions or elevated premiums indicate the disruption persists.

- Weekly WTI price direction: A sustained move below $95 would suggest the geopolitical premium is unwinding. Holding above $100 indicates the market still prices supply risk as unresolved.

Duration positioning in context

The entry-point logic for long-duration bonds at current levels splits into two timeframes. The opportunistic case assumes a peace deal materialises within weeks, driving a rapid yield decline from the 10-year at 4.595% and the 30-year above 5.1%. The patient case assumes normalisation unfolds over 3-6 months as oil prices gradually moderate.

Alpine Macro advises investors not to abandon the position if near-term inflation prints remain elevated. The thesis is predicated on forward oil dynamics rather than backward-looking CPI data. A hot inflation reading in June or July would not invalidate the trade if Hormuz shipping has resumed and oil is trending lower.

The 1-2 week geopolitical resolution window makes current positioning decisions time-sensitive. The informational inflection point, the moment when the binary outcome becomes clear, is approaching rapidly.

Alpine Macro’s contrarian call is a thesis, not a certainty

The logical chain is clean: if Hormuz opens, oil falls, inflation moderates, the Fed holds, and bonds rally. The Alpine Macro trade works across both fixed income and equities under that sequence. The barbell equity positioning and the long-duration bond entry compound the return if the scenario materialises.

That chain depends on a 50% probability event. Investors sizing this trade appropriately need to account for the mirror scenario in which conflict escalates and inflation embeds further into the rate structure. Position sizing, not conviction, is how a coin-flip thesis gets expressed responsibly.

Alpine Macro’s thesis horizon is 3-6 months: long enough for oil normalisation to flow through to yields, short enough to evaluate with specific, observable milestones along the way.

The value of the framework is not in predicting the outcome. It is in giving investors a structured set of indicators to monitor as the scenario develops, with defined entry levels, a clear timeline, and specific conditions under which the trade should be reconsidered.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.